What does it mean to say that a firm has been made liable?

a. The firm is legally responsible to compensate other parties for damage.

b. The firm has begun to treat any external costs as private costs.

c. The firm has received the property rights to a disputed resource.

d. The firm is required to pay a Pigou tax to the government.

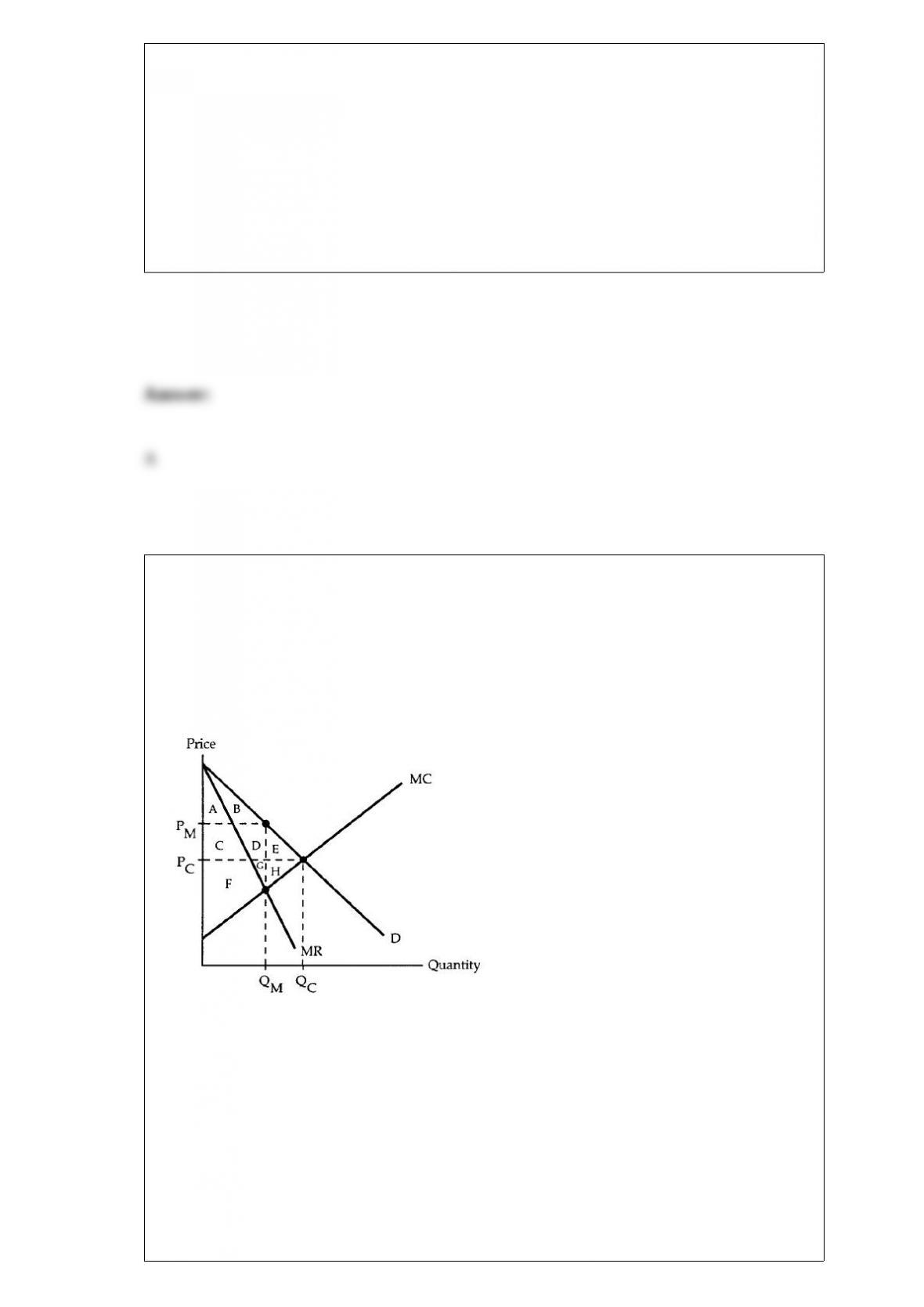

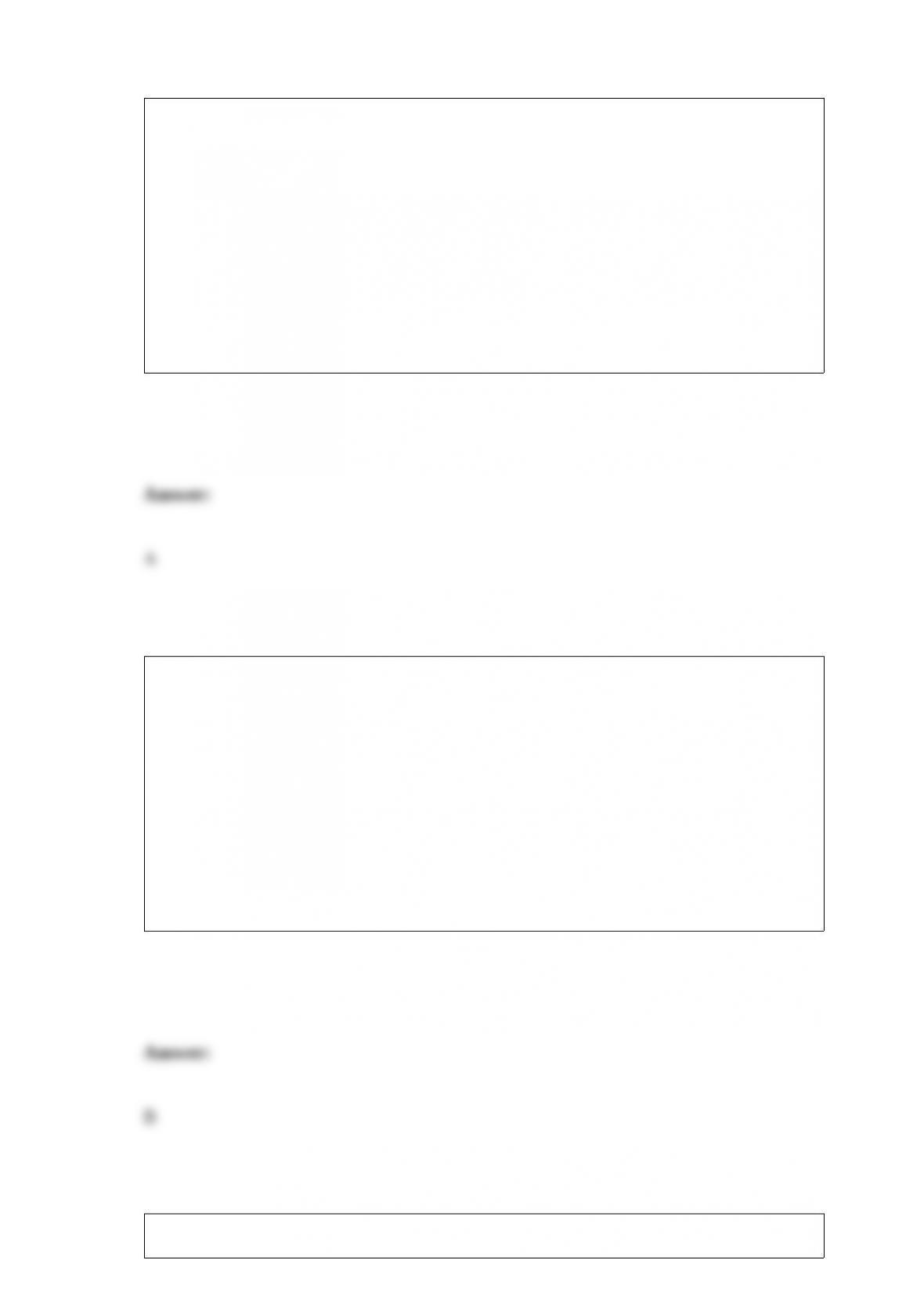

Market Diagram

The following questions refer to the accompanying market diagram. PC and QC are the

equilibrium price and quantity if the firm behaves competitively, and PM and QM are

the equilibrium price and quantity if the firm is a simple monopoly.

The difference between producer’s surplus as a monopolist and producer’s surplus when

setting price at what would exist in a competitive market is

a. Area C + D + E – G – H.

b. Area C + D – H.

c. Area C + D + E – A – B.

d. Area E + H.

Assume chiropractic care is provided by a competitive industry. A new government

regulation requires each chiropractor to take a costly new exam for certification. What

happens to the price of dental care?

a. The price of chiropractic care rises in the short run and rises further in the long run.

b. The regulation will cause higher prices in the short run, but it will have no long-run

impact.

c. There is no change in the short run, but chiropractors will exit and prices will rise in

the long run.

d. The exam is a sunk cost, so the price of chiropractic care does not change in either

the short run or the long run.

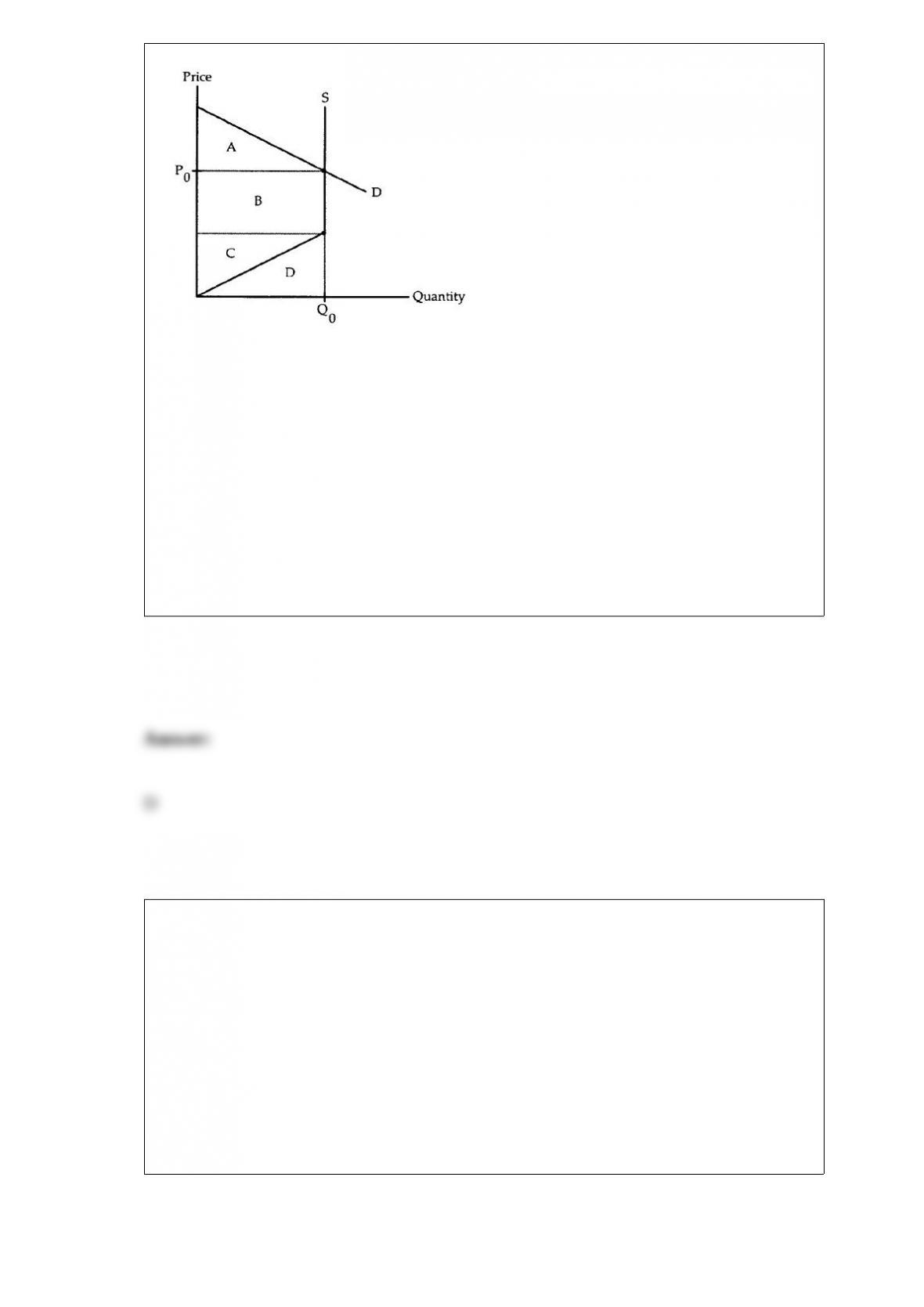

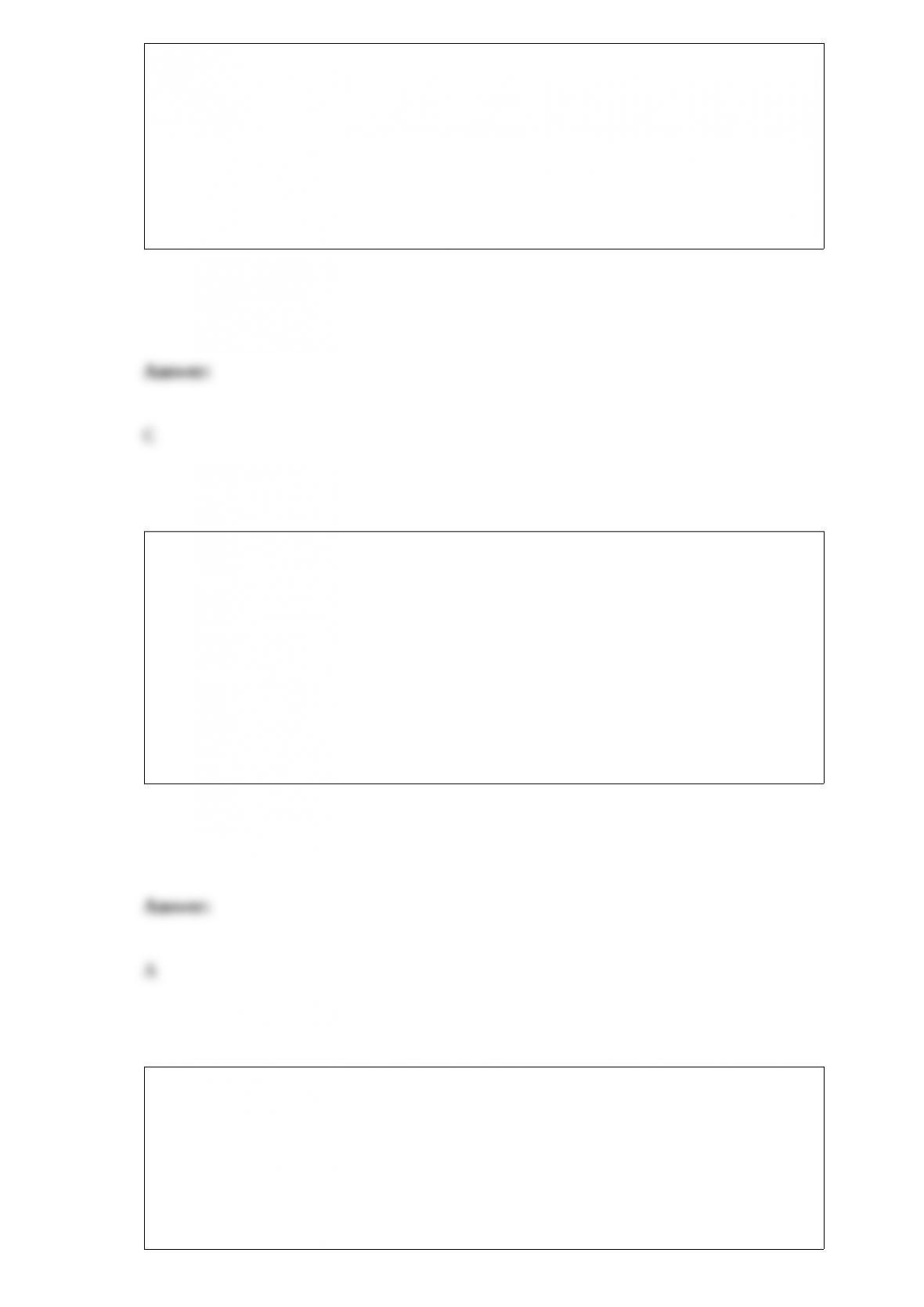

Resource Supply/Demand

The following questions refer to the accompanying graph, which shows the supply and

demand for a resource. The owner of the resource is receiving the price P0 and is

providing the quantity Q0.

What does area D represent?

a. The value that Q0 units of the resource gives to demanders.

b. The revenue generated from selling Q0 units of the resource.

c. The rent that resource owner earns from providing Q0 units.

d. The minimum payment needed for the resource owner to supply Q0 units.

There are two states of the world. In state one the person receives one hundred dollars.

In state two the person receives fifty dollars. If the person is rational and their expected

return is $87.50, then the probability with which state one occurs must be

a. 0.25.

b. 0.50.

c. 0.75.

d. 1.00.

Suppose the government spends $5,000 per person this year. The market for borrowing

and lending is competitive, and the market interest rate is 6%. Which of the following

plans to finance the government’s spending is best for consumers?

a. A tax of $5,000 per person this year.

b. A tax of $5,300 per person next year.

c. An annual tax of $300 per person forever.

d. All of the above plans have the same effect on consumers.

All points on the firm’s expansion path

a. give the firm the maximum possible profit.

b. minimize the firm’s cost of producing some level of output.

c. have the same long-run average cost.

d. make the marginal product of labor equal to the marginal product of capital.

For a firm in the long-run, an increase in the market wage rate will cause it to reduce

the employment of labor. With fewer workers, the firm’s marginal revenue product for

capital

a. shifts downward leading the firm to use less capital.

b. shifts upward leading the firm to use more capital.

c. twists so that is becomes more elastic

d. is not affected.

Hillary and Bill are playing backgammon. Hillary offers to place a wager on the game’s

outcome at fair odds. Bill is risk-averse and believes that he has a 60% chance of

winning the game. When will Bill accept the wager?

a. Always.

b. When the wager is sufficiently small.

c. When the wager is sufficiently large.

d. Never.

Which of the following is most likely to be a variable cost in the short run?

a. A fee paid to obtain a license.

b. The cost of owning machinery.

c. The energy costs of running a factory.

d. Rent payments for office space.

Suppose a permanent technological improvement raises labor’s marginal productivity.

Whether or not workers own capital, we can conclude that

a. the wage rate will rise.

b. employment will fall.

c. the supply of labor will rise.

d. the demand for labor will fall.

When an industry’s demand curve for labor is derived from the individual firms’

demand curves, what complication must be taken into account?

a. Adjustments in the amount of capital employed.

b. The factor-price effect.

c. Changes in the price of the firms’ product.

d. Monopsony power.

When will an individual’s indifference curves be identical with the iso-expected value

lines?

a. Never.

b. When the individual is risk averse.

c. When the individual is risk neutral.

d. When the individual is risk preferring.

If a worker has chosen a quantity of labor where the marginal value of leisure exceeds

the wage rate, she would be better off by

a. choosing less leisure.

b. providing fewer hours of labor.

c. providing more hours of labor.

d. staying at this combination of labor and consumption.

A factor-price effect occurs when increases in the industry’s output

a. attract new firms to the industry.

b. raise the cost of a variable input.

c. cause new subindustries to be developed.

d. result in lower prices for consumers.

If labor and capital are complements in production, then an increase in the amount of

capital will

a. reduce the firm’s demand for labor.

b. raise the firm’s marginal cost of production.

c. cause the scale effect to outweigh the substitution effect.

d. increase labor’s marginal product.

A positive theory of common law, in which the positions of the courts are predicted

based on the assumption that they are attempting to promote efficiency, is proposed by

a. Pigou.

b. Coase.

c. Posner.

d. Epstein.

If the supply of hotel rooms falls and all other relevant factors remain unchanged, then,

a. the demand for hotel rooms will fall.

b. the quantity demanded of hotel rooms will fall.

c. the demand for hotel rooms will rise.

d. the quantity demanded of hotel rooms will rise.

Suppose that the due to technological innovations, the absolute price of a recordable

CD declines by 25% while the absolute price of a recordable cassette tape declines by

10%. In this situation, the price of the CD relative to the price of a tape

a. falls.

b. rises.

c. remains the same.

d. changes unpredictably.

Tax Problem. Consider a perfectly competitive market were demand is Q = 100 – P and

Supply isQ = P – 10.

The deadweight loss due to a $10 per unit consumption tax is

a. zero.

b. $10.

c. $25.

d. $50.

Suppose a duopoly is operating in a market where demand is linear and marginal costs

are constant. We can conclude that the total output supplied by the duopoly is

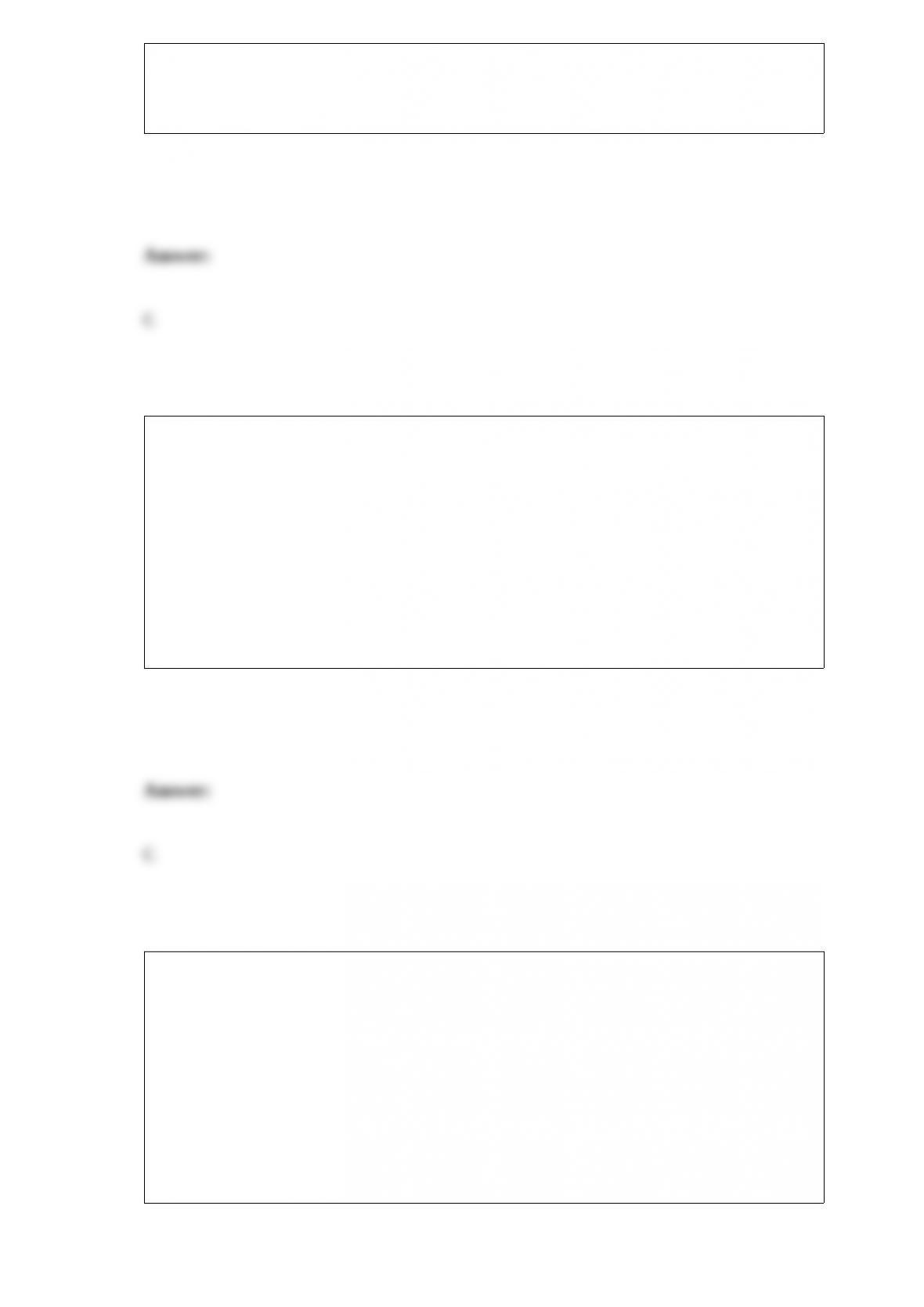

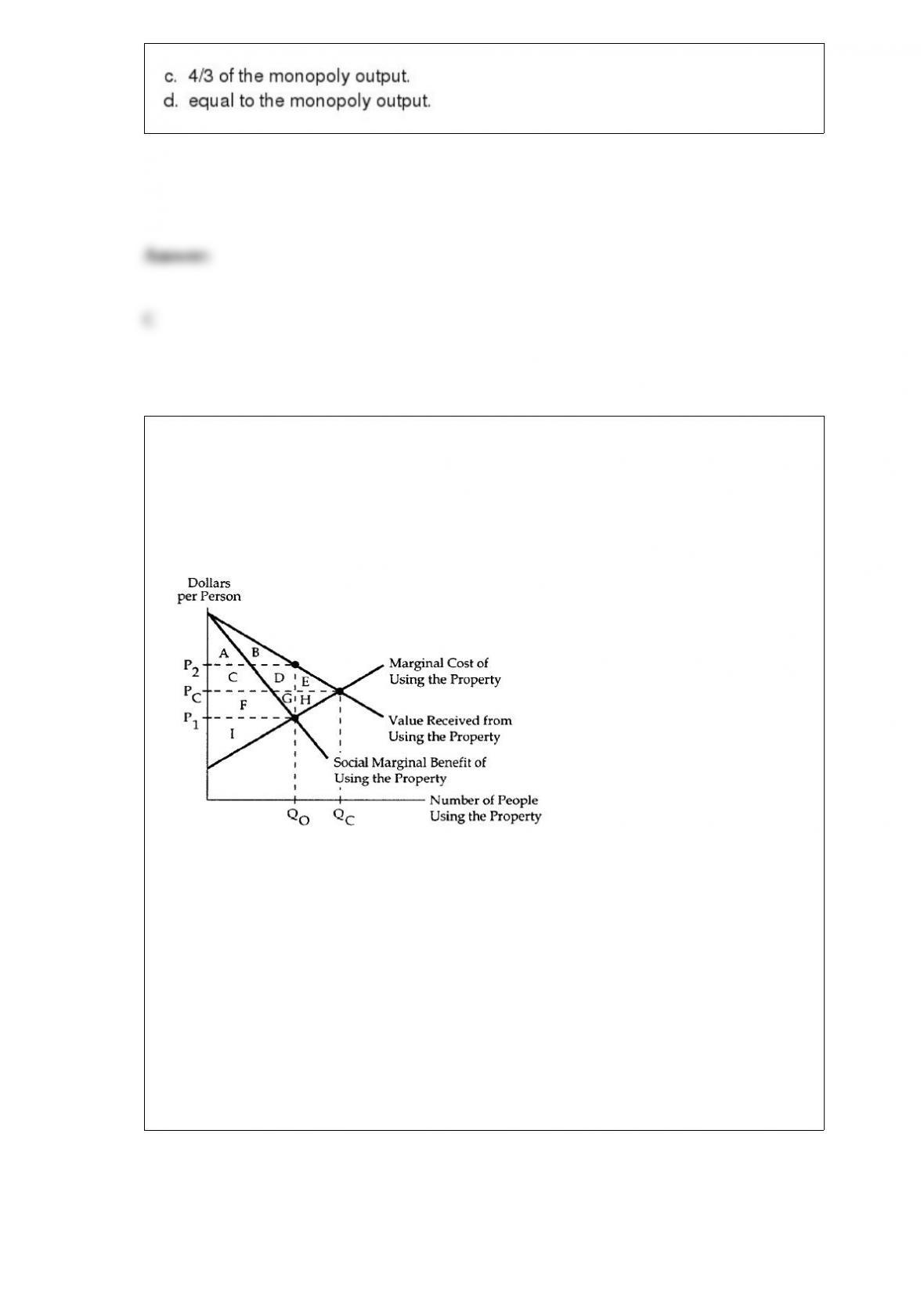

Common Property II

The following questions refer to the accompanying diagram, which shows the benefits

and costs associated with the use of a common property.

Refer to Common Property II. Suppose the common property becomes privately owned.

If the owner charges a competitive entrance fee for the right to use the property, social

gain will equal

a. area C + D + F + G + I.

b. area F + G + H + I.

c. area A + B + C + D + F + G + I.

d. area A + B + C + D + E + F + G + H + I.

All of the following are true of models except:

a. they simplify reality.

b. they are good if they make predictions that align with real world observations.

c. they are used exclusively by economists.

d. supply/demand analysis is an example of a model.

When Homer has 5 doughnuts, his marginal value is 15¢ per doughnut. We can

conclude that Homer

a. places a value of 3¢ on each doughnut he owns.

b. needs to purchase more than 5 doughnuts to reach his optimum.

c. receives 75¢ worth of total satisfaction from his 5 doughnuts.

d. would refuse to pay more than 15¢ for a sixth doughnut.

Advocates of limiting anti-trust action to cases which would promote economic

efficiency believe that

a. courts should consider the distribution of income between producers and consumers.

b. the welfare of small firms should be a factor in pursuing anti-trust action.

c. preventing mergers that would benefit consumers constitutes a misapplication of the

law.

d. more competition is always preferred to less.

Bonzo is in business for himself making and selling Easter baskets. His daily cost for

wicker is $100 and his daily revenue is $120. Bonzo quit his job at the Basket Weaving

factory where he earned $15 a day, to enter the Easter basket business. Given this

information, we know that his accounting profit

a. is $120 while his economic profit is $105.

b. and economic profit are both $20.

c. is $20 while his economic profit is $5.

d. and economic profit are both $5.

If labor and capital are substitutes in production, then an increase in the amount of

capital will

a. reduce the total product associated with each quantity of labor.

b. decrease the marginal product of labor.

c. increase the marginal product of labor.

d. have no effect on labor productivity.

When will consumers’ surplus overstate the actual gains received by consumers?

a. When allocation decisions are not made on the basis of price.

b. When the commodity is not equally divided among consumers.

c. When all consumers place the same marginal value on the good.

d. When the distribution of goods is Pareto optimal.

Consider a potato farmer whose cost of production is $2.25 a bushel. In May, she

expects that the potato when harvested in July will sell for either $2 a bushel or $3.00.

She could avoid the probability of a loss by contracting to deliver the potatoes in July at

$2.50. Such a contract is traded in a

a. futures market.

b. spot market.

c. portfolio market.

d. diversified market.

A firm is defined in Economics as

a. a corporation that creates demand for the goods it produces.

b. an entity that produces and sells goods that individuals demand.

c. an individual or group of individuals providing public services at no charge.

d. any group of individuals seeking to increase their income.

Coase argues that every case of externalities

a. has a clearly identifiable cause.

b. requires government intervention if efficiency is to be achieved.

c. can be traced back to a principal-agent problem.

d. is reciprocal in nature.

When does a higher wage rate lead to an increase in the number of work hours supplied

by laborers?

a. Always.

b. When the substitution effect outweighs the income effect.

c. When the income effect outweighs the substitution effect.

d. Never.

A person is seen placing a wager on the Super Bowl. It can be concluded that

a. the person is risk-preferring.

b. the person is either risk-averse or risk-neutral, but not risk-preferring.

c. the person is either risk-neutral or risk-preferring, but not risk-averse.

d. we need more information before making a conclusion regarding this person’s

attitudes towards risk.

The Cournot model specifies how two firms in a duopoly compete in terms of quantity.

Briefly describe how the outcome of Cournot duopoly competition relates to the

outcomes of perfect competition and monopoly in terms of output and market

efficiency/inefficiency. Can you be more precise about the relation between Cournot,

monopoly, and perfectly competitive outputs if you know that demand is linear and

marginal costs are constant? Explain.

The cost of producing furniture is not the resources used in its production, but the

alternative uses for those resources.

Whether a good is distributed by a social planner or a market system, the area beneath

the demand curve out to the quantity available accurately measures the value consumers

receive.

The substitution effect on labor always decreases the amount of labor employed when

the wage rate goes up.

Beginning in 2010, a local government in Georgia is instituting a tax on owners of land

at a flat rate of $100 per acre every year.

A doubling of all prices has the same effect on the budget line as reducing income by

half.

An HBO broadcast over cable television is rival in consumption but non-excludable.

A risk-free basket has only one possible outcome.

A competitive firm will exit the industry in the long run if the price of its product falls

below its average cost.

The number of firms in an industry is fixed in the short run.

Assume that there are only two good for a consumer to purchase. Explain why a

consumer can not be maximizing utility if both goods are inferior.

Costs are forgone opportunities.

If marginal value is constant, then the consumer’s indifference curves are straight lines.

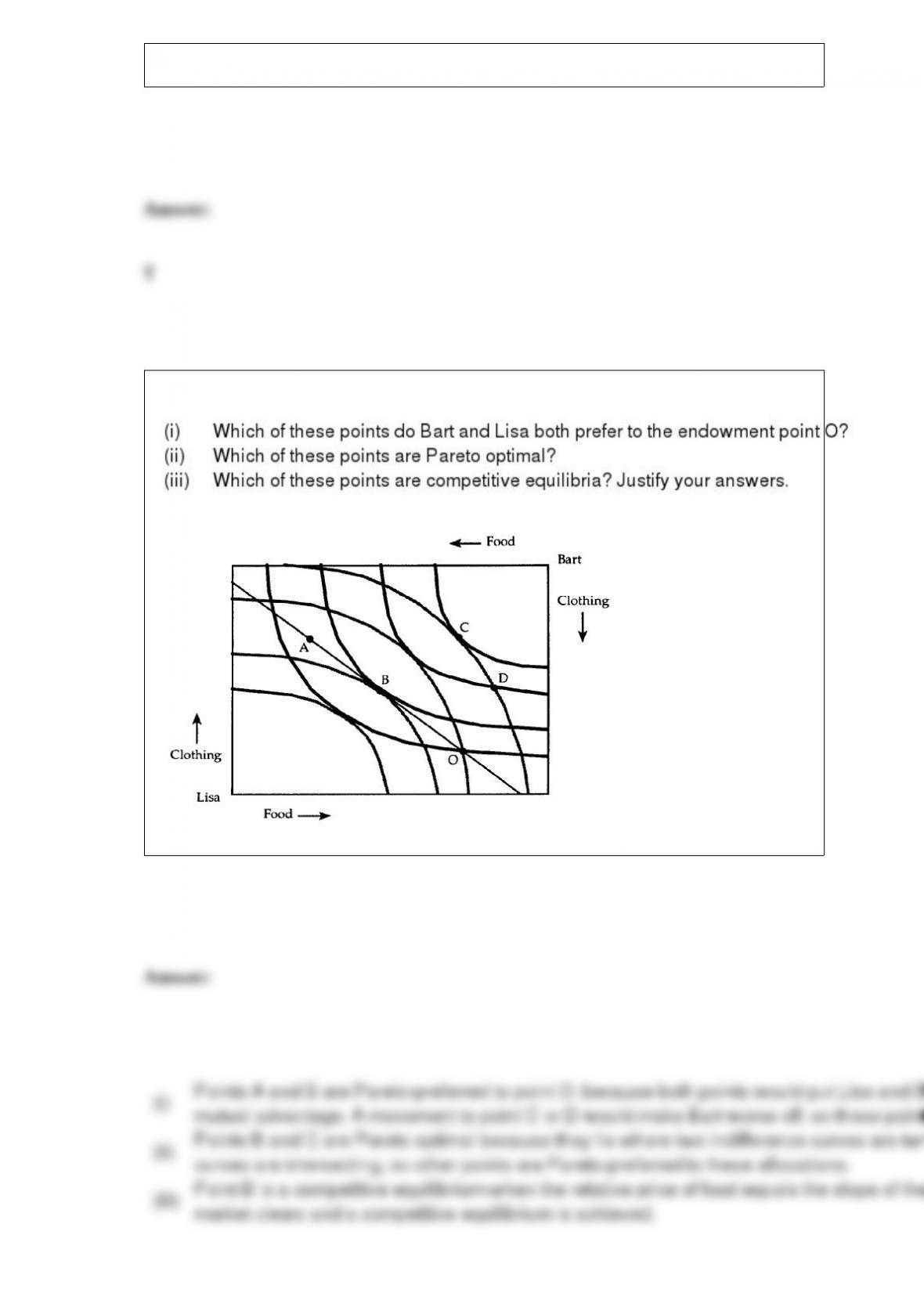

Consider points A, B, C, and D shown in the accompanying Edgeworth box diagram.

A change in a variable cost causes a parallel upward shift in the marginal cost curve.

Average Variable Cost can always be expressed as the ratio of the price of labor to the

Average Product of Labor.

Whether or not people have identical tastes, the marginal entrant is indifferent about

using a common property.

Derived demand for an input is the process by which individual firm’s demand for labor

are aggregated to get the industry demand for labor.