Covered interest rate arbitrage is possible when:

a. both currencies are appreciating.

b. the actual inflation rates are identical in both countries.

c. the difference in the interest rates in two countries exactly equals the spot-to-forward

exchange rate differential.

d. the difference in interest rates in two countries is out of line with the spot-to-forward

exchange rate differential.

e. none of the above

Answer:

_________ allowed any institution to “truncate” the paper check at any point in the

check clearing process.

a. Riegle-Neal Interstate Banking and Branching Efficiency Act

b. Fair and Accurate Credit Transactions Act

c. Troubled Asset Relief Program

d. Sarbanes-Oxley Act

e. Check 21 Act

Answer:

Asset based loans:

a. are not generally tied to inventory.

b. include loans to finance leveraged buyouts.

c. put more weight on cash flow than collateral when evaluating the loan.

d. All of the above.

e. None of the above.

Answer:

A __________ controls at least two commercial banks.

a. one-bank holding company

b. state holding company

c. national holding company

d. multibank holding company

e. financial holding company

Answer:

Which of the following is a non-discretionary factor that will decrease a bank’s daily

reserves held at the Federal Reserve?

a. Deferred availability items

b. Payments on loans from Federal Reserve

c. Remittances charged

d. Excess from local clearing house

e. Federal funds sold

Answer:

CDs sold at a steep discount from par and appreciate to face value at maturity are

known as:

a. zero coupon CDs.

b. variable rate CDs.

c. callable CDs.

d. stock market indexed CDs.

e. immediately available funds CDs

Answer:

A bank estimates that their average balance on demand deposit accounts is $2,500, net

of float. Each account costs the bank $175 per year in processing costs. The bank

collects an average of $5 per month on each account in service charges. Assume reserve

requirements are 10%. What is the net cost of an average demand deposit?

a. 4.5%

b. 4.8%

c. 5.1%

d. 6.8%

e. 7.0%

Answer:

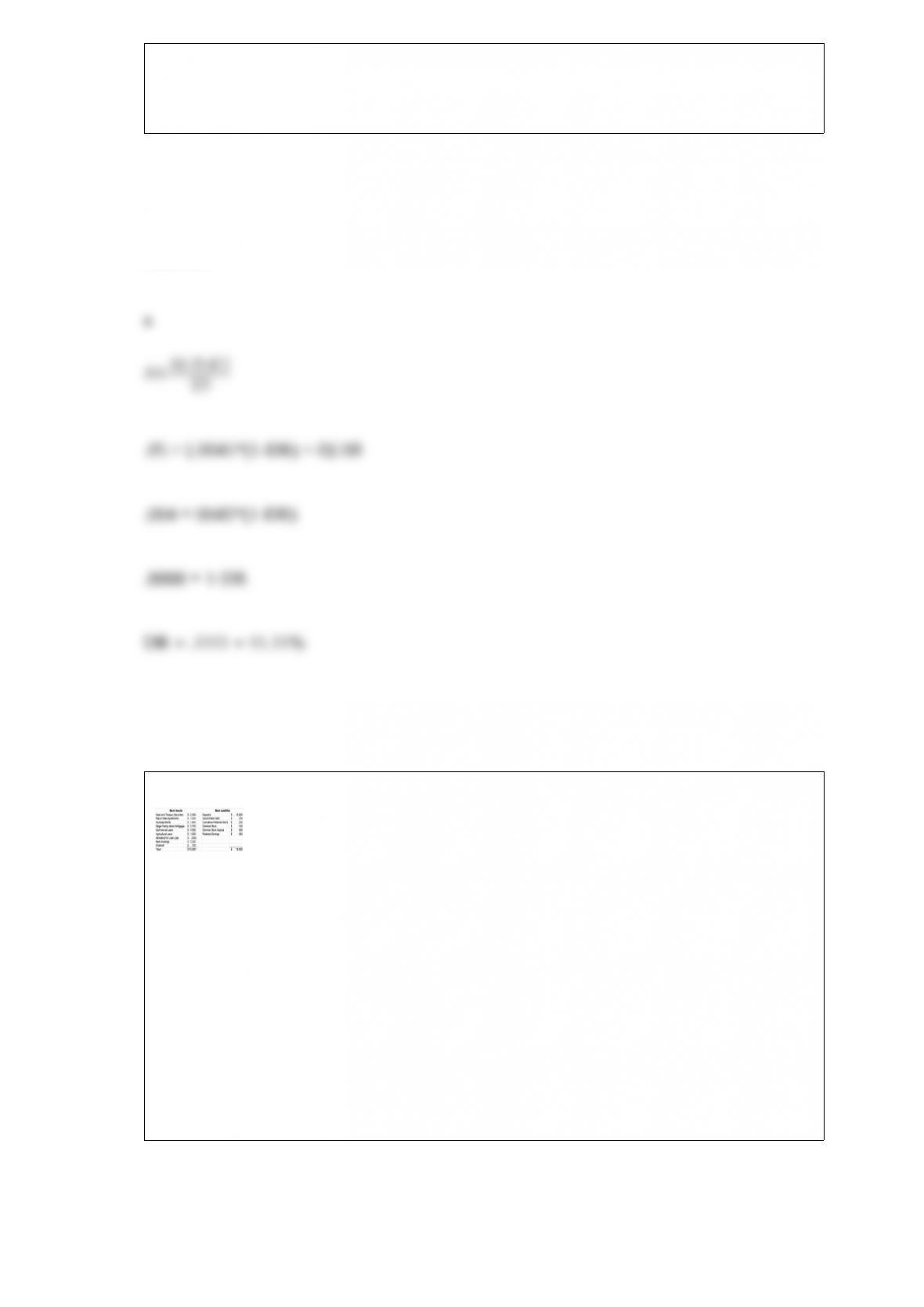

Use the following information.

A bank currently just meets its total capital requirements of 8%. The bank currently has

a dividend payout ratio of 35%. Assets are expected to grow at 5%.

If the bank expects its ROA to be .45%, what is the maximum dividend payout ratio to

support the increase in assets?

a. 11.1%

b. 22.2%

c. 33.3%

d. 44.4%

e. 89.9%

Answer:

Use the following information.

The tangible common equity (TCE) ratio for this bank is:

a. 4.00%

b. 4.04%

c. 5.00%

d. 5.05%

e. 5.39%

Answer:

In regards to repurchase agreements, the margin is:

a. a good faith deposit.

b. a loan against the repurchase agreement.

c. a risk-free guarantee.

d. the difference between the market value of the collateral and the amount of the loan.

e. all of the above.

Answer:

Which of the following is true regarding money market deposit accounts (MMDAs)?

a. A maximum of three checks per month may be written on a MMDA account.

b. The average check size on an MMDA account is smaller than the average demand

deposit check size.

c. MMDAs are formally transaction accounts.

d. Required reserves on MMDAs are higher than on demand deposit accounts.

e. Rates paid on MMDAs are generally higher than rates on money market mutual

funds.

Answer:

Use the following bank information.

What is the weighted average duration of liabilities?

a. 1.25 years

b. 2.03 years

c. 2.12 years

d. 3.00 years

e. 4.25 years

Answer:

The Tax Reform Act of 1986 made home equity loans more appealing by:

a. eliminating the tax deduction of interest on consumer loans not secured by real estate.

b. allowing banks to lend up to 125% of the equity in a home.

c. preventing homes from being liquidated in Chapter 13 bankruptcy cases.

d. reducing bank income taxes on mortgage loan income.

e. all of the above.

Answer:

Large time deposits are generally referred to as:

a. mini CDs.

b. jumbo CDs.

c. big CDs.

d. giant CDs.

e. super CDs.

Answer:

A trader buys a 90-day Eurodollar futures contract at 95.25. The next day, interest rates

rise to 25%. Which of the following is true? Assume that the initial and maintenance

margins are $5,000.

a. The trader would have to deposit an additional $5,000 into her account.

b. The trader would have to deposit an additional $1,250 into her account.

c. The trader would have to deposit an additional $625 into her account.

d. The trader could withdraw $1,250 from her margin account.

e. The trader could withdraw $625 from her margin account.

Answer:

International banking facilities (IBFs):

a. cannot offer transaction accounts to non-bank customers.

b. must hold reserves with the Federal Reserve against deposits.

c. do not have to pay FDIC insurance premiums on Eurodollar deposits.

d. all of the above

e. a. and c. only

Answer:

The most important of the five Cs of credit when evaluating a consumer loan

application is:

a. cash.

b. capacity.

c. character.

d. conditions.

e. competition.

Answer:

Noninterest-checking accounts are called:

a. Automatic transfer from savings accounts.

b. NOW accounts.

c. demand deposit accounts.

d. repurchase accounts.

e. whole-tail accounts.

Answer:

Liquidity risk is a function of many factors. Which of the following is NOT one of

those factors?

a. Funding sources.

b. Location of depositors.

c. Average size of accounts.

d. Number of depositors.

e. All of the above are liquidity risk factors.

Answer:

Historically, a commercial bank was defined as a firm that:

a. accepted NOW accounts and made consumer loans.

b. accepted demand deposits and made business loans.

c. accepted government deposits and made public loans.

d. accepted demand deposits and made consumer loans.

e. is regulated by the Federal Reserve.

Answer:

According to the Federal Reserve, a non-card bank:

a. issues its own card.

b. does not issue its own card.

c. operates under a regional card bank.

d. a. and c.

e. b. and c.

Answer:

How do capital requirements constrain bank growth?

a. By discouraging investments in Treasury securities.

b. By disallowing the ownership of mortgage loans.

c. By decreasing a bank’s net interest margin.

d. By limiting the amount of new assets that a bank can acquire through debt financing.

e. By reducing a bank’s CAMELS ratings.

Answer:

Investment banks generally engage in all of the following types of business activities

except:

a. proprietary trading.

b. goodwill recovery.

c. market making.

d. securities underwriting.

e. advisory services

Answer:

Which of the following would generally be considered price sensitive?

a. Fed funds purchased

b. Fed funds sold

c. Repurchase agreements

d. Demand deposits

e. A 20-year zero coupon bond

Answer:

Why do regulators prefer higher capital requirements?

a. It justifies the existence of regulatory agencies.

b. It better protects the deposit insurance fund.

c. It enhances bank asset quality.

d. It decreases bank profitability.

e. It increases bank leverage.

Answer:

Overdraft fees:

a. represent a risk charge.

b. are a source of wholesale funding.

c. reduce reserve requirements.

d. increases capital.

e. have increased in maturity.

Answer:

An “independent” bank is:

a. an “independent” subsidiary of a multi-bank holding company.

b. another name for a one-bank holding company.

c. a bank that is exempt from paying federal income taxes.

d. a bank that is specifically created to underwrite corporate debt issues.

e. not controlled by a multi-bank holding company or any other outside interest.

Answer:

The Federal Reserve has Reserve Banks and branches in ___ districts across the

country.

a. 10

b. 12

c. 14

d. 16

e. 18

Answer:

A bank’s “burden” is defined as:

a. net interest income minus non-interest income.

b. non-interest income minus non-interest expense.

c. non-interest expense minus non-interest income.

d. net interest income plus non-interest income.

e. interest expense plus non-interest expense.

Answer:

Which of the following is false regarding community banks?

a. They typically have extensive operations in specific regions of the country.

b. They typically operate in a limited geographic area.

c. They often focus on lending to small businesses.

d. The bulk of their funding comes from deposits.

e. They tend to grow at a modest rate.

Answer:

A bond that with a 12% coupon rate (paid semi-annually) has two years to maturity. If

the current discount rate is 10%, what is the bond’s Macaulay’s duration?

a. 4.00 years

b. 3.47 years

c. 2.00 years

d. 1.73 years

e. 1.50 years

Answer: