In the United States, payments to labor account for:

A) 70% of total income, a share that has not fluctuated much in the past 30 years.

B) 50% of total income, but the returns to land have been increasing.

C) only 30% of total income, and this number is falling.

D) 90% of income and can be broken down into human capital and physical capital.

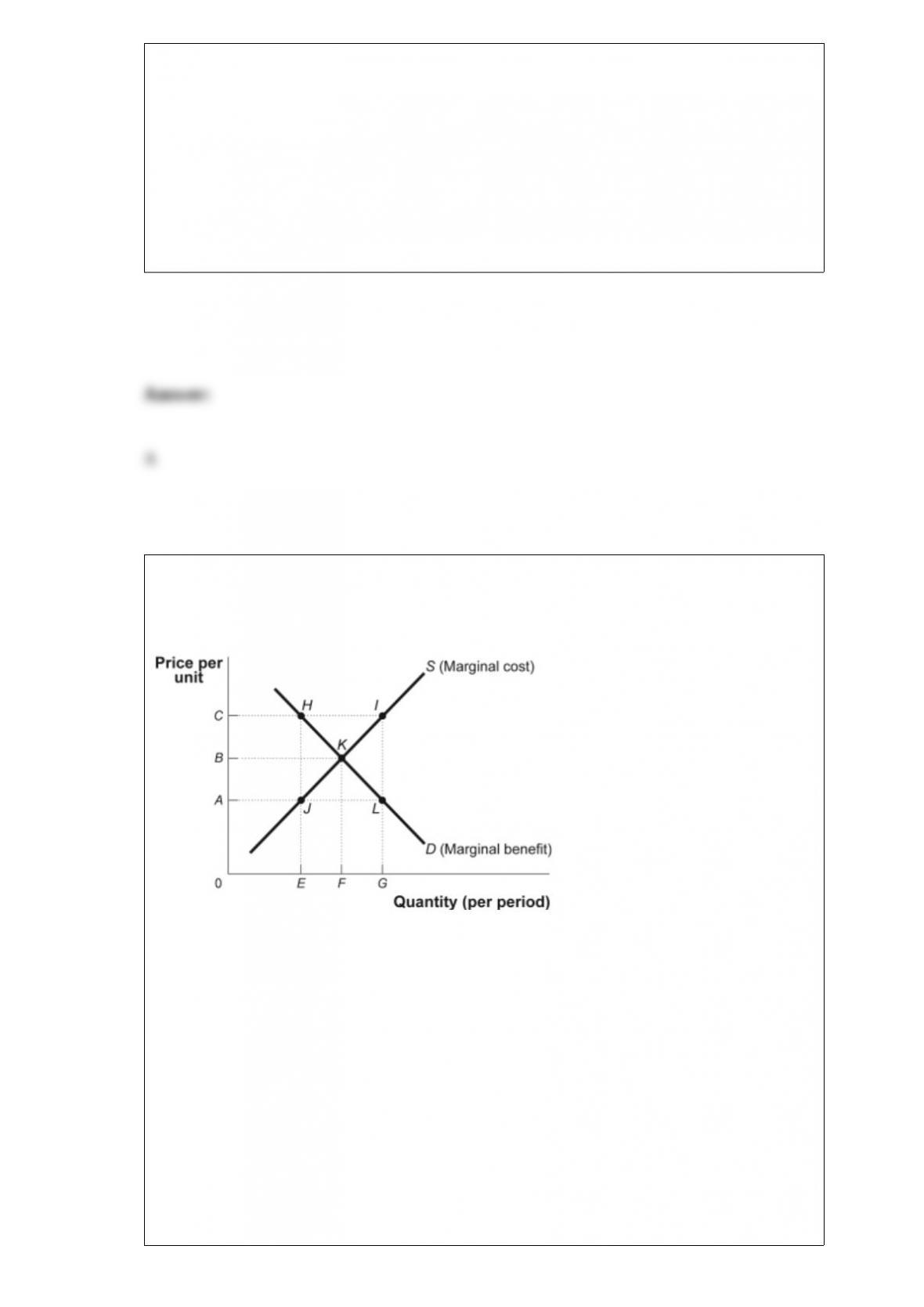

Figure: Market Failure

(Figure: Market Failure) Look at the figure Market Failure. Suppose the supply curve

represents the marginal cost of providing streetlights in a neighborhood that is

composed of two people, Ann and Joe. The demand curve represents the marginal

benefit that Ann receives from the streetlights. Suppose that Joe’s marginal benefit from

the streetlights is a constant amount equal to AC. The market would provide _____

streetlights. The efficient quantity of streetlights is _____.

A) 0; F

B) F; F

C) E; F

D) F; G

The private market will lead to _____ of clean air because _____.

A) too little consumption; it is nonexcludable but rival in consumption

B) too much consumption; it is nonexcludable but rival in consumption

C) production of the socially optimal amount; the marginal cost is zero

D) government provision; it is a public good

Which of the following taxes best illustrates the benefits principle of tax fairness?

A) The local city playground is funded through a tax on all citizens.

B) Roads and highways are built and maintained through revenue from a tax on

gasoline.

C) A property tax that is proportional to the value of the home is charged to

homeowners to fund primary and secondary education.

D) A sales tax on food pays for police and fire protection.

Economists use models to explain real-life situations because:

A) such models tend to be exactly what is occurring in each situation.

B) assumptions found in such models tend to make analyzing the situation more

difficult.

C) simplifications and assumptions often yield results that can help to explain the more

difficult real-life situations.

D) real-life situations are not relevant to the building of models.

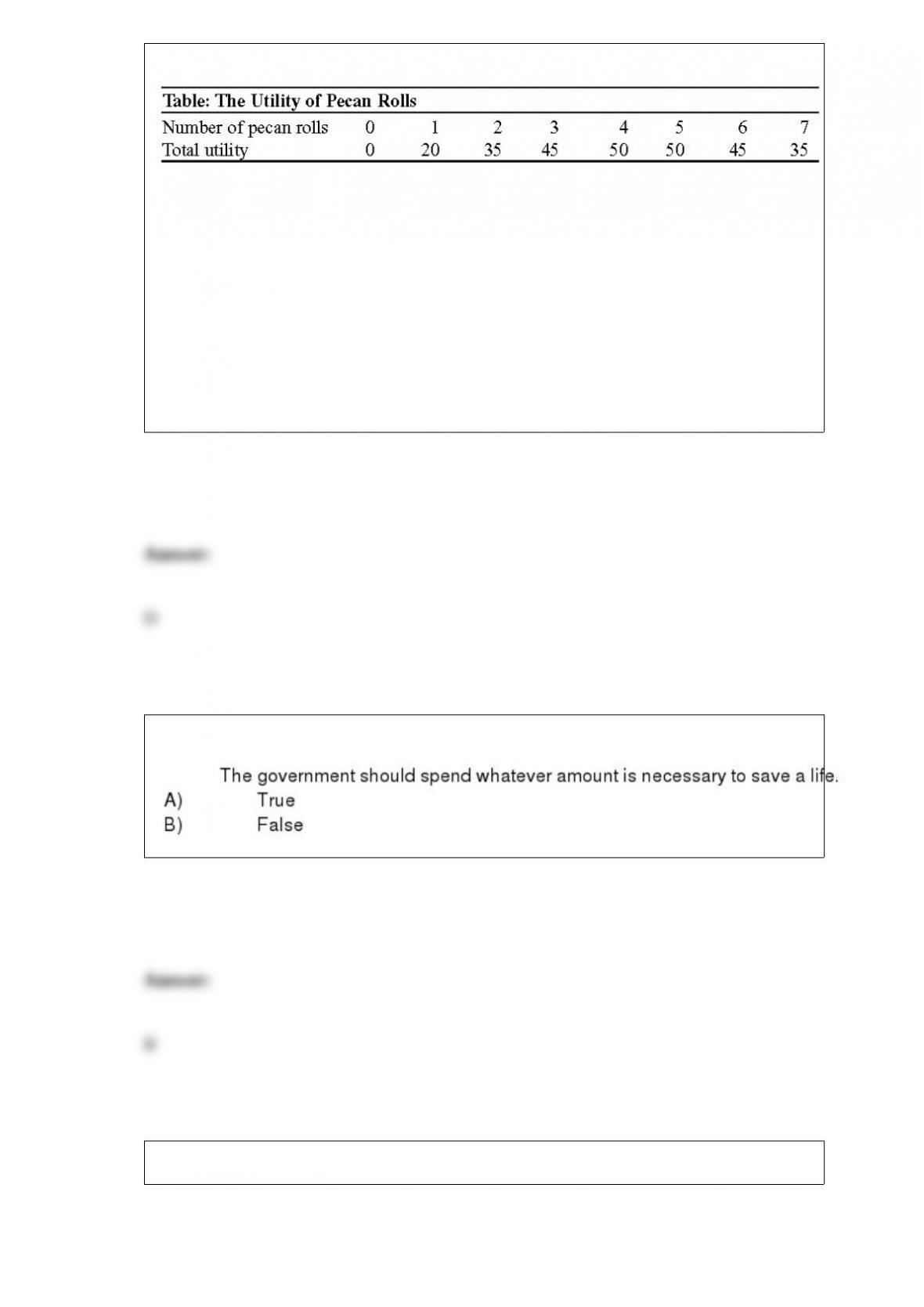

(Table: The Utility of Pecan Rolls) Look at the table The Utility of Pecan Rolls.

Marginal utility becomes negative at the _____ roll.

A) first

B) second

C) fifth

D) sixth

Assume that diminishing marginal utility applies to both slippers and tutus and that

Natasha is spending all of her income. If Natasha purchases a combination of ballet

slippers and tutus such that MUSlippers / PSlippers = 20 and MUTutus / PTutus = 5, to

maximize utility, Natasha should buy _____ slippers and _____ tutus.

A) more; fewer

B) fewer; more

C) more; more

D) fewer; fewer

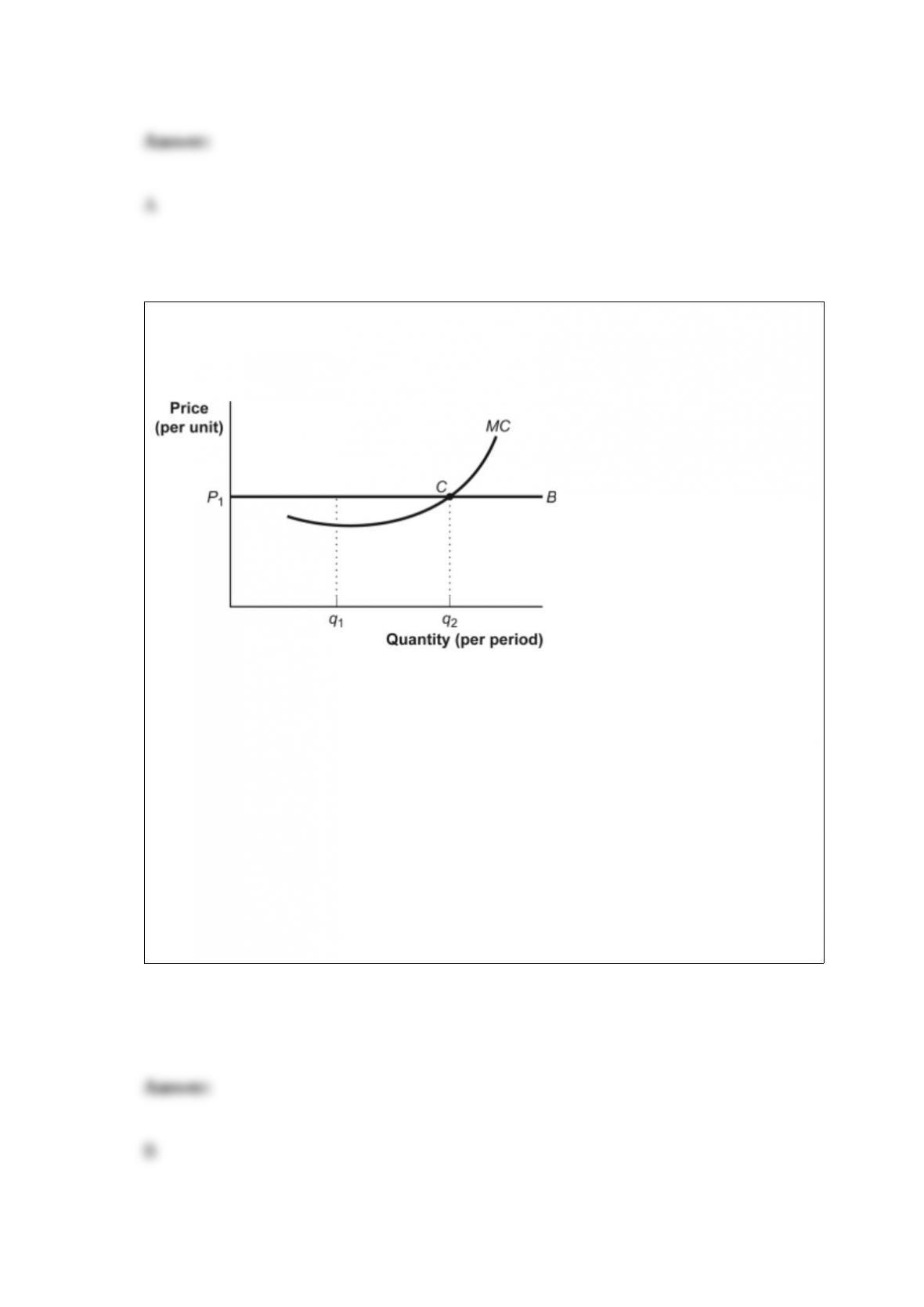

Figure: The Marginal Decision Rule

(Figure: Marginal Decision Rule) Look at the figure The Marginal Decision Rule. As

long as the price is above the minimum variable cost, this firm should produce quantity

_____ where _____ equals _____ to maximize economic profit.

A) q1; MR; MC

B) q2; price; MC

C) q2; MR; TR

D) q1; TR; TC

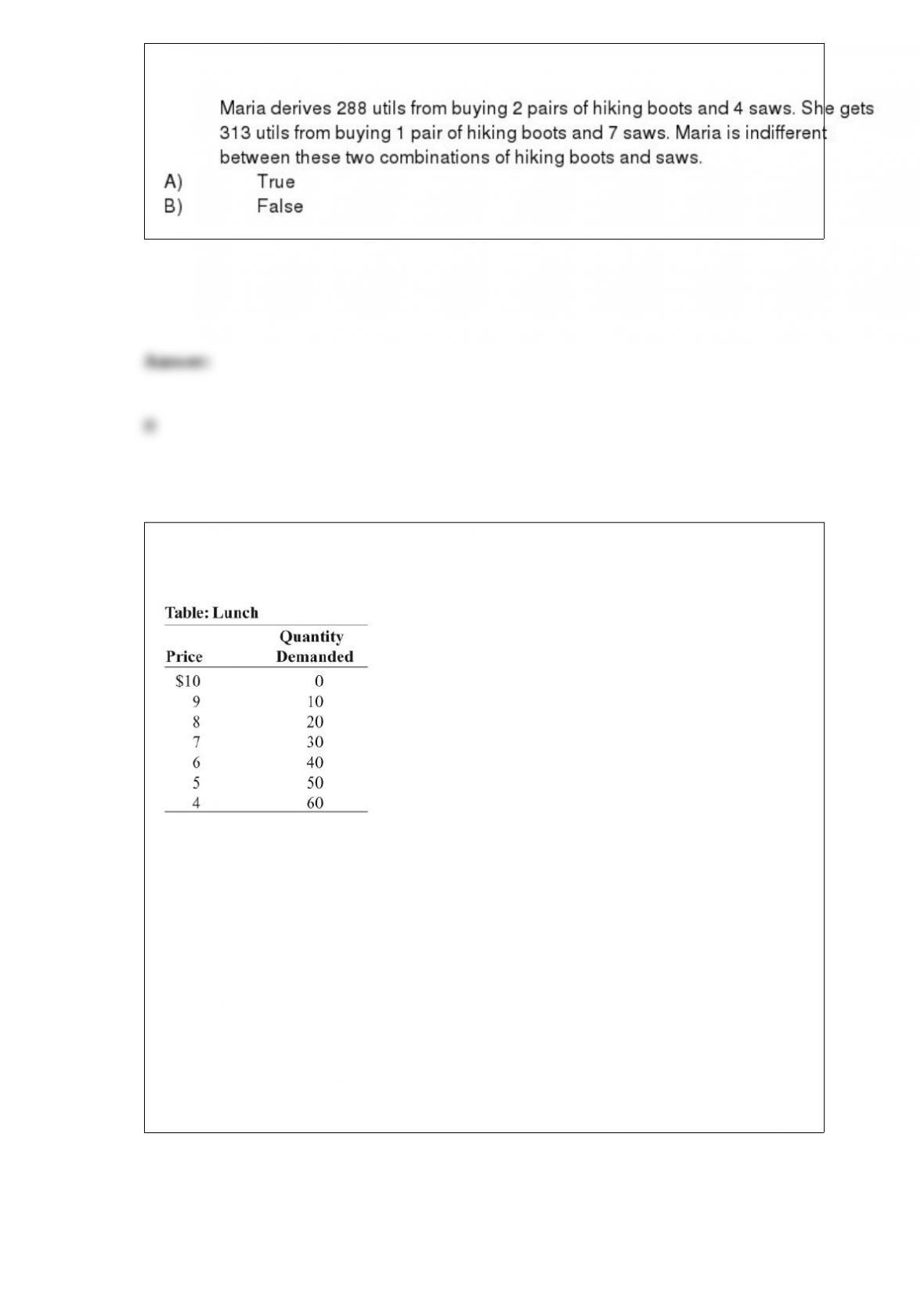

(Table: Lunch) Look at the figure Lunch. Joe makes and sells picnic lunches to people

taking all-day rafting trips on the river. The marginal cost and average cost of each

lunch are a constant $4. If Joe is a monopolist, what price will he charge for a lunch in

the long run?

A) $9

B) $7

C) $5

D) $3

When a firm produces a small amount of output, the spreading effect:

A) is stronger than the diminishing returns effect.

B) is weaker than the diminishing returns effect.

C) and diminishing returns effect are equal.

D) is zero.

Monopolistic competitors sell products that are _____ and as a result, each firm has a

_____ demand curve.

A) imperfect substitutes; downward-sloping

B) perfect substitutes; horizontal

C) imperfect substitutes; horizontal

D) perfect substitutes; downward-sloping

Along a given downward-sloping demand curve, an increase in the price of a good will

_____ consumer surplus.

A) increase

B) decrease

C) not change

D) The answer cannot be determined without information about the supply curve.

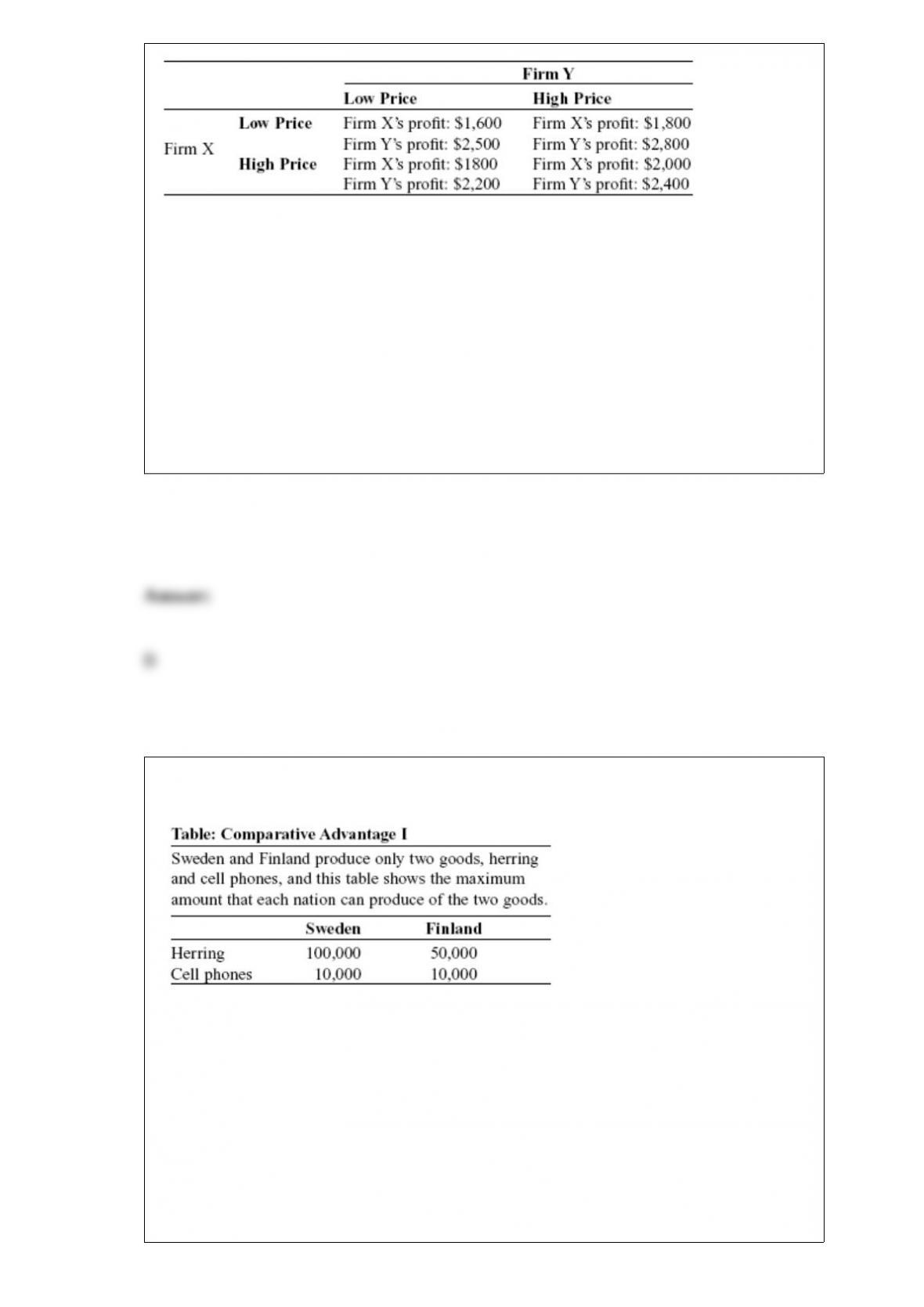

Scenario: Payoff Matrix for Firms X and Y

The following payoff matrix depicts the profits for the only two firms in this

oligopolistic industry.

(Scenario: Payoff Matrix for Firms X and Y) In the scenario Payoff Matrix for Firms X

and Y, if firm Y were to choose its dominant strategy, it would:

A) choose a low price.

B) choose a high price.

C) encounter a dilemma, since there are two dominant strategies.

D) allow firm X to dominate the industry.

(Table: Comparative Advantage I) Look at the table Comparative Advantage I. The

opportunity cost of producing 1 box of herring for Sweden is _____ box(es) of cell

phones.

A) 10

B) 0.5

C) 5

D) 0.1

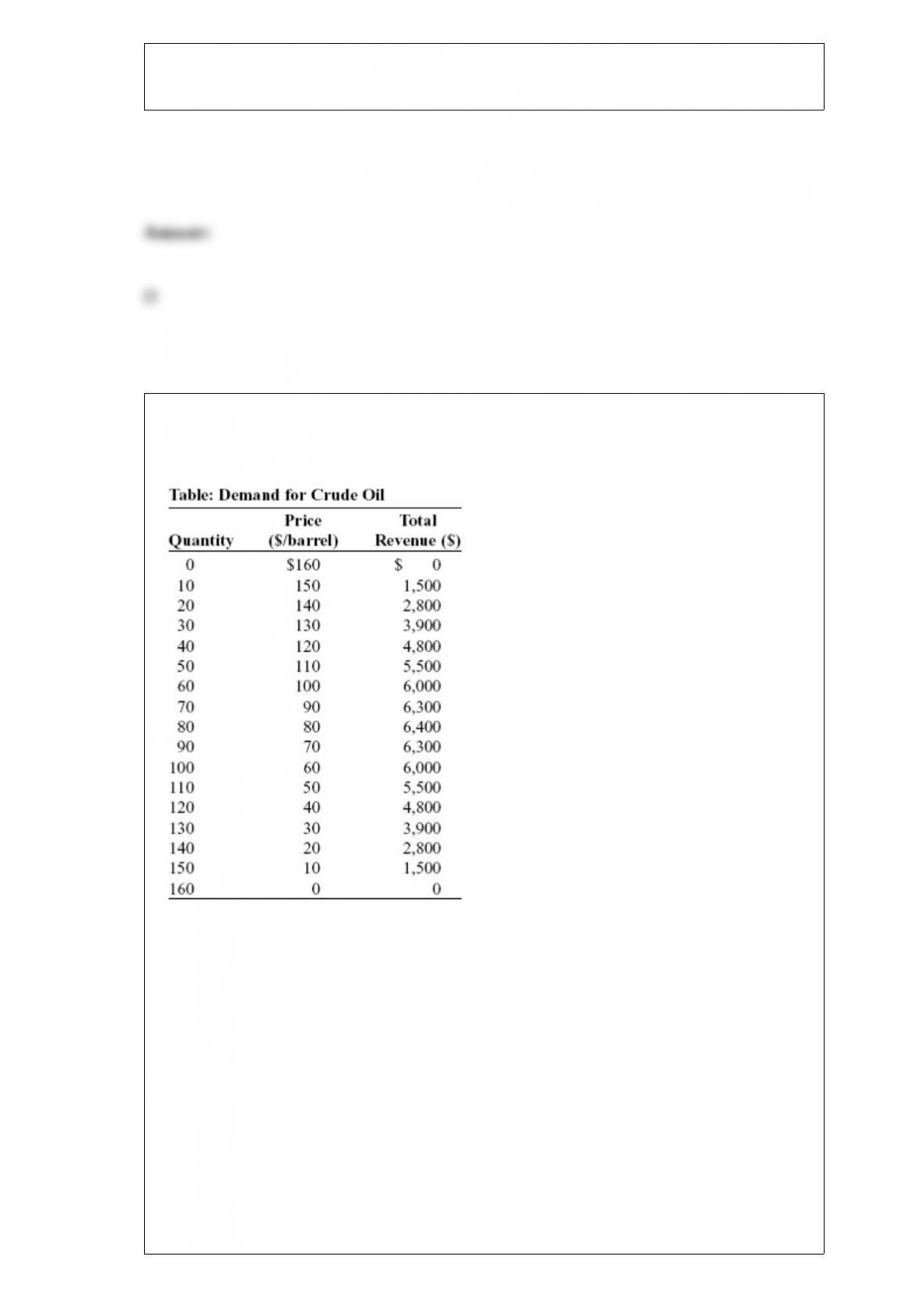

(Table: Demand for Crude Oil) Look at the table Demand for Crude Oil. For simplicity,

assume that the marginal cost of producing crude oil is zero. There are only two

producers of crude oil, and they cannot cooperate. But they play this game every week,

each player has a tit-for-tat strategy, and the other player knows this. When both firms

use a tit-for-tat strategy, firm 1 will produce _____ barrels, and firm 2 will produce

_____ barrels.

A) 40; 40

B) 40; 50

C) 50; 50

D) 30; 30

In perfect competition, the profit-maximizing level of output occurs where the:

A) MR = MC above minimum AVC.

B) price < marginal cost above minimum AVC.

C) MR > MC below minimum AVC.

D) P = MR above MC.

If a California avocado stand operates in a perfectly competitive market, that stand

owner will be a price:

A) maker.

B) taker.

C) discriminator.

D) maximizer.

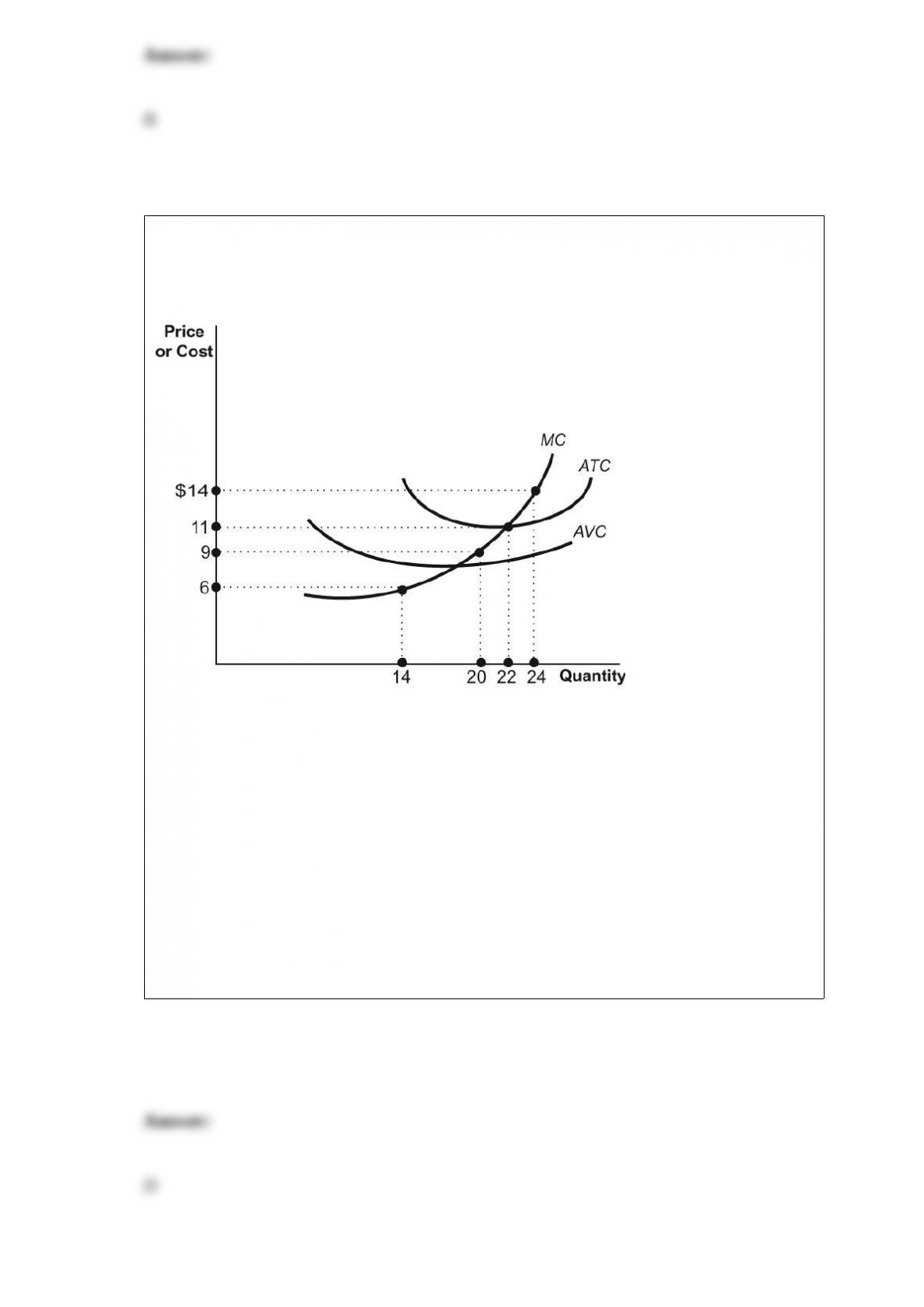

Figure: Game-Day Shirts

(Figure: Game-Day Shirts) Rick is one of 10 vendors who sell game-day T-shirts at

football games in a perfectly competitive market. His costs are identical to the costs of

the other 9 vendors. If the price of a shirt is $14, the short-run industry supply will be

_____ shirts.

A) 140

B) 200

C) 220

D) 240

The market price of airline flights increased recently. Some economists suggest that the

price increased because jet fuel is much more expensive than before. As a result, they

believe that in the market for flights:

A) supply increased.

B) supply decreased.

C) demand increased.

D) demand decreased.

The effect of an increase in productive inputs such as labor and capital can be shown

by:

A) a point inside of the production possibility frontier.

B) an outward shift of the production possibility frontier.

C) a movement from one point to another along the production possibility frontier.

D) an inward shift of the production possibility frontier.

In economic analysis, the principle of marginal analysis refers to:

A) dividing large problems into smaller, more manageable ones.

B) the notion that a group’s problems can be effectively analyzed by focusing on only a

small subsample of the group.

C) the result that the optimal quantity of an activity is that at which marginal benefit is

equal to marginal cost.

D) the result that the optimal quantity of an activity is that at which the net benefit of

the representative, or marginal, individual is maximized.

Long-run equilibrium in perfect competition and in monopolistic competition are

similar because in both models, firms:

A) produce at the minimum point of the average total cost curve.

B) set price equal to marginal cost.

C) make zero economic profits.

D) have excess capacity.

When adverse selection occurs, healthy people pay premiums that are _____ their

actual health care costs.

A) higher than

B) equal to

C) less than

D) positively correlated to

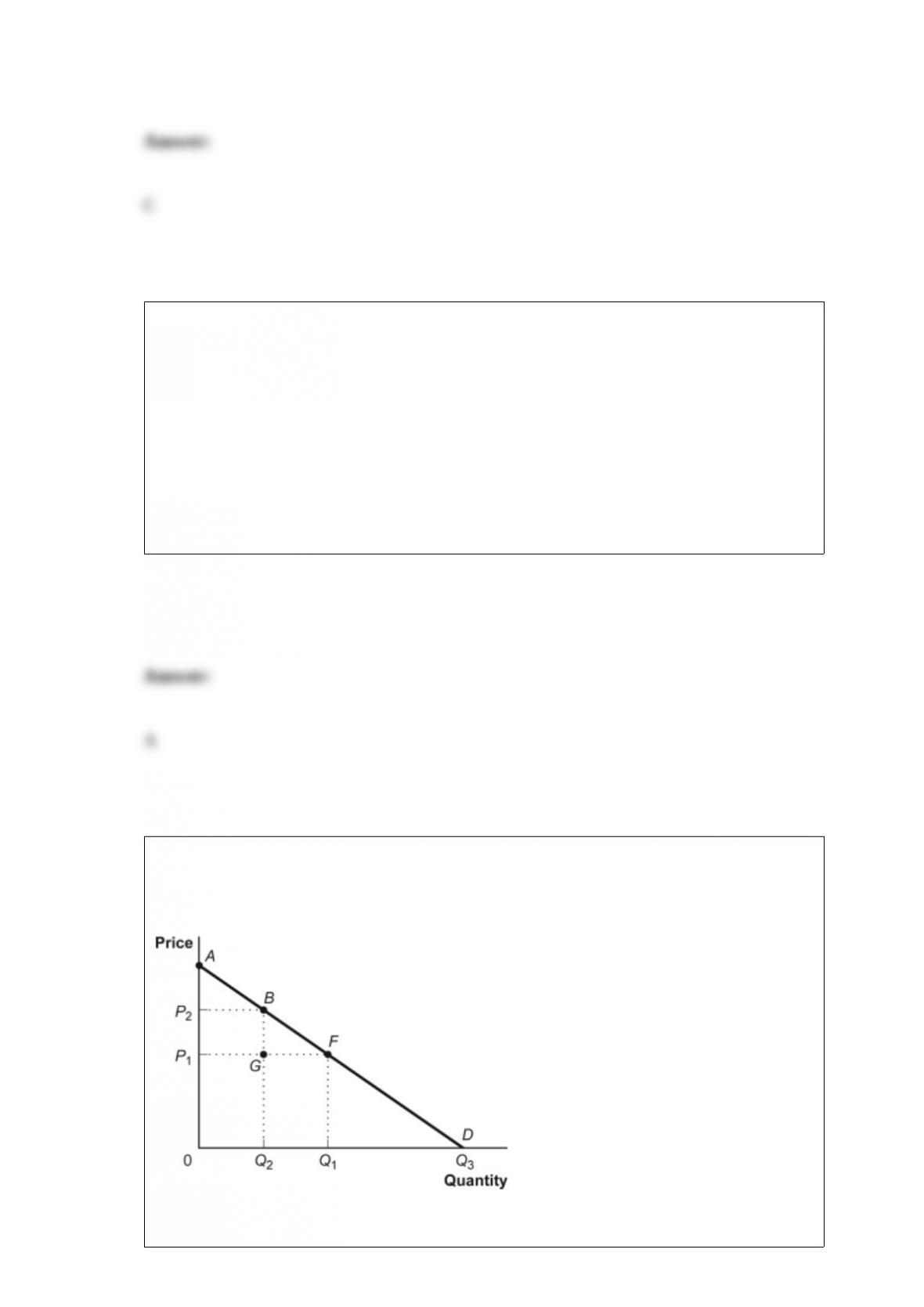

Figure: Consumer Surplus I

(Figure: Consumer Surplus I) Look at the figure Consumer Surplus I. If the price falls

from P2 to P1, consumer surplus increases by the area:

A) ABP2.

B) AFP1.

C) BGF.

D) P1P2BF.

Tacit collusion is difficult to achieve in practice:

A) the larger the number of firms in the industry.

B) the fewer the number of products being sold.

C) the more similar the marginal costs of each firm.

D) if customers have little or no bargaining power.

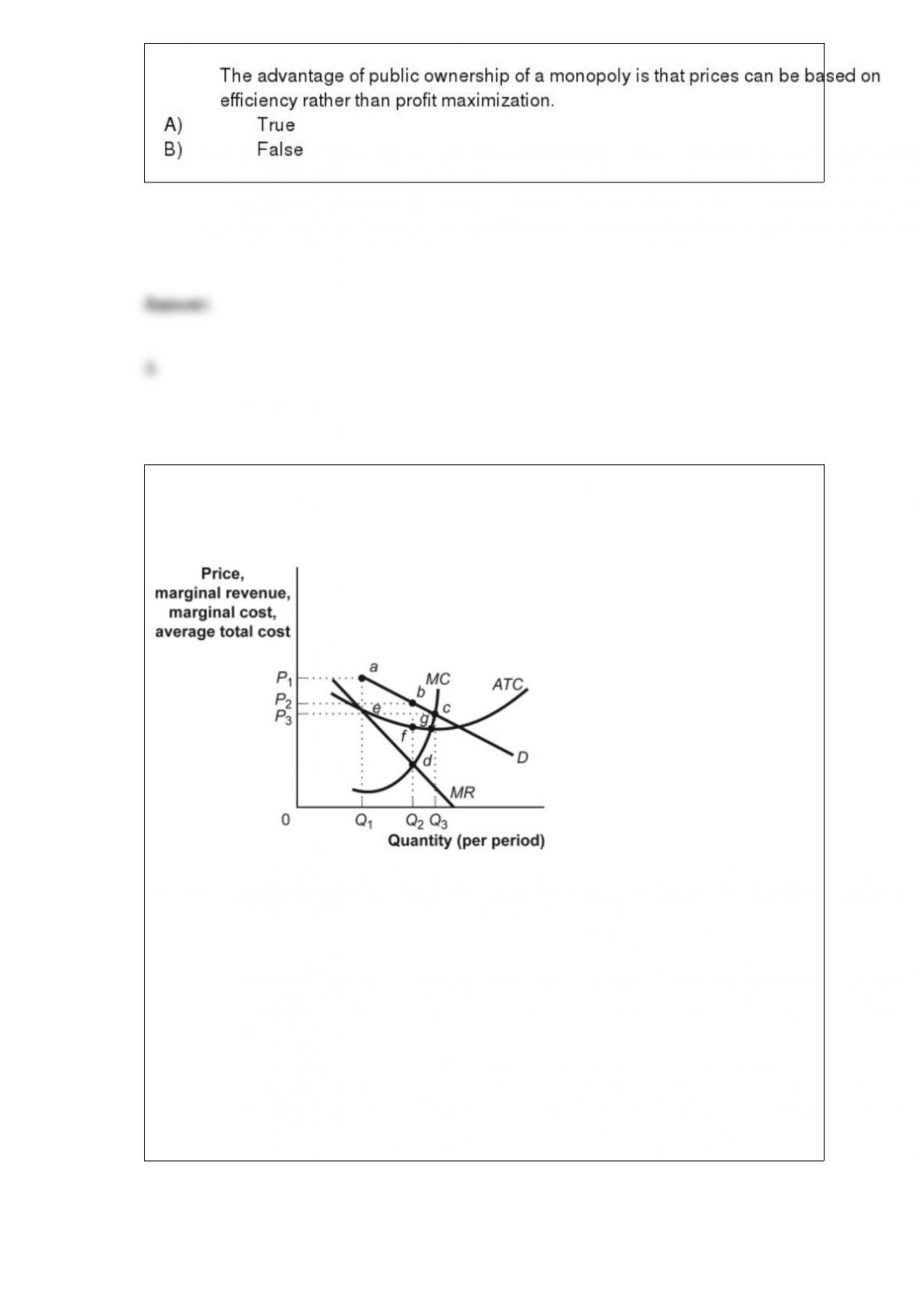

Figure: The Restaurant Market

(Figure: The Restaurant Market) The figure The Restaurant Market shows curves facing

a typical restaurant. Assume that many firms, differentiated products, and easy entry

and exit characterize the restaurant market. If the restaurant shown here were to raise its

price above the profit-maximizing price, its total revenue would:

A) decrease.

B) increase.

C) not change.

D) Not enough information is given to answer the question.

Suppose purchases do not occur because the value of the good to the potential seller

exceeds the value to a potential consumer. This situation will occur in:

A) a market dominated by government regulation.

B) well-functioning markets.

C) a market made up of many buyers and sellers.

D) a centralized market system.