1) Suppose that policymakers are considering placing a tax on either of two markets. In

Market A, the tax will have a significant effect on the price consumers pay, but it will

not affect equilibrium quantity very much. In Market B, the same tax will have only a

small effect on the price consumers pay, but it will have a large effect on the

equilibrium quantity. Other factors are held constant. In which market will the tax have

a larger deadweight loss?

a.Market A

b.Market B

c.The deadweight loss will be the same in both markets.

d.There is not enough information to answer the question.

2) The marginal product of any factor of production depends on

a.the quantity of the factor used.

b.the price of the final good.

c.the demand for the final good.

d.All of the above are correct.

3) Two variables that have a positive correlation move in the same direction.

a.True

b.False

4) Consider the market for medical doctors. Suppose the opportunity cost of going to

medical school decreases for many individuals. Suppose it generally takes about ten

years to become a practicing doctor. Holding all else constant, in ten years the

equilibrium wage for doctors will

a.increase.

b.decrease.

c.not change.

d.It is not possible to determine what will happen to the equilibrium wage.

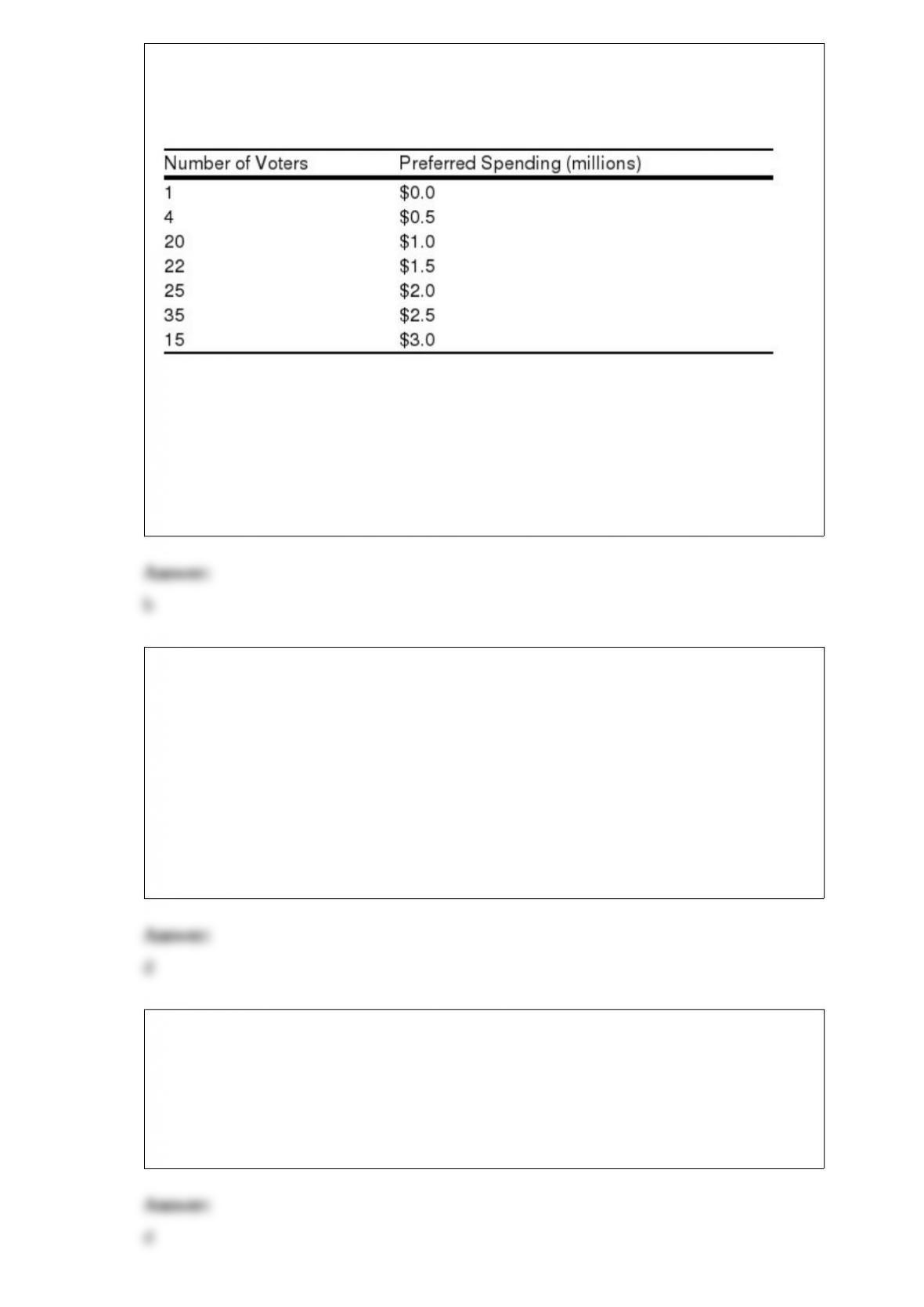

5) Table 22-21

The following table shows the number of voters preferring various amounts of spending

to develop a river to make it more attractive for canoeing and kayaking.

Refer to Table 22-21. Suppose the voters are asked to choose between $1 million and

$2.5 million. If all voters cast a vote for the spending amount closest to their own

preference, how many votes will the $1 million spending amount receive?

a.25

b.47

c.72

d.102

6) The nation of Aquilonia has decided to end its policy of not trading with the rest of

the world. When it ends its trade restrictions, it discovers that it is importing incense,

exporting steel, and neither importing nor exporting rugs. We can conclude that

Aquilonia’s new freetrade policy has

a.increased consumer surplus and producer surplus in the incense market.

b.increased consumer surplus in the steel market and left producer surplus in the rug

market unchanged.

c.decreased consumer surplus in both the steel and rug markets.

d.decreased consumer surplus in the steel market and increased total surplus in the

incense market.

7) Refer to Figure 9-25. Suppose the government imposes a tariff of $5 per unit. The

amount of revenue collected by the government from the tariff is

a.$50.

b.$100.

c. $150.

d. $200.

8) A university’s football stadium is always sold out, and students who wait in line for

hours may be turned away. This indicates

a.the ticket price is above the equilibrium price.

b.the ticket price is below the equilibrium price.

c.the ticket price is at the equilibrium price.

d.nothing about the equilibrium price.

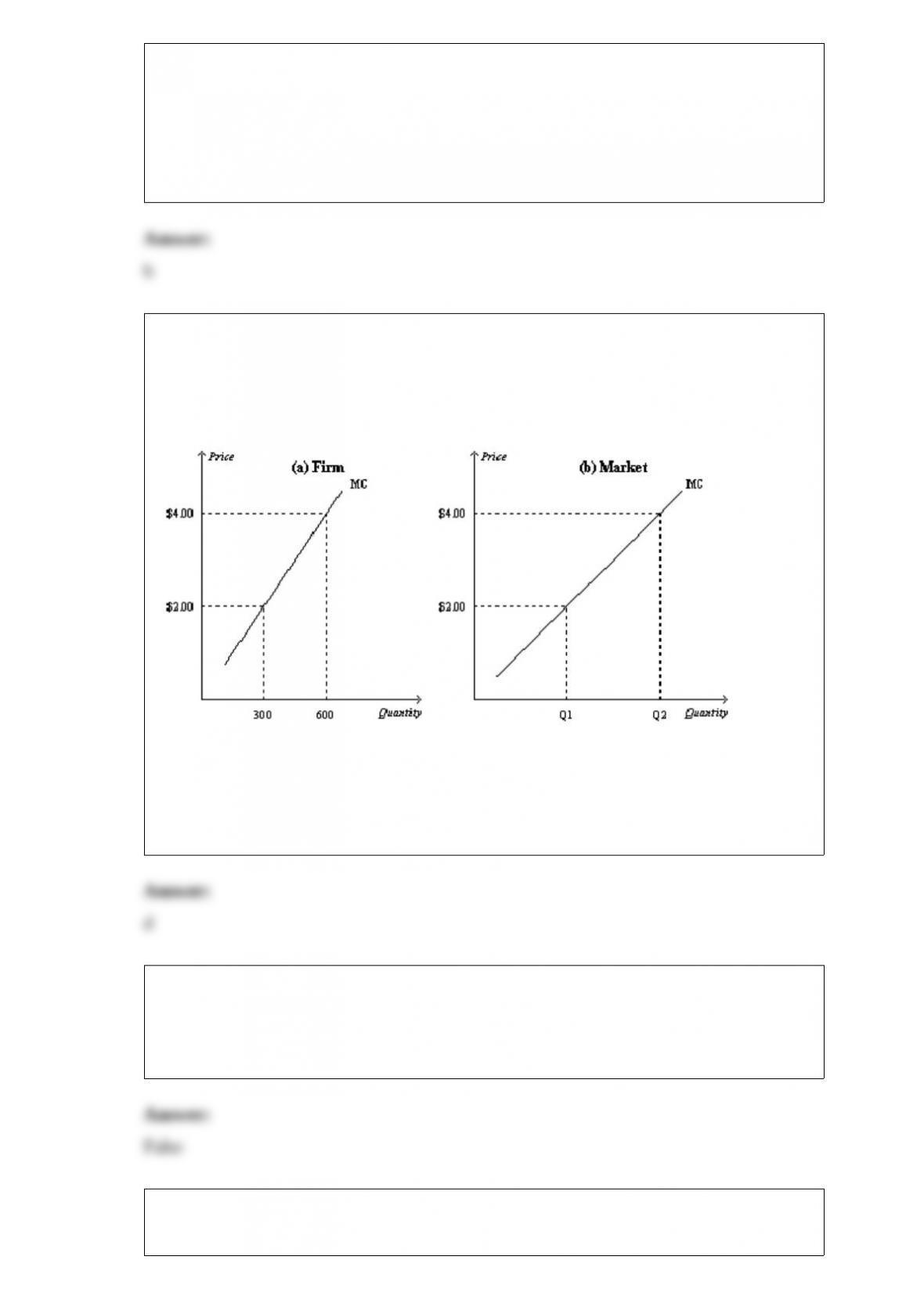

9) Figure 14-10

In the figure below, panel (a) depicts the linear marginal cost of a firm in a competitive

market, and panel (b) depicts the linear market supply curve for a market with a fixed

number of identical firms.

If there are 500 identical firms in this market, what is the value of Q2?

a. 12,000

b. 60,000

c. 240,000

d. 300,000

10) In a long-run equilibrium where firms have identical costs, it is possible that some

firms in a competitive market are making a positive economic profit.

a.True

b.False

11) In the market for oil in the short run, demand

a.and supply are both elastic.

b.and supply are both inelastic.

c.is elastic and supply is inelastic.

d.is inelastic and supply is elastic.