1) Which of the following statements about a competitive firm is correct?

A.To maximize profits a competitive firm should produce at that output at which total

revenue is greatest

B.In long-run equilibrium a competitive firm will produce at the point of minimum

average costs

C.A competitive firm will produce in the short run so long as total receipts are sufficient

to cover total fixed costs

D.A competitive firm will close down in the short run whenever price is less than the

minimum attainable average total cost

2) An indifference curve shows all:

A.possible equilibrium positions on an indifference map.

B.equilibrium combinations of two products that are obtainable with a given money

income.

C.combinations of two products yielding the same total utility to a consumer.

D.possible combinations of two products that a consumer can purchase, given her

income and the prices of the products.

3) Which of the following is correct?

A.The nominal wage may fall, but the real wage can never decline.

B.The real wage may fall, but the nominal wage can never decline.

C.Both the nominal and the real wage must always rise.

D.The nominal and the real wage may both fall.

4) Firms in an industry will not earn long-run economic profits if:

A.Fixed costs are zero

B.The number of firms in the industry is fixed

C.There is free entry and exit of firms in the industry

D.Production costs for a given level of output are minimized

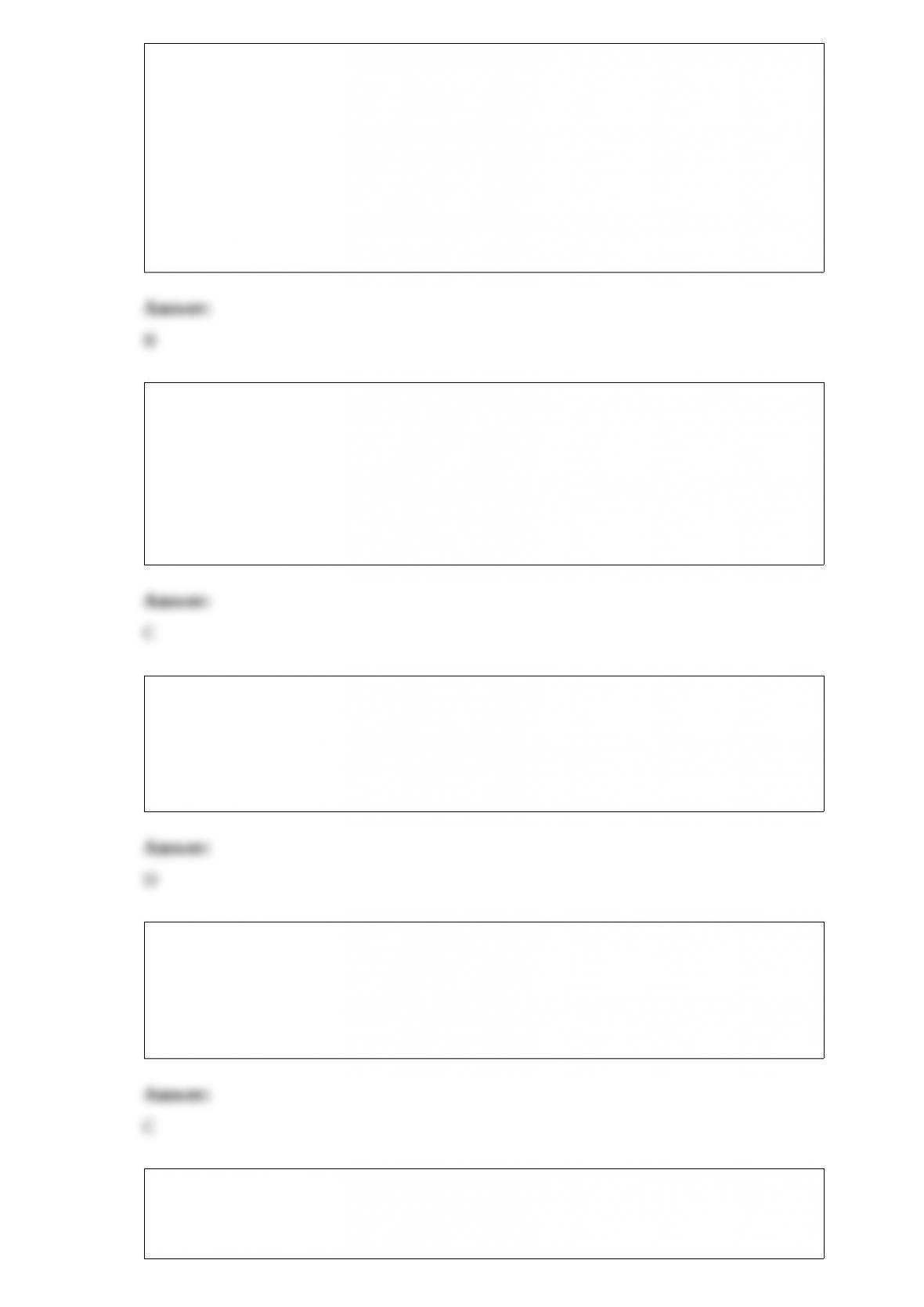

5) Answer the question based on the following payoff matrix for a duopoly in which the

numbers indicate the profit in thousands of dollars for a high-price or a low-price

strategy.

Refer to the above payoff matrix. If both firms collude to maximize joint profits, the

total profits for the two firms will be:

A.$1,200,000

B.$1,250,000

C.$1,400,000

D.$1,500,000

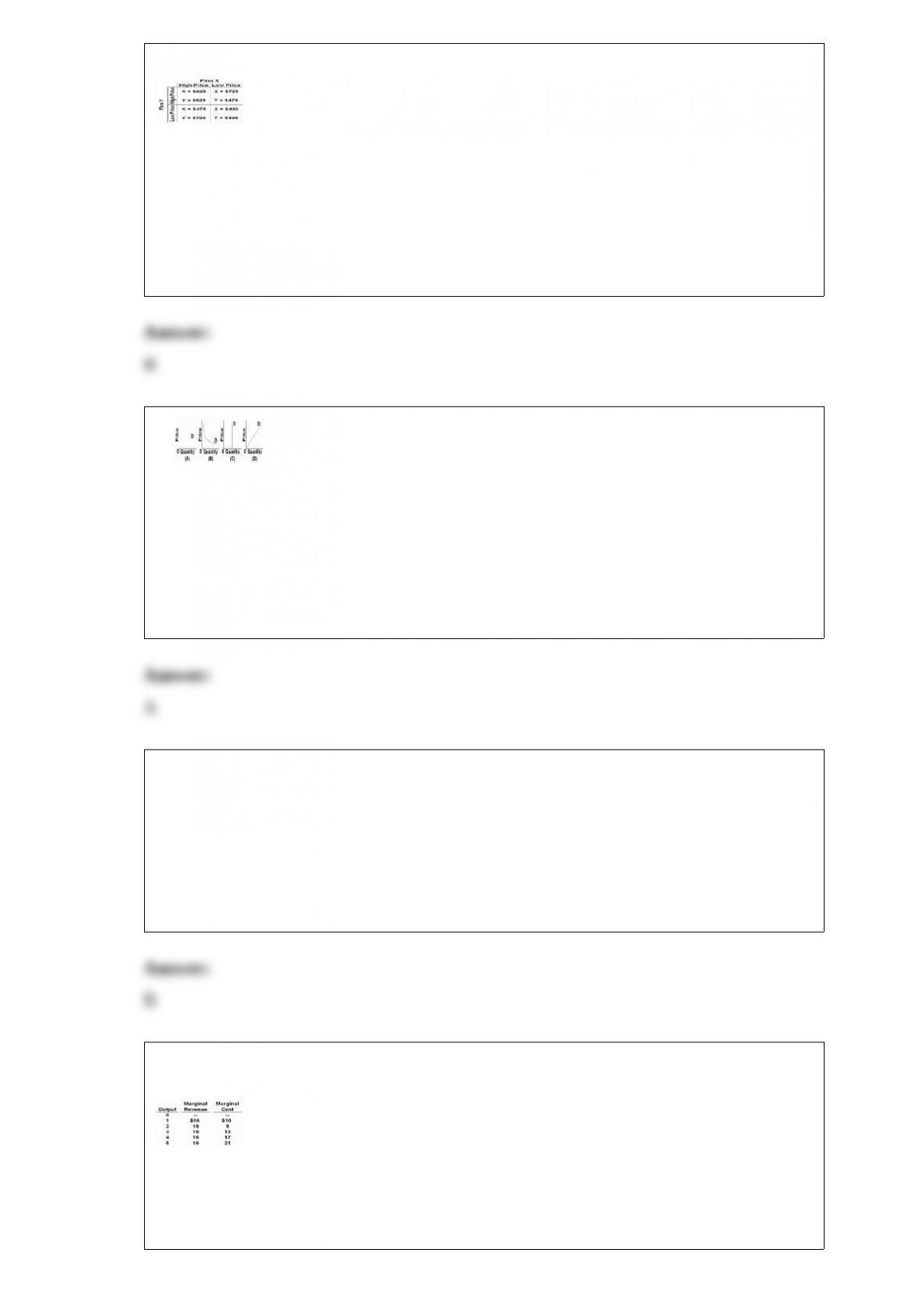

6)

Refer to the graphs above. Which one shows a situation where buyers are all willing to

pay one uniform price for the product?

A.Graph A

B.Graph B

C.Graph C

D.Graph D

7) Which of the following best explains why the solar panel companies Solyndra and

Abound went bankrupt in 2011 and 2012, respectively?

A.Overreliance on government subsidies that made them inefficient.

B.Oversupply of solar panels on the world market that drove down prices and made

these firms uncompetitive in the market.

C.Expansion of other alternative energy sources made solar power unprofitable.

D.Dramatic and unexpected increases in input costs caused huge economic losses.

8) Answer the question on the basis of the following data confronting a firm:

Refer to the data. At the profit-maximizing output, the firm’s total revenue is:

A.$48.

B.$32.

C.$80.

D.$64.

9) Under what conditions would an increase in demand lead to a lower long-run

equilibrium price?

A.The firms in the market are part of a decreasing-cost industry.

B.The firms in the market produce an inferior good.

C.Potential new firms in the market are not attracted by economic profits.

D.Increases in demand cannot lead to lower long-run equilibrium prices.

10)

The industry represented by the graph above must be one where:

A.Resource prices rise when the industry contracts

B.Resource prices fall when the industry expands

C.Resource prices fall when the industry contracts

D.Resource prices are unaffected by the industry’s expansion

11) You are the newly appointed sales manager of the Rock Computer Tablets Company

and have been charged with the task of increasing revenues. Your economics

consultants have informed you that at present price and output levels, price elasticity of

demand for your product is less than one. You should:

A.Decrease prices

B.Increase prices

C.Hold prices constant and increase supply

D.Cut advertising expenditures to save money

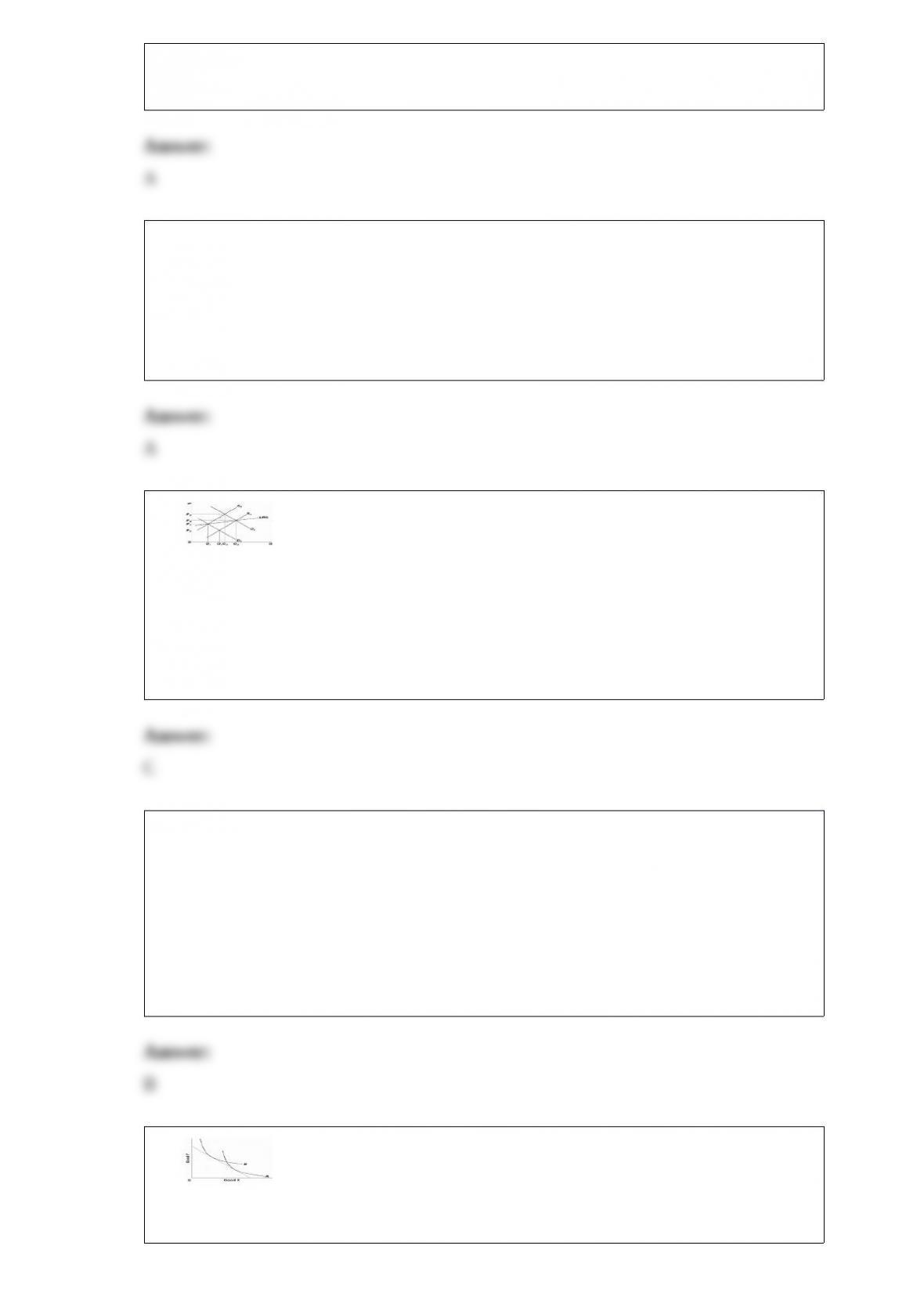

12)

In the graph above, the change in the individual’s preferences indicated by a shift from

indifference curve A to indifference curve B will result in:

A.A decrease in demand for good Y

B.No change in the demand for good Y

C.A decrease in demand for good X

D.An increase in demand for good X

13)

Refer to the diagram. The direct economic impact of the destruction and loss of lives

caused by the terrorist attacks of September 11, 2001, is illustrated by the:

A.shift of the production possibilities curve from CD to AB.

B.shift of the production possibilities curve from AB to CD.

C.move from x to y on production possibilities curve AB.

D.move from y to x on production possibilities curve AB.

14) The market system:

A.produces considerable inefficiency in the use of scarce resources.

B.effectively harnesses the incentives of workers and entrepreneurs.

C.is not consistent with freedom of choice in the long run.

D.has slowly lost ground to emerging command systems.

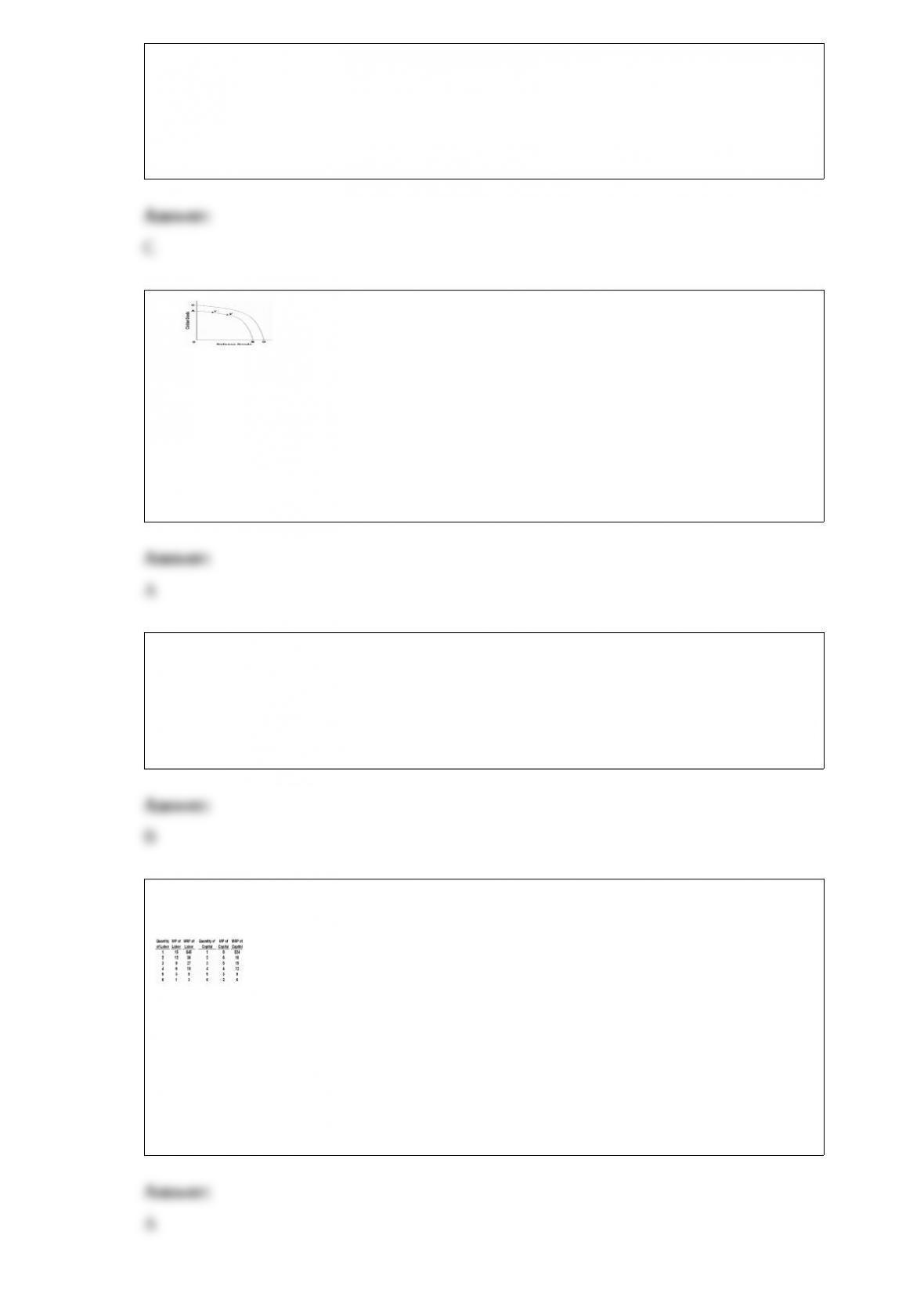

15) Answer the question on the basis of the following data:

Refer to the given data. If the prices of labor and capital are $9 and $15 respectively,

and labor and capital are the only inputs, the firm’s economic profits will be:

A.$102.

B.$82.

C.$67.

D.$28.

16) When a tariff or quota on a product is removed, this policy action:

A.Benefits domestic producers of the product

B.Benefits consumers of the product

C.Benefits the government

D.Hurts nations exporting the product

17) The TANF program:

A.is a form of social insurance.

B.has been found to be unconstitutional by the Supreme Court.

C.limits total lifetime welfare benefits to 5 years and requires able-bodied adults to

work after receiving benefits for 2 years.

D.perpetuates the so-called culture of poverty.