A fixed input, X, and a variable input, Y, are used to produce good A. If the marginal

physical product (MPP) of Y is constant, it follows that the

a. marginal cost curve is upward sloping.

b. total fixed cost curve is vertical.

c. total variable cost curve is downward sloping.

d. b and c

e. none of the above

In the acreage allotment program, a farmer’s acreage allotment is sometimes based on a

farmer’s

a. history of production.

b. income.

c. location.

d. b and c

e. none of the above

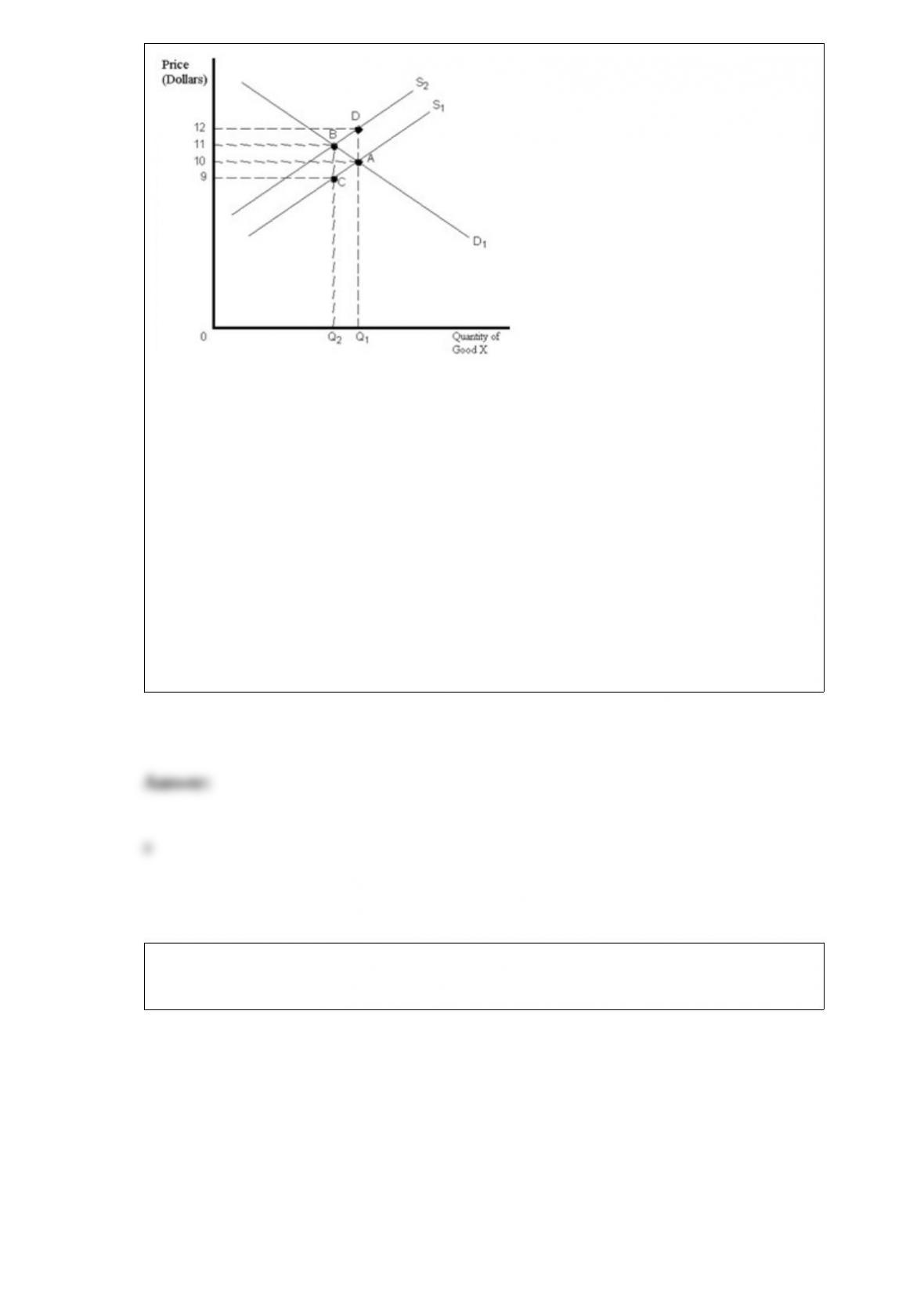

Exhibit 20-8

The market for good X is initially at point A. A tax is then placed on the production of

good X. At the new equilibrium, point __________, buyers end up paying __________

of the tax and sellers end up paying __________ of the tax.

a. B; one-half; one-half

b. D; one-half; one-half

c. C; one-half; one-half

d. B; one-quarter; three-quarters

e. none of the above

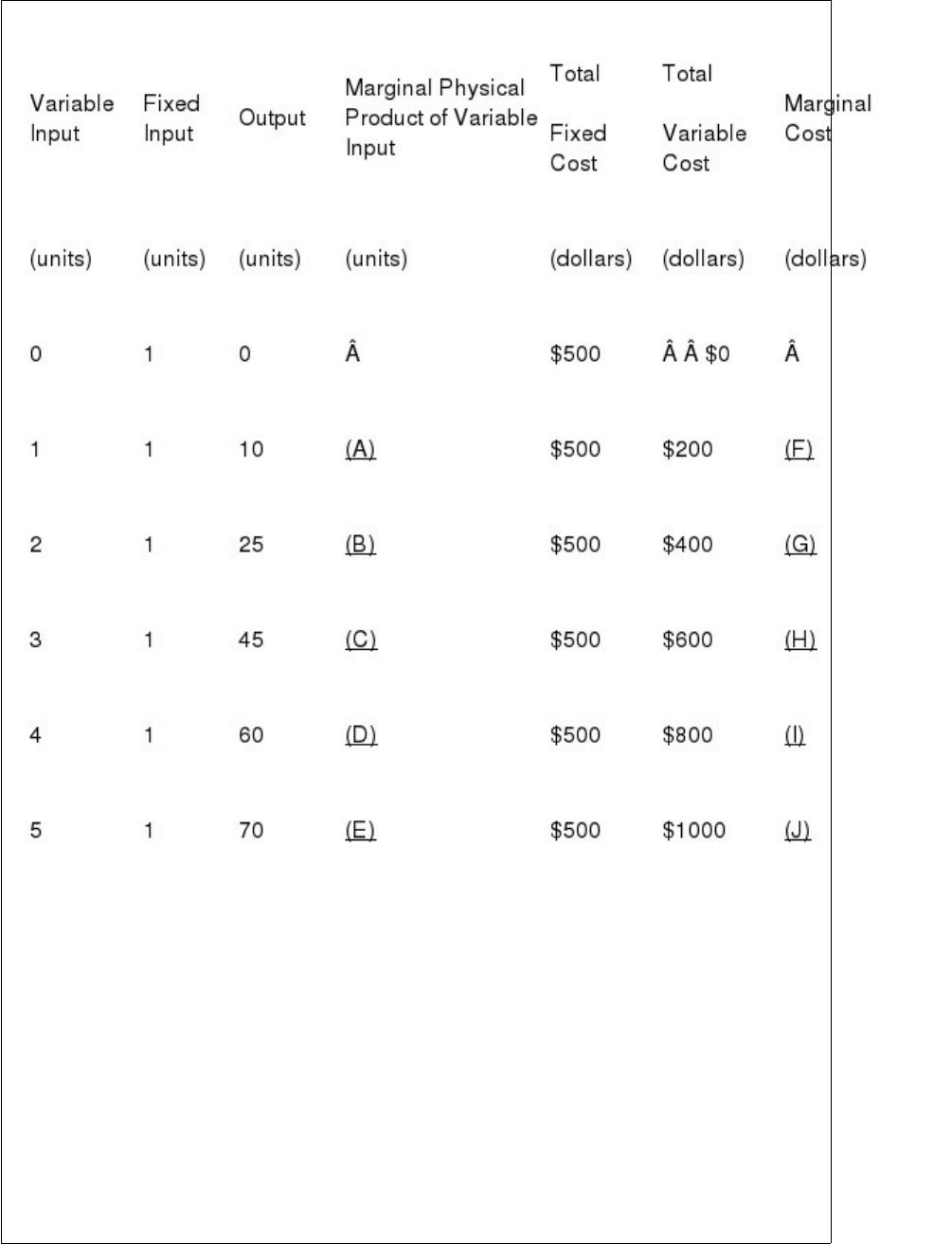

Exhibit 22-3

The average fixed cost of producing 10 units of output is

a. $50.00.

b. $10.00.

c. $2.50.

d. $1.00.

e. $500.00.

The theory of consumer choice assumes that consumers attempt to maximize

a. the difference between total utility and marginal utility.

b. average utility.

c. total utility.

d. marginal utility.

If a firm has no variable costs, the profit-maximizing price is also the

revenue-maximizing price.

a. True

b. False

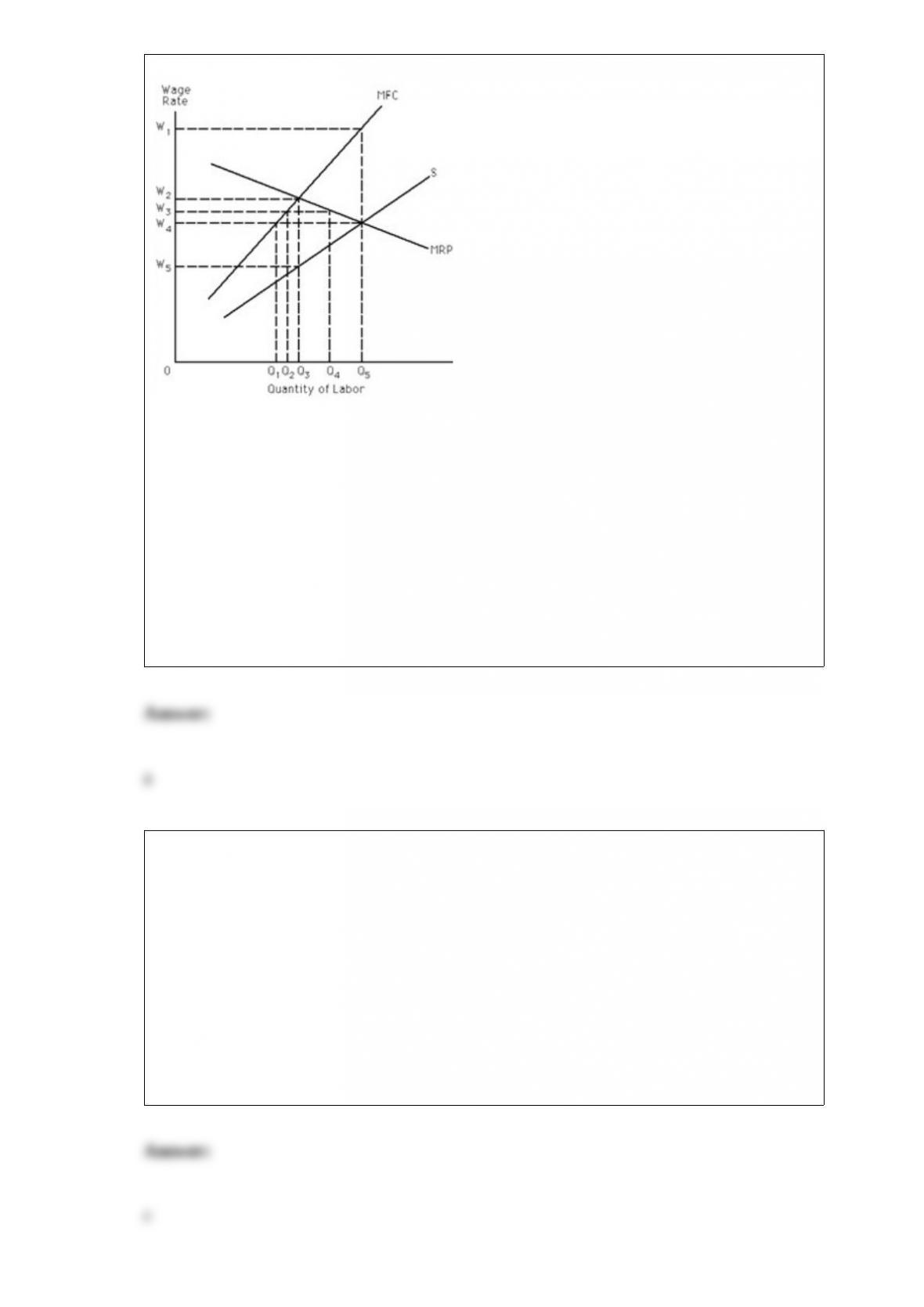

Exhibit 28-8

What is the total wage bill of the profit- maximizing monoposonist?

a. W5 x Q3

b. W4 x Q5

c. W3 x Q2

d. W2 x Q3

According to the text, the _______________ is currently the primary reserve currency.

a. Chinese renmimbi

b. euro

c. U.S. dollar

d. Japanese yen

e. British pound

A line is parallel to the vertical axis. The slope of the line is

a. zero.

b. infinite.

c. indicative of an inverse relationship between two variables.

d. indicative of a direct relationship between two variables.

e. b and d

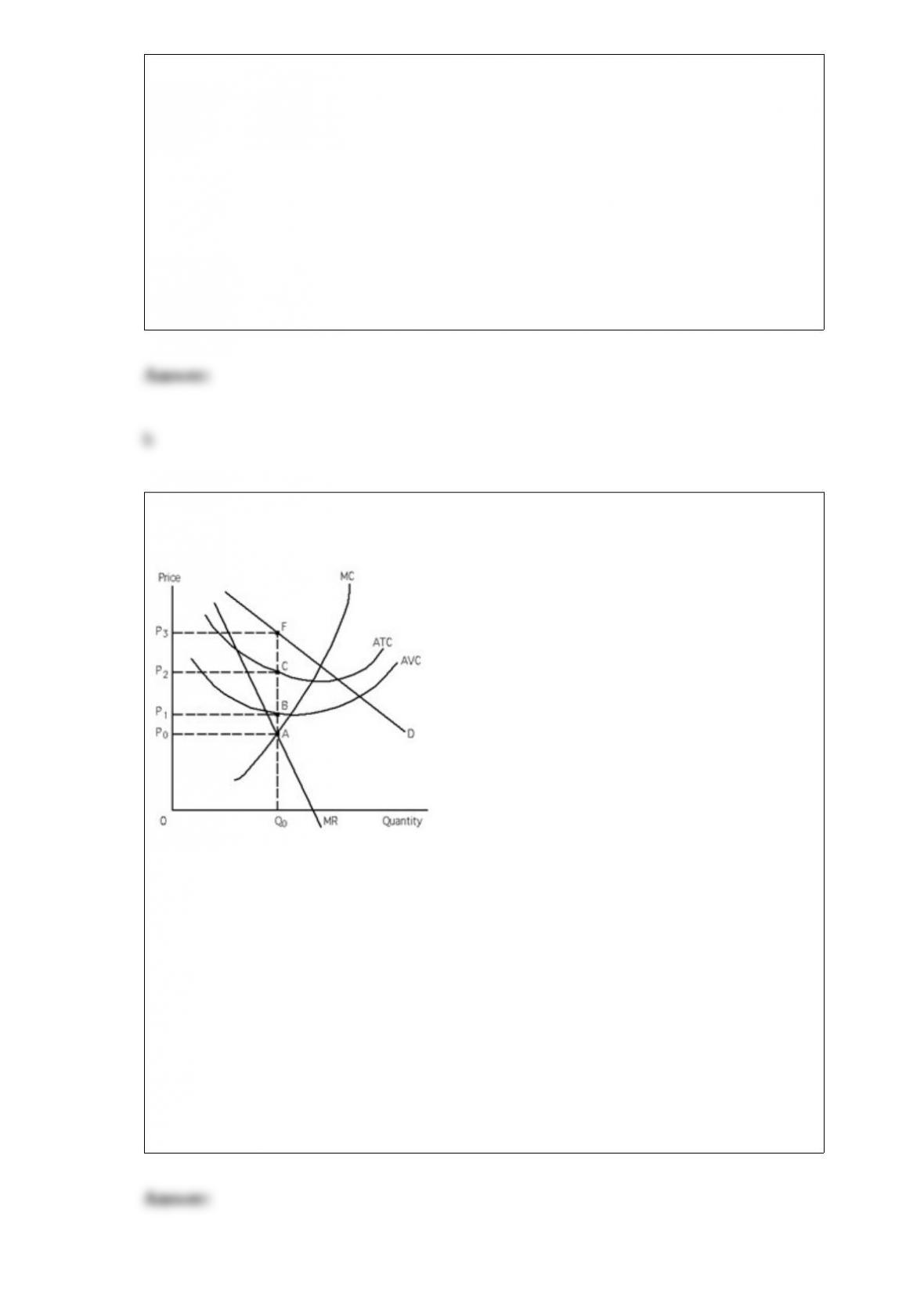

Exhibit 24-2

The profit-maximizing monopolist produces Q0 units and charges a price of

a. P0.

b. P1.

c. P3.

d. P2.

e. none of the above

Which of the following is not a way that natural monopolies are regulated?

a. Government regulators determine the price of the product.

b. Government regulators determine an acceptable profit.

c. Government regulators determine an acceptable output.

d. Government regulators determine which patents the monopoly can retain.

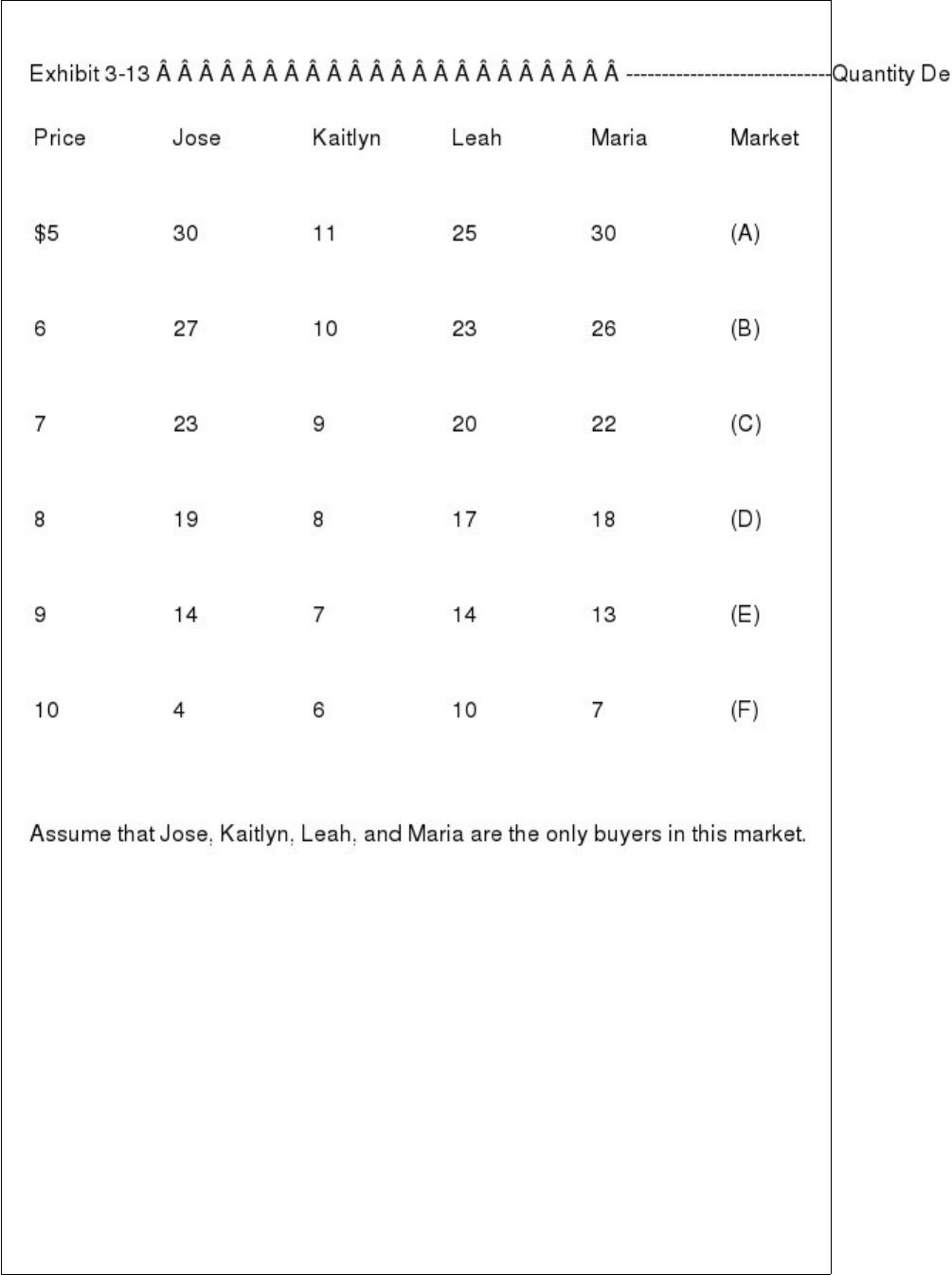

Fill in blanks (E) and (F) respectively with the market quantity demanded at each given

price.

a. 12; 6.75

b. 25; 19

c. 75; 64

d. 48; 27

e. none of the above