1) If the price of a good is low,

a.firms would increase profit by increasing output.

b.the quantity supplied of the good could be zero.

c.the supply curve for the good will shift to the left.

d.firms can and should raise the price of the product.

2) Individual demand curves are summed horizontally to obtain the market demand

curve.

a.True

b.False

3) When average total cost rises if a producer either increases or decreases production,

then the firm is said to be operating at efficient scale.

a.True

b.False

4) To maximize profit, a competitive firm hires workers up to the point of intersection

of the

a.marginal product curve and the wage line.

b.value of marginal product curve and the wage line.

c.value of marginal product curve and the marginal revenue curve.

d.total revenue curve and the wage line.

5) Assume the market for pork is perfectly competitive. When one pork buyer exits the

market,

a.the price of pork increases.

b.the price of pork decreases.

c.the price of pork does not change.

d.there is no longer a market for pork.

6) The quantity supplied of a good or service is the amount that sellers are willing and

able to sell at a particular price.

a.True

b.False

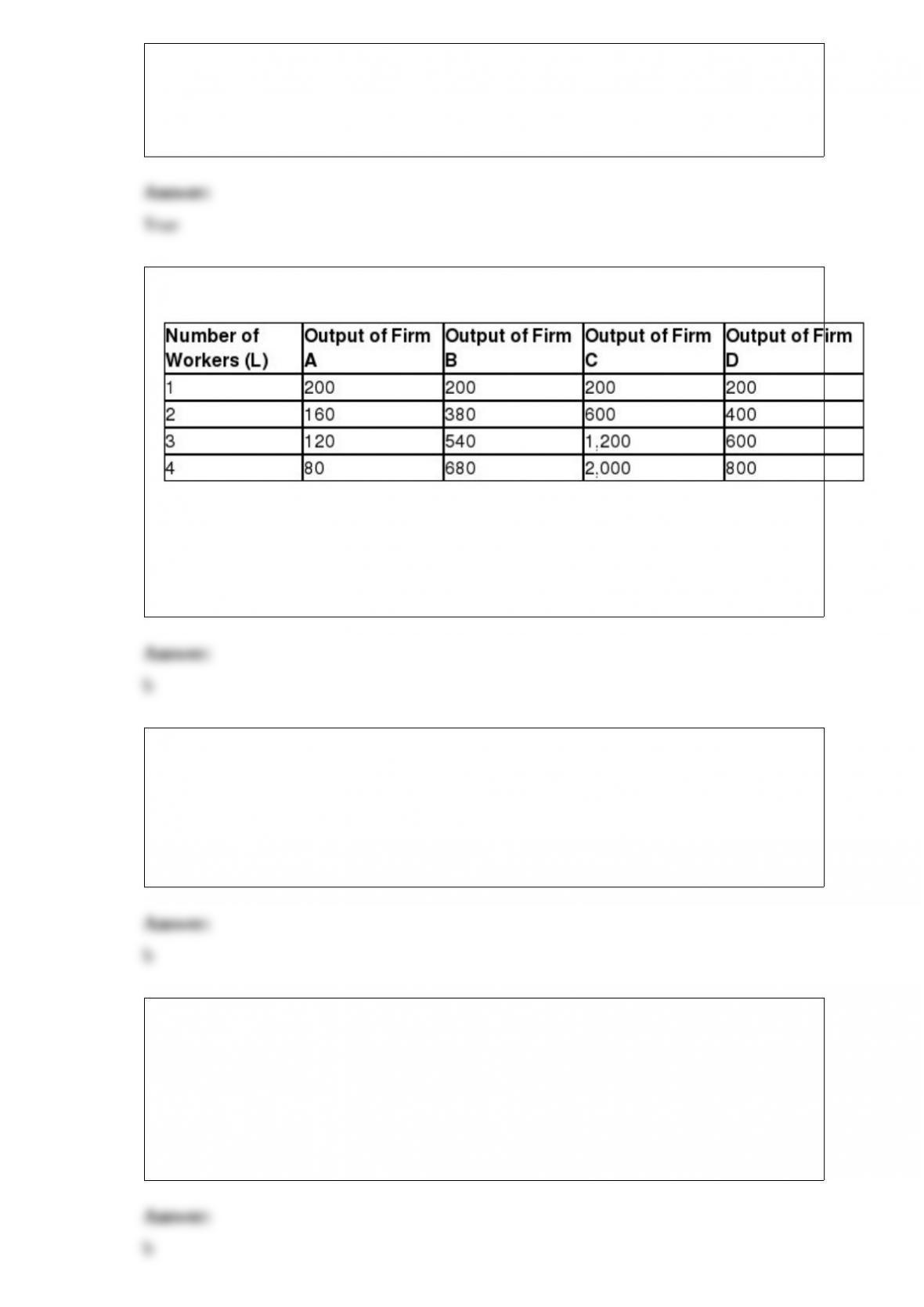

7) Table 18-3

Refer to Table 18-3. For Firm D, the marginal product of labor is

a.increasing.

b.constant.

c.decreasing.

d.negative.

8) The very high pay earned by the best actors and actresses is partially explained by

the fact that

a.they benefit from a compensating differential.

b.moviegoers all want to see the very best actors, not second-rate actors.

c.they have acting degrees from accredited acting schools.

d.the supply of good actors is very large.

9) Roger owns a small health store that sells vitamins in a perfectly competitive market.

If vitamins sell for $12 per bottle and the average total cost per bottle is $12.50 at the

profit-maximizing output level, then in the long run

a.more firms will enter the market.

b.some firms will exit from the market.

c.the equilibrium price per bottle will fall.

d.average total costs will fall.

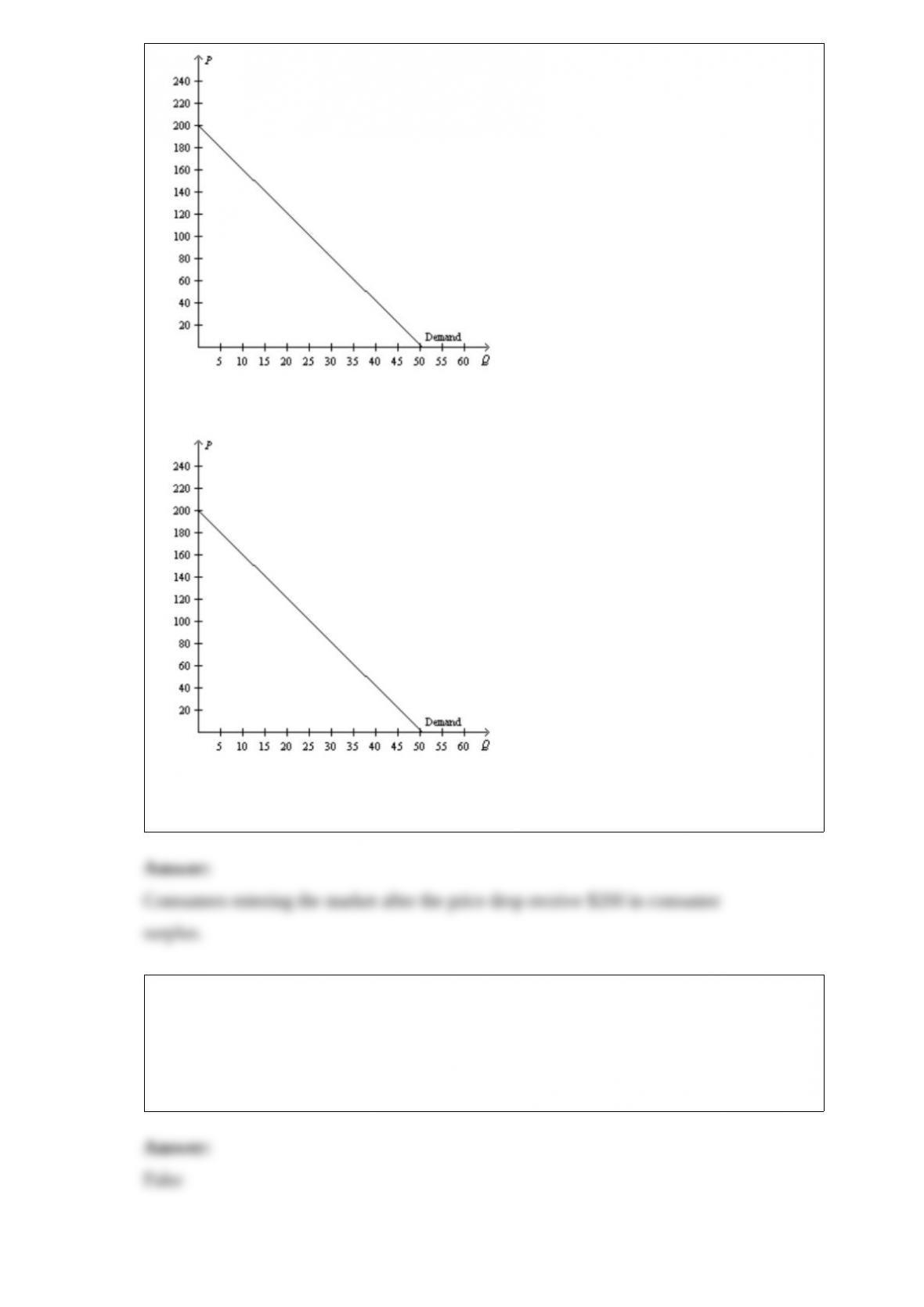

10) Figure 7-30

Refer to Figure 7-30. If the market equilibrium price falls from $120 to $80, how much

consumer surplus do consumers entering the market after the price drop receive?

11) Total surplus in a market does not change when the government imposes a tax on

that market because the loss of consumer surplus and producer surplus is equal to the

gain of government revenue.

a.True

b.False