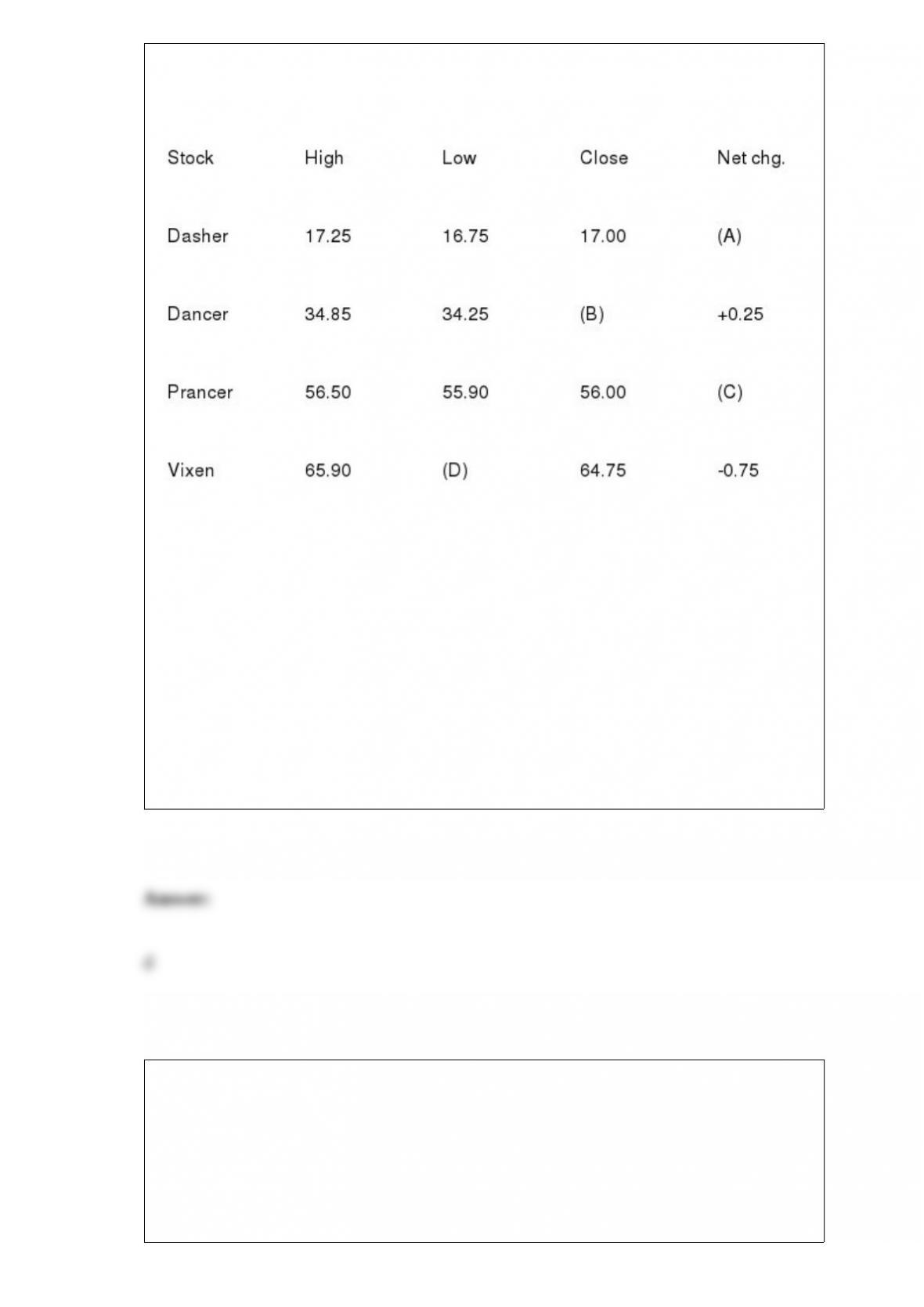

Exhibit 38-2

If the closing price of Dancer’s stock on the previous day was $34.25, what value goes

in blank (B)?

a. 34.85

b. 34.00

c. 34.75

d. 34.50

e. There is not enough information given to answer this question.

When money is used to buy a computer, it is functioning as a

a. unit of account.

b. store of value.

c. medium of exchange.

d. none of the above

Demand for a food item increases by more than the supply of the food item. One thing

for certain is that

a. the price of the food item rises.

b. income elasticity of demand (for the food item) is greater than 1.

c. the supply curve is price elastic.

d. real income rises as a result.

e. none of the above

When total expenditure (TE) exceeds total production (TP), inventory levels rise

unexpectedly, which sends a signal to firms that they have overproduced, so they cut

back on production.

a. True

b. False

If the supply of and demand for a product decrease at the same time, then equilibrium

a. quantity and equilibrium price must both decline.

b. quantity must decline, but equilibrium price may either rise, fall, or remain

unchanged.

c. price must fall, but equilibrium quantity may either rise, fall, or remain unchanged.

d. quantity must fall and equilibrium price must rise.

If expectations are formed rationally, wages and prices are completely flexible in both

the short run and the long run, and policy is correctly anticipated, increases in aggregate

demand will stimulate the economy to higher levels of Real GDP in

a. the short run or the long run.

b. neither the short run nor the long run.

c. the short run, but not in the long run.

d. the long run, but not in the short run.

The ______________ the gap between the tuition a college student pays and the

equilibrium tuition for that college, the _____________ likely the student’s instructors

will be on time and attentive during their office hours.

a. larger; less

b. smaller; more

c. larger; more

d. smaller; less

e. a and b

If an economy is operating on its production possibilities frontier (PPF), are there any

unemployed resources in the economy?

a. Yes, because if there weren’t any unemployed resources the economy would be

producing beyond its PPF.

b. No, because if there were any unemployed resources the economy would be

producing below its PPF.

c. It depends on whether the economy’s PPF is a concave (downward-sloping) curve or

a straight line.

d. Yes, because there are always some natural resources that are unemployed.

e. The answer is “yes,” but not for any of the reasons specified in answers a through d.

Situation 4-1

During the winter of 1973-74, a general system of wage and price controls (including a

price ceiling on gasoline) was in force in the United States. At the beginning of 1974,

some oil-producing countries imposed an oil embargo (a legal prohibition on

commerce) on the West. In the spring of 1974, price controls were abolished. An

economist would have most likely predicted that the oil embargo imposed in 1974

would result in a

a. leftward shift in the supply (curve) of gasoline.

b. rightward shift in the supply (curve) of gasoline.

c. leftward shift in the demand (curve) for gasoline.

d. rightward shift in the demand (curve) for gasoline.

e. both a and d

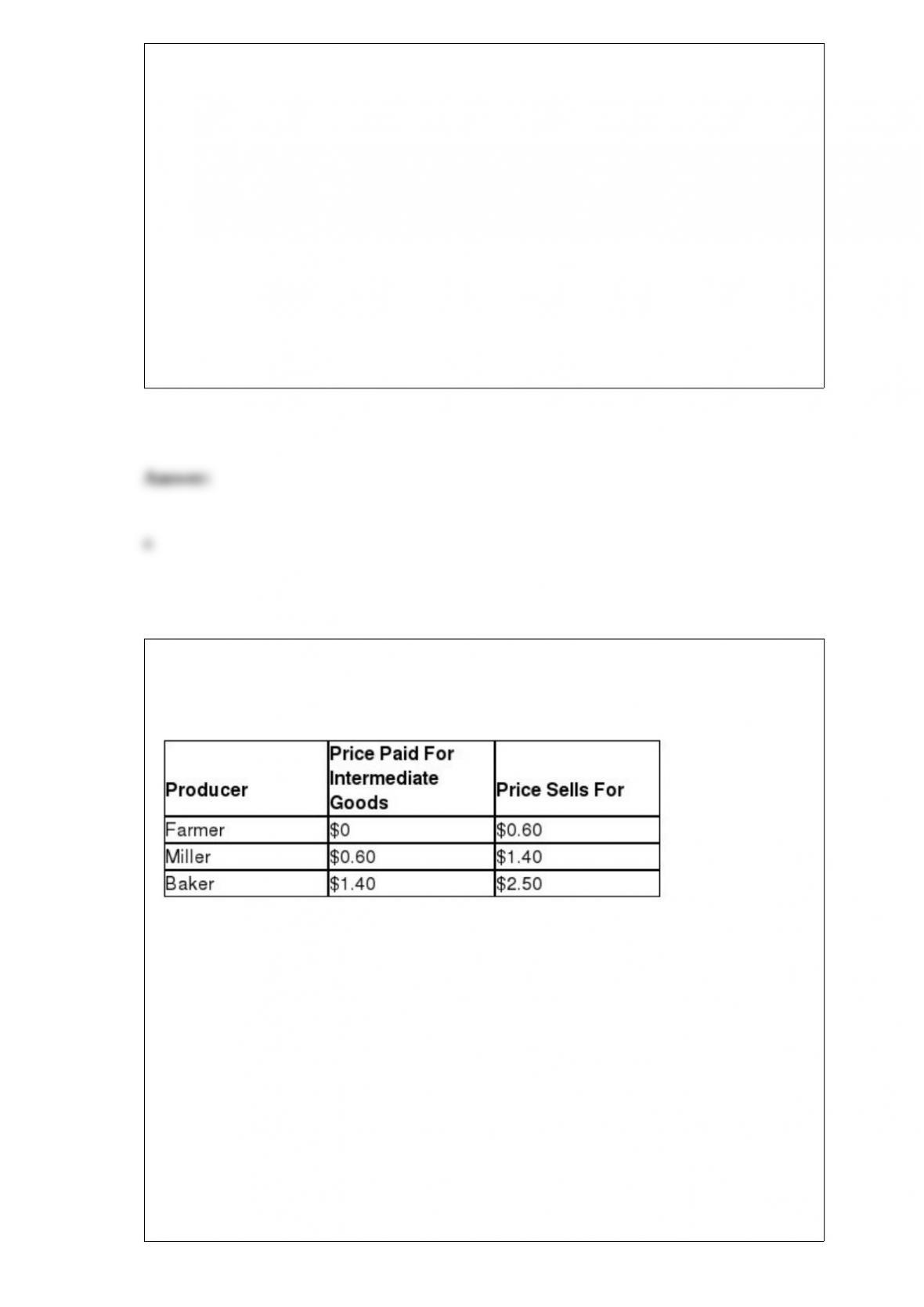

Exhibit 11-5

Assume that the farmer grows wheat and sells it to the miller, the miller turns the wheat

into flour and sells it to the baker, and the baker turns the flour into bread and sells it to

the final consumer. Which summarizes the situation prior to the value added tax

(VAT).If the government imposes a VAT rate of 10 percent, the baker must pay

___________ in VAT tax and will need to raise the price he charges the final consumer

to _______________.

a. $0.06; $2.25

b. $0.11; $2.75

c. $0.25; $2.75

d. $0.60; $2.57

Both open market purchases and quantitative easing are directed at increasing reserves

in the banking system and increasing the money supply.

a. True

b. False

The four federal taxes that together accounted for 88 percent of all federal government

tax receipts in 2013 were:

a. individual income tax, corporate income tax, property tax, and sales tax.

b. corporate income tax, national consumption tax, estate tax, and social security tax.

c. individual income tax, social security tax, corporate income tax, and Medicare tax.

d. social security tax, Medicare tax, estate tax, and corporate income tax.

e. none of the above

If you believe the economy is self-regulating, you are more likely to be a(an)

__________ than a(an) __________.

a. nonactivist; activist

b. Keynesian; monetarist

c. activist; nonactivist

d. advocate of fiscal policy; advocate of monetary policy

e. b and d

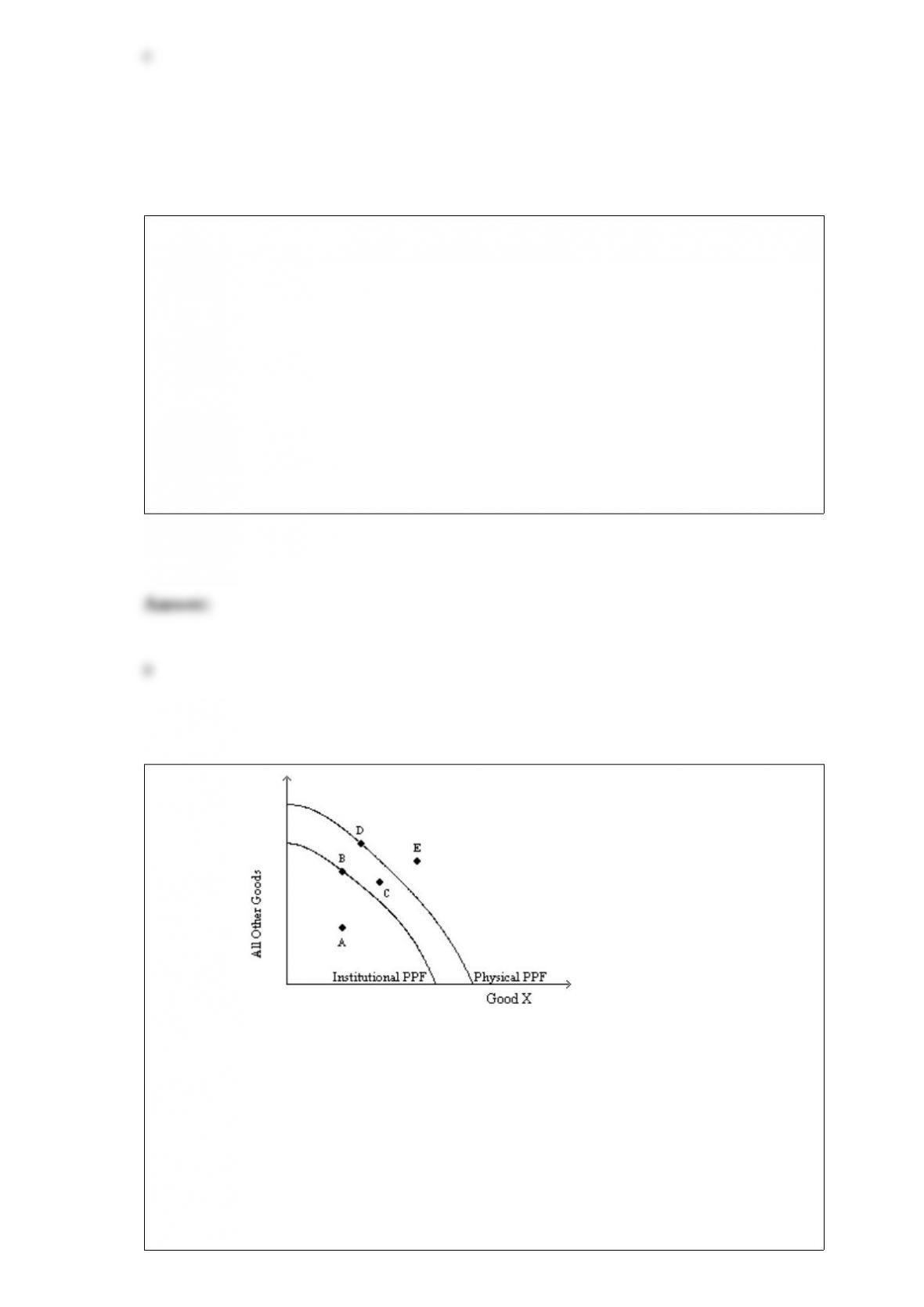

Exhibit 9-7

Which point is representative of the economy experiencing labor market shortages?

a. A

b. B

c. C

d. E