1) if a profit-seeking competitive firm is producing its profit-maximizing output and its

total fixed costs fall by 25 percent, the firm should:

a.use more labor and less capital to produce a larger output.

b.not change its output.

c.reduce its output.

d.increase its output.

2) Suppose the aggregate demand and supply schedules for a hypothetical economy are

as shown below:

(a)Use these sets of data to graph the aggregate demand and supply curves on the below

graph.

(b)What will be the equilibrium price and output level in this hypothetical economy? Is

it also the full-employment level of output? Explain.

(c)Why wont the 150 index be the equilibrium price level? Why wont the 250 index be

the equilibrium price level?

(d)Suppose demand increases by $400 billion at each price level. What will be the new

equilibrium price and output levels?

(e)What factors might cause a change in aggregate demand?

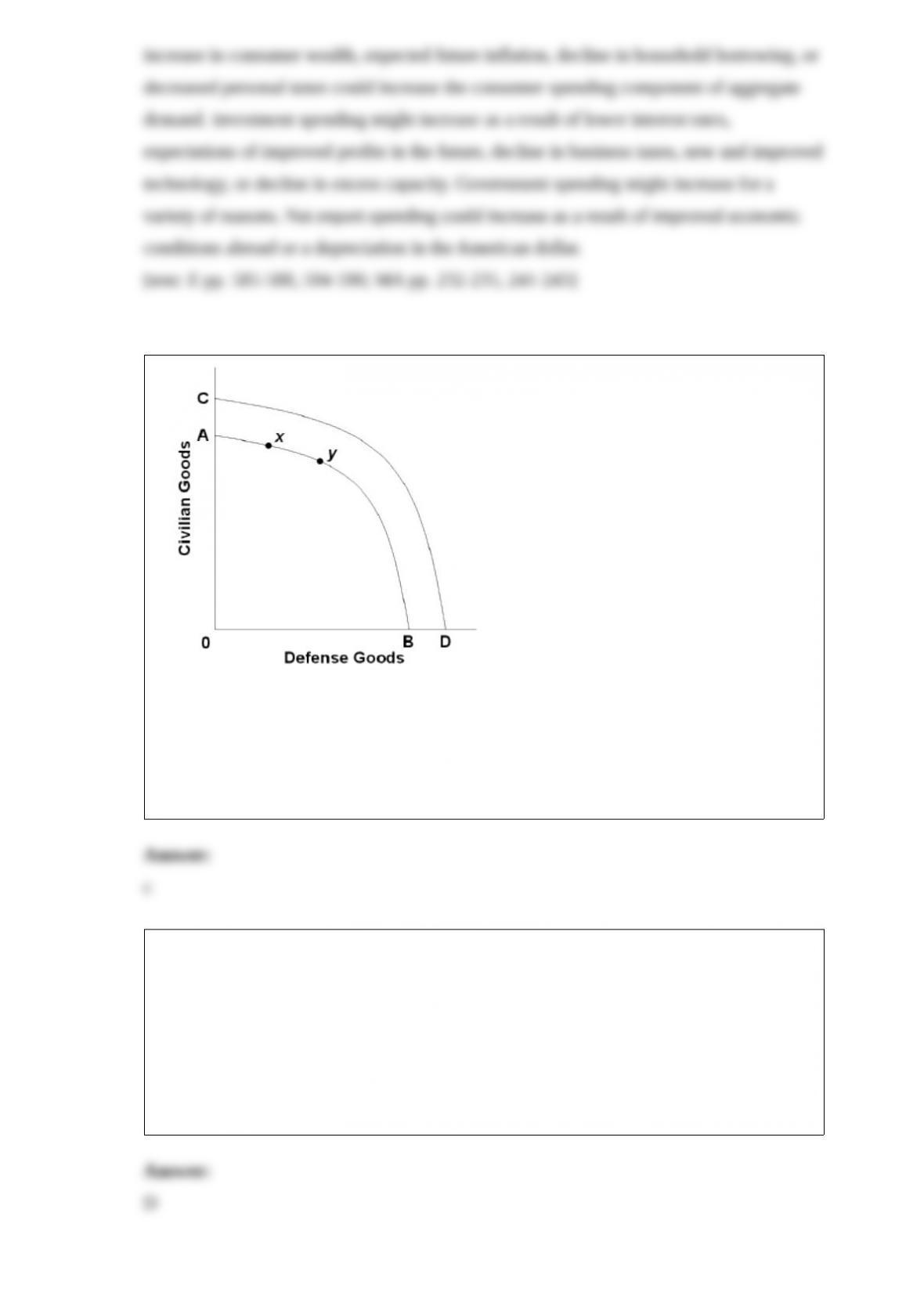

3)

(consider this) refer to the above diagram. the u.s. response to the events of september

11, 2001, is illustrated by the:

a.shift of the production possibilities curve from cd to ab.

b.shift of the production possibilities curve from ab to cd.

c.move from x to y on production possibilities curve ab.

d.move from y to x on production possibilities curve ab.

4) Suppose that the Anytown city government asks private citizens to donate money to

support the town’s annual holiday lighting display. Assuming that the citizens of

Anytown enjoy the lighting display, the request for donations suggests that:

A.the display creates negative externalities.

B.government should tax the producers of holiday lighting.

C.resources are currently overallocated to the provision of holiday lighting in Anytown.

D.resources are currently underallocated to the provision of holiday lighting in

Anytown.

5) Which of the following is considered a non-renewable natural resource?

A.solar power.

B.coal.

C.oceans.

D.aquifers.

6) (Last Word) According to economists Ayres and Levitt, owners of car that have

traditional automobile alarms:

A.may impose costs on owners of unalarmed cars whose cars become greater targets for

thieves.

B.create spillover benefits for owners of unalarmed cars.

C.cause widespread negative externalities in the form of the noise pollution that results

from false alarms.

D.create a moral hazard problem because they tend to park their cars in riskier locations

than they would otherwise.

7) refer to the above data. the average product (ap) when two units of labor are hired is:

a.8

b.9

c.10

d.18

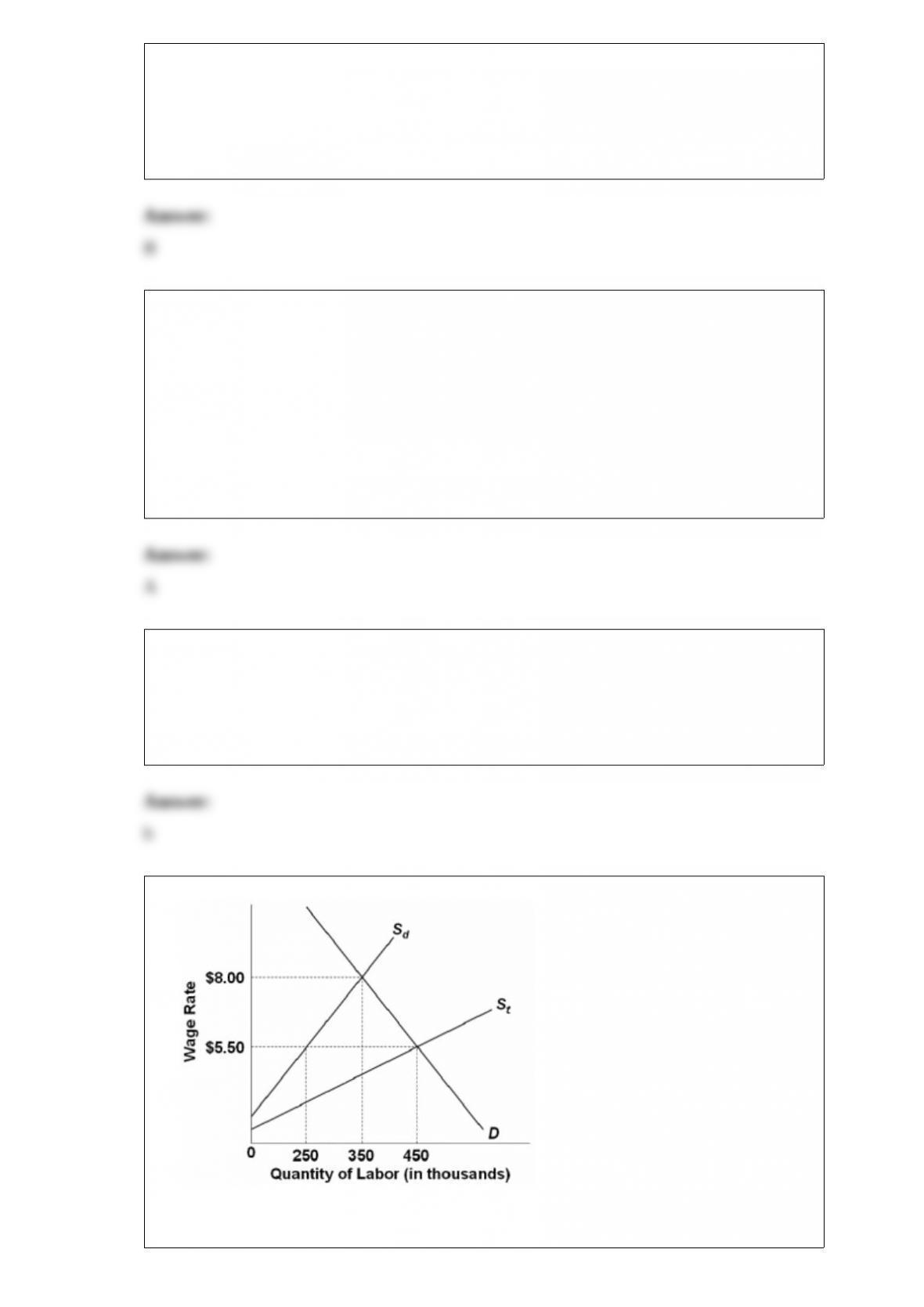

8)

assumptions: 1) employers in this market are willing and able to ignore minimum wage

laws; 2) sd represents the supply of domestically-born (and legal immigrant) workers;

3) st represents the total supply of workers in this labor market (sd plus illegal

immigrants); and 4) unless otherwise stated, illegal immigration is not effectively

blocked by the government.

refer to the above figure. the equilibrium wage and level of employment are,

respectively:

a.$5.50 and 250,000

b.$5.50 and 350,000

c.$8 and 350,000

d.$5.50 and 450,000

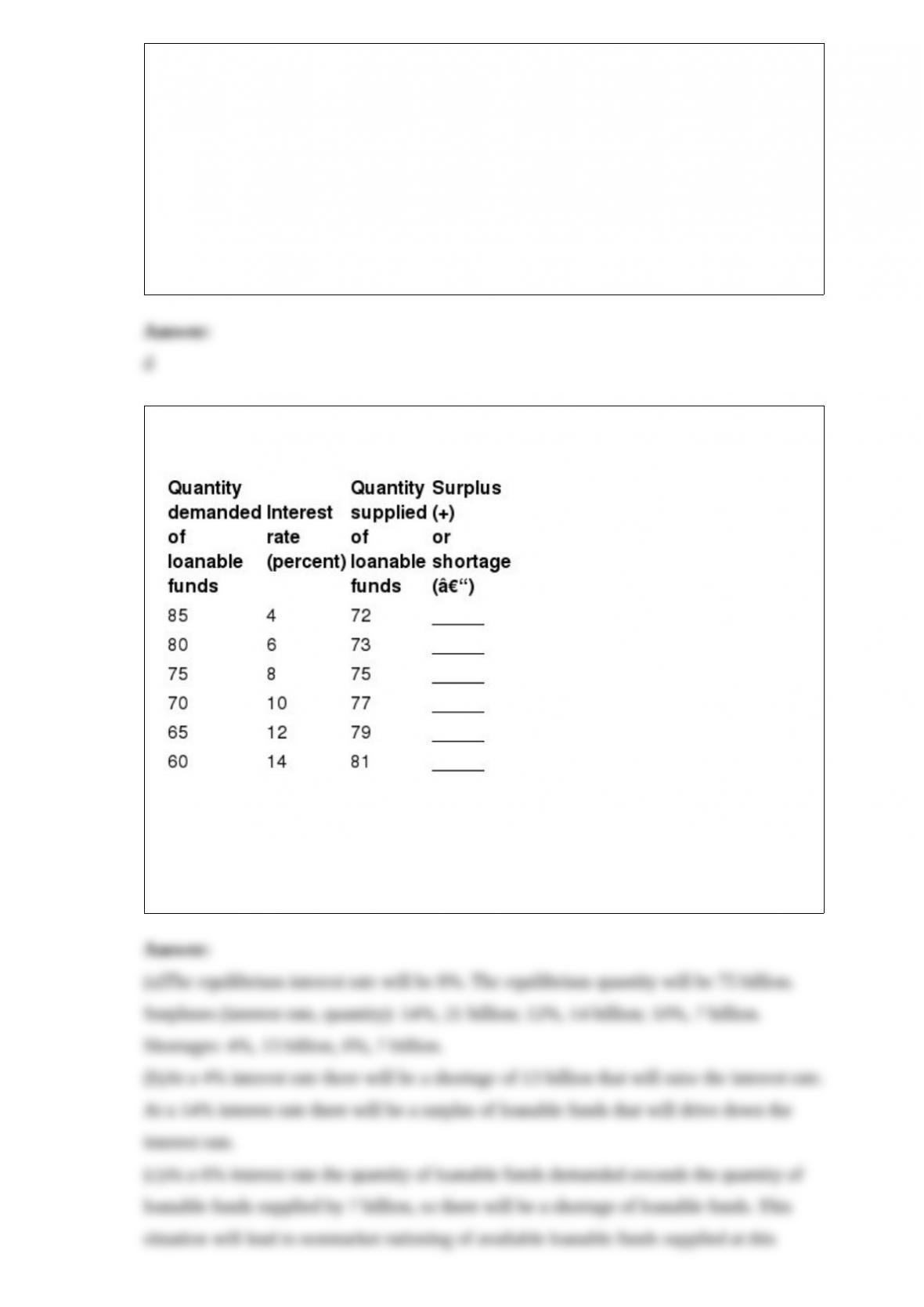

9) Suppose the total demand and supply of loanable funds (in billions) are as follows:

(a)What will be the market or equilibrium interest rate? What is the equilibrium

quantity of loanable funds? Complete the surplus-shortage column.

(b)Why will 4% not be the equilibrium interest rate in this market? Why not 14%?

(c)Now suppose that the government establishes a usury loan that sets the interest rate

at 6%. Explain the economic effects of this usury law.

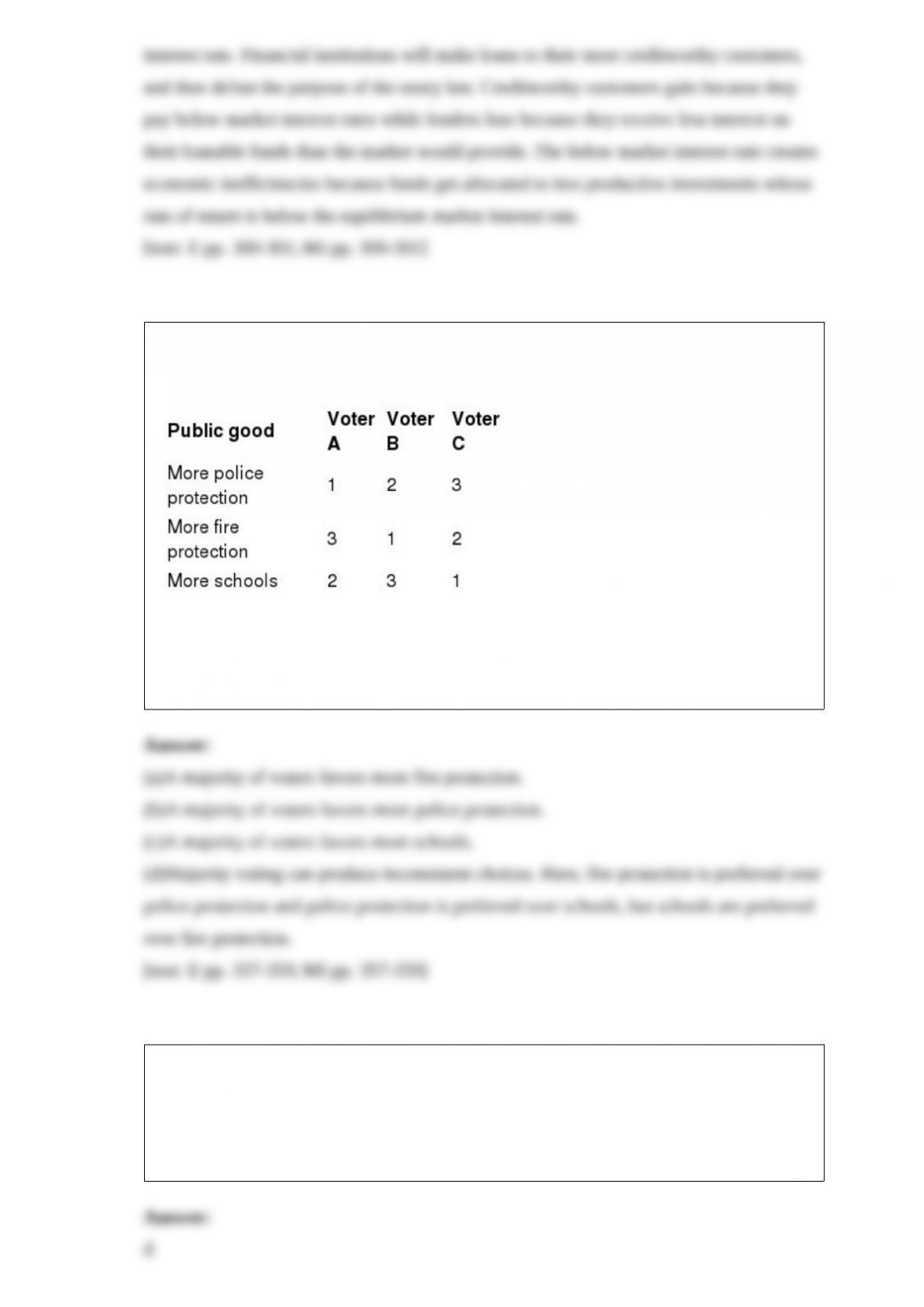

10) Answer the next four questions on the basis of the following table which shows the

rankings of the public goods by three voters: A, B, and C.

(a)What will be the choice between more police protection and more fire protection?

(b)What will be the choice between more schools and more police protection?

(c)What will be the choice between more fire protection and more schools?

(d)What do the rankings in the table indicate about choices made under majority rule?

11) refer to the above diagram. which line(s) show(s) a negative vertical intercept?

a.c only.

b.both c and e

c.b, c, and e

d.both b and c

12) the total amount of u.s. tax revenue needed to finance the public sector:

a.has been a declining percentage of the domestic output in this century.

b.equals about 40 percent of domestic output.

c.equals about 15 percent of domestic output.

d.is larger today, as a percentage of total output, than in 1960.

13) The profit-maximizing and the least-cost combination of inputs are:

A.the result of unrelated decisions.

B.always identical.

C.such that the minimization of costs always results in profit maximization.

D.such that the maximization of profits always entails the least-cost combination of

inputs.

14) implicit costs are:

a.regarded as costs by accountants but not by economists.

b.payments that a firm makes to other firms or individuals who supply resources to it.

c.non-expenditure costs.

d.costs that vary proportionately with output.

15) the production possibilities curve:

a.shows all of those levels of production that are consistent with a stable price level.

b.indicates that any combination of goods lying outside the curve is economically

inefficient.

c.is a frontier between all combinations of two goods that can be produced and those

combinations that cannot be produced.

d.shows all of those combinations of two goods that are most preferred by society.

16) suppose that salsa manufacturers sell 2 million bottles at $3.50 in one year, and 3

million bottles at $3 in the next year. based on this information we can conclude that

the:

a.law of supply has been violated.

b.law of demand has been violated.

c.demand for salsa has increased.

d.supply of salsa has increased.