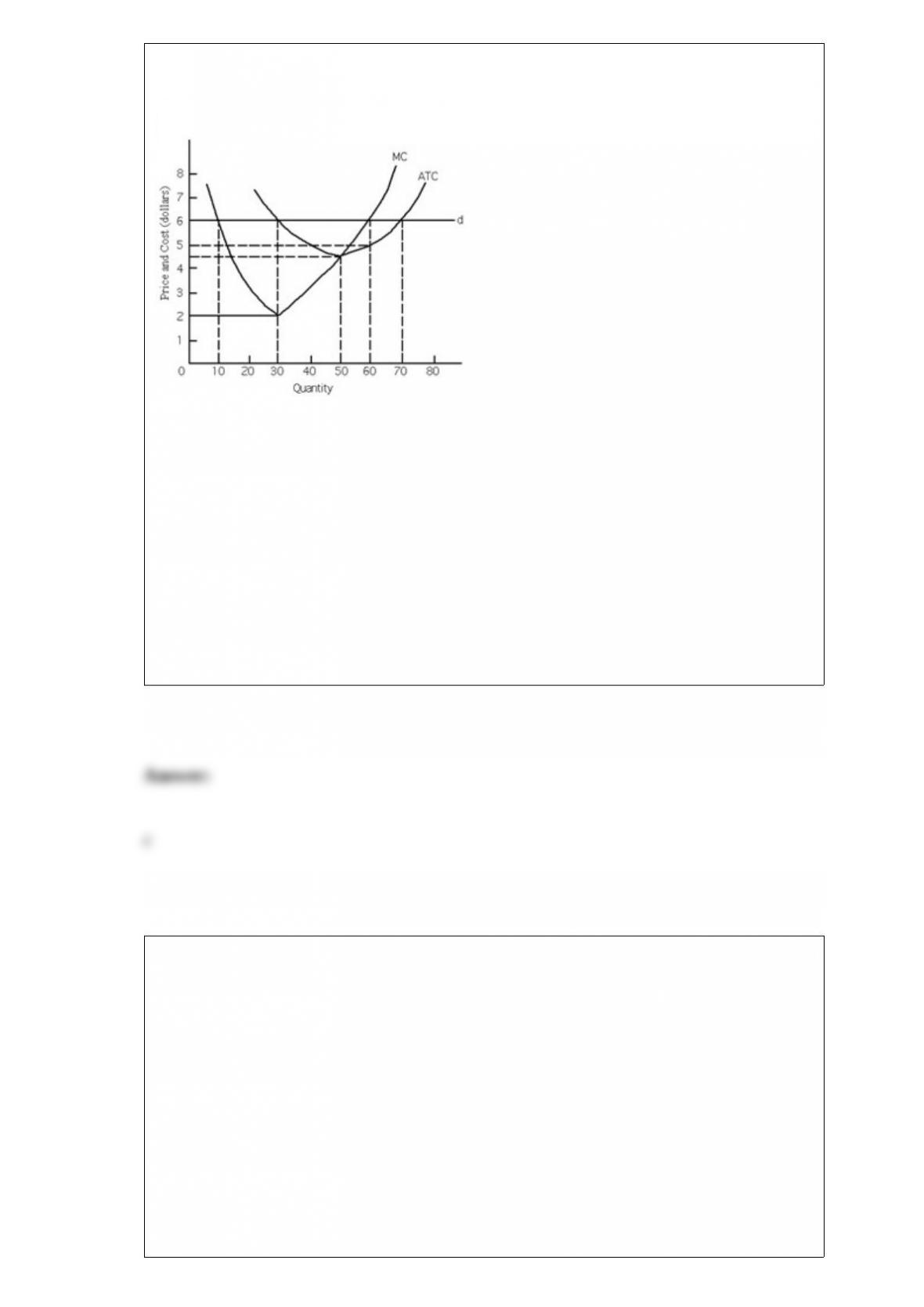

Exhibit 23-7

At the profit-maximizing output level, average total cost is

a. $2.00.

b. $4.50.

c. $5.00.

d. $6.00.

e. This cannot be determined based on the information provided.

As firms exit an industry, the industry supply curve shifts __________ and the

equilibrium price __________ until long-run competitive equilibrium is established and

the surviving firms are earning __________ economic profits.

a. leftward; rises; zero

b. leftward; falls; positive

c. leftward; rises; positive

d. rightward; falls; negative

e. rightward; rises; positive

The type of proposed merger that generally concerns the federal government the most is

a horizontal merger.

a. True

b. False

Which of the following statements is false?

a. A call option will sell for a fraction of the cost of the stock.

b. A futures contract can be written for a commodity (such as wheat), or for a currency.

c. A futures contract gives the owner the right, but not the obligation, to buy or sell a

commodity at a specified price on a given future date.

d. The specified price at which an option gives the owner the right to buy a stock at is

called the stick price.

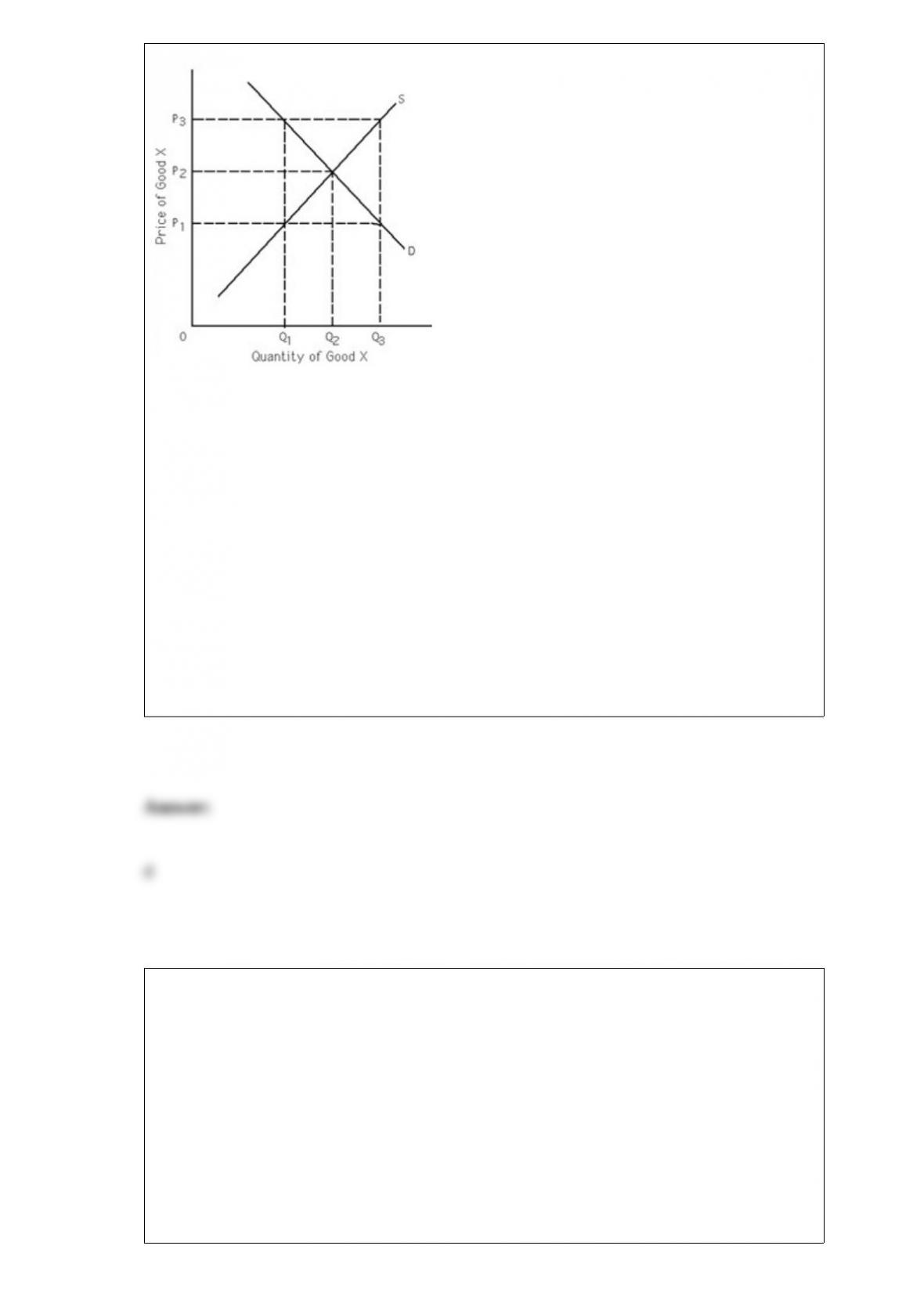

Exhibit 4-3

If P1 is a price ceiling, the highest price for good Y, which is tied (a tie-in sale) to good

X, is

a. P1.

b. P2.

c. P3.

d. P3 – P1.

e. P1 + P2.

It is argued that the market will

a. not produce a nonexcludable public good.

b. produce the socially optimal output of a nonexcludable public good.

c. produce too much of a nonexcludable public good.

d. produce a nonexcludable public good if marginal social benefits are equal to

marginal private benefits.

e. b and d

If the four-firm concentration ratio is 0.45, and the top four firms account for $10

million in sales, it follows that total industry sales equal

a. $28.57 million.

b. $12.00 million.

c. $35.00 million.

d. $15.00 million.

e. $22.22 million.

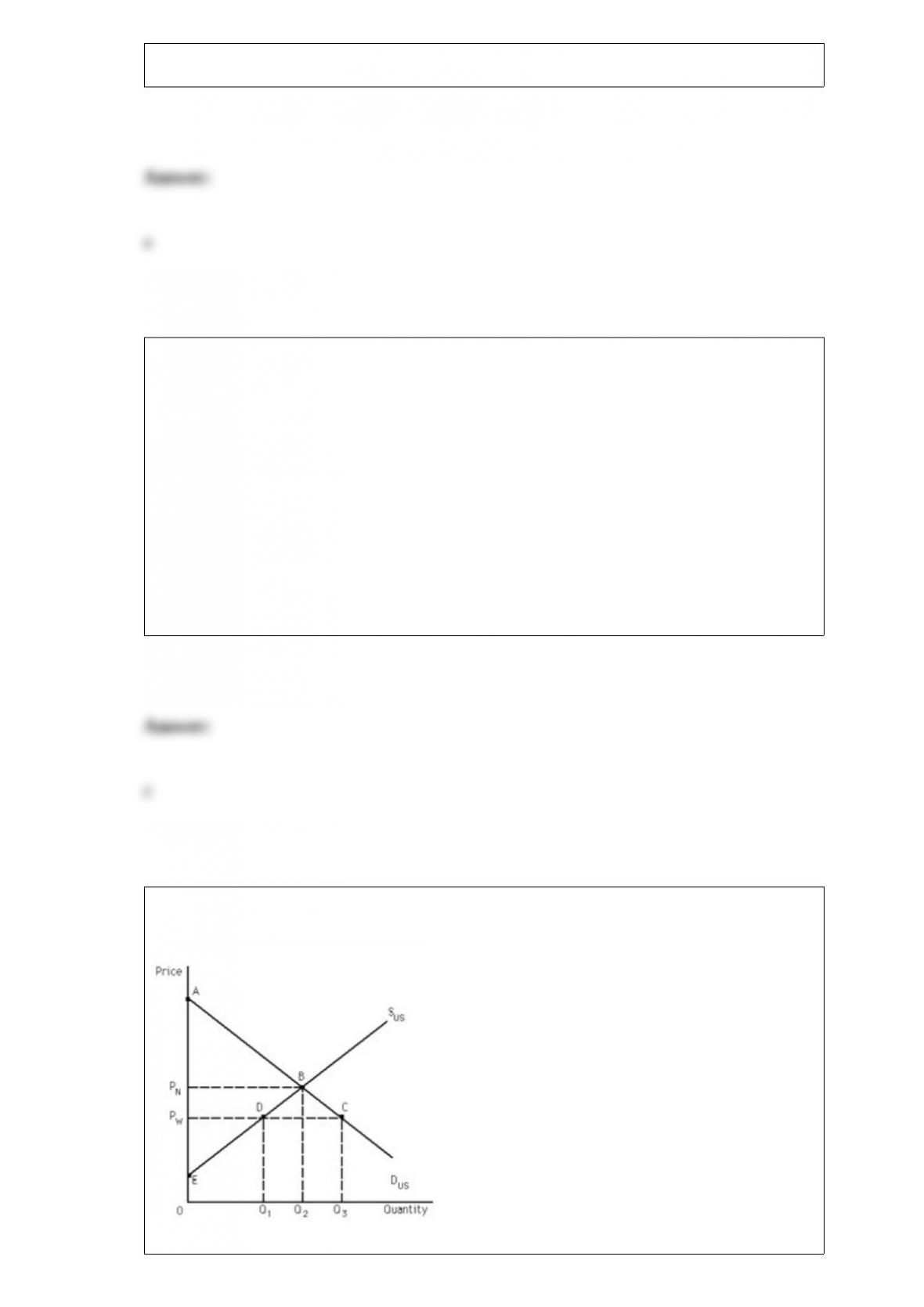

Exhibit 34-2

The U.S. demand and supply for a good are shown. Under a policy of free trade, the

world price is PW. If there is a policy change such that imports are prohibited, the price

becomes PN, U.S. consumers are worse off if imports are __________; specifically,

their consumers’ surplus changes by area __________.

a. prohibited; PWABD

b. permitted; PWDE

c. prohibited; PNBCPW

d. permitted; PN BDPW

e. none of the above

A college professor berates his political science students for being uninformed on

current political and government issues. For example, most of them do not know who

represents them in the U.S. House of Representatives. He tells his students that they

will never get very far in life by staying so uninformed and uninterested. The professor

is probably overlooking the fact that

a. people are uninformed and uninterested in only some things-not all things.

b. his students could be choosing rational ignorance.

c. by not taking out time to find out certain things, his students have more time to study

for his tests.

d. a, b, and c

e. none of the above

Which of the assumptions below assures us that economic profit will be zero in

long-run equilibrium for perfectly competitive firms?

a. buyers and sellers having all relevant information

b. firms producing heterogeneous goods

c. too few buyers

d. easy entry and exit

e. smallness of firms with respect to the market

Which of the following statements is false?

a. If the MC curve is rising, the AVC curve must be rising.

b. If MC is below ATC, ATC must be falling.

c. If MC is above AVC, then AVC must be rising.

d. If MC is above ATC, then ATC must be rising.

Suppose that when the price of cigarettes decreases by 20 percent, the quantity

demanded increases by 10percent. The price elasticity of demand for cigarettes is

__________, making cigarettes an ____________ product (in this example).

a. 0.6; elastic

b. 1.7; inelastic

c. 0.5; inelastic

d. 1.7; elastic

e. 2.0; elastic

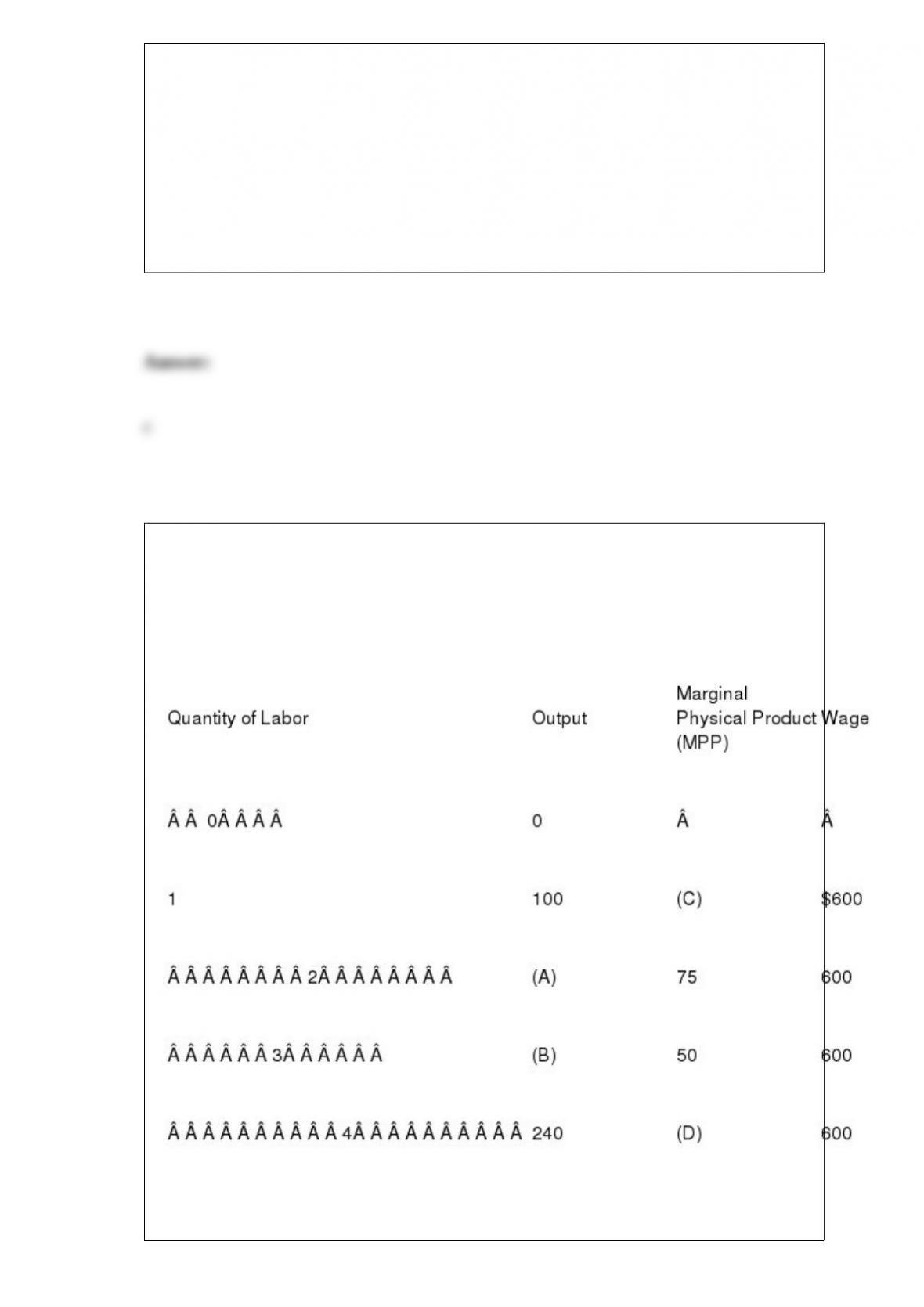

Exhibit 22-14

Assume that labor is the only variable input and that each additional laborer is paid

$600.

What is the marginal cost of producing this good with 1 and 2 laborers working [blanks

(E) and (F)], respectively?

a. $600; $300

b. $60; $30

c. $8; $12

d. $6; $8

e. none of the above

A “decrease in the quantity demanded” means that

a. the demand curve has shifted to the right.

b. the supply curve has shifted to the left.

c. price has declined and consumers therefore want to purchase more of the good.

d. price has increased and consumers therefore want to purchase less of the good.

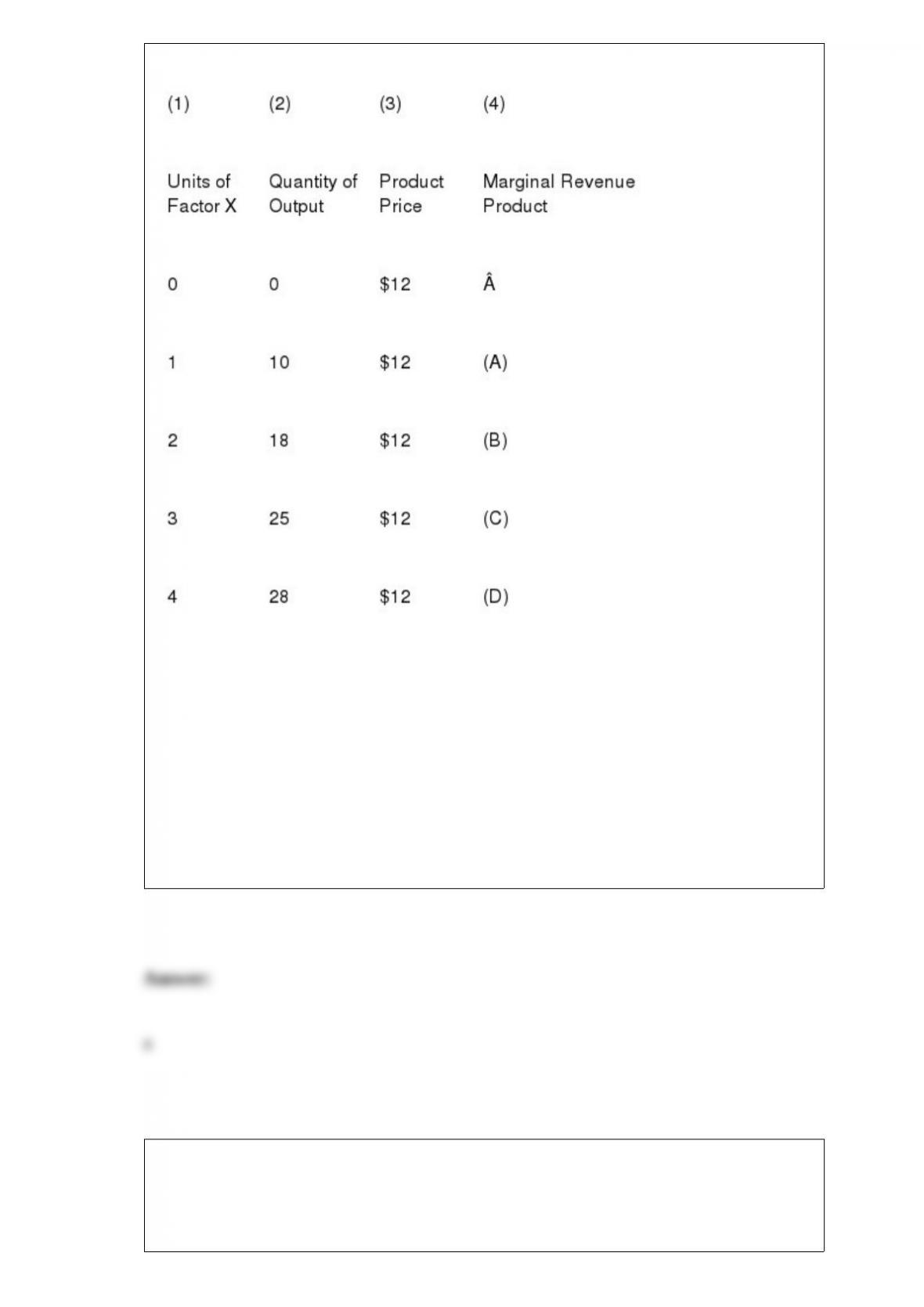

Exhibit 27-1

What dollar value goes in blank (A)?

a. $120

b. $96

c. $48

d. $35

The demand curve facing a monopolist is always

a. the same as the industry demand curve.

b. perfectly inelastic.

c. perfectly elastic.

d. unit elastic.

One of the ways in which monopolistic competitors differ from perfect competitors is

that

a. perfect competitors produce the quantity of output at which marginal revenue equals

marginal cost and monopolistic competitors do not.

b. perfect competitors produce a homogeneous product and monopolistic competitors

do not.

c. there is easy entry and exit for a perfect competitor, but not for a monopolistic

competitor.

d. a and c

e. b and c

Normative economics is concerned with

a. value judgments.

b. opinions.

c. cause-effect relationships.

d. observations that can be proved.

e. both a and b

Price ceilings and price floors

a. shift demand and supply curves and therefore have no effect upon the rationing

function of prices.

b. interfere with the rationing function of prices.

c. make the rationing function of free markets more efficient.

d. cause surpluses and shortages, respectively.