If a monopolist is producing a quantity that generates MC < MR, then profit:

A) is maximized.

B) is maximized only if MC = P.

C) can be increased by increasing production.

D) can be increased by decreasing production.

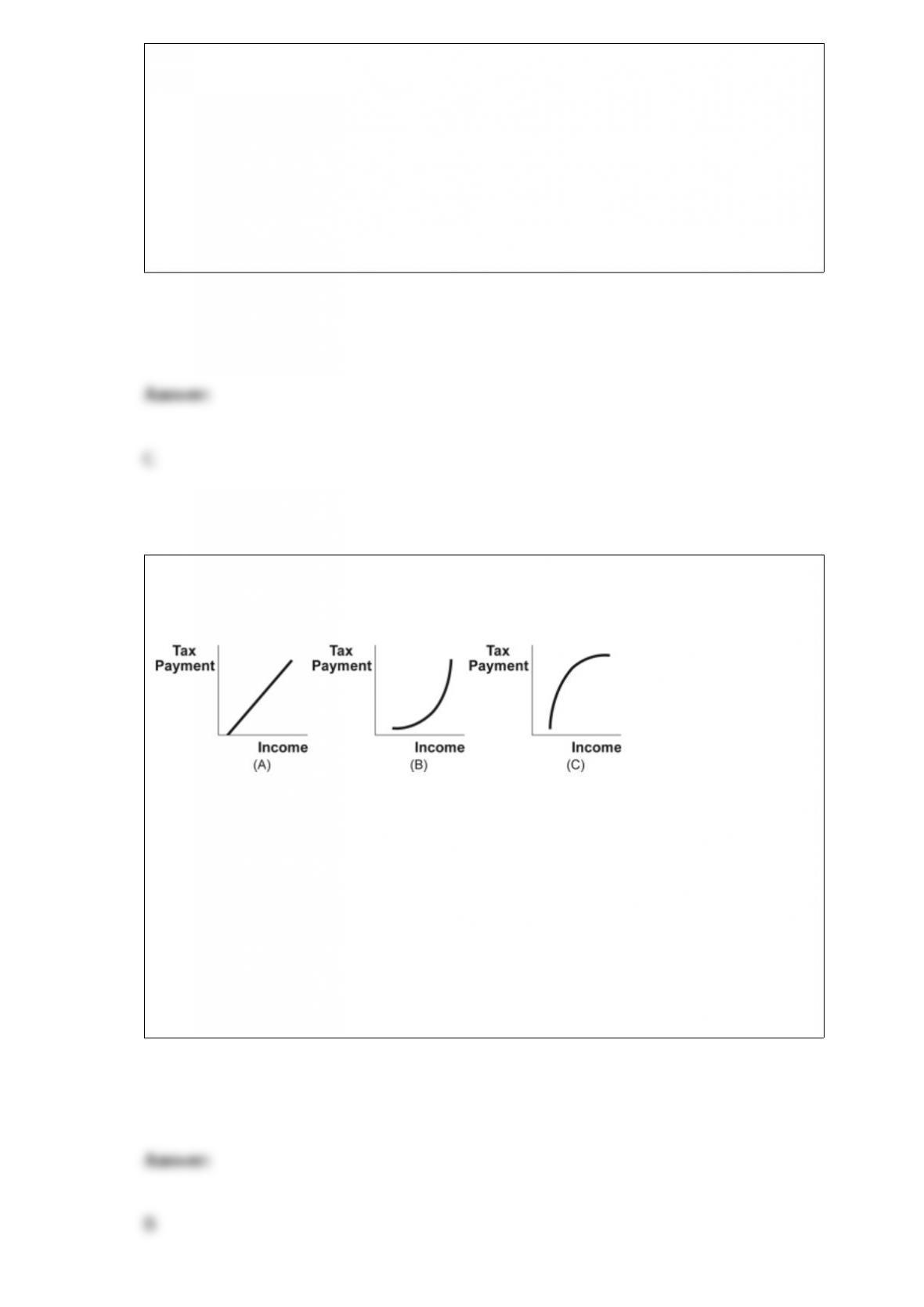

Figure: Income Tax Payments

(Figure: Income Tax Payments) Look at the figure Income Tax Payments. Which panel

or panels best represent the effects of a progressive income tax?

A) A

B) B

C) C

D) A and B

A familiar example of a negative externality is loud music on a college campus. In

principle, it should be possible to internalize this externality by permitting students to

negotiate rights to play music during particular times. The most likely reason that this

does NOT happen is that:

A) most students are unfamiliar with the Coase theorem.

B) the transaction costs associated with identifying and establishing communication

with students would be high.

C) agreements arising from such negotiations could not be enforced.

D) most students don’t view loud music as a negative externality.

In the short run, a perfectly competitive firm produces output and incurs an economic

loss if:

A) P > ATC.

B) P < AVC.

C) AVC > P > ATC.

D) AVC < P < ATC.

The _____ is the amount by which an additional unit of activity increases its total cost.

A) marginal cost

B) average cost

C) average profit

D) marginal benefit

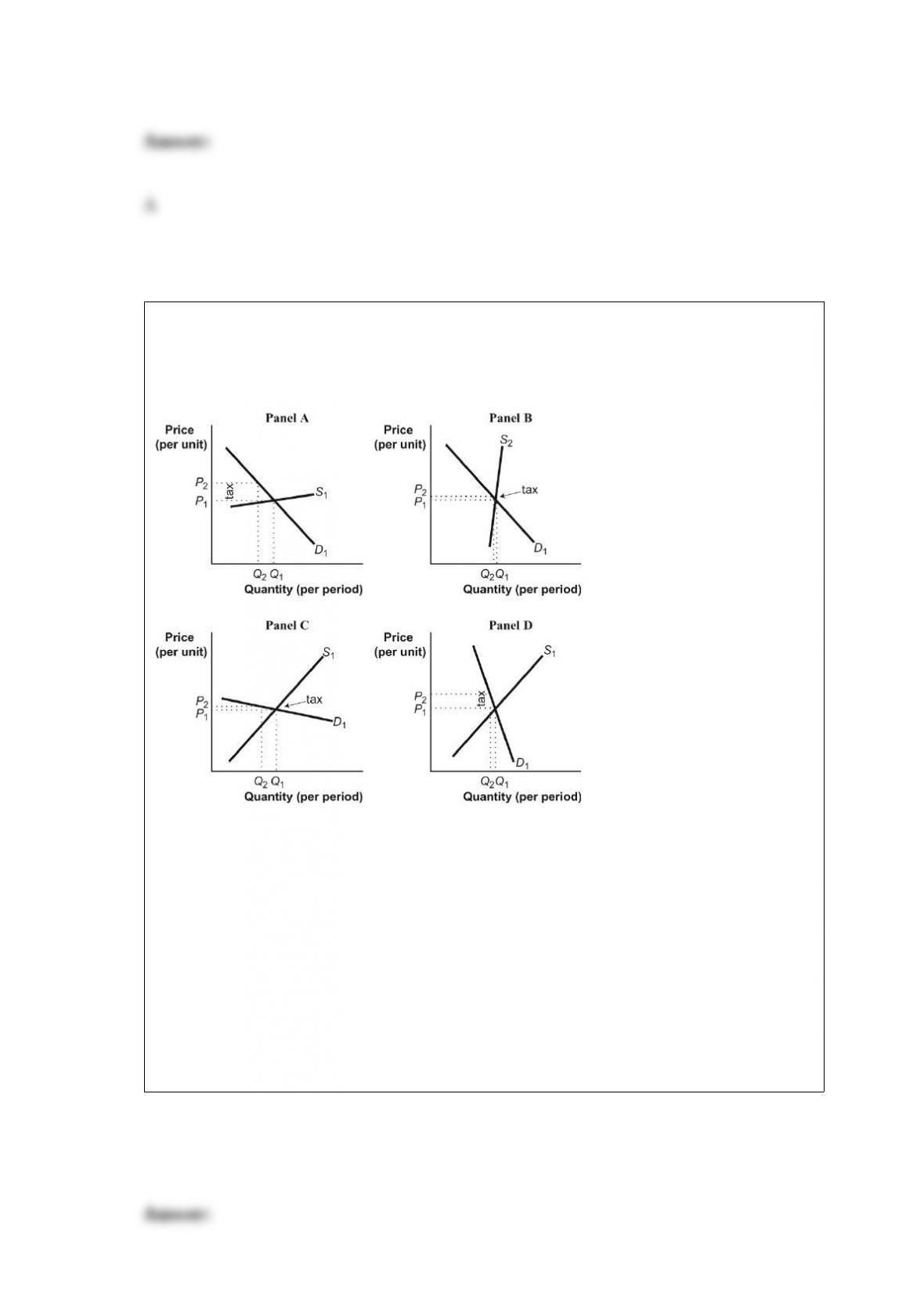

Figure: Tax Incidence

(Figure: Tax Incidence) Look at the figure Tax Incidence. All other things unchanged,

when a good or service is characterized by a relatively inelastic demand, as shown in

panel _____, the greater share of the burden of an excise tax on it is borne by _____.

A) C; buyers

B) C; sellers

C) D; sellers

D) D; buyers

Good X and good Y are related goods. Holding everything else constant, if the price of

X decreases and the demand for Y increases, X and Y are probably:

A) complements.

B) substitutes.

C) inferior.

D) normal.

Along a given upward-sloping supply curve, a decrease in the price of a good will

_____ producer surplus.

A) increase

B) decrease

C) have no effect on

D) It’s impossible to tell what will happen to producer surplus.

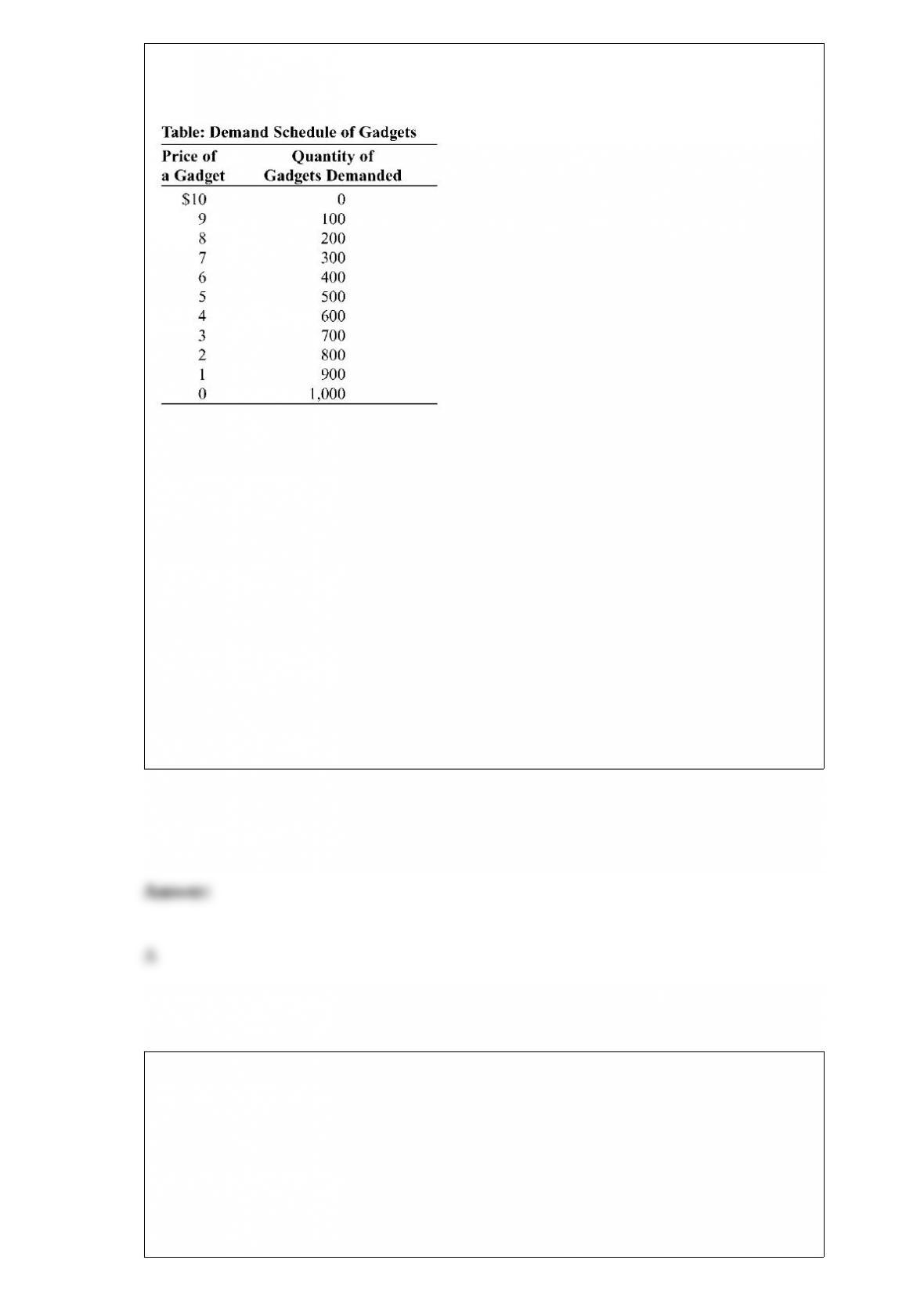

(Table: Demand Schedule for Gadgets) Look at the table Demand Schedule for

Gadgets. The market for gadgets consists of two producers, Margaret and Ray. Each

firm can produce gadgets with no marginal cost or fixed cost. Suppose that these two

producers have formed a cartel, agreed to split production of output evenly and are

maximizing total industry profits. If Margaret decides to cheat on the agreement and

sell 100 more gadgets, the market price of gadgets will be:

A) $4.

B) $5.

C) $6.

D) $7.

Maximum total surplus in the market for chocolate occurs when:

A) total net gain to producers is minimized.

B) all consumers who value chocolate can buy chocolate.

C) all producers can sell their chocolate.

D) the market is in equilibrium.

The government imposes a tax of $1,000 per household to fund a new public swimming

pool. This tax is:

A) regressive.

B) proportional.

C) progressive.

D) flat.

General Snacks is a typical firm in monopolistic competition. If the market is in

long-run equilibrium, then the price General Snacks charges for its snack goods:

A) equals average total cost.

B) exceeds average total cost.

C) is less than average total cost.

D) is more than the average for all other firms in the market.

According to the benefits principle, which of the following is the BEST example of

taxation?

A) personal income tax

B) sales tax

C) corporate income tax

D) gasoline tax

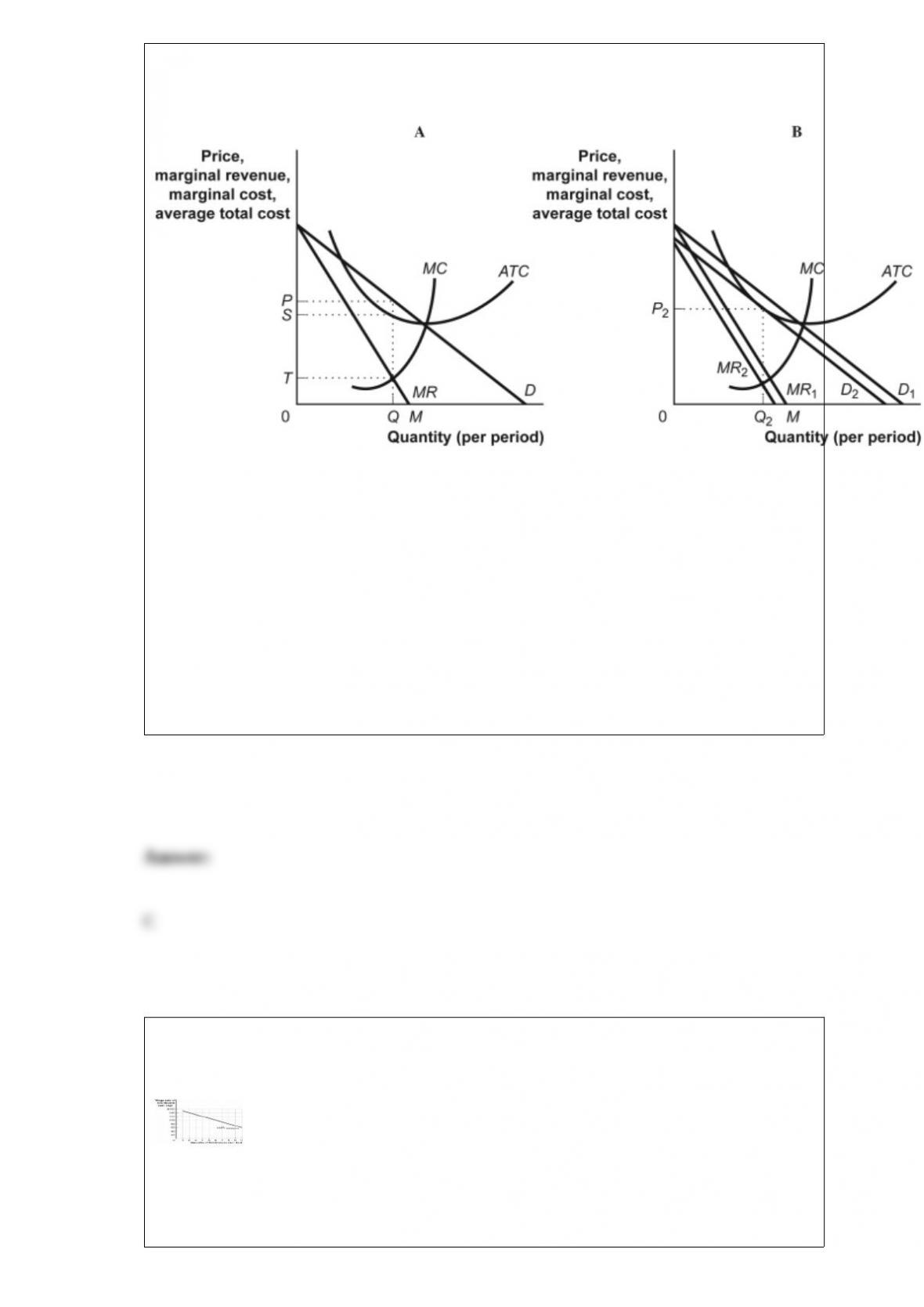

Figure: Profit Maximization in Monopolistic Competition

(Figure: Profit Maximization in Monopolistic Competition) In the short run, a firm in

monopolistic competition may earn economic profits. The profits in the figure Profit

Maximization in Monopolistic Competition, panel (A), are:

A) PS.

B) PS × M.

C) PS × Q.

D) PT × Q.

Figure: The Demand for Bricklayers

(Figure: The Demand for Bricklayers) Look at the figure The Demand for Bricklayers.

If the price for bricks laid in the wall is $0.10 a brick, the total production of bricks by

the first three bricklayers is _____ bricks.

A) 1,500

B) 2,900

C) 4,200

D) 5,400

Monopolistic competitors:

A) have some ability to set price.

B) must accept the price as given and therefore are price takers.

C) produce goods that are standardized and hard to differentiate.

D) eventually produce at their minimum ATC at the profit-maximizing level.

Figure: Game-Day Shirts

(Figure: Game-Day Shirts) Rick is one of 10 vendors who sell game-day T-shirts at

football games in a perfectly competitive market. His costs are identical to the costs of

the other 9 vendors. If the price of a shirt is $6, the short-run industry supply will be

_____ shirts.

A) 0

B) 140

C) 220

D) 240

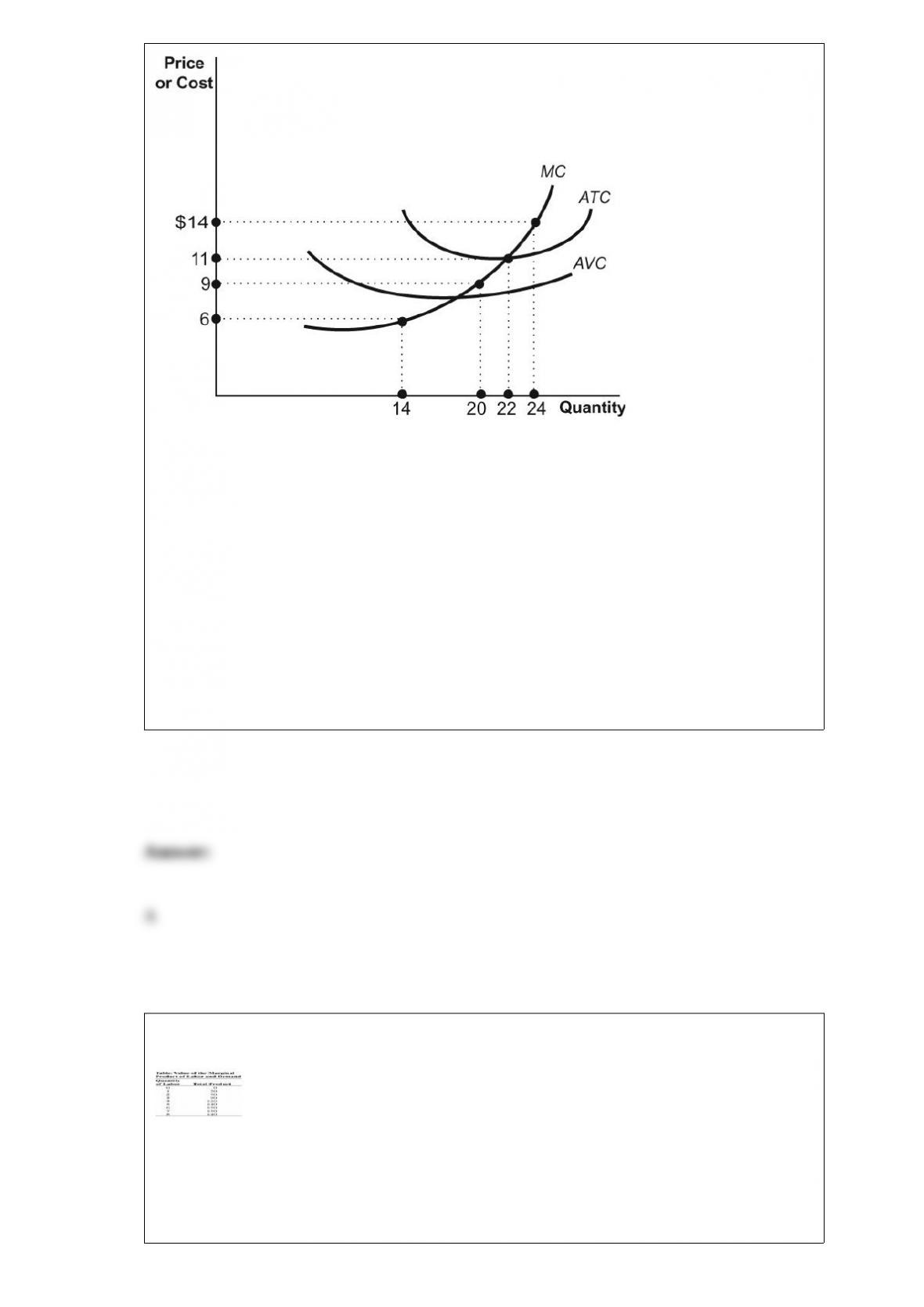

(Table: Value of the Marginal Product of Labor and Demand) In the figure Value of the

Marginal Product of Labor and Demand, the total product of labor is shown for the

hourly production of power cords. Assume that the market for power cords is perfectly

competitive. If the price of a power cord is $2 and the wage rate is $90 per hour, the

profit-maximizing quantity of labor is _____ workers.

A) zero

B) two

C) four

D) six

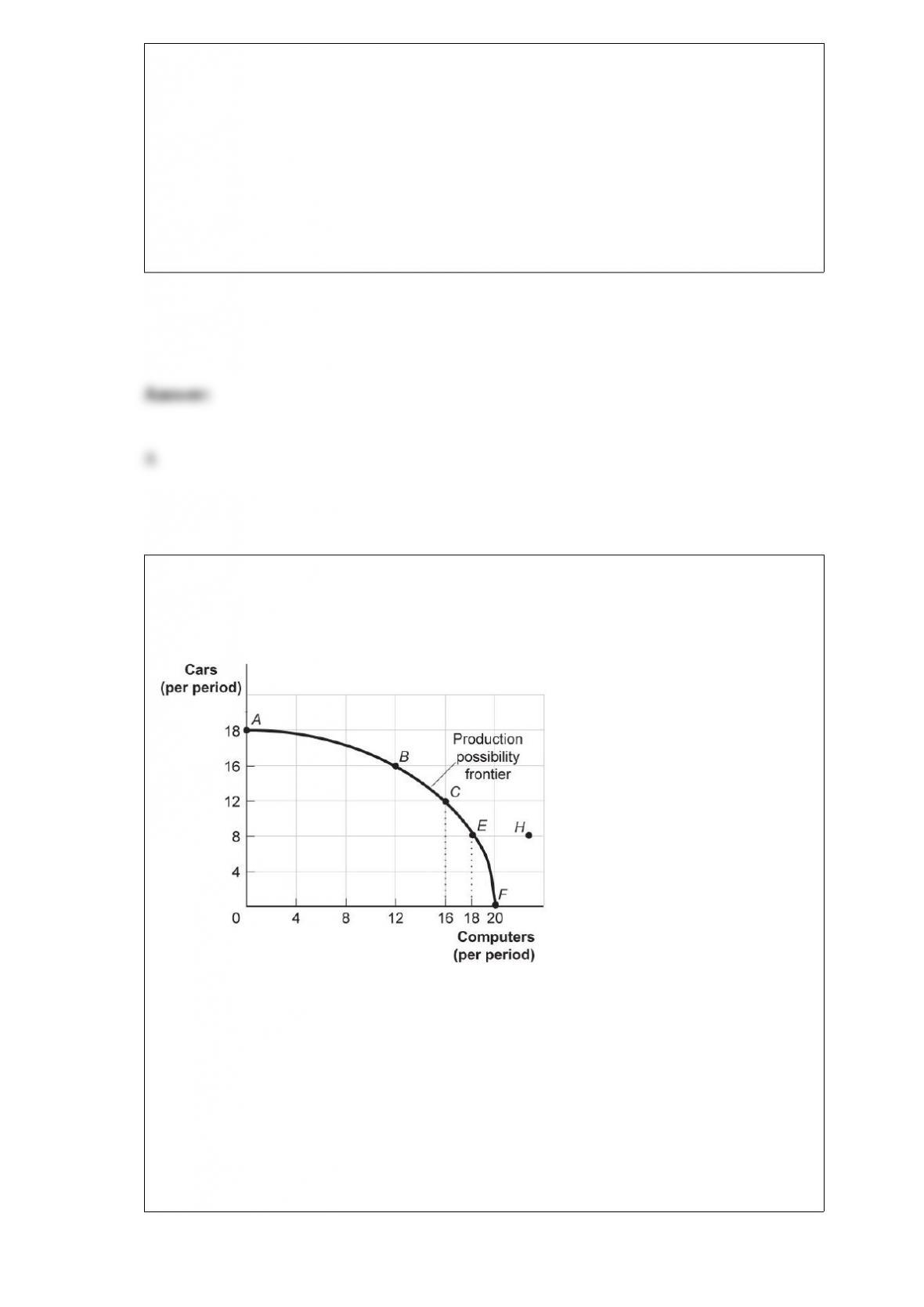

Figure: Production Possibility Frontier

(Figure: Production Possibility

Frontier) Look at the figure Production Possibilities Frontier. The combination of cars

and computers at point H:

A) can be attained but would cost too much.

B) cannot be attained given the level of technology and the resources available.

C) has no meaning, since it is not what consumers want.

D) is attainable but would increase unemployment.

Benny employs people to sell candy bars at intersections. The marginal product of the

last worker Benny hired is 20 candy bars per hour. Benny pays $7 per worker per hour

and sells the candy bars for $1 each. If the price of candy bars rises to $2, then the:

A) demand for labor increases.

B) demand for labor decreases.

C) quantity demanded of labor increases, but the demand for labor curve does not shift.

D) quantity demanded of labor decreases, but the demand for labor curve does not shift.

The Herfindahl”Hirschman index is a measure of concentration found by:

A) squaring the percentage market share of each firm in the industry.

B) squaring the percentage market share of each firm in the industry and then summing

the squared market shares.

C) summing the percentage market shares of each firm in the industry.

D) squaring the sums of the concentration ratios found in an industry survey of the

largest four and largest eight firms.

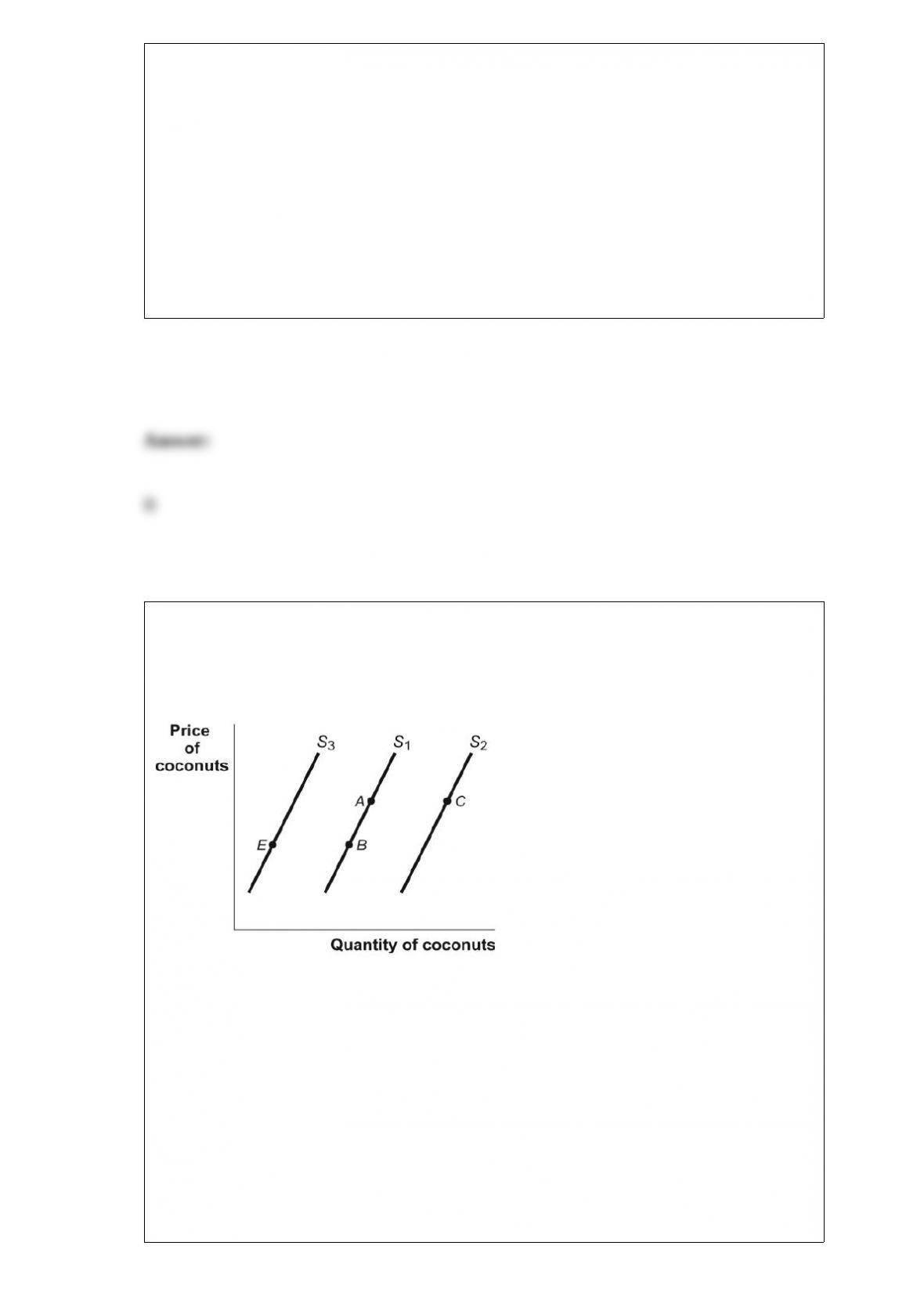

Figure: Supply of Coconuts

(Figure: Supply of Coconuts) Look at the figure Supply of Coconuts. An expectation on

the part of coconut suppliers that the price of coconuts will be significantly higher in the

very near future would be represented in the figure as a movement from:

A) A to B.

B) B to A.

C) A to C.

D) B to E.

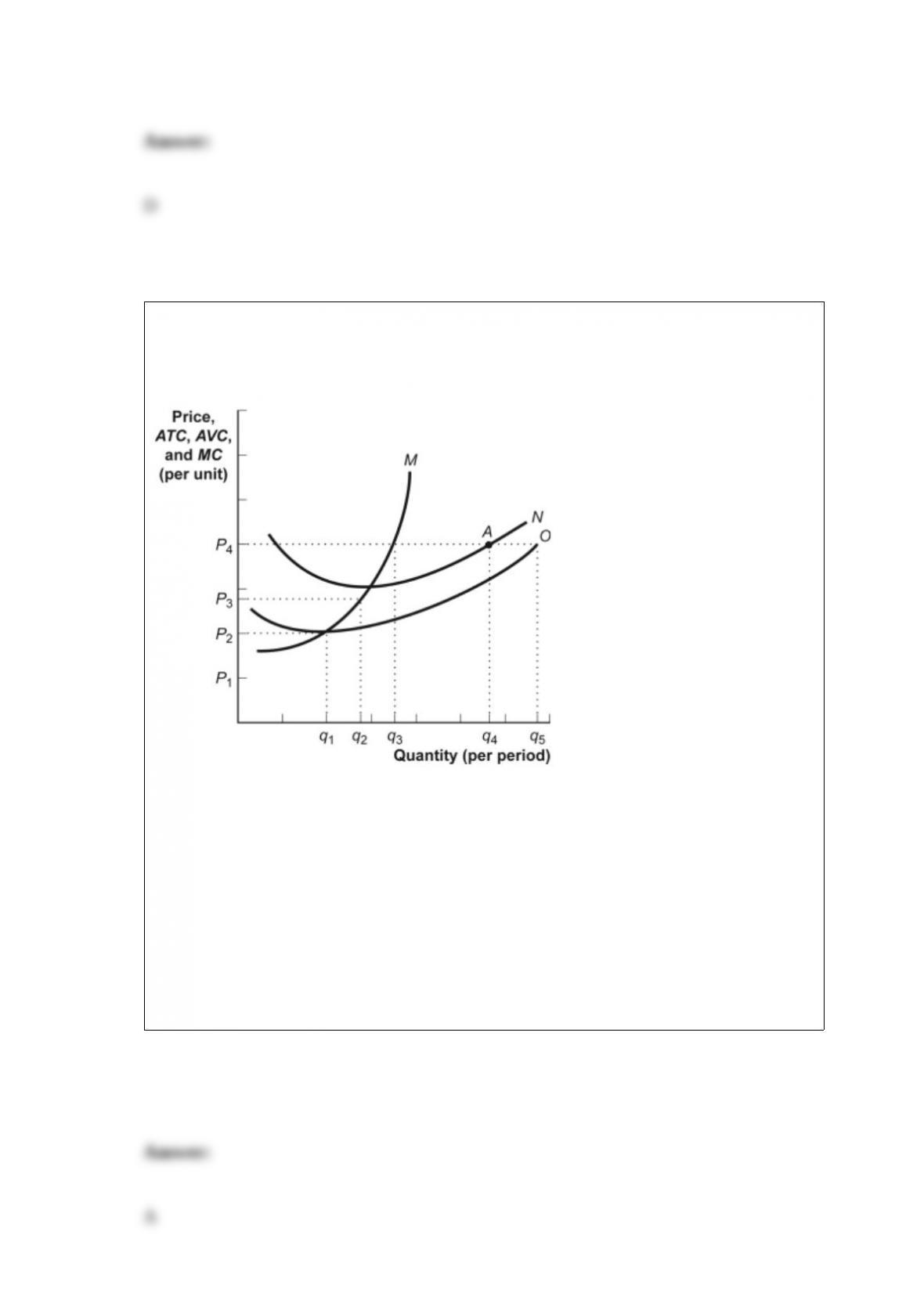

Figure: The Profit-Maximizing Firm in the Short Run

(Figure: The Profit-Maximizing Firm in the Short Run) Look at the figure The

Profit-Maximizing Firm in the Short Run. The ATC curve is represented by:

A) curve N.

B) curve M.

C) curve O.

D) none of the curves.

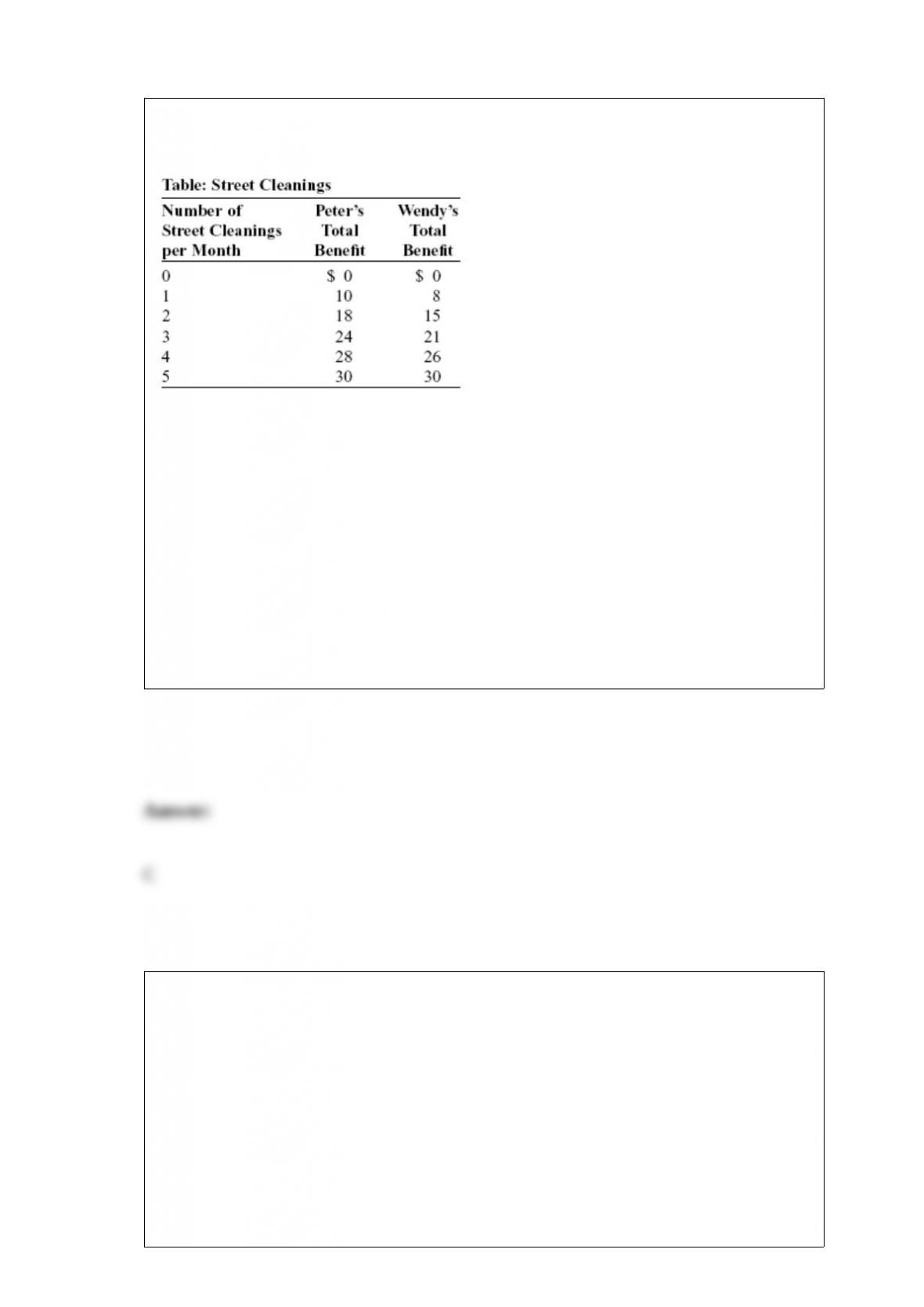

(Table: Street Cleanings) Look at the table Street Cleanings. What is the marginal social

benefit for Peter and Wendy together when the number of street cleanings per month

increases from 4 to 5?

A) $30

B) $60

C) $6

D) $15

Table: Utility from Oranges and Star Fruit Pounds of Oranges Total Utility from

Oranges Pounds of Star Fruit Total Utility 0 0 0 0 1 24 1 70 2 44 2 130 3 60 3 180 4

72 4 220 5 80 5 250 6 84 6 270 7 84 7 280

(Table: Utility from Oranges and Star Fruit) Look at the table Utility from Oranges and

Star Fruit. Oranges cost $2 per pound and star fruit costs $5 per pound. Calvin has $26

to spend. If Calvin buys 4 pounds of star fruit, how many pounds of oranges can he

buy?

Pounds of Oranges Total Utility from Oranges Pounds of Star Fruit Total Utility

0 0 0 0

1 24 1 70

2 44 2 130

3 60 3 180

4 72 4 220

5 80 5 250

6 84 6 270

7 84 7 280

A) 2

B) 3

C) 4

D) 7

When a firm finds that its ATC of production decreases as it increases production, this

firm is said to be experiencing:

A) profit maximization.

B) economic profit.

C) economies of scale.

D) a barrier to entry.