If the cross elasticity of demand between goods A and B is positive, then

A) the demands for A and B are both price elastic.

B) the demands for A and B are both price inelastic.

C) A and B are complements.

D) A and B are substitutes.

E) A and B are independent goods.

A very small country is an international borrower and its demand for loanable funds

increases. As a result, the equilibrium quantity of loanable funds used in the country

________ and the country’s foreign borrowing ________.

A) does not change; increases

B) does not change; does not change

C) increases; increases

D) increases; does not change

E) increases; decreases

The long-run aggregate supply curve is

A) vertical.

B) negatively sloped.

C) positively sloped but extremely steep.

D) almost flat.

E) positively sloped at low levels of real GDP and vertical at high levels of real GDP.

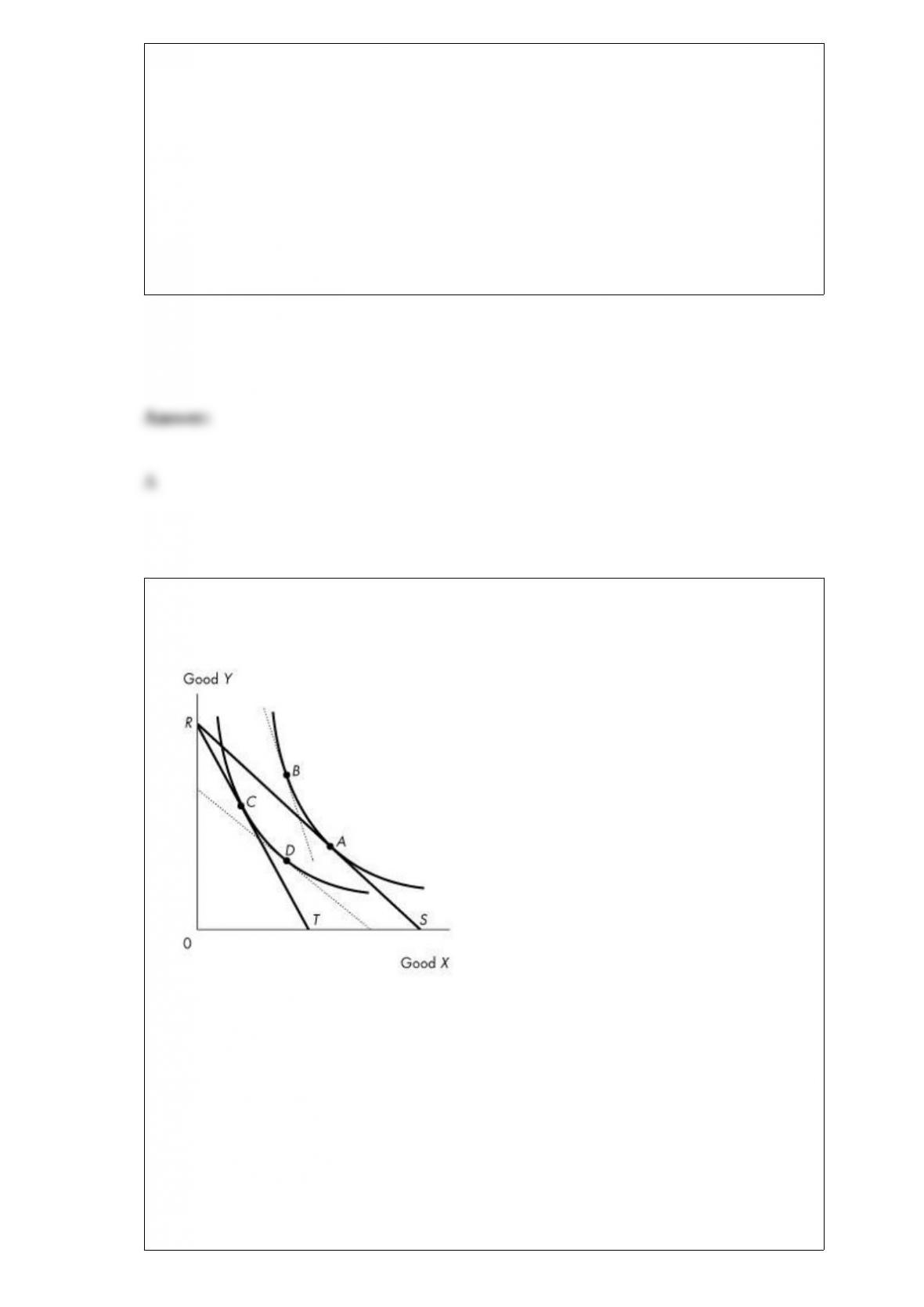

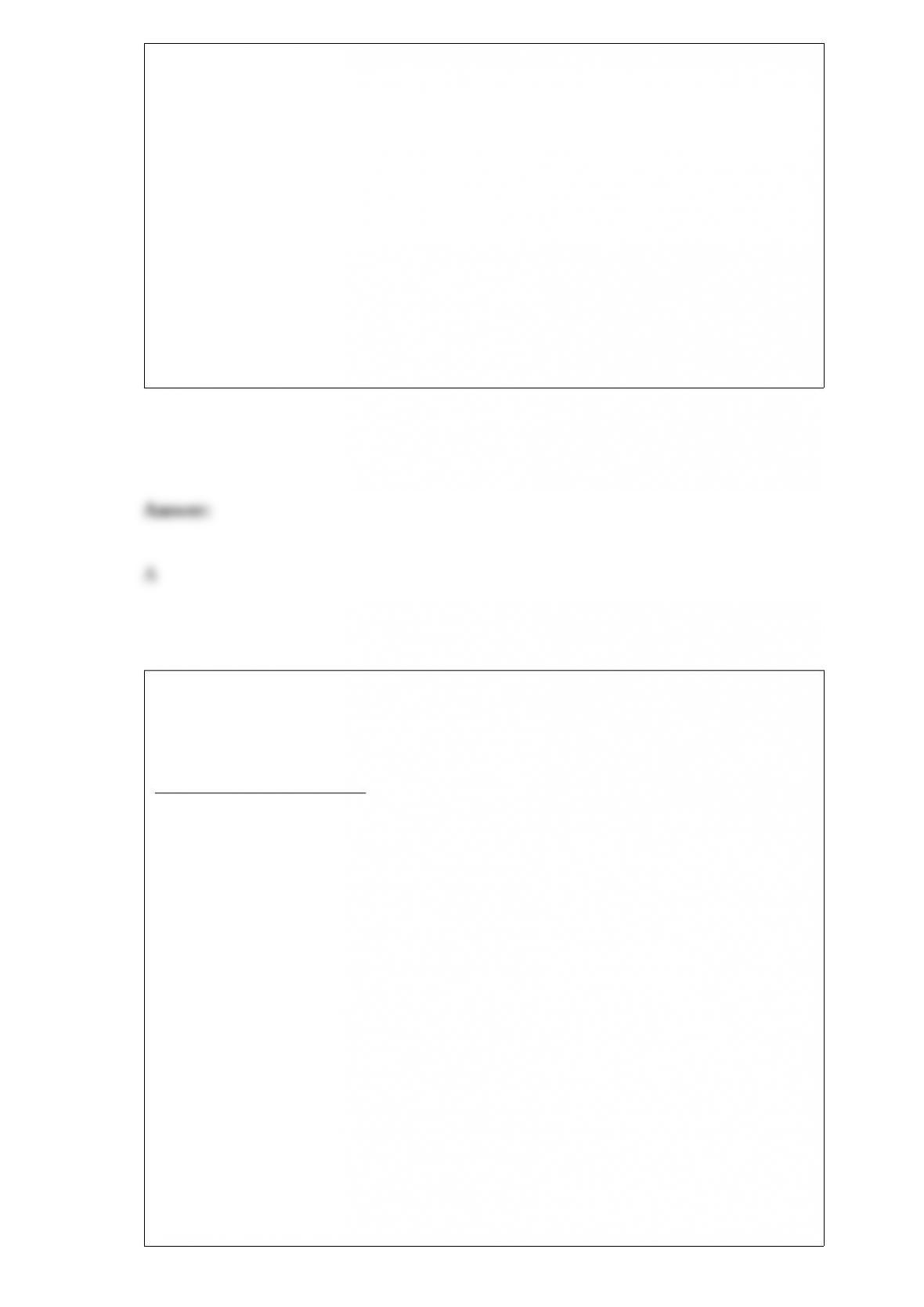

Use the figure below to answer the following questions.

Figure 9.3.3

Consider an initial budget line labelled RS in Figure 9.3.3. The budget line becomes RT

with

A) a rise in the price of good X.

B) a fall in the price of good X.

C) a rise in the price of good Y.

D) a decrease in the preference for good X.

E) an increase in real income.

Behavioural economics and neuroeconomics seek to achieve

A) the reason why we do not always make rational economic decisions.

B) a method of using willpower and self-interest to gain utility maximization.

C) a theory in which consumers are always utility-maximizers.

D) a new method for the human brain to work out rational choice.

E) the rational concepts that support the law of demand and the law of supply.

The quantity of a public good produced by private provision

A) is less than the efficient quantity.

B) is equal to the efficient quantity.

C) is greater than the efficient quantity.

D) maximizes total public benefit.

E) maximizes net public benefit.

In Table 3.5.4 potatoes and rice are

A) substitutes in Region 1 and complements in Region 2.

B) substitutes in Region 2 and complements in Region 1.

C) complements in both regions.

D) substitutes in both regions.

E) unrelated goods in both regions.

The Competition Act distinguishes between business practices that are criminal and

noncriminal. Which of the following is noncriminal?

A) conspiracy to fix prices

B) bid-rigging

C) resale price maintenance

D) false advertising

E) refusal to deal

Flora’s Flowers bought a new van last year for $10,000. It can now sell the van for

$8,500. To buy this year’s model of the same van it would have to pay $11,000. What is

the implicit rental rate using the car for one year at a zero percent interest rate?

A) $2,500

B) $3,500

C) $1,000

D) $10,000

E) $1,500

According to the quantity theory of money, an increase in the quantity of money will

increase the price level

A) but have no effect on real GDP or the velocity of circulation.

B) and increase real GDP and the velocity of circulation.

C) and increase real GDP but decrease the velocity of circulation.

D) and decrease real GDP and increase the velocity of circulation.

E) but have no effect on real GDP and will decrease the velocity of circulation.

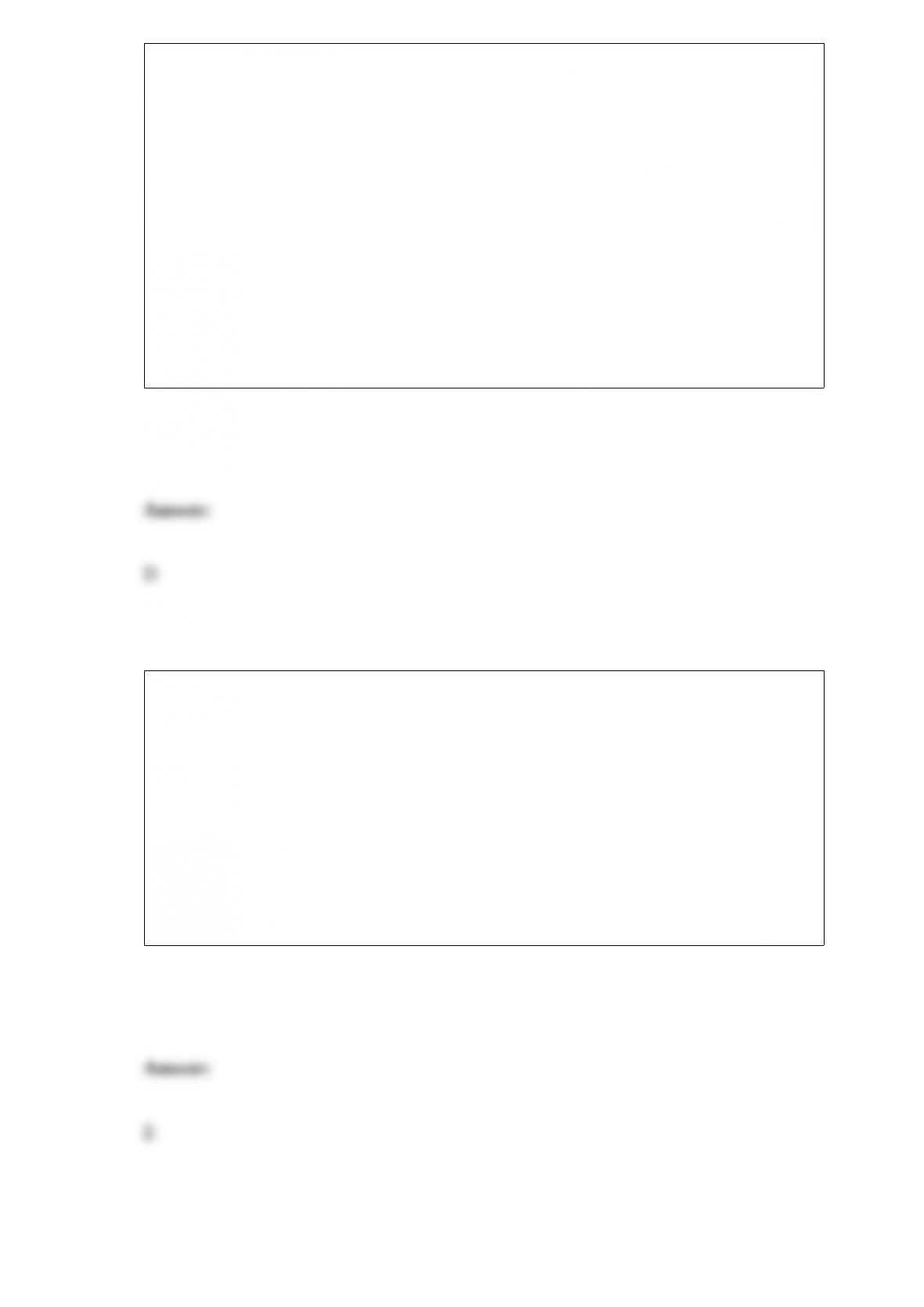

Refer to Figure 26.2.1. Which graph illustrates what happens when government

expenditure decreases?

A) (a) only

B) (b) only

C) (c) only

D) (d) only

E) Both (a) and (d)

A group of business people are having coffee. Which of the following quotations

describes economies of scale?

A) “The new production process we’ve installed uses less capital and labour than the old

one.”

B) “The new assembly line has higher capital costs, but the fall in workers’ hours has

lowered overall costs.”

C) “The costs of per-unit production have fallen dramatically as we have increased the

length of the production runs.”

D) “Despite the higher costs of negotiating the contracts, hiring the cleaning firm is

much cheaper than using our own staff.”

E) “The computer servicing people we have hired work very well as an integrated

problem-solving group.”

Which of the following statements about the Keynesian view of the macroeconomy is

incorrect?

A) Technological change is the most significant influence on both aggregate demand

and aggregate supply.

B) To achieve and maintain full employment, active help from fiscal policy and

monetary policy is required.

C) Expectations are based on “animal spirits.”

D) The money wage rate is extremely sticky in the downward direction so there is no

automatic mechanism for eliminating a recessionary gap.

E) Expectations are the most significant influence on aggregate demand.

The government sets a price floor for corn, which is above the equilibrium price of

corn. As a result

A) the market for corn is efficient.

B) a shortage of corn occurs.

C) consumer surplus is maximized.

D) a deadweight loss is created.

E) the sum of consumer surplus and producer surplus is maximized.

A person who has an absolute advantage in the production of all goods will

A) also have a comparative advantage in the production of all goods.

B) not be able to gain from specialization and trade.

C) produce all goods at the lowest opportunity cost.

D) not have a comparative advantage in the production of any goods.

E) have a comparative advantage in the production of only some goods and not others.

Nominal GDP is $1,800 and real GDP is $1,600. The GDP deflator is

A) 112.5.

B) 88.8.

C) 8.88.

D) 11.25.

E) 1125.

In the prisoners’ dilemma with players Art and Bob, each prisoner would be best off if

A) both prisoners confess.

B) both prisoners deny.

C) Art denies and Bob confesses.

D) Bob denies and Art confesses.

E) none of the above is done.

A movement along the aggregate production function is the result of a change in

A) capital.

B) technology.

C) the quantity of labour.

D) the interest rate.

E) the inflation rate.

If you increase your consumption of pop by one additional can a week, your marginal

benefit from this last can is $1.00. For you, the ________ this last can of pop is $1.00

A) price of

B) marginal cost of

C) value from

D) consumer surplus from

E) producer surplus

If real GDP is $800 million and aggregate labour hours are 20 million, labour

productivity is

A) $40 an hour.

B) $16,000 million.

C) $40 million.

D) $160 an hour.

E) $16 an hour.

Suppose a firm increases the quantity of labour employed from 5 to 6 workers, and as a

result, the firm’s total output increases from 100 units to 400 units. The marginal

product of the sixth worker is

A) 150 units.

B) 100 units.

C) 400 units.

D) 300 units.

E) 66.67 units.

Whenever desired reserves exceed actual reserves, the bank

A) can make new loans.

B) will call in loans.

C) will go out of business.

D) is in a profit-making position.

E) has excess reserves.

A relative price is all of the following except

A) the ratio of one price to another.

B) an opportunity cost.

C) a quantity of a “basket” of goods and services forgone.

D) determined by demand and supply.

E) the lowest possible price available.

One difference between perfectly competitive markets and a single-price monopoly is

that

A) marginal revenue equals marginal cost for perfectly competitive firms, but not for

single-price monopolists.

B) marginal cost equals average variable cost for perfectly competitive firms but not for

single-price monopolists.

C) price equals minimum average total cost for single-price monopolists but not for

perfectly competitive firms.

D) marginal revenue equals price for perfectly competitive firms, but not for

single-price monopolists.

E) marginal revenue equals marginal cost for single-price monopolists but not for

perfectly competitive firms.

Junkfood Jill spends all of her income on jellybeans and Jolt cola. Suppose that Jill’s

income is $30, the price of a bag of jellybeans is $6, and the price of a bottle of Jolt cola

is $2. Which of the following combinations of jellybeans and Jolt cola lies inside Jill’s

budget line?

A) 2 bags of jellybeans and 8 bottles of Jolt

B) 5 bags of jellybeans and 0 bottles of Jolt

C) 4 bags of jellybeans and 4 bottles of Jolt

D) 3 bags of jellybeans and 6 bottles of Jolt

E) 5 bags of jellybeans and 15 bottles of Jolt

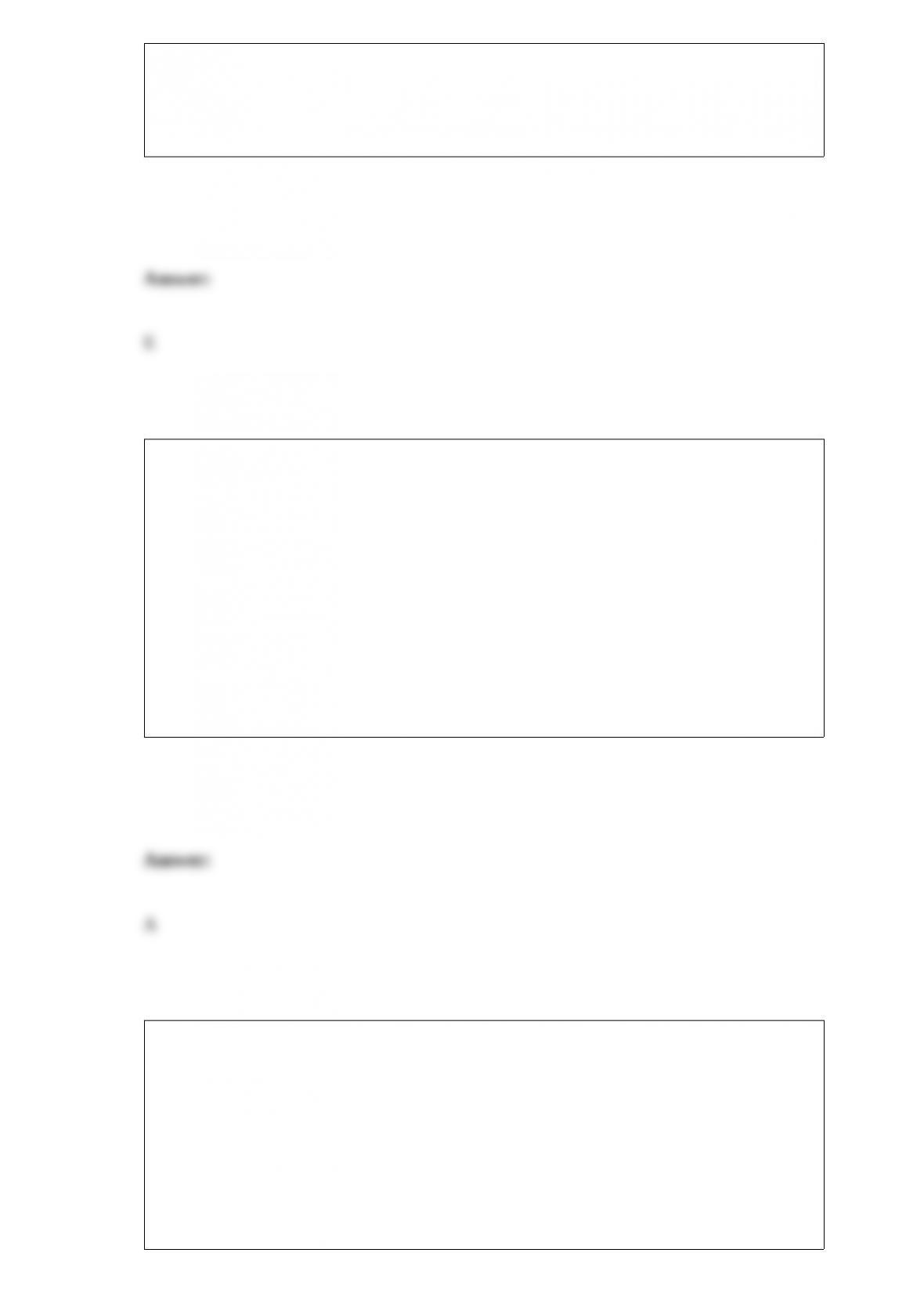

Consider the following information on cola sales by number of cases for a typical

university residence floor:

Temp. Price (dollars per case)

(C) 10.00 12.50 15.00 17.50

15 50 40 30 20

20 60 50 40 30

25 70 60 50 40

30 80 70 60 50

35 90 80 70 60

Refer to Figure 1A.4.5. Which line shows the relationship of cola sales and the

temperature when the price of a case is $15.00?

A) A

B) B

C) C

D) D

E) none of the above.

Capital is

A) the tools, instruments, machines, buildings, and other items that have been produced

in the past and that are used today to produce goods and services.

B) financial wealth.

C) the sum of investment and government expenditure on goods.

D) net investment.

E) gross investment.

Choose the correct statements about the real exchange rate.

1. The real exchange rate is a measure of how much of one money exchanges for a unit

of another money.

2. The real exchange rate is the value of the Canadian dollar expressed in units of

foreign currency per Canadian dollar.

3. The real exchange rate is the relative price of Canadian-produced goods and services

to foreign-produced goods and services.

4. The real exchange rate is a measure of the quantity of the real GDP of other countries

that we get for a unit of Canadian real GDP.

A) Statements 1 and 2 are correct.

B) Statements 2 and 4 are correct.

C) Statements 1 and 3 are correct.

D) Statements 3 and 4 are correct.

E) Statements 2 and 3 are correct.

A modified version of utilitarianism proposed by John Rawls could be summarized as

A) transfer everything to the poor.

B) transfer everything to the rich.

C) expand the size of government.

D) minimize the size of government.

E) make the poorest as well off as possible.

A monopolist under rate of return regulation has an incentive to

A) pad costs.

B) produce more than the efficient quantity of output.

C) charge a price equal to marginal cost.

D) maximize consumer surplus.

E) maximize shareholder profits

A difference between a quota and a tariff is that

A) a tariff generates a higher price than does an import quota.

B) a tariff generates a greater reduction in exports than does an import quota.

C) an import quota increases profits of domestic producers more than a tariff.

D) the government collects revenue from a tariff but does not collect revenue from an

import quota.

E) an import quota creates a social loss and a tariff does not.

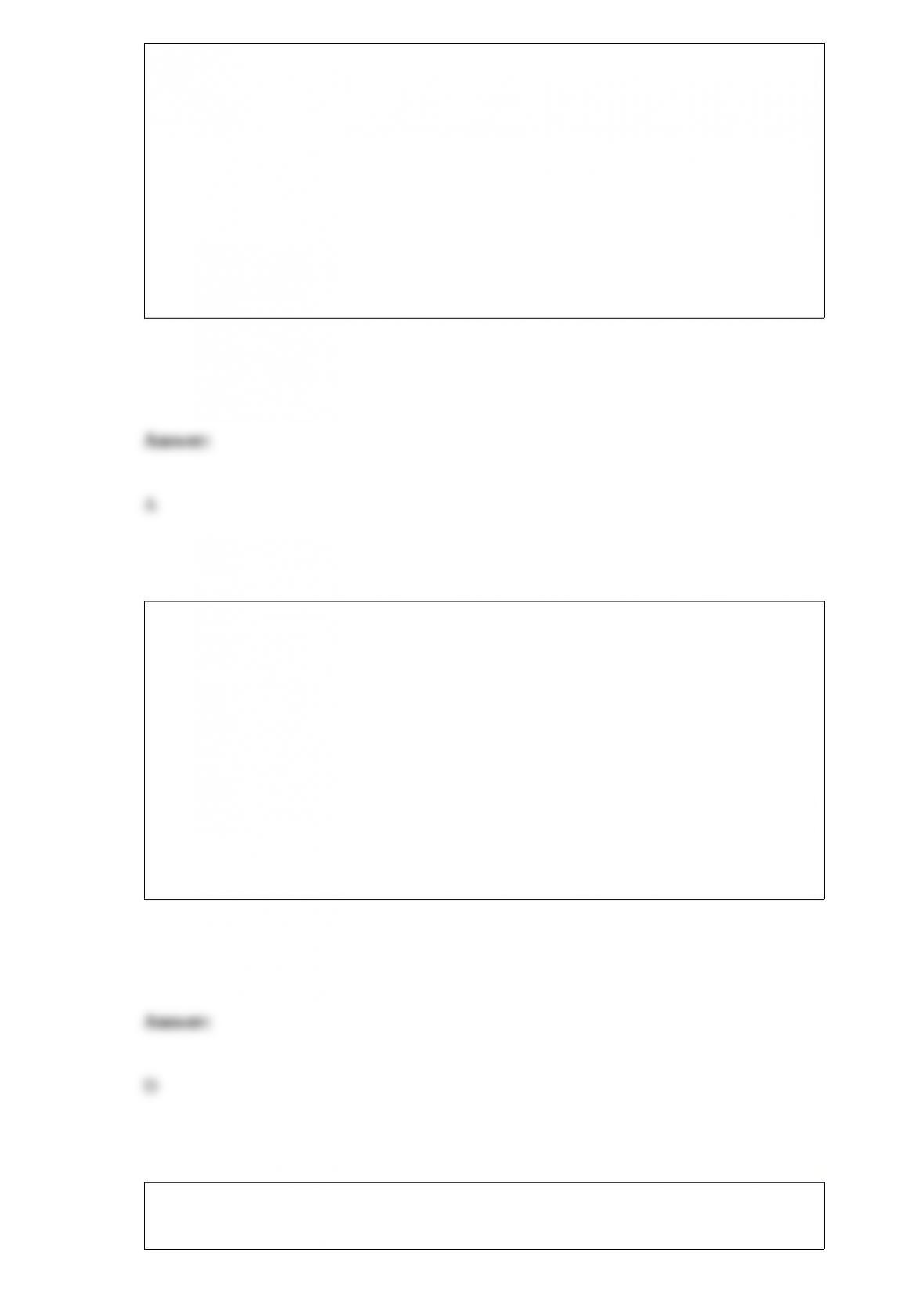

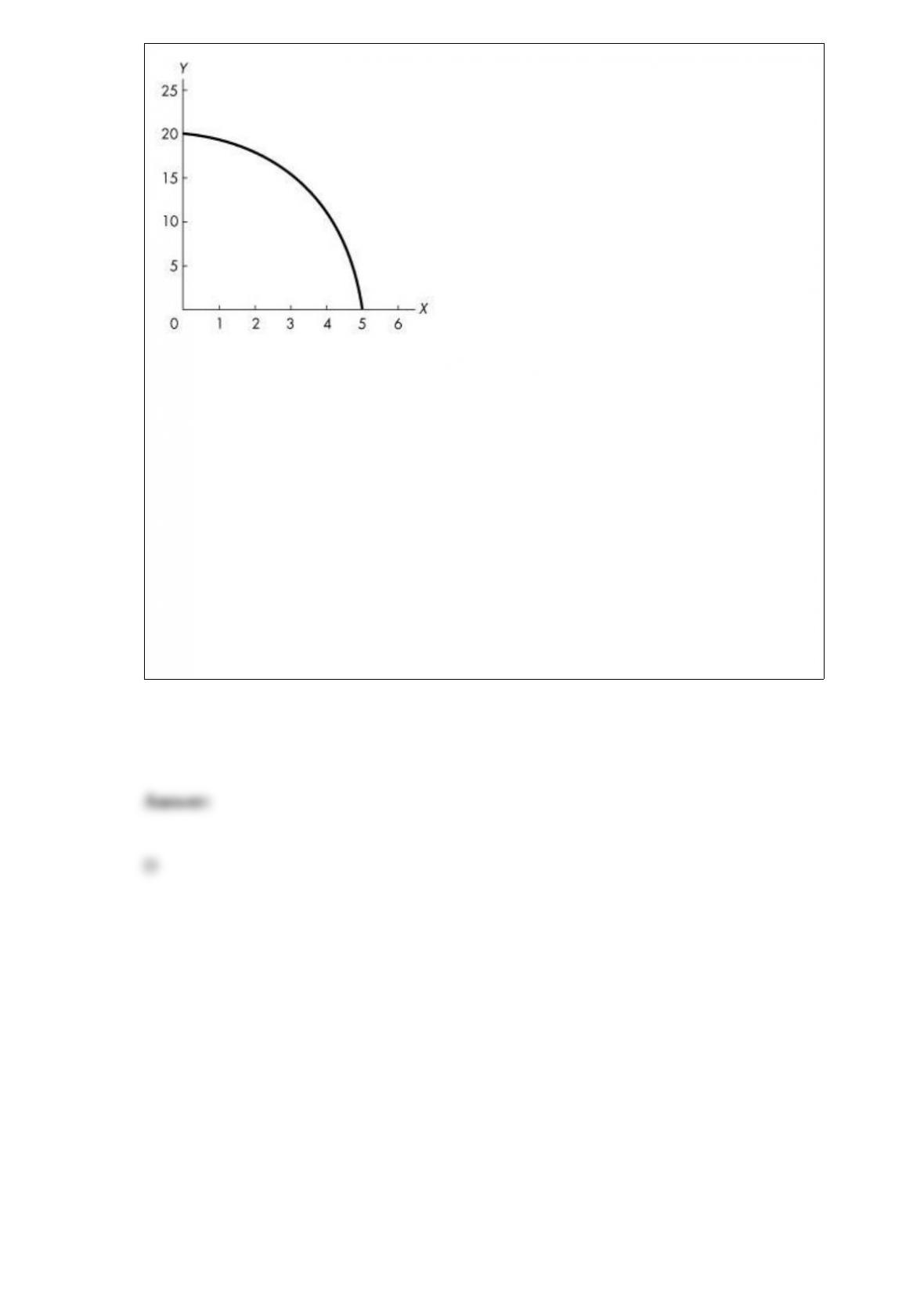

Use the figure below to answer the following question.

Figure 1A.3.11

Refer to Figure 1A.3.11. The graph shows a ________ relationship. The absolute value

of the slope of the relationship ________ as the value of x increases.

A) positive; increases

B) positive; decreases

C) negative; decreases

D) negative; increases

E) negative; does not change