The production possibilities frontier model assumes all of the following except

A) labor, capital, land and natural resources are fixed in quantity.

B) the economy produces only two products.

C) any level of the two products that the economy produces is currently possible.

D) the level of technology is fixed and unchanging.

With an optimal two-part tariff

A) consumer surplus equals producer surplus.

B) all consumer surplus is transformed into profit.

C) consumers maximize consumer surplus.

D) the firm earns zero profit.

Suppose that an increase in capital per hour worked from $15,000 to $20,000 increases

real GDP per hour worked by $500. If capital per hour worked increases further to

$25,000, by how much would you expect real GDP per hour worked to increase if there

are diminishing returns?

A) by less than $500

B) by exactly $500

C) by more than $500 but less than $5,000

D) by more than $5,000 but less than $20,000

If the cross-price elasticity of demand between beer and wine is 0.31, then beer and

wine are

A) complements.

B) price inelastic goods.

C) substitutes.

D) necessities.

Joss is a marketing consultant. Iris and Daphne are potential customers interested in

commissioning Joss to undertake a market survey and compile the findings in a report.

Iris is willing to pay $500 for the service while Daphne is willing to pay $800. Suppose

that the opportunity cost of Joss’s time is $1,200. Assume that Iris and Daphne do not

know each other. If the price is $800 per copy

A) both Iris and Daphne will purchase Joss’s services and Joss will undertake the job.

B) only Daphne will purchase Joss’s services and Joss will undertake the job for her.

C) only Daphne will want to purchase Joss’s services but Joss will not be willing to do

the work.

D) neither Iris nor Daphne will commission the work.

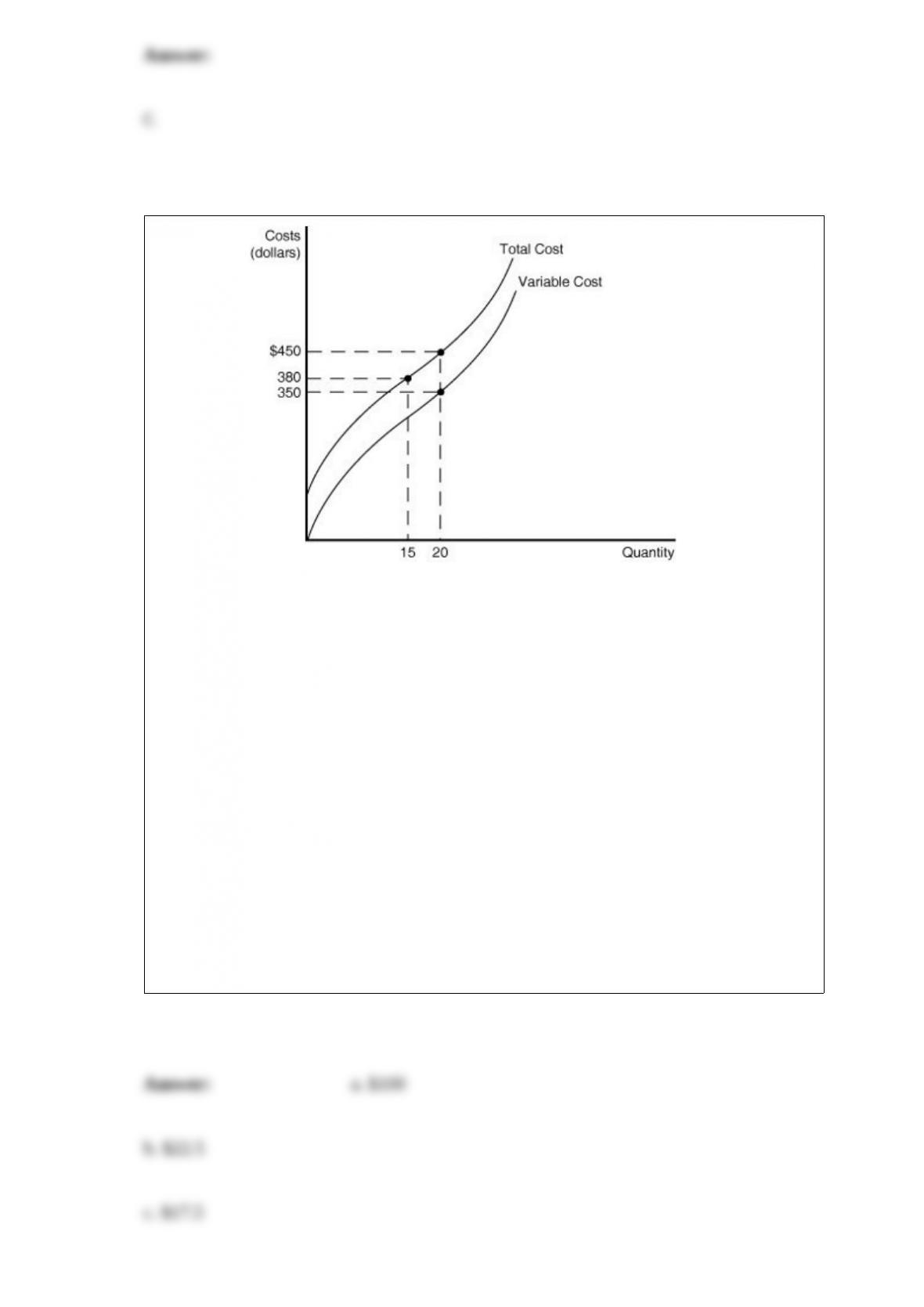

Figure 11-9

Solve the following problems.

a. Calculate the fixed cost of production.

b. Calculate the average total cost of production when the firm produces 20 units of

output.

c. Calculate the average variable cost of production when the firm produces 20 units of

output.

d. Calculate the average fixed cost of production when the firm produces 20 units of

output.

e. Calculate the average fixed cost of production when the firm produces 15 units of

output.

f. If the firm increases output from 15 to 20 units what is the marginal cost of output?

Figure 4-5

The figure above represents the market for pecans. Assume that this is a competitive

market. If the price of pecans is $9, what changes in the market would result in an

economically efficient output?

A) The price would decrease, the quantity supplied would decrease, and the quantity

demanded would increase.

B) The quantity supplied would increase, the quantity demanded would decrease, and

the equilibrium price would decrease.

C) The price would decrease, the demand would increase, and the supply would

decrease.

D) The price would increase, the quantity demanded would decrease, and the quantity

supplied would increase.

Figure 5-2

Figure 5-2 shows a market with a negative externality.

The true marginal cost of the last unit produced is represented by the price

A) Pa.

B) P.

C) Pc.

D) Pf.

Firms that are price takers

A) must lower their prices to increase sales.

B) are able to sell a fixed quantity of output at the market price.

C) can raise their prices as a result of a successful advertising campaign.

D) are able to sell all their output at the market price.

Pricing insurance policies is made Difficult because buyers have more information than

sellers. This Difficulty is an example of

A) moral hazard.

B) adverse selection.

C) asymmetric information.

D) the free rider problem.

Ceteris paribus, a rise in interest rates in the United States will cause the yen price of

the dollar in international exchange markets to ________. I.e., the dollar ________ in

value against the yen.

A) increase; appreciates

B) increase; depreciates

C) decrease; depreciates

D) decrease; appreciates