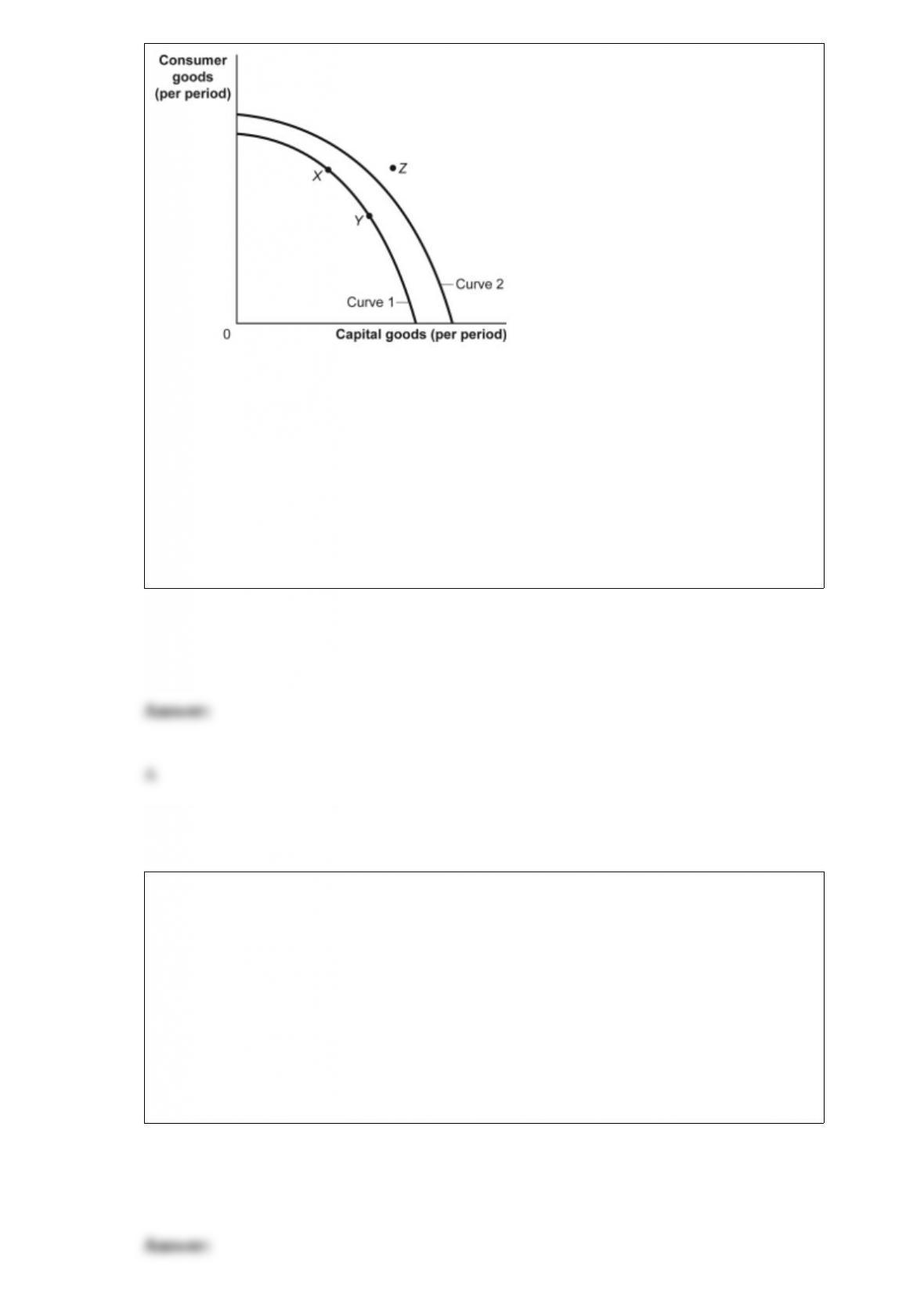

Figure: Consumer and Capital Goods

(Figure: Consumer and Capital Goods)

Look at the figure Consumer and Capital Goods. The movement from curve 1 to curve

2 indicates:

A) a growing ability of the economy to produce capital and consumer goods.

B) going from unemployment to full employment.

C) a decrease in the factors of production.

D) a shift of the production possibility frontier toward producing fewer goods.

Which of the following is a form of strategic behavior intended to influence the future

actions of other players?

A) dormant strategy

B) trigger strategy

C) conclusive strategy

D) tit-for-tat strategy

A decrease in demand and a decrease in supply will lead to _____ in equilibrium

quantity and _____ in equilibrium price.

A) a decrease; an indeterminate change

B) an indeterminate change; an increase

C) an indeterminate change; a decrease

D) an increase; an indeterminate change

A decrease in supply is caused by:

A) a decrease in input prices.

B) an increase in the number of sellers in the market.

C) suppliers’ expectations of higher prices in the future.

D) an advancement in the technology for producing the good.

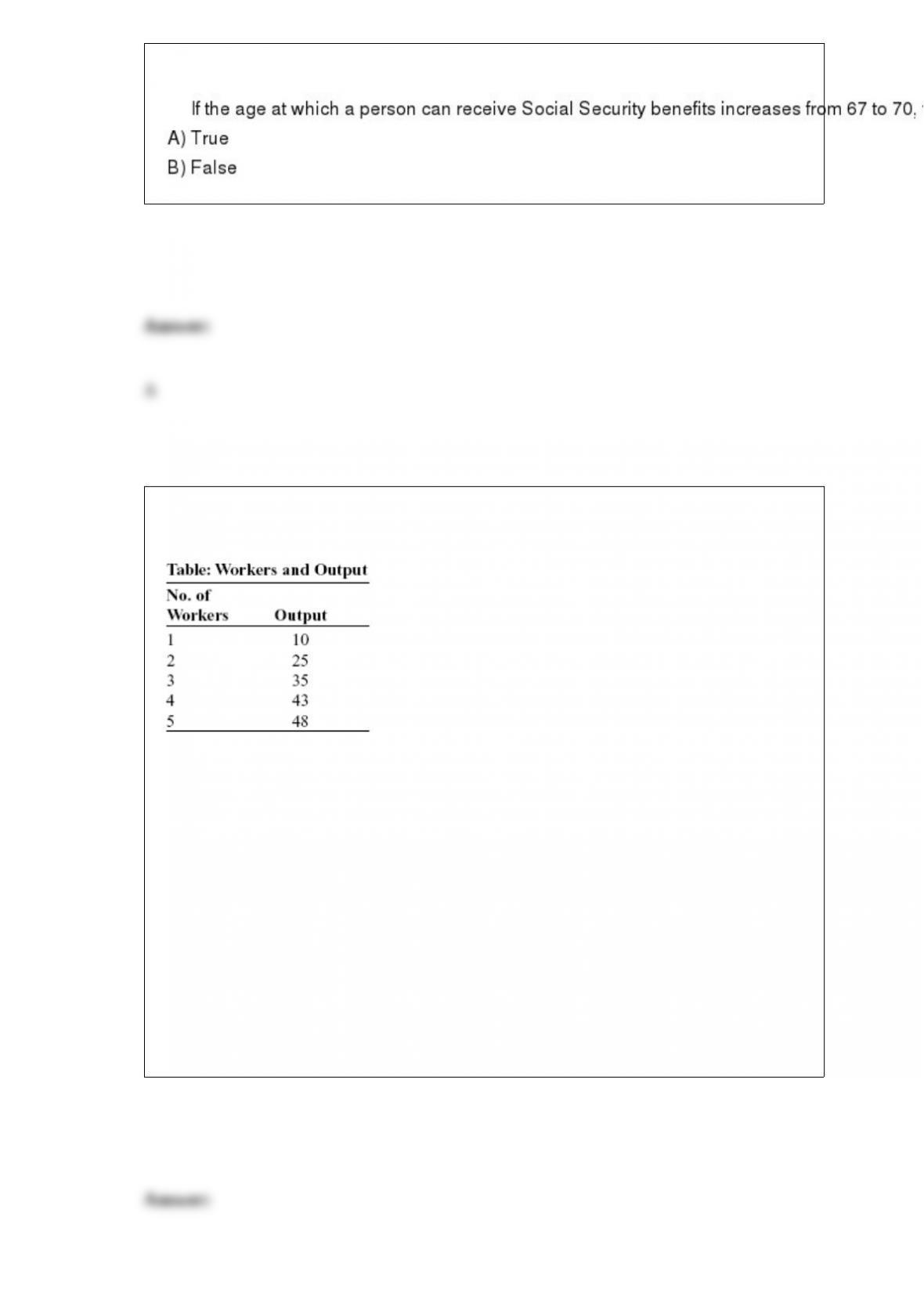

(Table: Workers and Output) Look at the table Workers and Output. After graduation

you achieve your dream of opening an art shop that specializes in selling mud statues.

You pay $10 per day on a loan from your uncle, and regardless of how much you

produce, you pay $10 per day to each of the workers who make the mud statues. How

many workers should you hire to minimize your marginal costs?

A) two

B) three

C) four

D) five

When a market is in equilibrium, the quantity:

A) demanded is equal to zero.

B) demanded is equal to quantity supplied.

C) demanded is greater than quantity supplied.

D) supplied is zero.

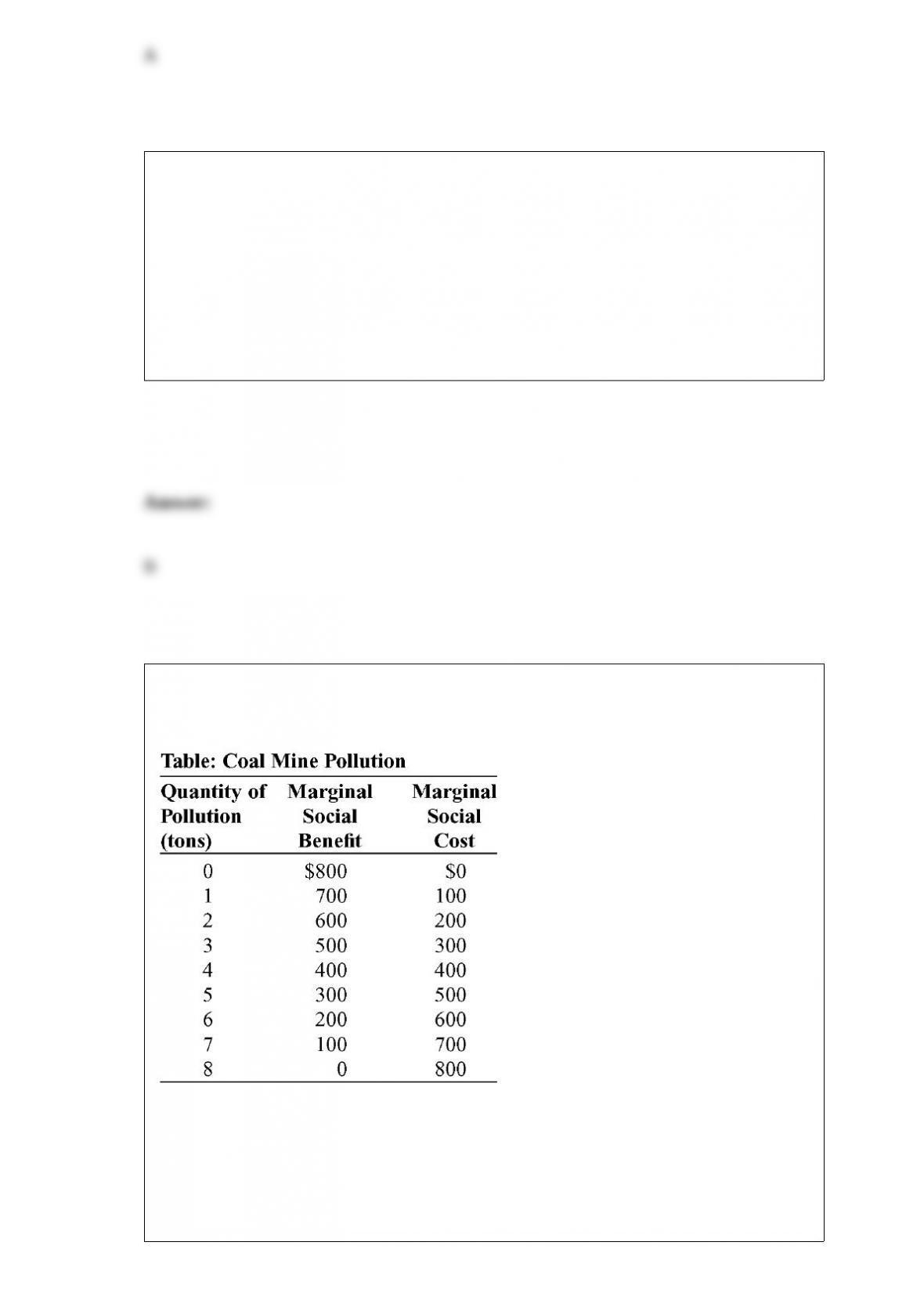

(Table: Coal Mine Pollution) The table Coal Mine Pollution shows the marginal social

benefit and cost of various amounts of pollution from a coal mine. If 2 tons of pollution

is produced, the marginal social benefit is _____, and the marginal social cost is _____.

A) $600; $200

B) $500; $300

C) $400; $400

D) $800; $0

An industry with easy entry and exit of a large number of small firms producing a

standardized product is:

A) in perfect competition.

B) in monopolistic competition.

C) an oligopoly.

D) a monopoly.

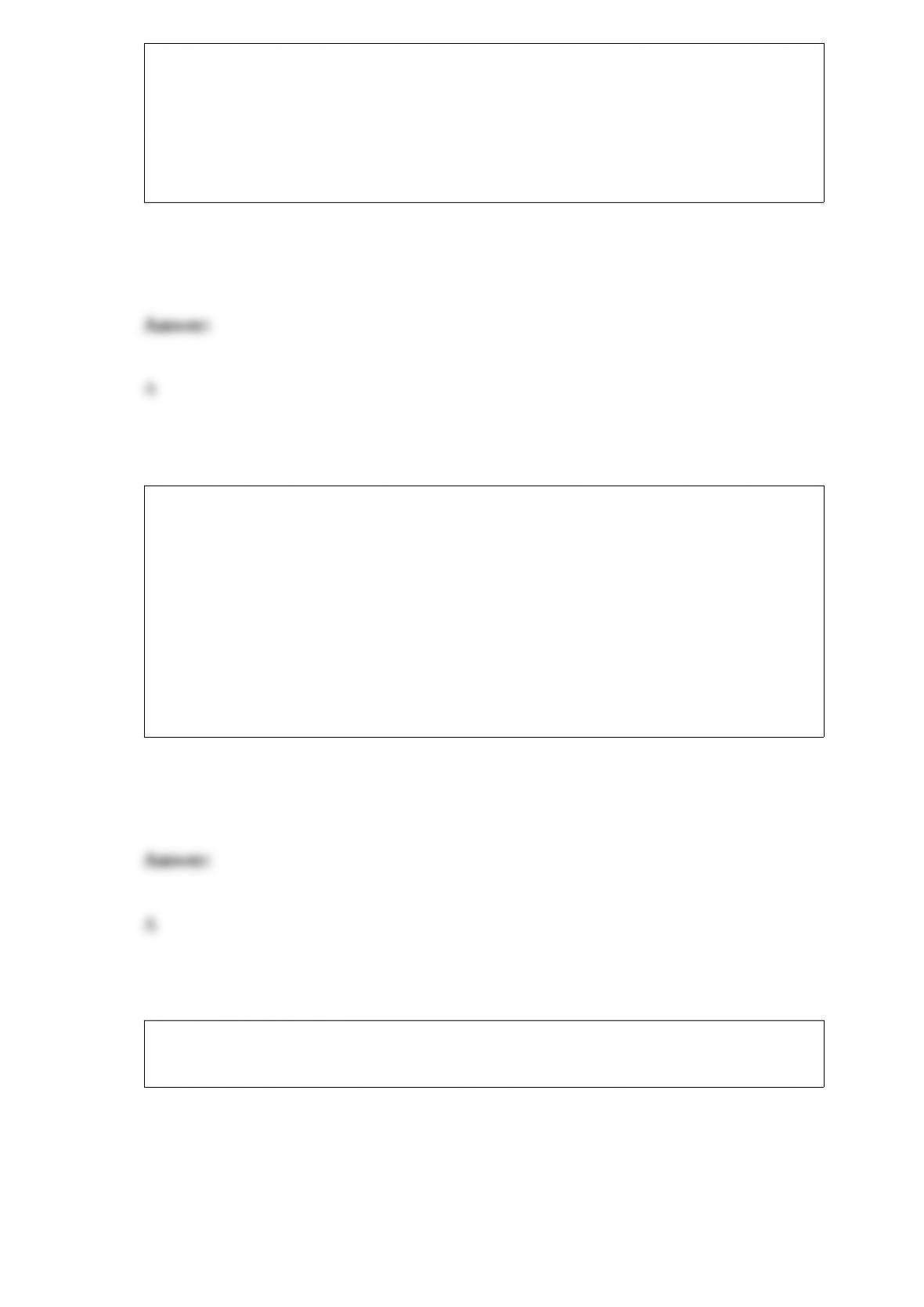

(Table: Marginal Benefit from Additional Streetlights) Look at the table Marginal

Benefit from Additional Streetlights. Suppose that the marginal cost of installing a

streetlight is $6. If Dave had to pay for streetlights on his own, how many streetlights

would there be?

A) 0

B) 1

C) 2

D) 3

If the demand for tires goes down when the price of gas goes up, then tires and gas are:

A) substitutes.

B) complements.

C) both expensive.

D) both inexpensive.

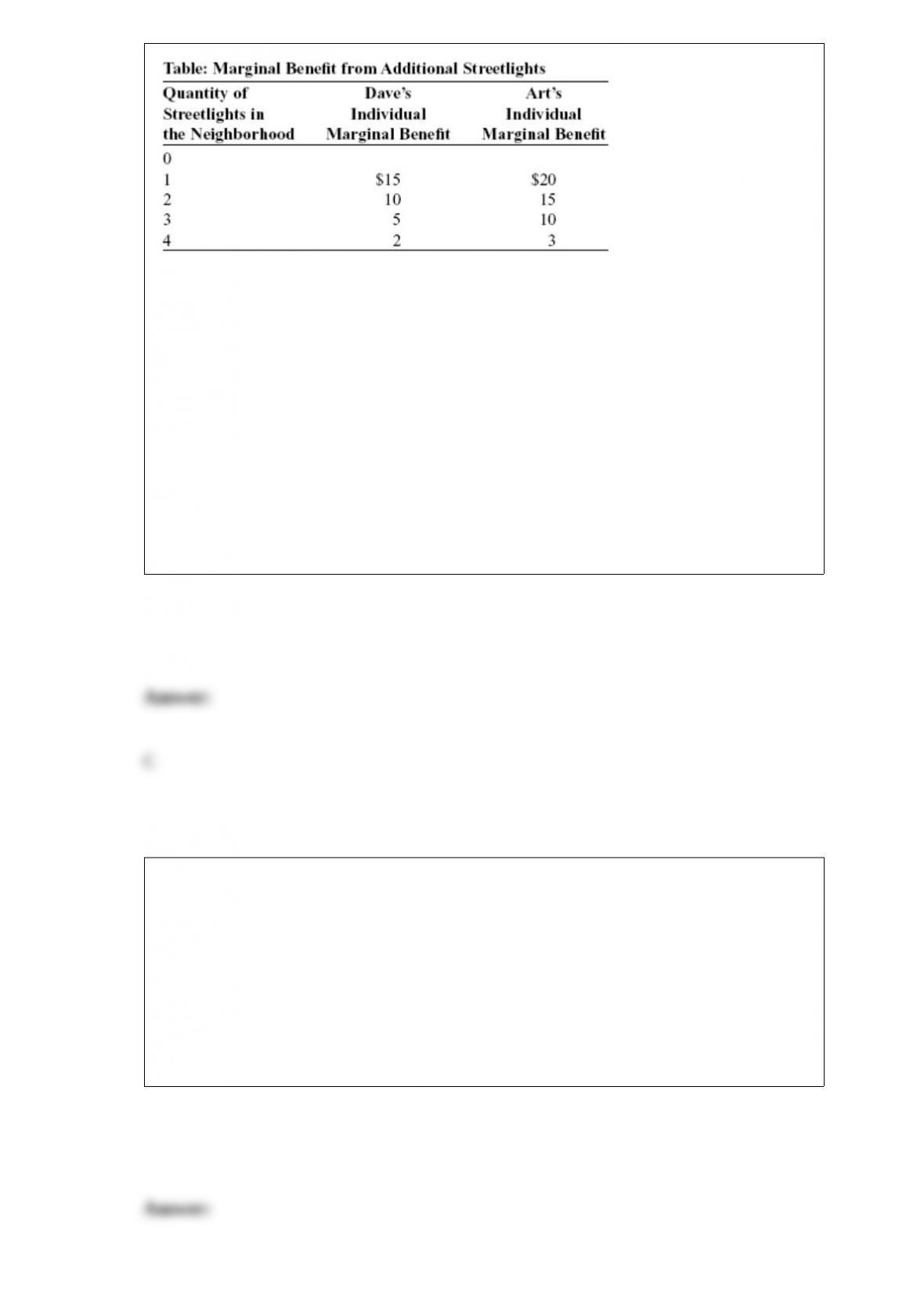

Figure: Guns and Butter

(Figure: Guns and Butter) Look at the figure Guns and Butter. The combination of guns

and butter at point H:

A) can be attained but would cost too much.

B) cannot be attained, given the level of technology and the factors of production

available.

C) has no meaning, since it does not relate to the preferences of consumers.

D) is attainable but would increase unemployment.

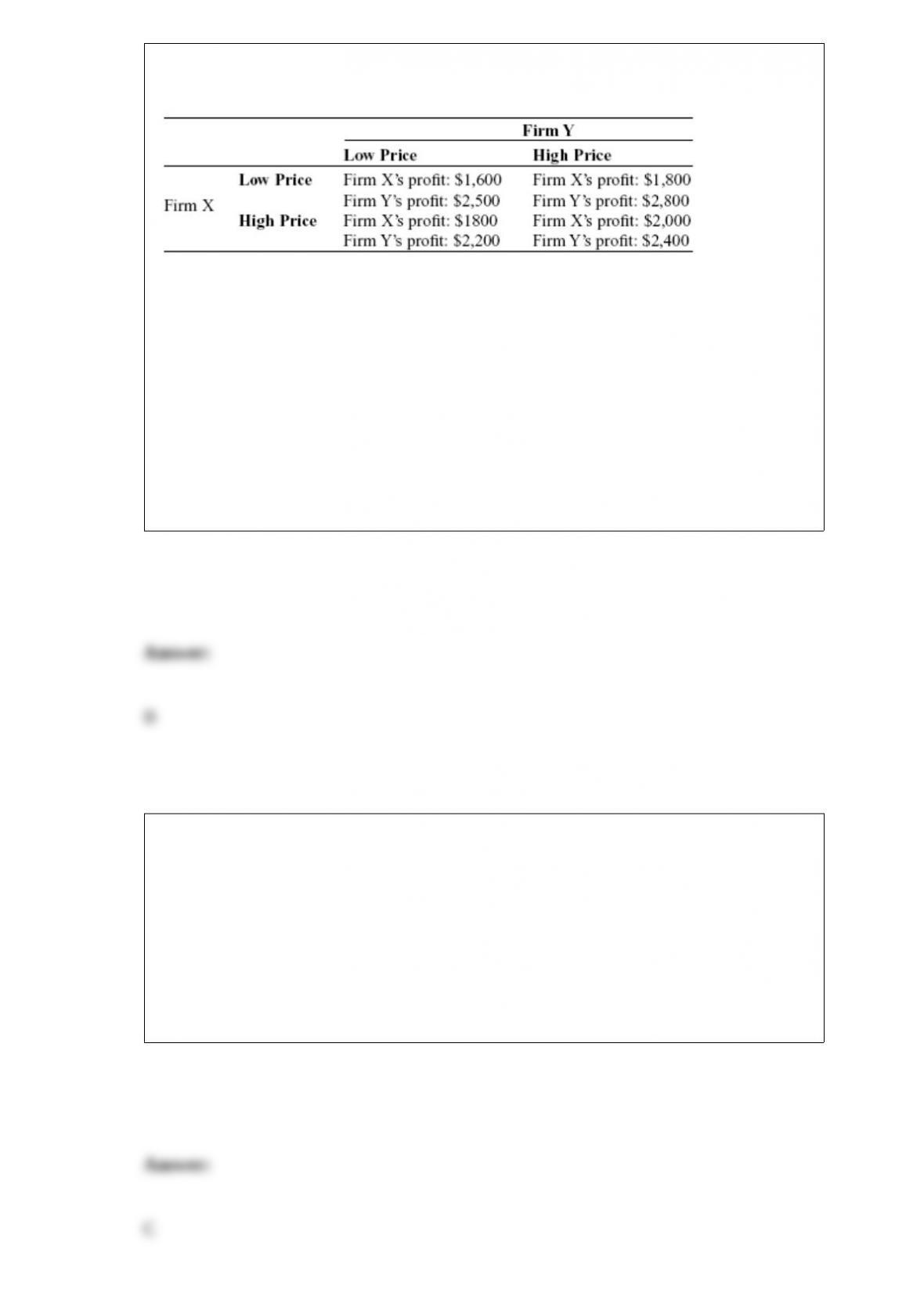

Scenario: Payoff Matrix for Firms X and Y

The following payoff matrix depicts the profits for the only two firms in this

oligopolistic industry.

(Scenario: Payoff Matrix for Firms X and Y) In the scenario Payoff Matrix for Firms X

and Y, if firm X were to choose its dominant strategy, it would:

A) choose a low price.

B) choose a high price.

C) encounter a dilemma, since there are two dominant strategies.

D) allow firm Y to dominate the industry.

If total revenue goes up when the price falls, demand is said to:

A) be price-inelastic.

B) be price unit-elastic.

C) be price-elastic.

D) have positive price elasticity.

The slope of a(n) _____ curve shows the rate at which two goods can be exchanged

_____ the consumer’s _____.

A) marginal utility; by increasing; marginal utility

B) indifference; without affecting; total utility

C) utility; without affecting; budget

D) indifference; without affecting; budget

When we are forced to make choices, we are facing the concept of:

A) human capital.

B) inflation.

C) scarcity.

D) market failure.

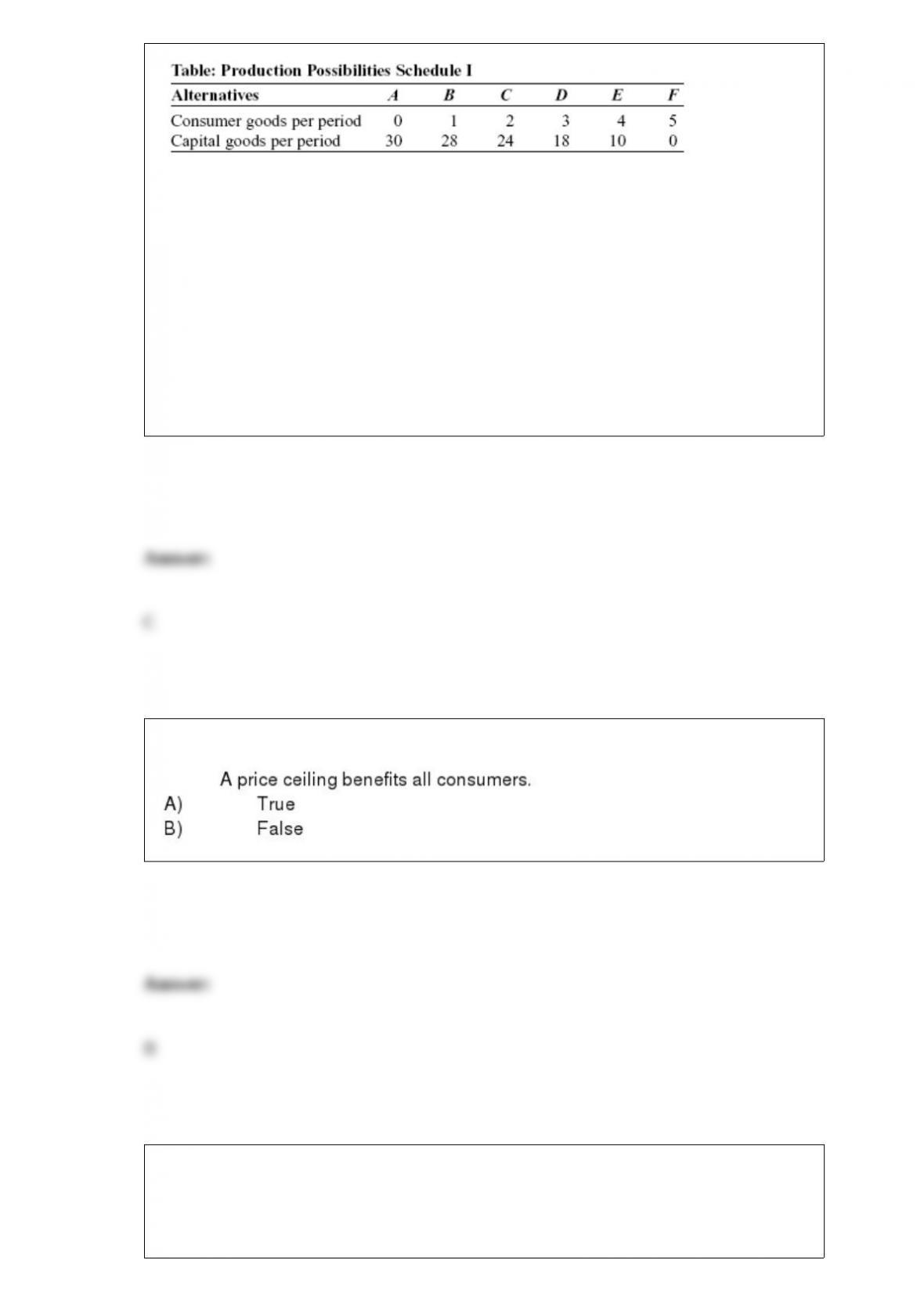

(Table:

Production Possibilities Schedule I) Look at the table Production Possibilities Schedule

I. The opportunity cost of producing the third unit of consumer goods is _____ units of

capital goods.

A) two

B) four

C) six

D) eight

One consequence of equilibrium is that when trying to figure out which checkout line at

the college bookstore is the fastest, one should choose:

A) the line nearest the door.

B) the line farthest from the door.

C) the middle line.

D) randomly; if one line were truly faster, everyone would move to it and it would no

longer be faster.

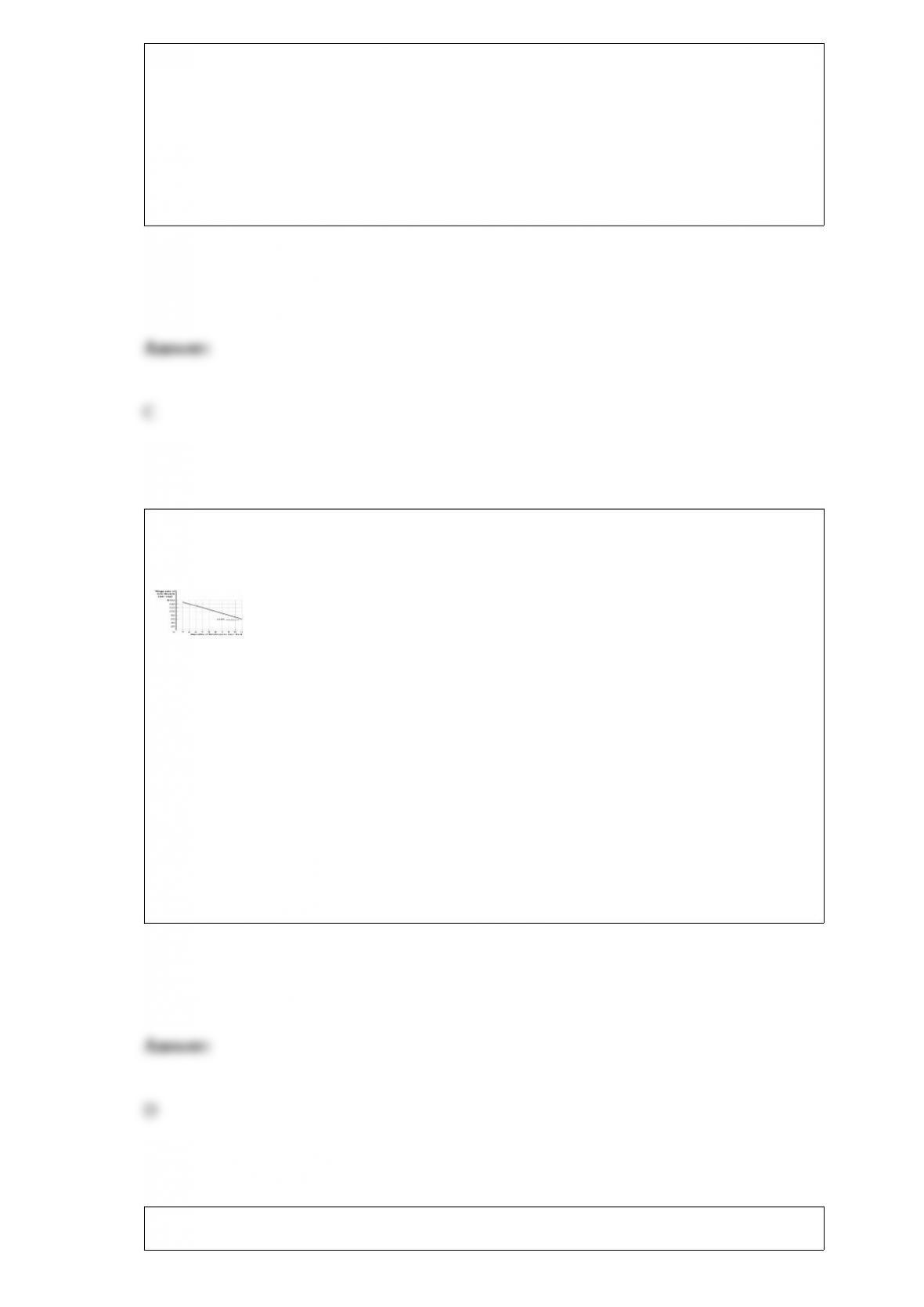

Figure: The Demand for Bricklayers

(Figure: The Demand for Bricklayers) Look at the figure The Demand for Bricklayers.

If the equilibrium market wage rate for bricklayers rises from $80 to $100, the _____

bricklayers will _____.

A) demand for; rise

B) quantity demanded of; rise

C) demand for; fall

D) quantity demanded of; fall

When consumers maximize utility, they obtain:

A) a point of intersection between indifference curves.

B) any intersection of the budget line and the indifference curve.

C) the highest indifference curve that touches their budget constraint.

D) the lowest indifference curve that touches their budget constraint.

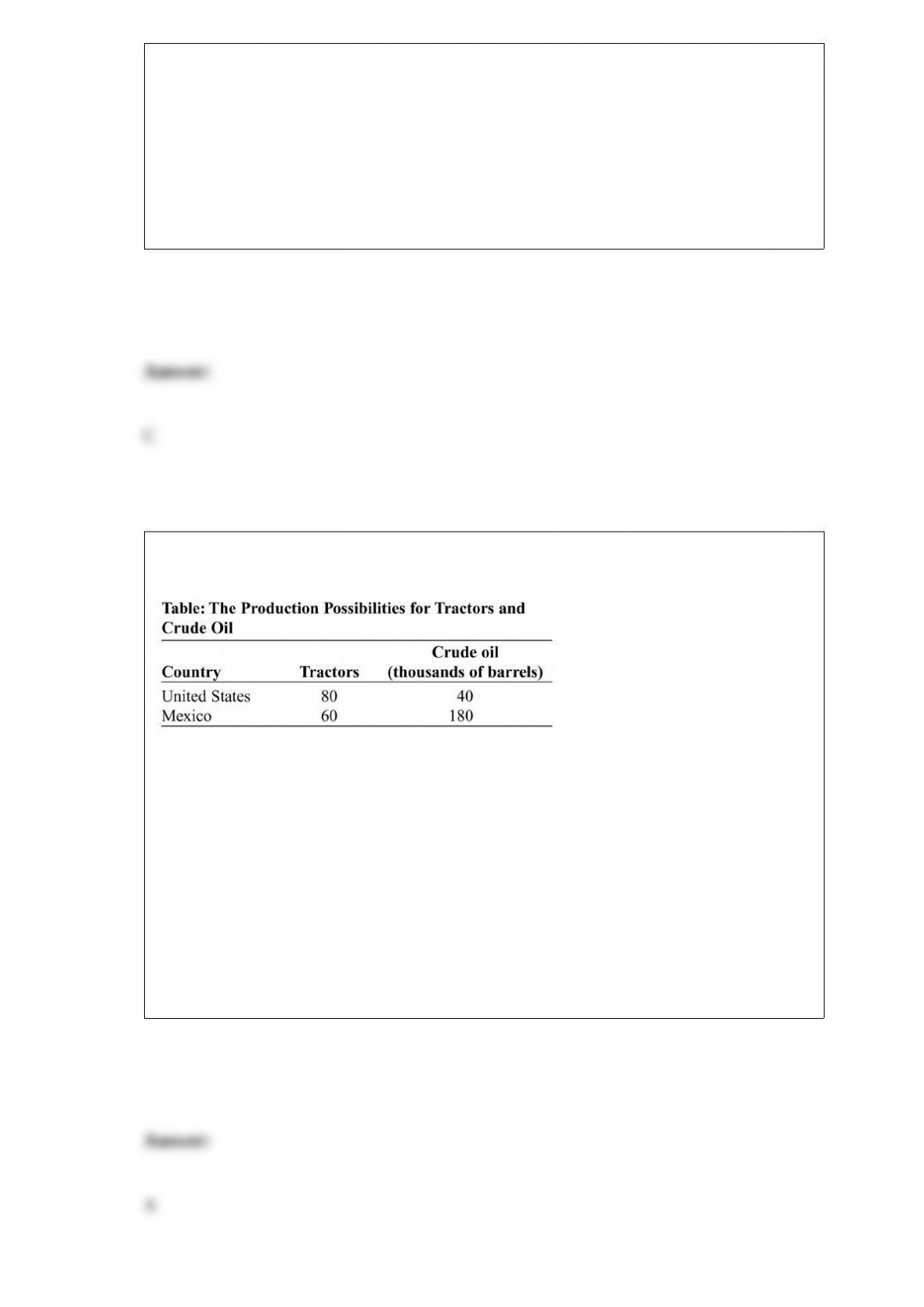

(Table: The Production Possibilities for Tractors and Crude Oil) Look at the table The

Production Possibilities for Tractors and Crude Oil. In the United States the opportunity

cost of producing 30,000 barrels of crude oil is _____ tractors.

A) 60

B) 80

C) 100

D) 120

Marginal revenue:

A) is the slope of the average revenue curve.

B) equals the market price in perfect competition.

C) is the change in quantity divided by the change in total revenue.

D) is the price divided by the change in quantity.

In autarky a country:

A) trades with other countries based on comparative advantage.

B) trades with other countries based on absolute advantage.

C) does not trade with other countries.

D) follows the Heckscher”Ohlin model of trade behavior.

A decrease in the price of a good will result in:

A) an increase in demand.

B) an increase in supply.

C) an increase in the quantity demanded.

D) more being supplied.

According to the _____ principle, those can afford it should pay more tax.

A) ability-to-pay

B) tax fairness

C) benefits

D) affordability