Producer surplus is

A) the difference between the maximum price consumers are willing to pay and the

minimum price producers are willing to accept.

B) the excess of the amount received from the sale of a good or service over the cost of

producing it.

C) equal to the marginal cost of production.

D) equal to the area under the supply curve.

E) the total amount paid for the good.

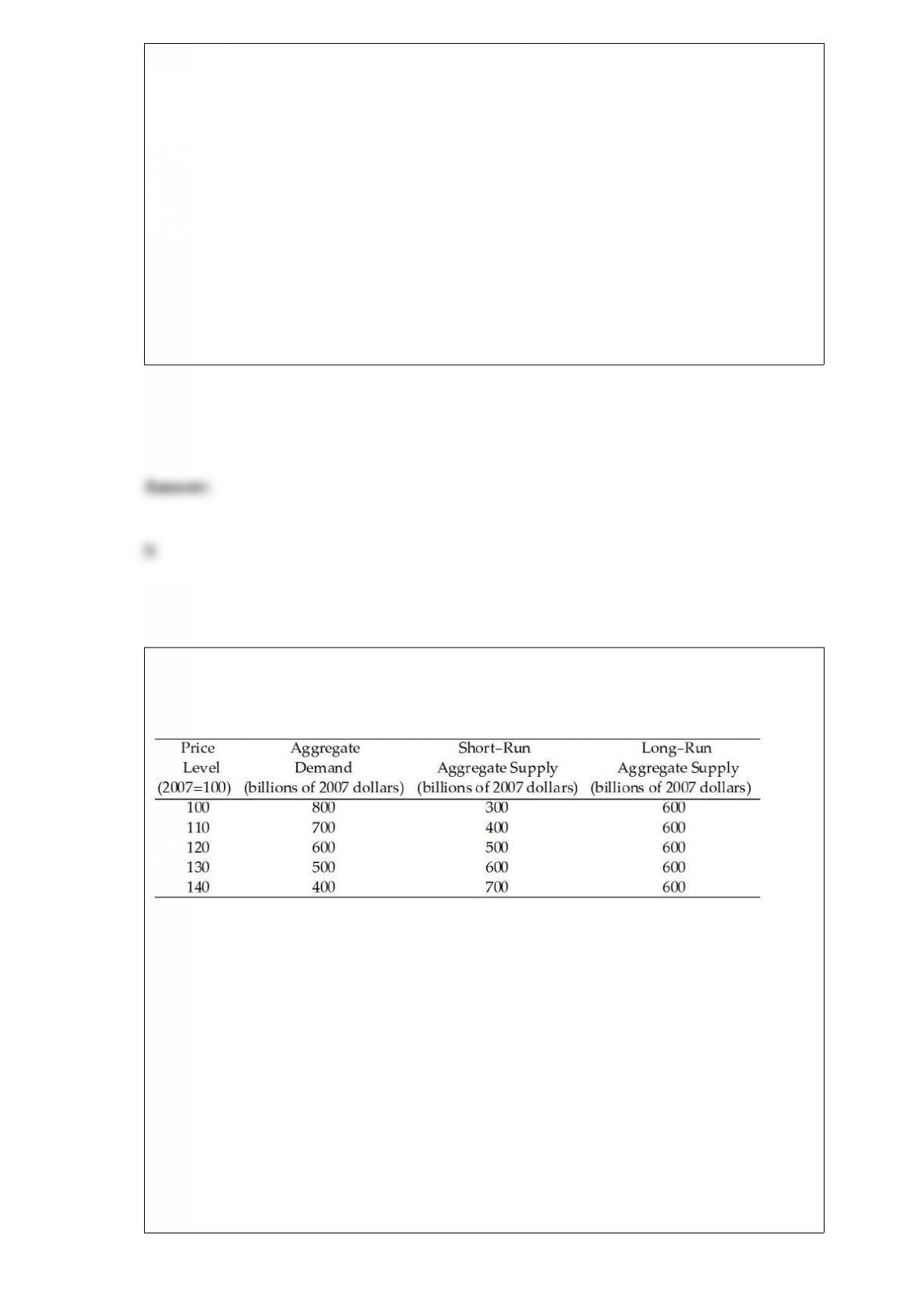

Use the table below to answer the following questions.

Table 26.3.1

Refer to Table 26.3.1. Consider the economy represented in the table. In short-run

macroeconomic equilibrium, the price level is ________ and the level of real GDP is

________ billion.

A) 120; $600

B) 120; $500

C) 125; $550

D) 130; $600

E) 130; $500

The Gini coefficient for a perfectly equal distribution of income is

A) equal to zero.

B) equal to 1.

C) equal to 100.

D) equal to infinity.

E) negative.

Producer surplus is

A) the value producers place on a good minus the price of the good.

B) the price of the good minus the value producers place on it.

C) zero if price equals marginal cost.

D) greater the more elastic the supply of the good.

E) equal to consumer surplus.

French fries and baked potatoes are

A) complements for consumers and complements in production for producers.

B) substitutes for consumers and substitutes in production for producers.

C) complements for consumers and substitutes in production for producers.

D) substitutes in production for consumers and inferior goods for producers.

E) normal goods for consumers and complements for producers.

Laura is a manager for HP. When Laura must decide whether to produce a few

additional printers, she is choosing at the margin when she compares

A) the total revenue from sales of printers to the total cost of producing all the printers.

B) the extra revenue from selling a few additional printers to the extra costs of

producing the printers.

C) the extra revenue from selling a few additional printers to the average cost of

producing the additional printers.

D) the revenue from selling HP’s printers as compared to printers from competing

companies, such as Lexmark.

E) the cost of producing HP’s printers as compared to printers from competing

companies, such as Lexmark.

Everything else remaining the same, an increase in the expected inflation rate

A) shifts the aggregate demand curve rightward.

B) shifts the aggregate demand curve leftward.

C) shifts the short-run aggregate supply curve leftward.

D) shifts the long-run aggregate supply curve rightward.

E) creates a movement up along the aggregate demand curve.

In a market that moves from a situation of no trade to a situation where a good is

imported, the price of the good ________ and the quantity produced by the domestic

industry ________.

A) rises; increases

B) falls; decreases

C) does not change; increases

D) does not change; decreases

E) rises; does not change

Which one of the following statements is false?

A) Average total cost is total cost per unit of output.

B) Average fixed cost plus average variable cost equals average total cost.

C) Marginal cost is the increase in total cost resulting from a one-unit increase in

output.

D) Total cost equals fixed cost plus average cost.

E) Marginal cost depends on the amount of labour hired.

The high price of diamonds relative to the price of water reflects the fact that, at typical

levels of consumption,

A) the total utility of water is relatively low.

B) the total utility of diamonds is relatively high.

C) the marginal utility of water is high.

D) the marginal utility of diamonds is relatively low.

E) the marginal utility of diamonds is greater than the marginal utility of water.

Opportunity cost of an action is

A) the best choice that can be made.

B) the highest-valued alternative forgone.

C) the money cost.

D) the comparative cost.

E) the absolute cost.

A price cap regulation

A) is a price floor.

B) is a price ceiling.

C) is illegal.

D) delivers marginal cost pricing.

E) sets price equal to average variable cost.