A market society will always protect the natural environment.

a. True

b. False

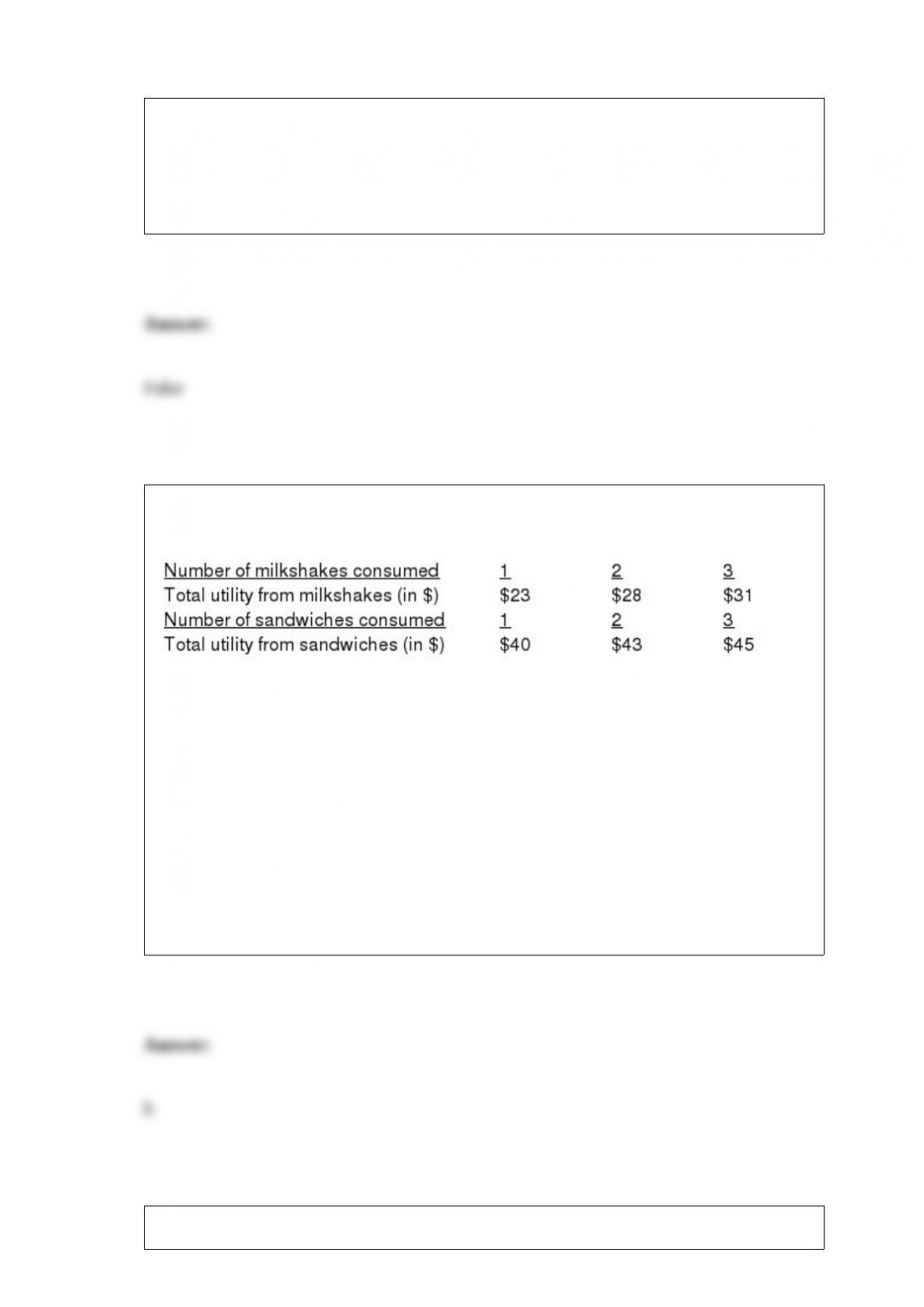

Table 5-1

Table 5-1 gives information on George’s total utility from consuming milkshakes and

sandwiches. If George’s income this week is $15, milkshakes are $3 each, and

sandwiches $2, he will maximize his utility if he buys

a. three milkshakes and two sandwiches.

b. three milkshakes and three sandwiches.

c. no milkshakes and as many sandwiches as possible.

d. two milkshakes and three sandwiches.

A graph of total profits is always likely to be positively sloped throughout its length.

a. True

b. False

If demand increases, the equilibrium price and equilibrium quantity will both fall,

everything else being equal.

a. True

b. False

Consumer surplus is what one consumer is willing to pay for a commodity over what

another consumer is willing to pay for the same commodity.

a. True

b. False

If an oligopolistic manufacturer believes that he faces a kinked demand curve for his

product, he thinks his competitors will ____ if he lowers his price and ____ if he raises

his price.

a. lower their prices; raise their prices.

b. lower their prices; not raise their prices

c. not lower their prices; raise their prices

d. not lower their prices; not raise their prices

Which of the following was designed to head off panics among market participants and

forestall crashes like the ones in October 1929 and October 1987?

a. Program trading

b. Circuit breakers

c. Derivatives

d. Volatility index

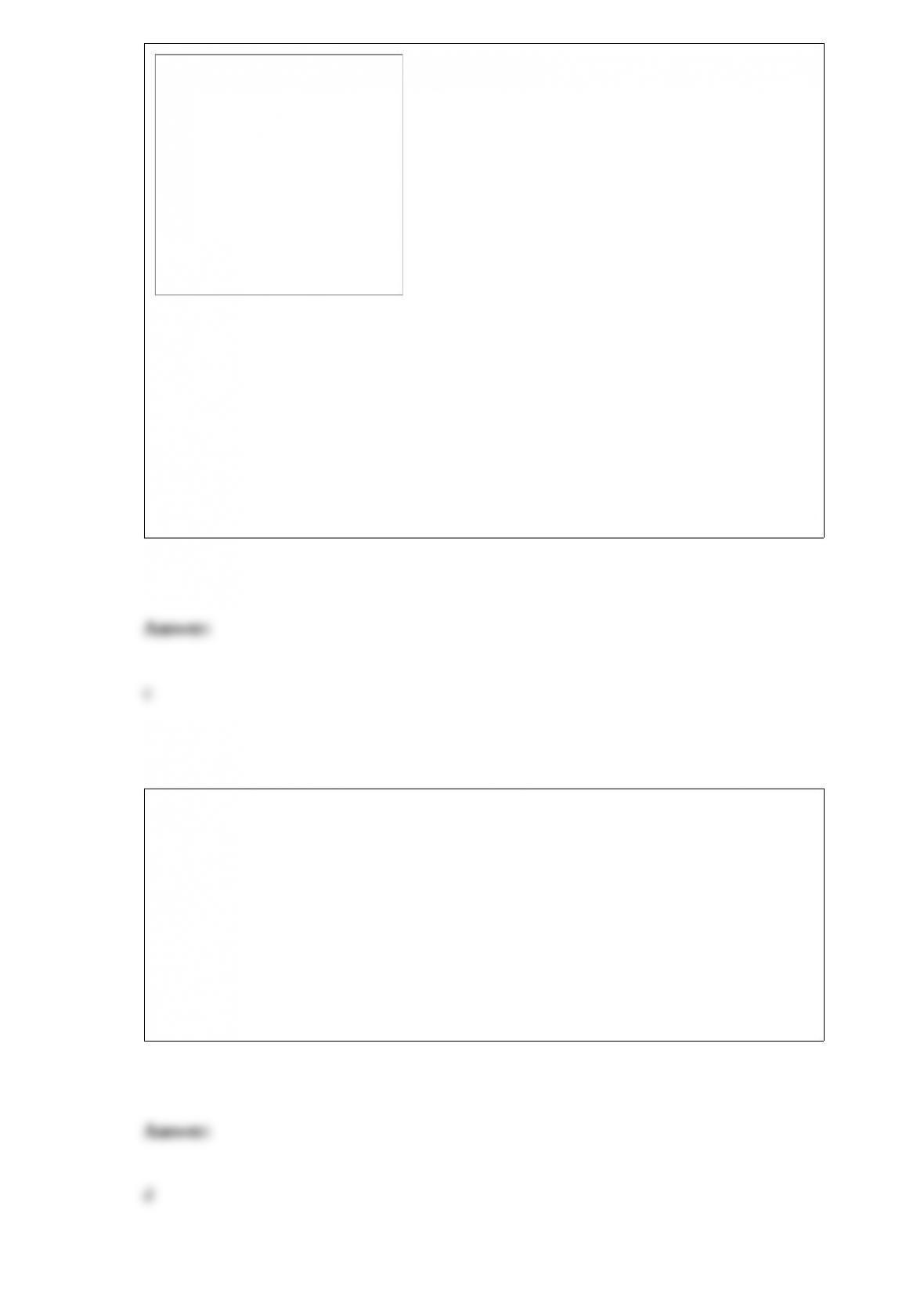

Figure 5-19

In Figure 5-19, the consumer experiences at point C

a. greater total utility than at point D.

b. greater total utility than at point E.

c. less total utility than at point D.

d. total utility equal to that experienced at point D.

Assume that a country imposes a tariff in order to gain a price advantage on an item.

What is the typical response from the exporting country?

a. It accepts the situation, and does nothing about it.

b. It seeks greater efficiency in order to offset the tariff.

c. It refuses to sell to the country that imposes the tariff.

d. It retaliates by imposing tariffs or quotas on items from the other country.

In long-run equilibrium under perfect competition,

a. the firm and the industry will have the same cost curves.

b. only a very few firms will be earning economic profits.

c. the demand curves facing individual firms will fall to the level of minimum AC.

d. individual firms will tend to increase their outputs.

Japan and China produce guns and rice. The country with the lowest opportunity cost of

guns (in terms of rice) will

a. import guns.

b. have a comparative advantage in guns.

c. have an absolute advantage in guns.

d. have a comparative advantage in rice.

When demand for a product is very inelastic, the burden of a tax falls mainly on

a. producers.

b. consumers.

c. tax collectors.

d. people who drop out of the market.

Public goods are

a. valuable socially.

b. not depletable and not excludable.

c. subject to the “free rider” problem.

d. All of the above are correct.

Figure 22-7

In Figure 22-7, AB represents the production possibilities of Pestoland and CD that of

Pastaland. The graph indicates Pestoland has an absolute

a. advantage in both pesto and pasta.

b. and comparative advantage in both pesto and pasta.

c. advantage in both goods, but a comparative advantage only in pesto.

d. advantage in pesto only and a comparative advantage only in pasta.

Elaine values the utility of her first cup of coffee at $1; a second cup, $.75; and a third

cup, $.50 If Elaine drinks three cups of coffee for breakfast, her total utility is equal to

a. $.50, the value of her last cup of coffee.

b. $1,00, the value of her first cup of coffee.

c. marginal utility.

d. $2,25

e. $1,50

Since a union represents individuals rather than firms, it cannot be considered a

monopoly.

a. True

b. False

In 2013, new bond issues and other forms of debt totaled ____ in corporate financing.

a. $650 billion

b. $783 tillion

c. $1 trillion

d. −$2 billion

If, as price increases by 10 percent, total revenue decreases by 10 percent demand is

a. elastic.

b. unit elastic.

c. inelastic.

d. perfectly inelastic.

Which of the following would not lead to more conservation?

a. higher prices for a resource

b. increased interest rates on bonds

c. public awareness of increasing scarcity

d. higher taxes on goods produced using the resource

Figure 4-23

In Figure 4-23, which movement will be caused by changes in income?

a. A to C

b. C to A

c. B to D

d. B to A

The demand for borrowed funds is a derived demand.

a. True

b. False

Because of the owner’s prejudice, a firm chooses to discriminate against hiring Oriental

workers. Compared to an otherwise identical nondiscriminating firm hiring in the same

competitive market, the discriminating firm will have

a. higher costs.

b. lower profits.

c. a lower quantity of labor supplied at every wage.

d. All of the above are correct.

If your cumulative Grade Point Average (GPA) after two years of college is 3,0, and

your grades for the current semester average 3,5, what will happen to your cumulative

GPA? Explain the similarity of this example to the case of marginal cost and average

cost.