1) In pure competition, if the market price of the product is initially higher than the

minimum average cost of the firms, then:

A.Some firms will exit the industry and the industry supply will decrease

B.Other firms will enter the industry and the industry supply will increase

C.Some firms will exit the industry and the industry supply will increase

D.Other firms will enter the industry and the industry supply will decrease

2) Capitalist income (corporate profits, interest, and rent) has:

A.declined sharply since 1900 because of the growing strength of labor unions.

B.remained approximately constant since 1900.

C.increased significantly because of rising rents.

D.fallen since 1900 because of the declining importance of corporations.

3) In a two-nation, two-good world, if country A has the comparative advantage in

producing good X over country B, then country A:

A.Should not trade with country B

B.Could have the comparative advantage in producing the other good Y as well

C.Must have the comparative disadvantage in producing the other good Y

D.Can produce good X with fewer resources than country B

4) The marginal revenue product of an economic resource for a firm operating in purely

competitive product and resource markets:

A.Is the marginal product of the resource divided by the price of the final product

B.Is the increase in total revenue resulting from the addition of one more unit of the

resource

C.Is equal to the average revenue product at the lowest point of the average revenue

product curve

D.Decreases as the quantity of output decreases

5) Sales and excise taxes are levied on retailers, but retailers add these taxes to the

prices of their products. This illustrates the:

A.equal sacrifice theory of taxation.

B.shifting of taxes to consumers.

C.ability-to-pay principle of taxation.

D.benefits-received principle of taxation.

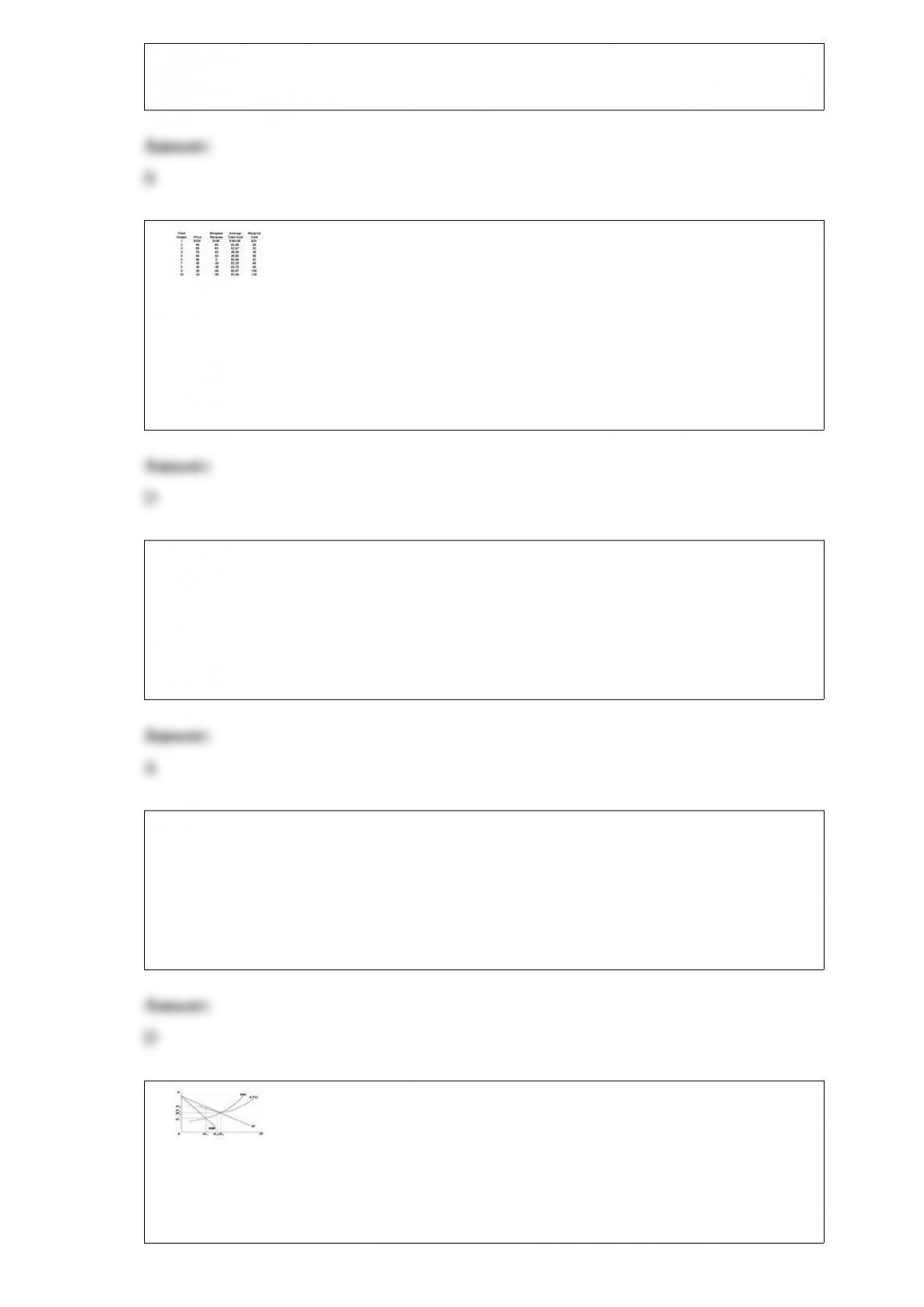

6)

Refer to the data. At its profit-maximizing output, this firm’s total revenue will be:

A.$300.

B.$198.

C.$180.

D.$280.

7) The long-run total demand for commodity resources is driven by which of the

following forces?

A.Rising number of people alive and an increasing amount of consumption per person

B.Stable number of people alive and an increasing amount of consumption per person

C.Rising number of people alive and a stable amount of consumption per person

D.Rising number of people alive and a decreasing amount of consumption per person

8) If you operated a small bakery, which of the following would be a variable cost in

the short run?

A.Baking ovens.

B.Interest on business loans.

C.Annual lease payment for use of the building.

D.Baking supplies (flour, salt, etc.).

9)

Refer to the above graph for a pure monopoly. A profit-maximizing monopolist would

set what price and quantity levels in the short run?

A.P1 and Q1

B.P2 and Q3

C.P3 and Q2

D.P4 and Q1

10) In which industry is monopolistic competition most likely to be found?

A.Utilities

B.Agriculture

C.Retail trade

D.Mining

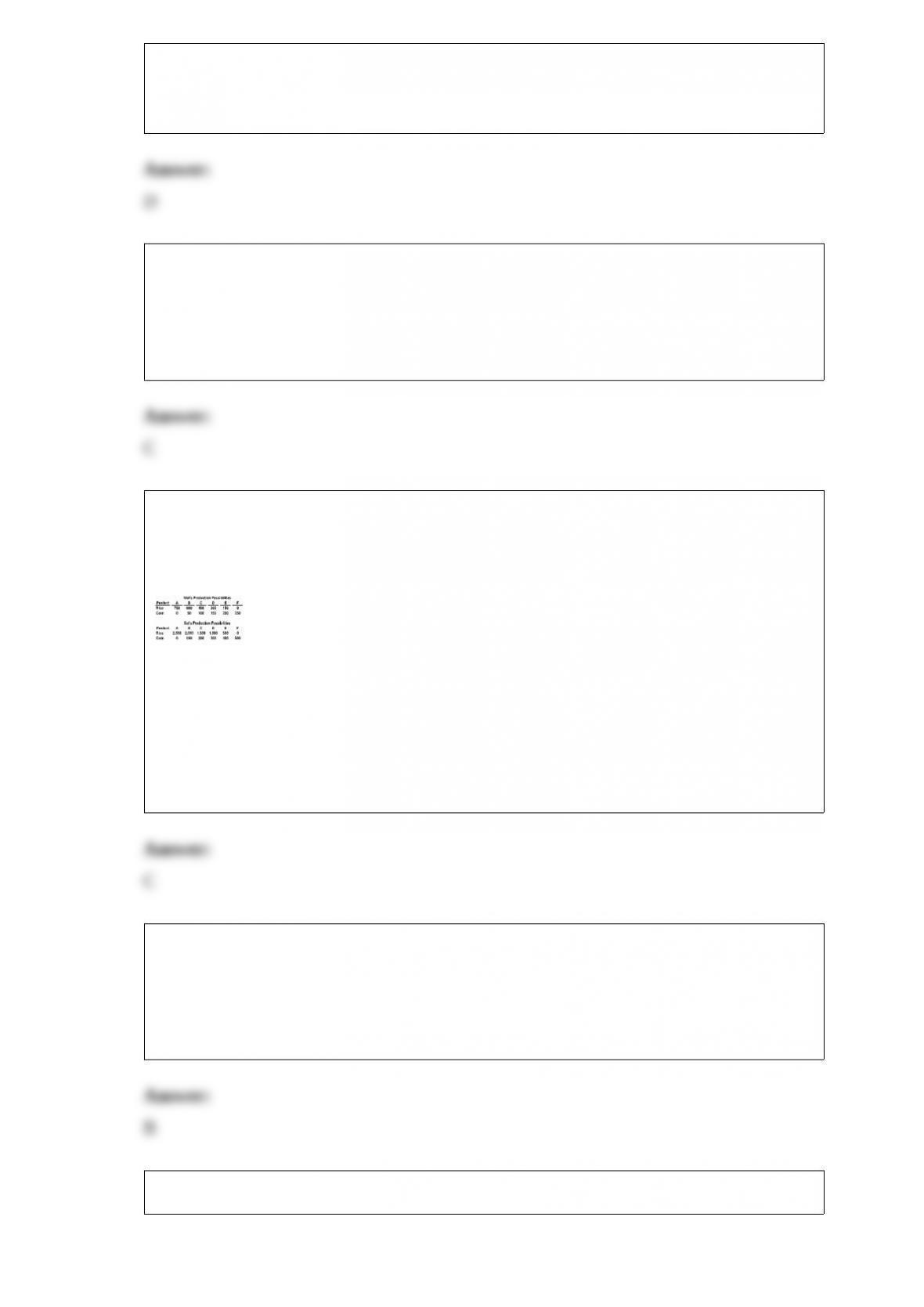

11) Answer the following question based on the data provided in the tables below for

two hypothetical nations, Wat and Xat. The nations have the production possibilities for

rice and corn given in the following table:

Refer to the data above. Which of the following statements about the two nations is

correct based on the principle of comparative advantage?

A.Xat should specialize in the production of corn

B.Wat should specialize in the production of rice

C.Xat has a comparative advantage in the production of rice

D.Xat has a comparative advantage in the production of corn

12) The difference between income and wealth is that income:

A.Is accumulated, while wealth is earned

B.Refers to a flow of earnings, while wealth is the stock of assets one has

C.Is measured at a point in time, while wealth is measured over a period of time

D.May not be in cash, while wealth is in cash

13)

In reality, the wage-gap between two countries will:

A.Always be reduced to zero through migration

B.Be greater than zero because of migration costs

C.Always be sufficient to cover the marginal costs of migration

D.Be smaller the greater the distance between the countries

14) If a buyer who wants product A is required by the seller to buy its products B and C

as well, this is called:

A.An exclusive contract

B.Profit maximization

C.Competitive pricing

D.A tying contract

15) Geographic immobility in the labor force results in:

A.Homogeneous wage rates

B.Homogeneous unemployment rates

C.Local labor markets which reach equilibrium quickly and efficiently

D.Persistent wage and unemployment differentials in different regions of the country

16) Which of the following is an example of voter failure?

A.Voters support adding stop lights that would increase congestion and travel costs

without increasing safety or convenience.

B.Government officials ignore voter calls for regulations that would reduce negative

externalities and enhance efficiency.

C.Voters wanting greater highway safety are unable to express their preferences on how

to achieve it because the voting system doesn’t allow it.

D.Voters wanting more government services are divided on what services they most

prefer, leaving government officials to determine what is best.

17) Competitive firms will always try to earn more than a normal profit by doing the

following, except:

A.Adopting better production technology

B.Improving their business organization and operation

C.Developing new products

D.Raising the prices of their existing products

18) The “coincidence of wants” problem associated with barter refers to the fact that:

A.for exchange to occur, each seller must have a product that some buyer wants.

B.money must be used as a medium of exchange or trade will never occur.

C.specialization is restricted by the size or scope of a market.

D.buyers in resource markets and sellers in product markets can never engage in

exchange.

19)

Refer to the figure above, which shows four different Lorenz curves (I, II, III, and IV).

Which point would indicate that the top 40% of households earned 60% of the nation’s

total income?

A.a

B.b

C.d

D.e

20) The following table contains hypothetical data for the U.S. balance of payments in a

year. Answer the following question on the basis of these data. All figures are in billions

of dollars.

U.S. goods exports +$390

U.S. goods imports -498

U.S. service exports +133

U.S. service imports -107

Net investment income +12

Net transfers -22

Capital account -5

Foreign purchases of U.S. assets +156

U.S. purchases of foreign assets -59

Refer to the table above. What does the figure for net investment income indicate?

A.Americans invested more abroad than the amount foreigners invested in the U.S.

B.The size of the net inflow of foreign investment to the United States in that year

C.The net amount Americans received as interest and dividends on existing American

investments abroad

D.The net amount Americans paid as interest and dividends on existing foreign

investments in the United States