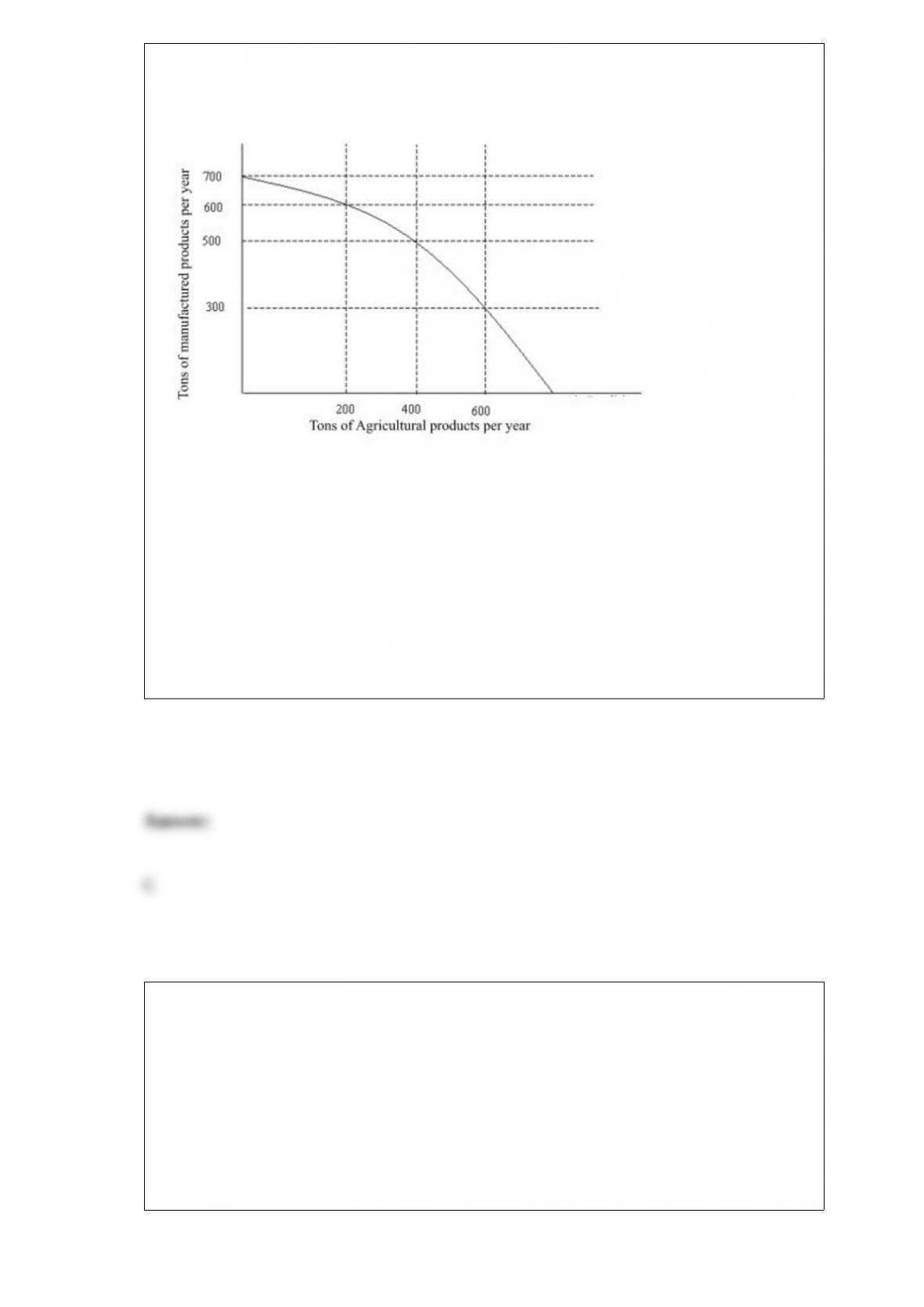

On the production possibilities curve in Figure 2.1 the gain from decreasing

manufacturing production from 700 tons to 500 tons is:

Figure 2.1

A) 700 tons of agriculture.

B) 500 tons of agriculture.

C) 200 tons of agriculture.

D) 100 tons of agriculture.

The market supply curve is:

A) downward sloping and is flatter than an individual’s supply curve.

B) upward sloping and is flatter than an individual’s supply curve.

C) downward sloping and is steeper than an individual’s supply curve.

D) upward sloping and is steeper than an individual’s supply curve.

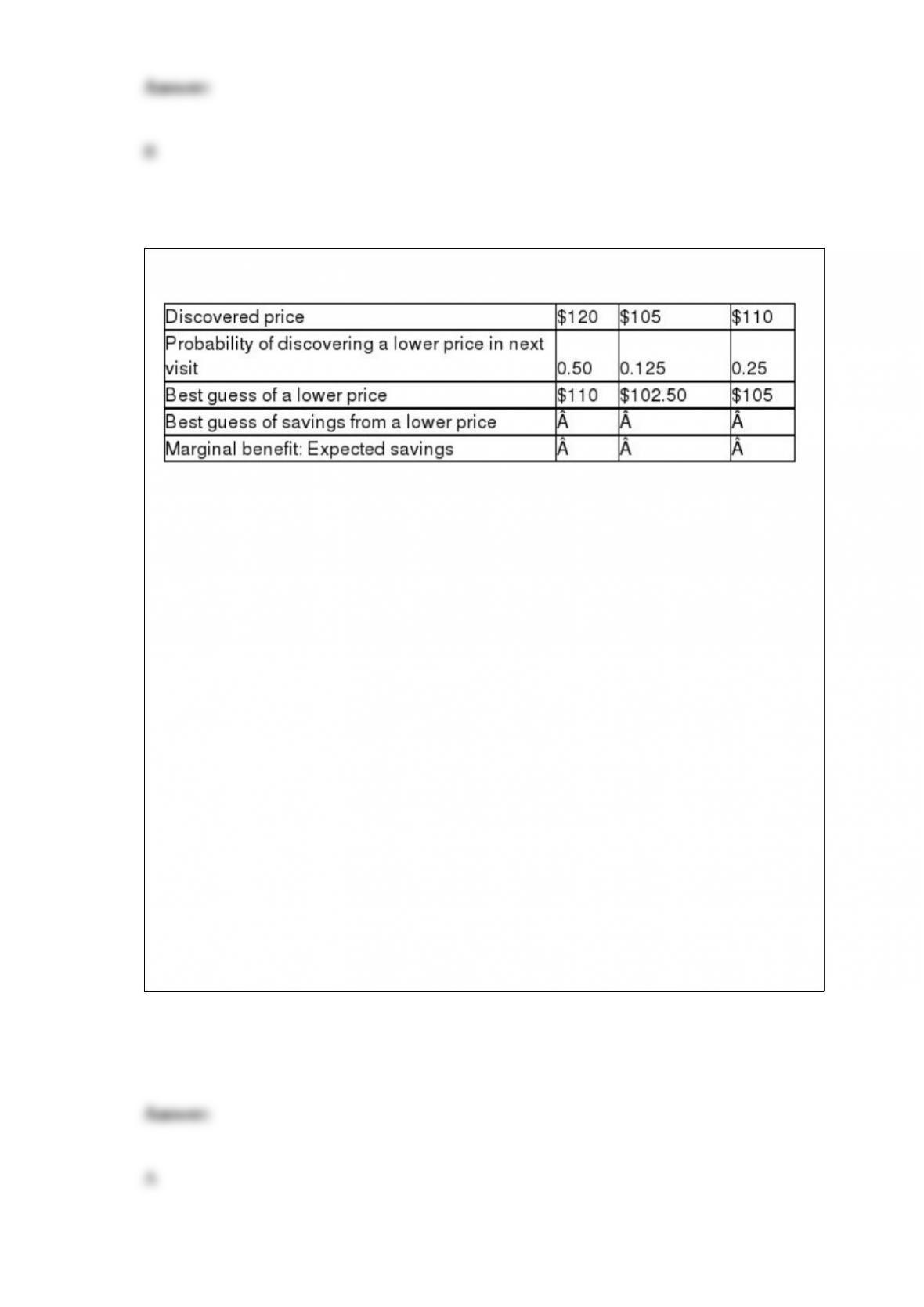

Table 14.5

Table 14.5 contains data on the marginal benefit of searching for a lower price for a

digital camera.

The price of the camera ranges from $100 at the lowest price store to $140 at the

highest price store.

For any randomly selected store, any price from the low price to the high price is

equally likely.

The marginal cost of visiting each store is constant at $1.50 per visit.

Refer to Table 14.5. At the discovered price of $105, the expected savings from visiting

another store is:

A) $0.3125.

B) $1.25.

C) $2.50.

D) $5.00.

A private good is a good that:

A) is nonrival.

B) is not excludable.

C) is provided only by private sectors.

D) is consumed by a single person or household.

A situation in which one side of an economic relationship takes undesirable or costly

actions that the other side of the relationship cannot observe. This kind of situation is

called:

A) adverse selection.

B) moral hazard.

C) thick markets.

D) an injunction.

Recall the Application about the external cost of young drivers to answer the

following question(s).

Recall the Application. If the external costs of drivers on average could be internalized

by a vehicle mileage traveled tax of 4.4 cents per mile, then you would expect that to

fully internalize the external costs of accident by drivers younger than 25 to be:

A) 4.4 cents per mile.

B) lower than 4.4 cents per mile.

C) higher than 4.4 cents per mile.

D) zero as there are no externalities in driving.

If a firm has already paid or has agreed to pay for something we call it:

A) a fixed cost.

B) a spent cost.

C) a sunk cost.

D) a lost cost.

For a firm in a perfectly competitive market, at the profit maximizing level of output:

A) Price = Marginal Revenue = Marginal Cost.

B) Price > Marginal Revenue > Marginal Cost.

C) Price < Marginal Revenue < Marginal Cost.

D) Price > 0 and Marginal Revenue = 0.

When a profit-maximizing firm in monopolistic competition is in long-run equilibrium:

A) the demand curve it faces will be perfectly elastic.

B) its marginal cost will be falling.

C) its price will be greater than its marginal cost.

D) its marginal revenue will be greater than its marginal cost.

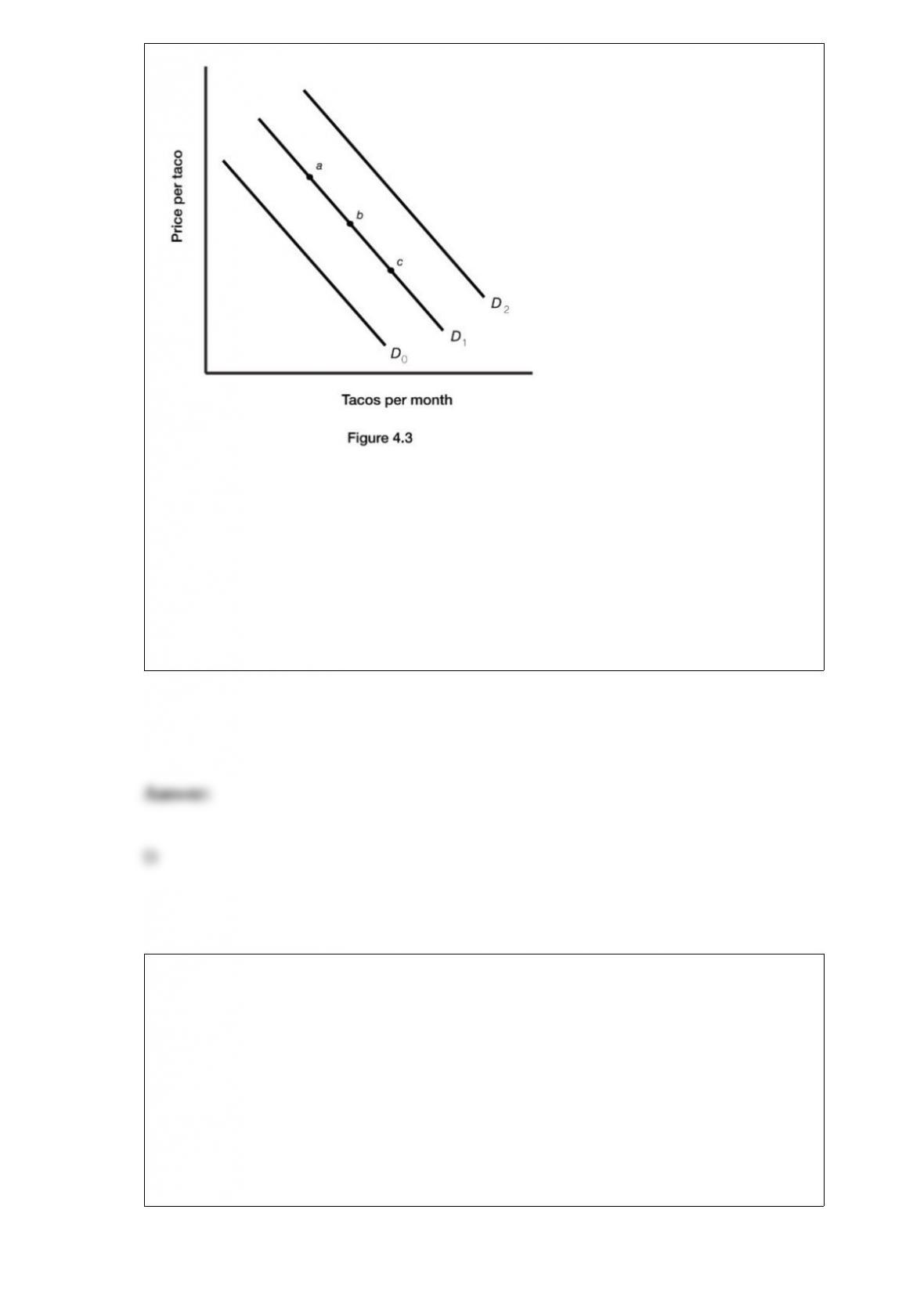

Figure 4.3 illustrates the demand for tacos. A successful advertising campaign to sell

tacos would bring about a movement from:

A) point a to point b.

B) point c to point b.

C) D2 to D1.

D) D0 to D1.

Suppose that the quantity supplied of cars exceeds the quantity of cars demanded. We

would expect that:

A) the price of cars will increase.

B) the price of cars will decrease.

C) the supply will increase to meet the demand.

D) the demand will decrease to meet the supply.

One role government can play in addressing market failure is to:

A) enforce the rules of exchange.

B) increase economic uncertainty.

C) promote imperfect competition.

D) facilitate decision making for private goods.

Dan is an entrepreneur who invests in commercial and residential real estate. He has a

savings account with $100,000 that earns 1% APY. Dan wants to buy a house that will

give him a monthly cash inflow of $200. What will opportunity cost of investing in the

house be?

A) 1000

B) 1200

C) 800

D) 200

Which of the following is a microeconomic question?

A) Should the government decrease unemployment benefits to reduce the

unemployment rate?

B) Why do some countries have higher inflation rates than other countries?

C) Should the government subsidize corn farmers to encourage the production of

ethanol?

D) Should congress decrease taxes to help stimulate the economy?

The famous economist who coined the metaphor “the invisible hand” is:

A) Mickey Kantor.

B) Ben Bernanke.

C) Milton Friedman.

D) Adam Smith.

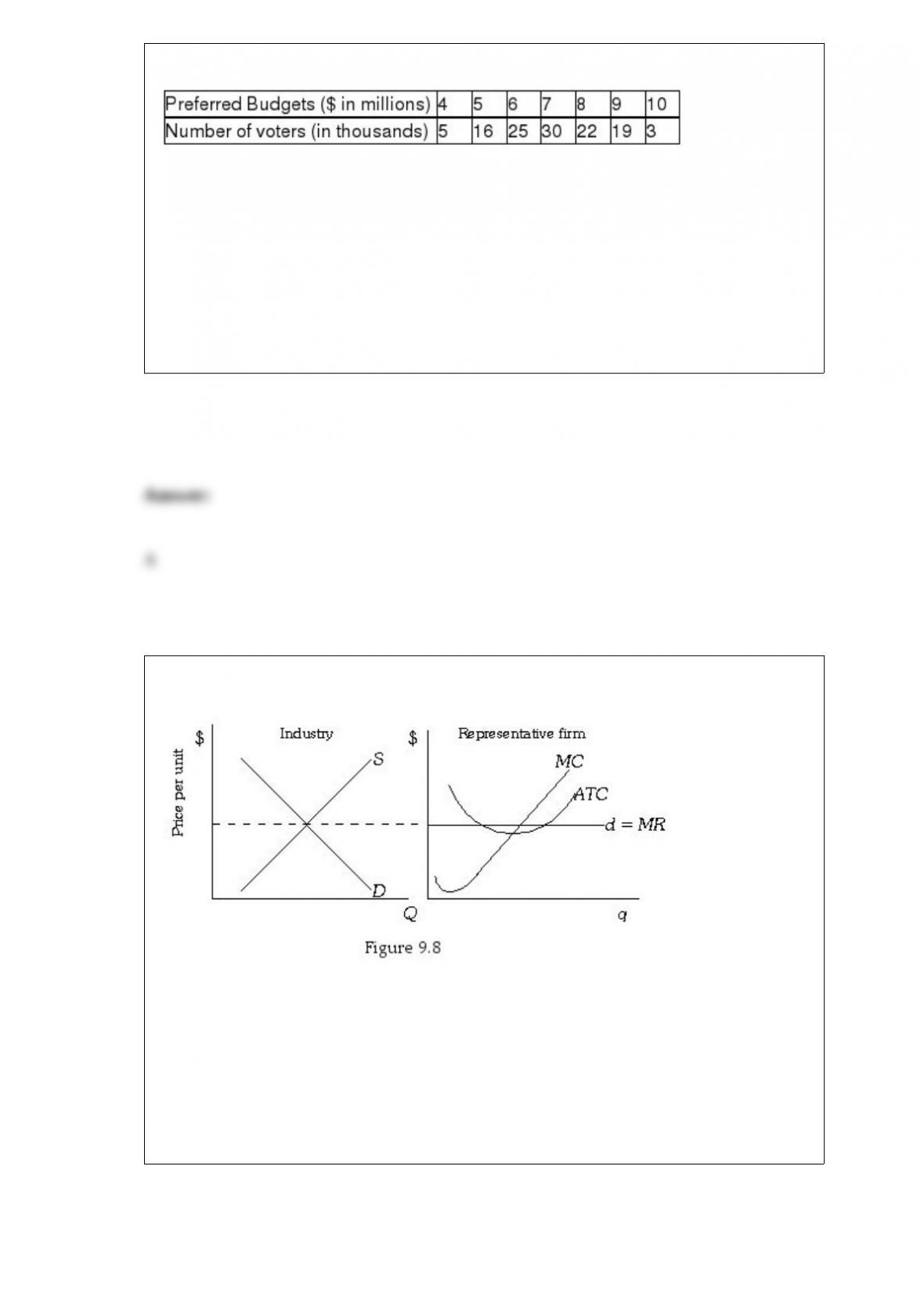

Table 15.3 shows the preferred budget for a new performance center and the number of

voters in a community who prefer that budget. Suppose that Dawn initially proposed $5

million while Terry proposed $9 million. Given the distribution of voters’ preferences,

Dawn can increase her chance of being elected by proposing:

Table 15.3

A) a greater budget toward the median budget.

B) a greater budget than $9 million.

C) a smaller budget than $5 million.

D) none of the above.

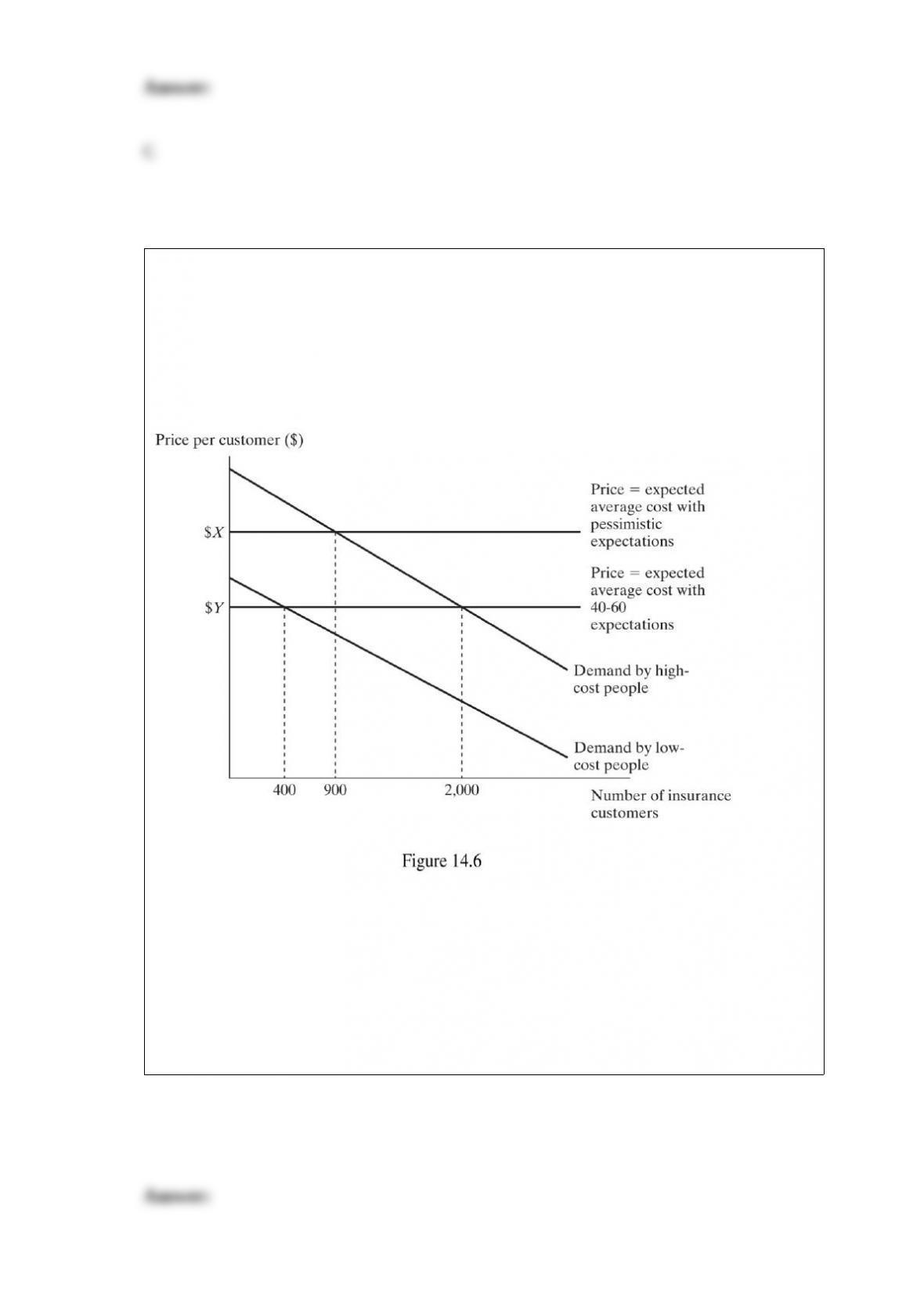

Refer to Figure 9.8. In the long run:

A) existing firms in this industry will contract output.

B) firms will leave this industry.

C) existing firms will expand and new firms will enter this industry.

D) the industry supply curve will shift to the left.

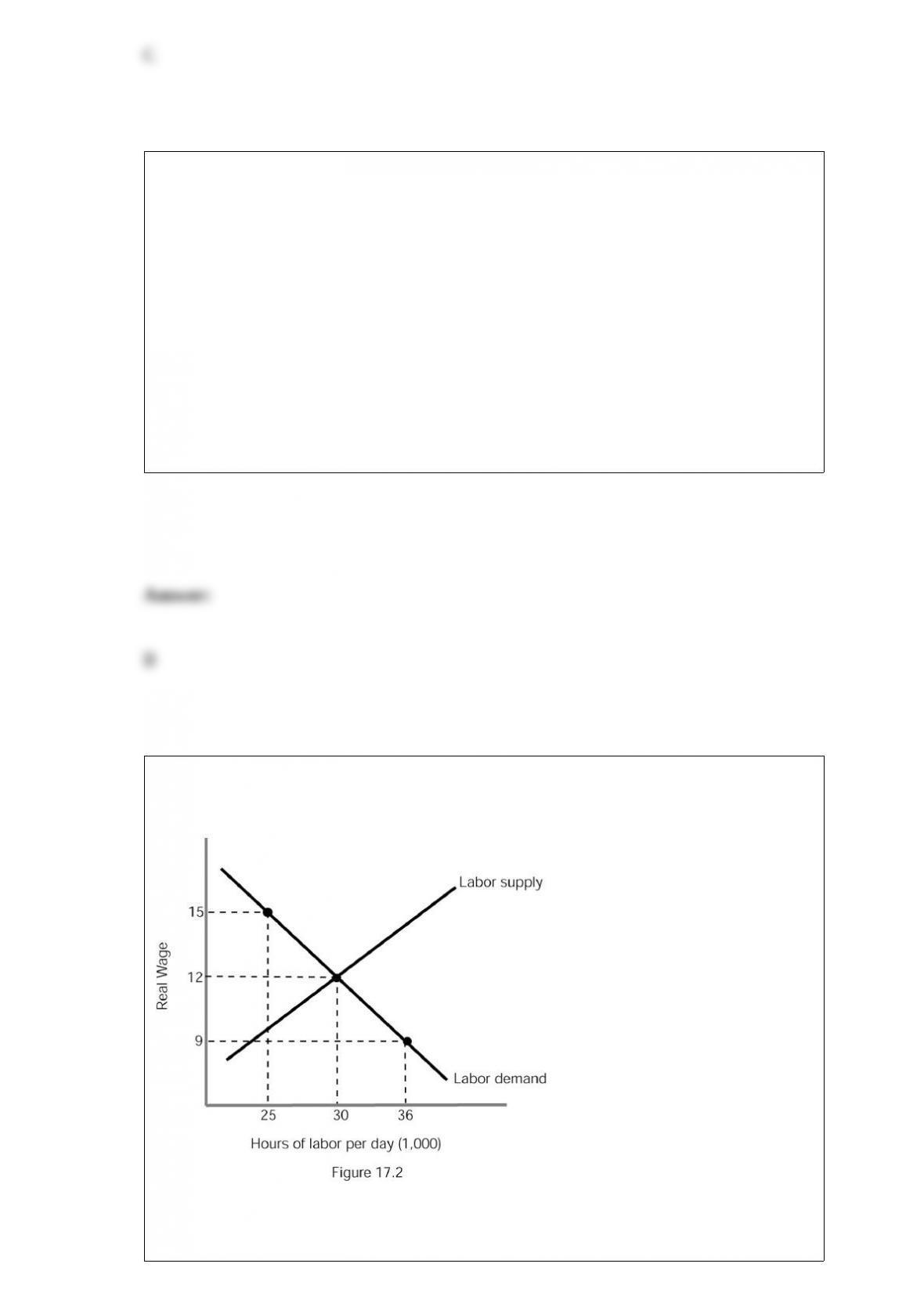

Figure 14.6 represents the market for health insurance. Suppose there are two types of

consumers, low-cost consumers with $2,000 average medical expenses per year, and

high-cost customers with $4,000 average medical expenses per year. The insurance

companies estimate that 40% of its customers are high-cost type. If the insurance

companies set the price equal to their average cost per customer, what is the insurance

companies’ average cost per customer ($Y)?

A) $4,000

B) $3,400

C) $2,800

D) $2,000

Which of the following statements is FALSE?

A) The production possibilities curve shows the combinations of goods that can be

consumed by a nation before trade begins.

B) The production possibilities curve shows the combinations of goods that can be

consumed by a nation after trade and specialization begins.

C) The production possibilities curve shows the combinations of goods that can be

produced by a nation before trading begins.

D) The production possibilities curve shows the combinations of goods that can be

produced by a nation after trade and specialization begins.

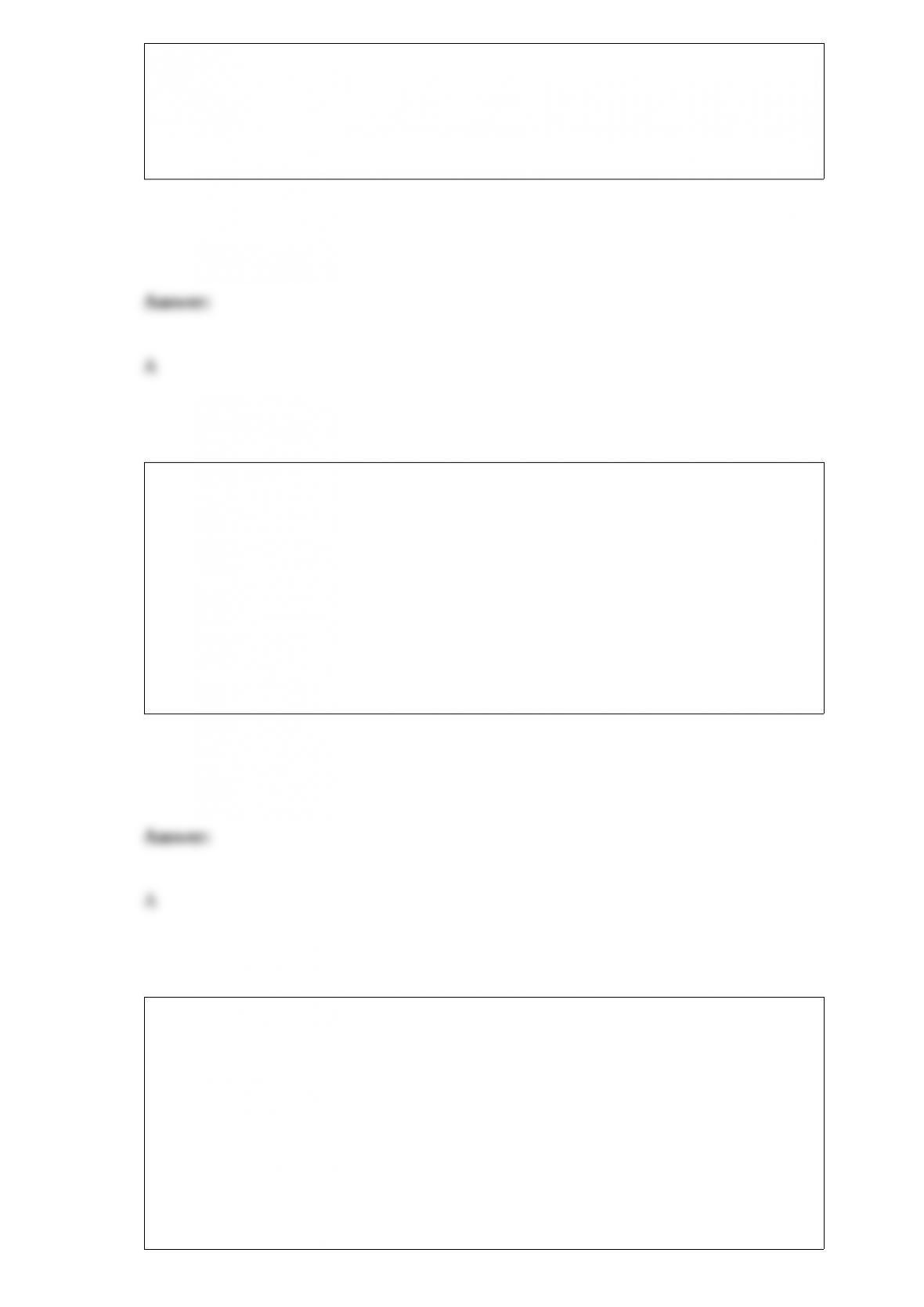

Refer to Figure 17.2. If the supply of labor decreases, then equilibrium wage will

________ and equilibrium quantity of hours will ________.

A) rise; fall

B) fall; fall

C) rise; rise

D) fall; rise

By imposing tolls on the drivers that drive during the busiest times, a government

would be attempting to:

A) internalize an externality.

B) institute a progressive tax.

C) externalize an internality.

D) encourage driving to generate revenue.

Consider two people involved in a marriage or relationship. If, when one person is

caught cheating on their agreement, the other divorces or leave them, then they are

using a:

A) tit-for-tat strategy.

B) grim trigger strategy.

C) dominant strategy.

D) predatory strategy.

During World War II, trade among camps caused the price of beef in camps with mainly

Sikh prisoners who did NOT eat beef to:

A) fall dramatically compared to the price other camps.

B) become roughly equal to the price in other camps.

C) rise above the price in other camps.

D) remain unchanged.

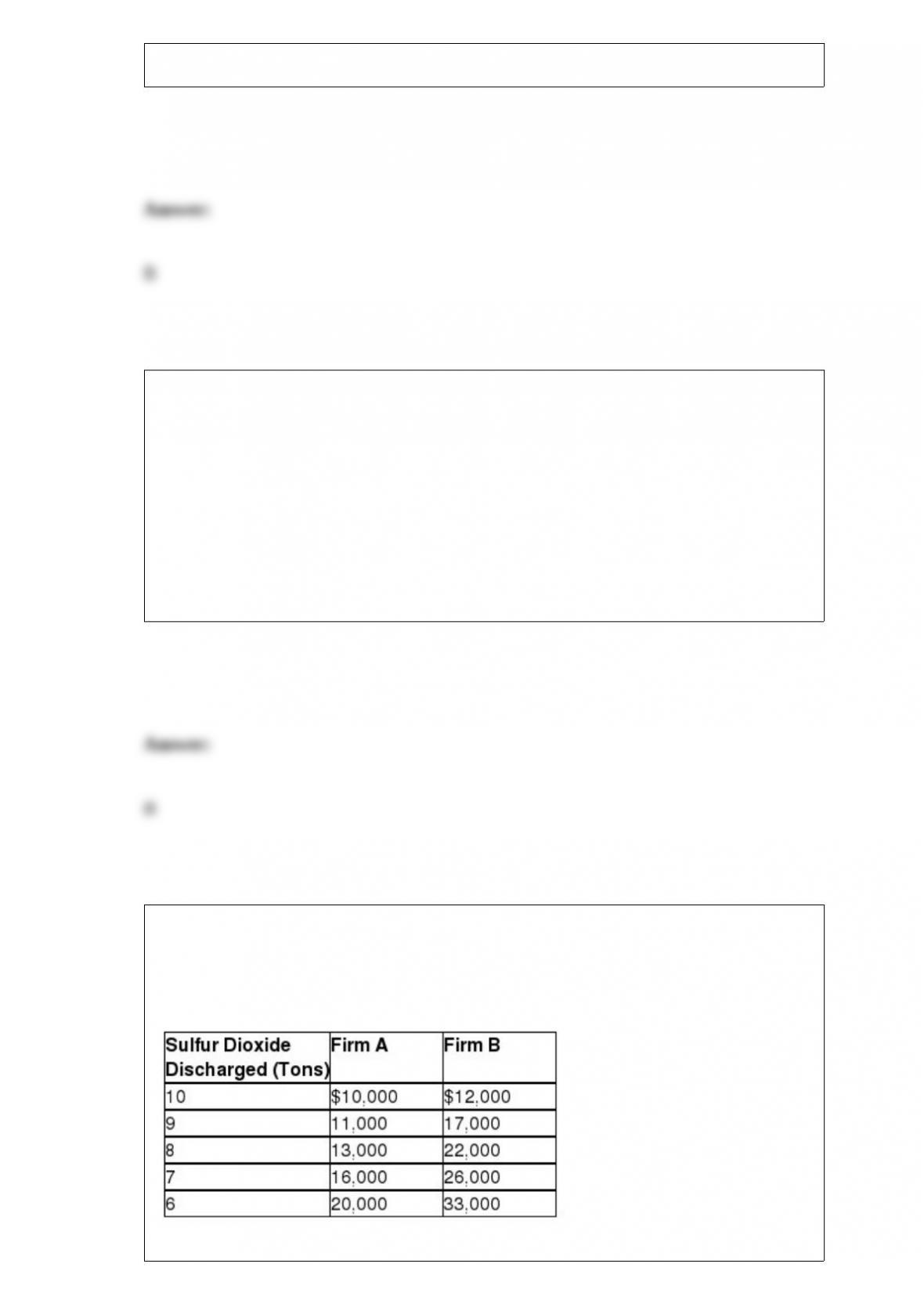

Table 16.4 shows the production cost for two utilities at different levels of sulfur

dioxide emissions. Assume that the government issued 8 marketable pollution permits

to each firm. If Firm A contemplates selling a second permit to Firm B, what is Firm A’s

willingness to accept?

Table 16.4

A) $2,000

B) $3,000

C) $4,000

D) $5,000

The reason why the government taxes the gasoline used by pollution-causing

automobiles is because it is trying to:

A) make the drivers face the full cost of their driving decisions.

B) make the government face the full cost of the driver’s driving decisions.

C) make the oil companies face the full cost of the driver’s driving decisions.

D) make the people who suffer from asthma face the full cost of the driver’s driving

decisions.

If you watch a football game on a cable TV, the cable TV is:

A) a private good but nonrival in consumption.

B) a private good and rival in consumption.

C) a public good but excludable.

D) a public good and nonexcludable.

Firms in monopolistic competition differentiate their products through:

A) physical characteristics.

B) price.

C) both A and B.

D) neither A nor B.

Bananas and apples are substitutes. When the price of bananas falls and a technological

advancement in apple production occurs at the same time:

A) the equilibrium price of apples rises and the equilibrium quantity of apples falls.

B) the equilibrium price of apples rises and the equilibrium quantity of apples rises.

C) the equilibrium price of apples rises and the equilibrium quantity of apples might

rise or fall.

D) the equilibrium price of apples falls and the equilibrium quantity of apples might

rise or fall.

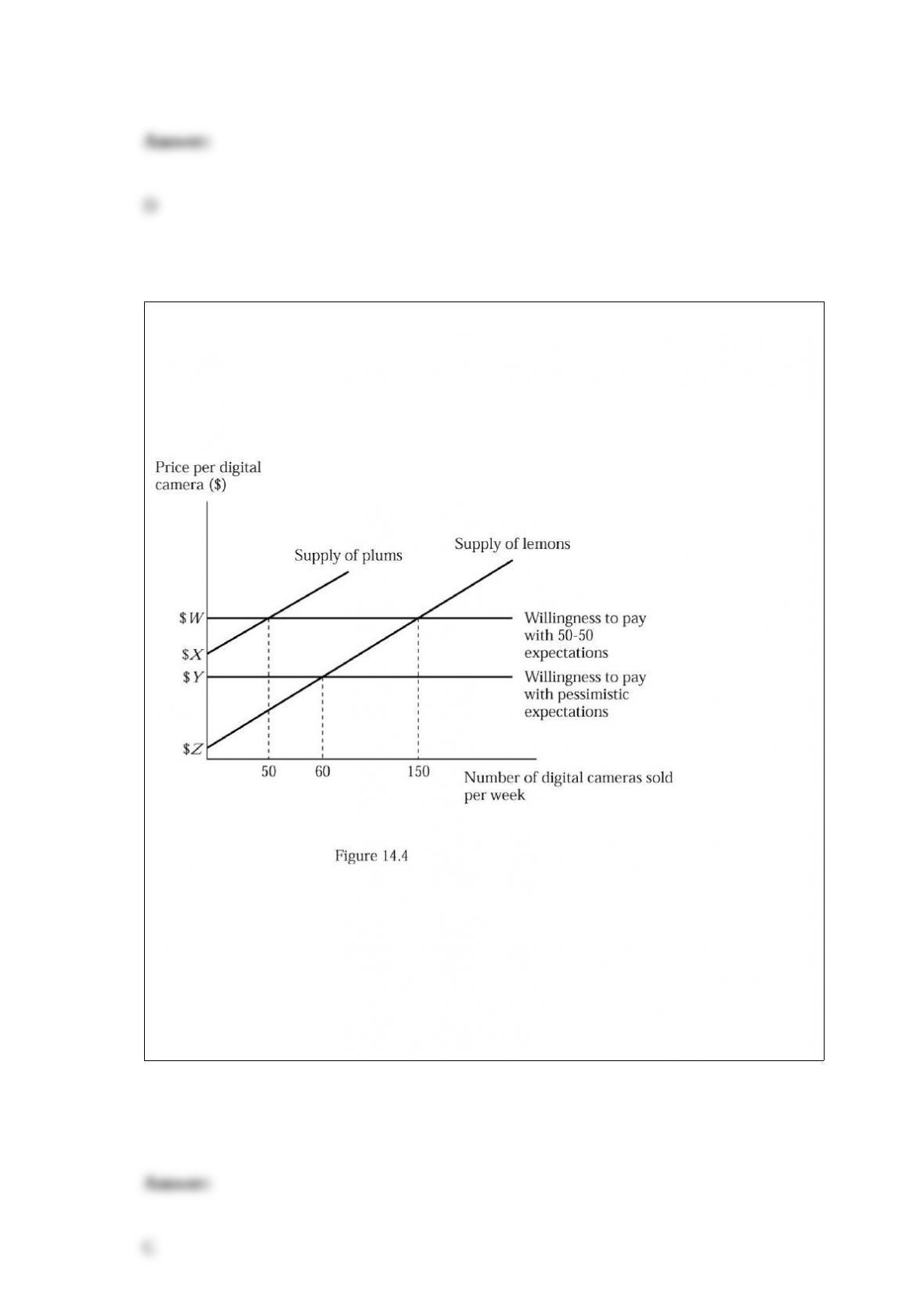

Figure 14.4 represents the market for used 12 megapixel digital cameras. Suppose

buyers are willing to pay $400 for a plum (high-quality) used digital camera and $200

for a lemon (low-quality) used digital camera. If buyers believe that 50% of used digital

cameras in the market are lemons (low quality), what is consumers’ willingness to pay

($W)?

A) $100

B) $200

C) $300

D) $400

Suppose the price of a box of pop tarts is $3. If Michael is willing to pay $4 for that box

of pop tarts, his consumer surplus is:

A) $0.

B) $1.

C) $2.

D) $3.

Based on society’s perspective, what are the benefits from pollution abatement?

A) better health

B) increased enjoyment of the natural environment

C) lower production costs

D) all of the above

You borrow money to buy a house in 2006 at a variable interest rate of 6.5%. Your

interest rate is always 2% more than the rate of inflation. By 2009, the inflation rate has

risen to 8.5%. Considering only your mortgage, is inflation good news or bad news for

you?

A) bad news, because inflation hurts everyone

B) good news, because it makes the real value of your mortgage payments decrease

C) bad news, because it makes the nominal value of your mortgage payments increase

D) neither, because your interest rate is tied to the rate of inflation

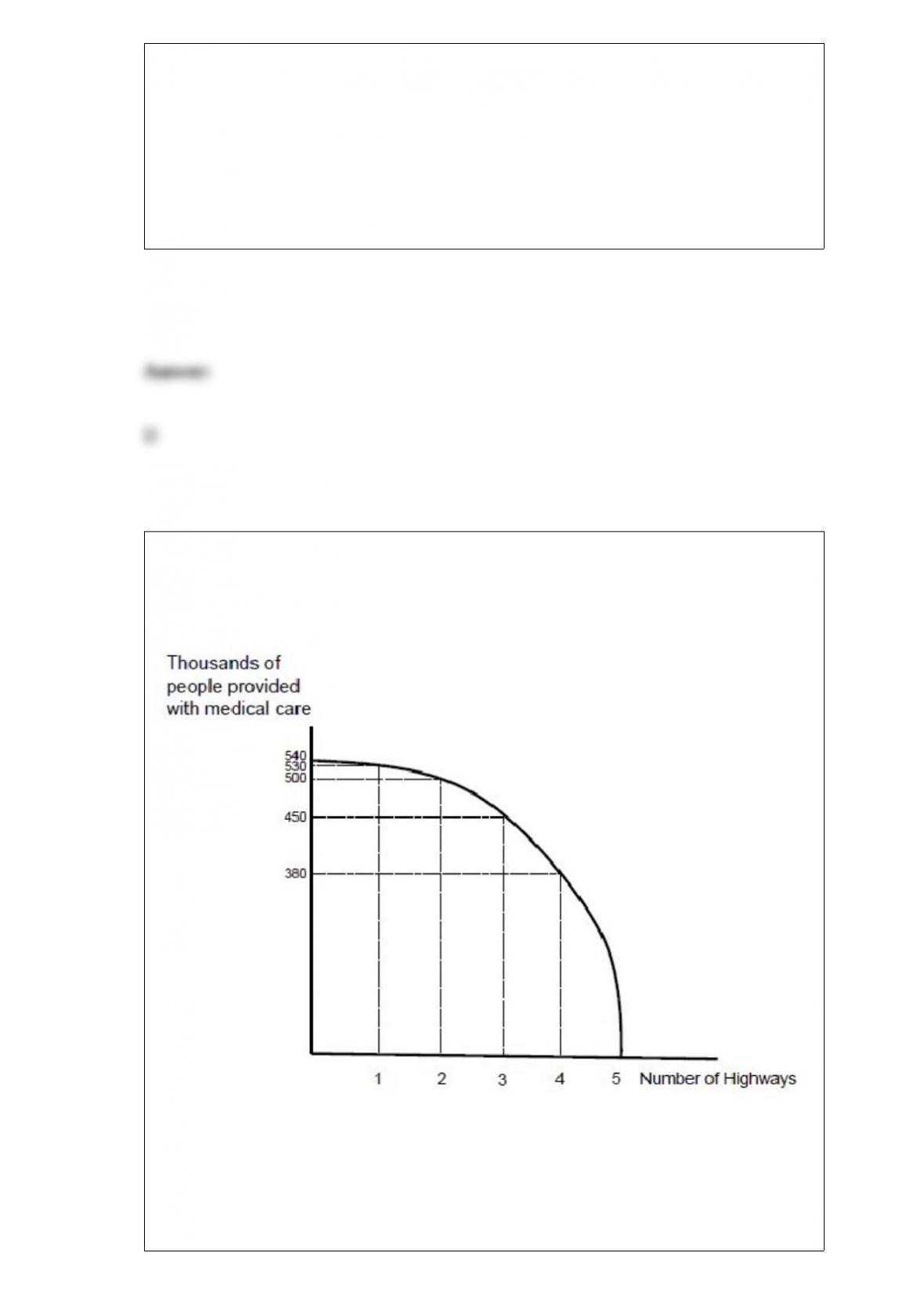

Figure 2.2 presents a production possibilities curve for a country that can either produce

highways or provide people with medical care in a given year. The opportunity cost of

the fourth new highway built in a year is:

Figure 2.2

A) less than the opportunity cost of the third new highway.

B) the same as the opportunity cost of the third new highway.

C) greater than the opportunity cost of the third new highway.

D) the sum of the opportunity costs of the first three highways built.

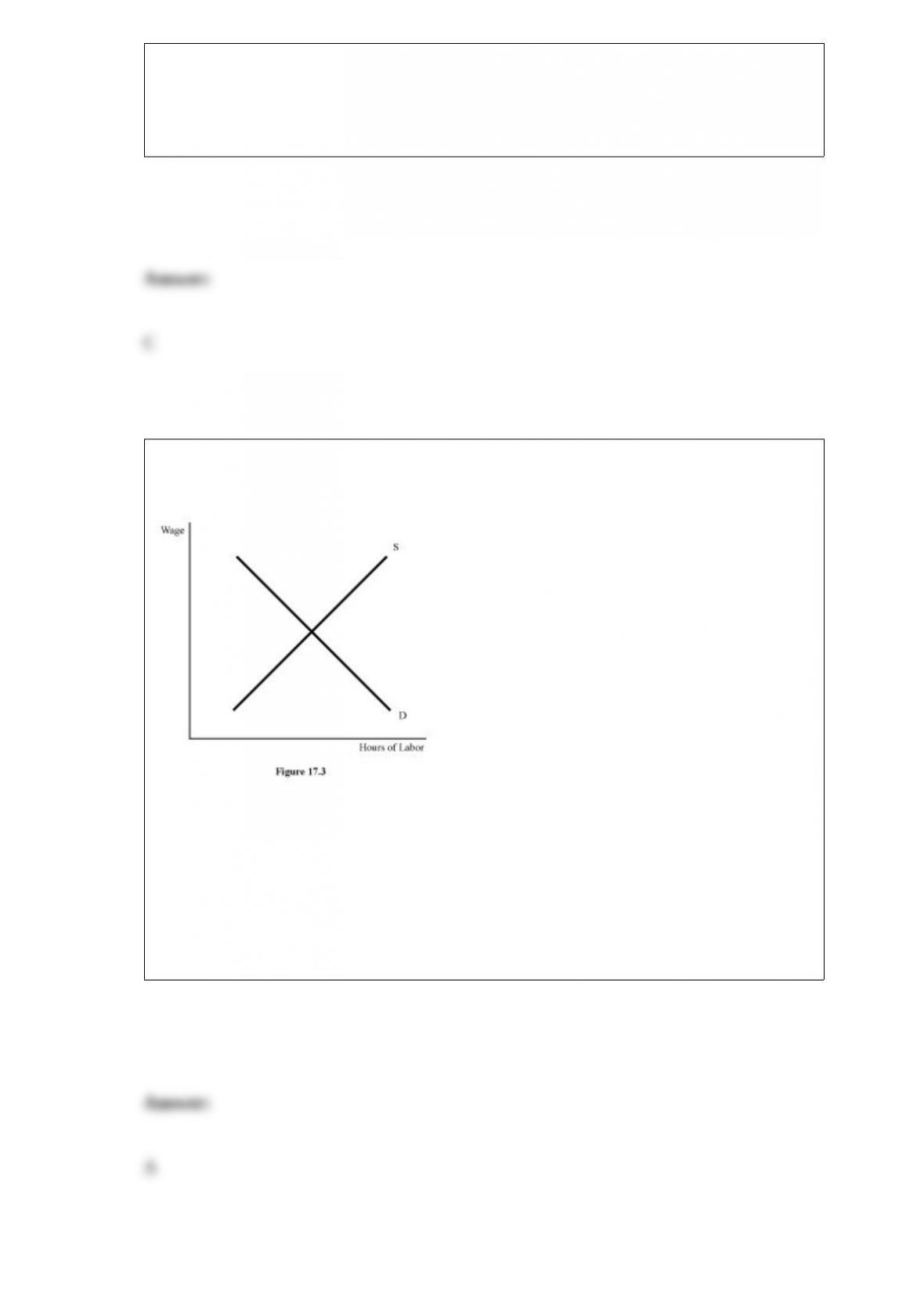

Figure 17.3 describes the labor market for a manufacturing industry. In the short run an

increase in the productivity of the workers will:

A) cause the equilibrium wage and the hours of labor used to increase.

B) not have an effect on this market.

C) cause the equilibrium wage to increase but will not change the hours of labor used.

D) cause the equilibrium wage to increase and the hours of labor used to decrease.

Recall the Application about the decline in honeybee colonies and its effect on the

price of ice cream to answer the following question(s). In the last few years

thousands of honeybee colonies have vanished, a result of bee colony collapse

disorder (CCD). Roughly one third of the U.S. food supply–including a wide

variety of fruits, vegetables, and nuts–depends on pollination from bees. The

decline of honeybees threatens $15 billion worth of crops in the United States.

According to this Application, the decline in honeybee colonies has caused ________ of

fruits and nuts used in ice cream production.

A) a decrease in the supply

B) an increase in the supply

C) an increase in the demand

D) a decrease in the demand

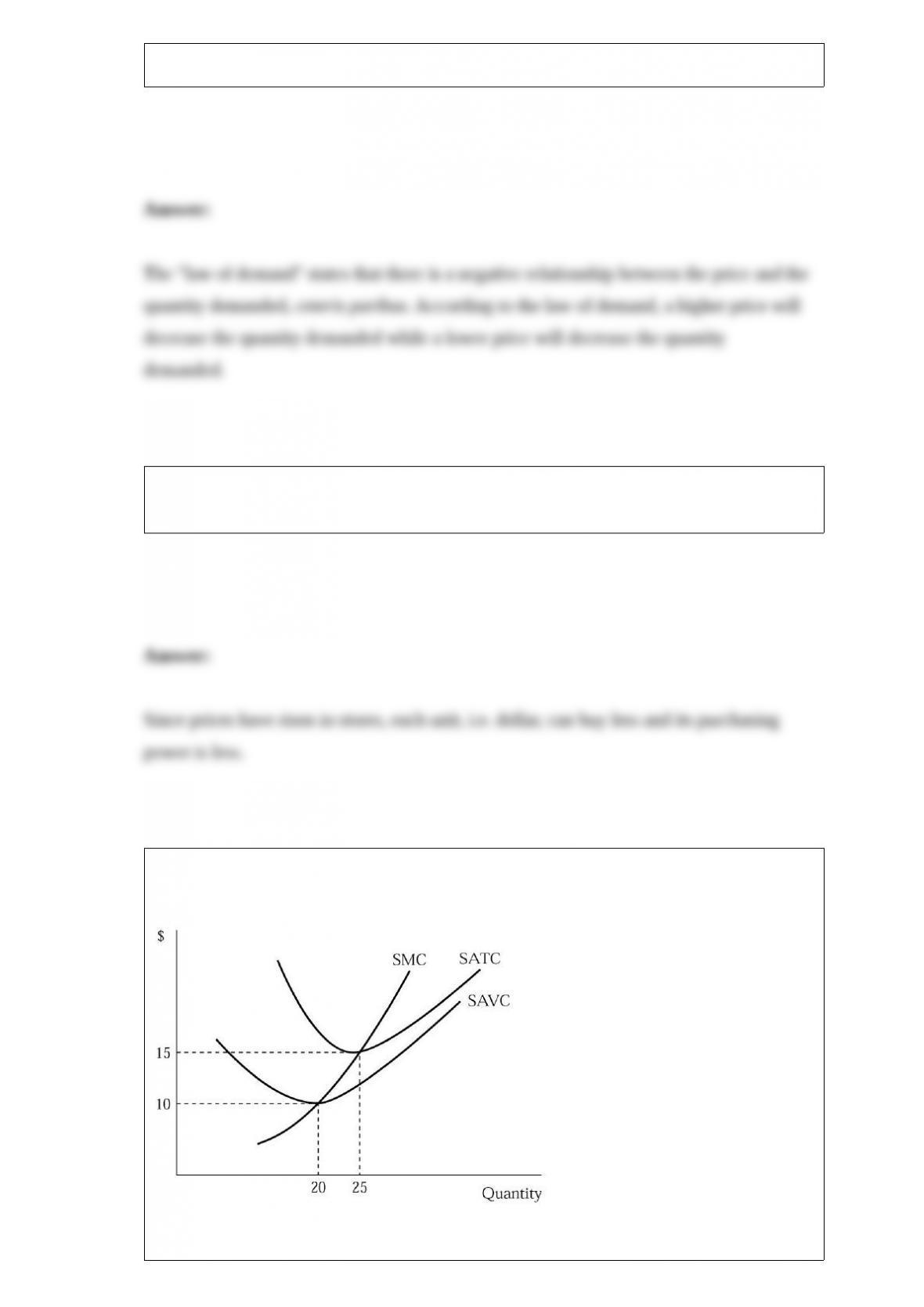

Lentz’s, Incorporated sells paper in a perfectly competitive market at a price of $2 per

ream. At the profit-maximizing (cost-minimizing) level of output, average total cost is

$2.50 per ream and average variable cost is $1.95 per ream. Should the firm continue to

operate in the short run? Explain.

What is the “law of demand”?

If your salary increases and the cost of goods in stores increase at the same rate, does a

unit of money have more or less buying power?

Figure 9.4 represents a perfectly competitive firm’s costs. Illustrate the firm’s short-run

supply curve on the graph. Explain.

Figure 9.4

Comment on the following statement: “For a nondiscriminating monopolist, marginal

revenue is always equal to price.”

Assuming that firms do not collude, compare the market outcome under oligopoly with

the outcome under monopoly.

What are the characteristics of monopolies?

Explain the characteristics of monopolistic competition. Explain how price and output

are determined in monopolistic competition.

Explain what is meant by the economic principle of voluntary exchange.

Is supply more elastic in the short run or the long run? Why?

The market maximizes total surplus under what conditions?

What is a reservation price?

Draw a graph to illustrate the effect of higher gasoline prices on the demand for large

SUVs. What is the relationship between gasoline and SUVs?

What does the income elasticity of demand measure? How is it calculated?

Explain the relationship between the price of a product, the opportunity cost of that

product, and activity in the insular cortex.

Lawyers are required to pass a comprehensive bar exam to be licensed to practice law.

What effect should this have on the number of lawyers, the wages they receive, and the

price people have to pay to receive legal services?

Explain why long-run labor demand curves slope downward using the concepts of the

input-substitution effect and the output effect.

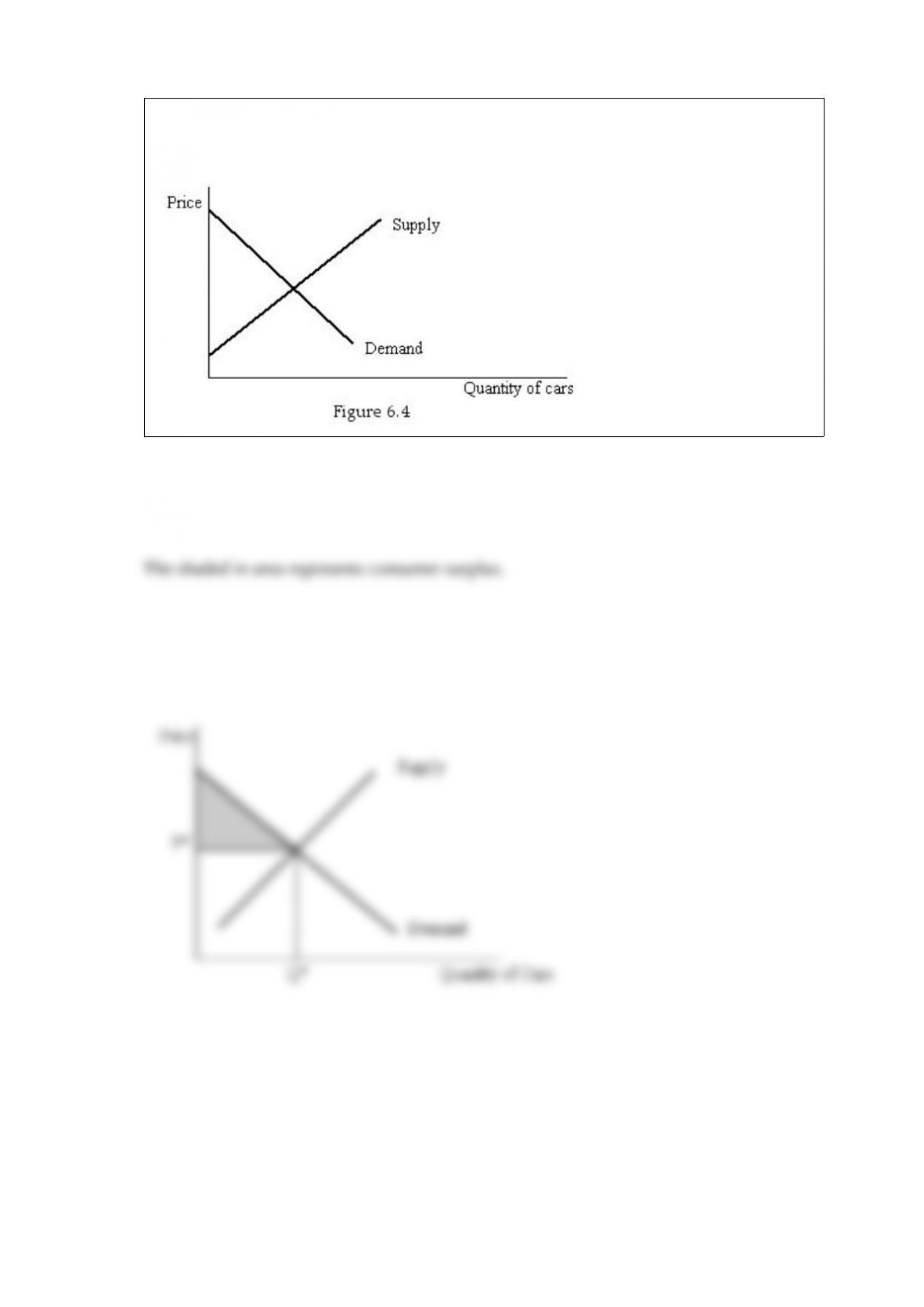

Figure 6.4 shows the market for new cars. Show the area of consumer surplus at the

market equilibrium.