A memorandum of understanding is a legal document that orders a firm to stop an

unfair practice.

Answer:

Today, most demand deposit accounts are owned by individuals.

Answer:

In 2008, the U.S. Treasury committed over $50 trillion dollars in financial support for

financial institutions.

Answer:

“Hot money” represents Goldman Groups’ greatest credit risk.

Answer:

Mutual of Omaha’s business model is to combine insurance and banking activities.

Answer:

Regarding interest expense, volume effects suggest that the mix of liabilities among

banks may differ.

Answer:

Today, many banks target individuals as the primary source of growth in attracting new

business.

Answer:

Economic value of equity analysis focuses on net interest income.

Answer:

All leveraged buyouts (LBOs) are labeled highly leveraged transactions.

Answer:

Mortgage origination makes up the largest portion of Goldman Groups’ business.

Answer:

The quality of bank loans varies with the business cycle.

Answer:

Using a 360-day year results in higher returns than using a 365-day year.

Answer:

When interest rates rise, average historical costs overstate the actual marginal costs of

issuing new debt.

Answer:

The Federal Reserve may prevent the formation of a financial holding company if one

of its insured depository institution subsidiaries is not well capitalized.

Answer:

A bank that holds only U.S. Treasury securities is not required to hold any capital since

all the assets are risk-less.

Answer:

Eurobonds are subject to fewer regulations than U.S. issued bonds.

Answer:

Non-earning assets are classified as rate-sensitive assets for GAP analysis purposes.

Answer:

Credit union membership is based upon a strict common bond that defines the

members.

Answer:

Banks labeled “consumer lenders” have the heaviest concentration of loans in credit

cards.

Answer:

An investor that matches the duration of an investment with her holding period balances

price risk and reinvestment risk.

Answer:

To help keep people in their homes, the SEC promoted loan modifications for troubled

home-loan borrowers.

Answer:

Demand for checking accounts is generally considered to be price inelastic.

Answer:

An asset that is rate-sensitive is generally not price sensitive.

Answer:

There is a constant relationship between changes in a bank’s portfolio mix and net

interest income.

Answer:

The duration of any security with interim cash flows will be less than the security’s

maturity.

Answer:

A firm generally should not count on collateral as the primary source of payment.

Answer:

Larger banks have lower efficiency ratios, on average, than smaller banks.

Answer:

Static GAP analysis focuses on the market value of stockholder’s equity.

Answer:

Smaller banks tended to have more subprime mortgage defaults than larger banks.

Answer:

Interest rate risk for banks arises largely from assets and liabilities that do not reprice at

the same time.

Answer:

Increased competition, following deregulation, has led to an increase in bank’s net

interest margin.

Answer:

Which of the following mortgage types were offered to “subprime” borrowers?

a. Interest Only

b. Option Adjustable-Rate

c. Principal Only

d. All of the above

e. a. and b. only

Answer:

___________ includes federal funds purchased, repurchase agreements and Federal

Home Loan Bank borrowings.

a. Retail funding

b. Wholesale funding

c. Borrowed funding

d. Equity funding

e. Lockbox funding

Answer:

The daily settlement process that credits gains or deducts losses from a futures

customer’s account is called:

a. the variation margin.

b. marking-to-market.

c. the initial margin.

d. the maintenance margin.

e. the gain/loss ratio.

Answer:

The primary federal regulator of state banks that are members of the Fed is the:

a. Resolution Trust Corporation

b. Federal Reserve

c. Office of the Comptroller of the Currency

d. State Banking Authorities.

e. Federal Deposit Insurance Corporation.

Answer:

Which of the following allows a security’s cash flows to change when interest rates

change?

a. Modified duration

b. Macaulay’s duration

c. Effective duration

d. Balance sheet duration

e. Income statement duration

Answer:

What is the equity multiplier for a bank where equity is equal to 12% of total assets?

a. 83.33

b. 1.12

c. 0.88

d. 12.00

e. 8.33

Answer:

A firm has the following financial statement data: Sales = $2,000, COGS = $800,

Operating Expenses = $600, and Taxes = $400. What is the firm’s profit margin?

a. 10%

b. 20%

c. 30%

d. 40%

e. 60%

Answer:

A zero cost collar:

a. is risk-free.

b. is designed to offset margin requirements.

c. has a larger premium than a reverse collar.

d. designed so the buyer has no net premium payment.

e. None of the above.

Answer:

To decrease asset sensitivity, a bank can:

a. buy longer-term securities.

b. pay premiums on subordinated debt.

c. shorten loan maturities.

d. make fewer fixed rate loans.

e. All of the above.

Answer:

Under the current capital requirements, assets in Category 2, such as repurchase

agreements, have an effective total capital-to-total-assets ratio of:

a. 1.6%.

b. 2.0%.

c. 4.0%.

d. 8.0%.

e. 8.6%.

Answer:

The vast majority of FDIC-insured institutions are classified as:

a. credit card banks.

b. agricultural banks.

c. consumer lenders.

d. commercial lenders.

e. mortgage lenders.

Answer:

At the end of 2013, there were approximately ______ independent banks and thrifts in

operation in the United States.

a. 300

b. 1,800

c. 4,200

d. 4,500

e. 6,300

Answer:

What is the equity multiplier for a bank where equity is equal to 10% of total assets?

a. 90.00

b. 10.00

c. 1.10

d. 110.00

e. 1.00

Answer:

Everything else the same, if the yield to maturity decreased 1 percentage point, which

of the following bonds would have the largest percentage increase in value?

a. A 25-year 11% coupon bond.

b. A 25-year 7.5% coupon bond.

c. A 25-year zero-coupon bond.

d. A 3-year zero coupon bond.

e. A 3-year bond with a 7.5% coupon.

Answer:

Which of the five Cs refers to an individual’s wealth?

a. cash.

b. capacity.

c. character.

d. conditions.

e. capital

Answer:

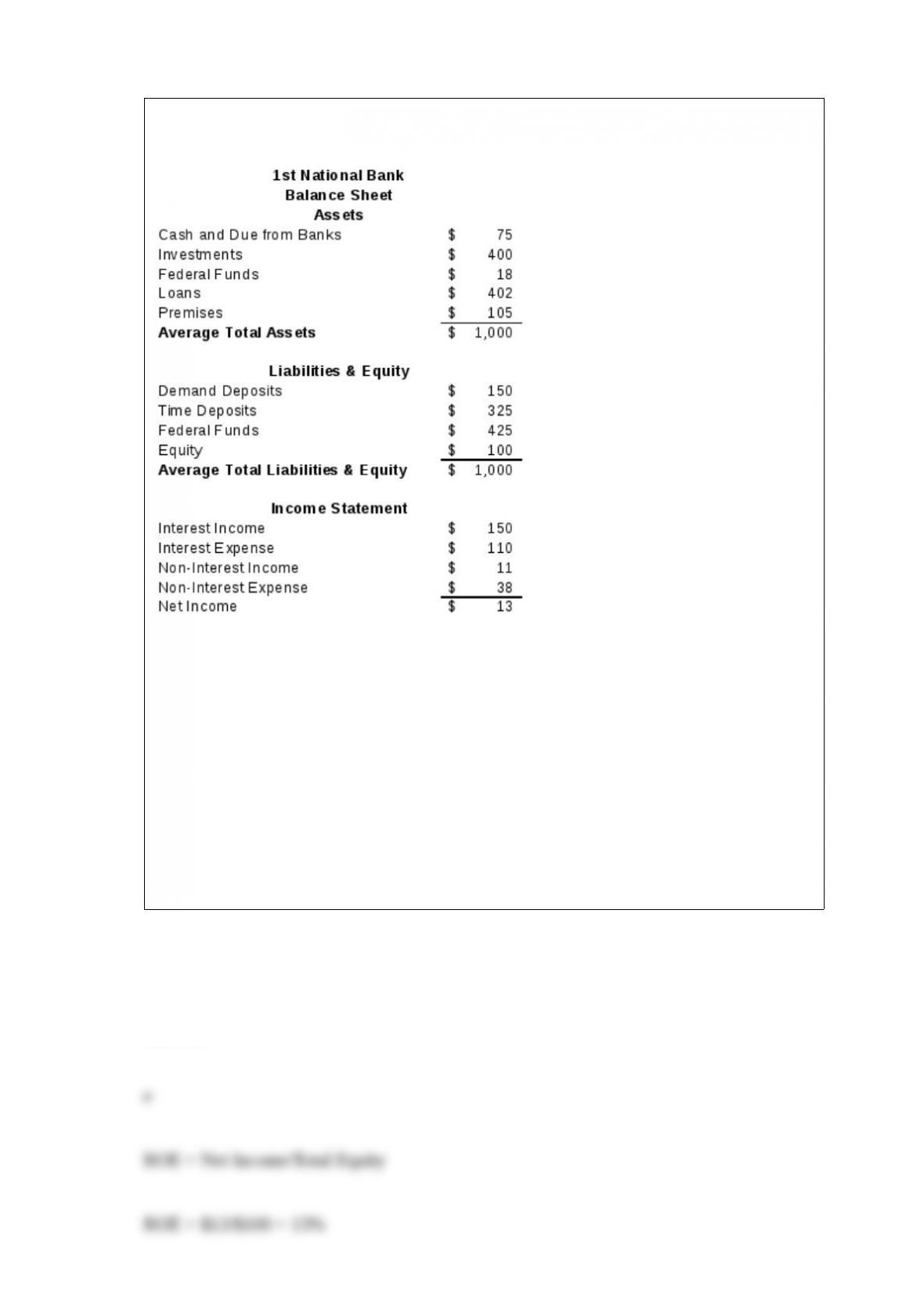

Use the following information.

What is 1st State’s return on equity?

a. 0.6%

b. 3.8%

c. 5.0%

d. 8.2%

e. 13.0%

Answer:

If $2,500 is invested today, the initial investment plus interest will be worth $5,000 in

eight years. What is the annual interest rate on the investment?

a. 1.09%

b. 5.00%.

c. 9.05%.

d. 10.00%.

e. 20.90%

Answer:

Use the following bank information.

If interest rates decrease 1% for all assets and liabilities, what is the approximate

expected change in the economic value of equity?

a. –$2.56

b. $5.84

c. –$5.84

d. $22.19

e. -$22.19

Answer:

If rate-sensitive assets equal $500 million and rate-sensitive liabilities equals $400

million, what is the expected change in net interest income if rates fall by 1%?

a. Net interest income will increase by $1 million.

b. Net interest income will fall by $1 million.

c. Net interest income will increase by $10 million.

d. Net interest income will fall by $10 million.

e. Net interest income will be unchanged.

Answer:

Which of the following is not a fundamental function of the Federal Reserve?

a. Conduct the nation’s monetary policy.

b. Provide an effective payments system.

c. Regulate banking operations.

d. Ensure bank profitability.

e. All of the above are fundamental functions of the Federal Reserve.

Answer:

The change in Net Fixed Assets equals:

a. capital expenditures minus depreciation.

b. capital expenditures plus depreciation.

c. capital expenditures minus cash flow from operations.

d. Gross fixed assets minus depreciation.

e. Gross fixed assets minus cash purchases.

Answer:

Which of the following is not one of the risks identified by the Federal Reserve Board?

a. Credit risk

b. Market risk

c. Ownership risk

d. Reputation risk

e. Legal risk

Answer:

Bank regulations:

a. can prevent bank failures.

b. can eliminate economic risk for banks.

c. serve as guidelines for sound operating policies.

d. guarantee bankers will make sound management decisions.

e. guarantee bankers act in an ethical manner.

Answer:

The purpose of the Truth in Lending Act of 1968 is to require lenders to quote:

a. home mortgage finance charges in a standardized manner.

b. rates on all certificates of deposit in a standardized manner.

c. payments with and without credit life insurance.

d. consumer loan finance charges in a standardized manner.

e. finance charges on loans over $100,000 in a standardized manner.

Answer:

Which of the following is not a channel for delivering banking services?

a. Mobile banking.

b. Online banking.

c. Automated Teller Machines.

d. Branch banking.

e. Retail banking.

Answer:

All of the following are considered transaction accounts except:

a. negotiable orders of withdrawal.

b. automatic transfer from savings.

c. demand deposit accounts.

d. money market deposit accounts.

e. all of the above are considered transaction accounts.

Answer:

Which of the following is not considered a monetary policy tool of the Federal

Reserve?

a. Changing float requirements

b. Open market operations

c. Changing the discount rate

d. Changing reserve requirements

e. All of the above are considered to be monetary policy tools

Answer:

Which of the following is correct about futures contracts?

a. Buyers of futures contracts make a profit when prices rise.

b. Buyers of futures contracts make a profit when interest rates rise.

c. Sellers of futures contracts make a profit when prices rise.

d. Sellers of futures contracts make a profit when prices interest rates fall.

e. b. and d.

Answer:

Which of the following would be the least sensitive to changes in interest rates?

a. Demand deposits

b. Repurchase agreements

c. Federal funds purchased

d. Eurodollar liabilities

e. Jumbo CDs

Answer:

The volume of net deferred credit is commonly referred to as:

a. the burden.

b. NOW balances.

c. reserve requirements.

d. equity.

e. float.

Answer:

Net interest income is the difference between:

a. gross interest income and net interest expense.

b. gross interest income and non-interest income.

c. the burden and realized gains or losses.

d. non-interest income and net interest expense.

e. gross interest income and gross interest expense.

Answer: