1) “International trade” refers to:

A.purchasing or selling currently produced goods or services across an international

border.

B.any transaction across an international border.

C.any financial transaction across an international border.

D.buyer or selling of preexisting assets across an international border.

2) a nation’s gross domestic product (gdp):

a.can be found by summing c + ig + g + xn.

b.is the dollar value of the total output produced by its citizens, regardless of where they

are living.

c.can be found by summing c + s + g + xn.

d.is always some amount less than its ndp.

3) Consider the following situations. Evaluate how they would affect the level of

productivity of labor.

(a)The cost of health care skyrockets.

(b)Trade barriers with other countries are reduced.

(c)An energy shortage develops.

(d)Vast improvements are made in production technology.

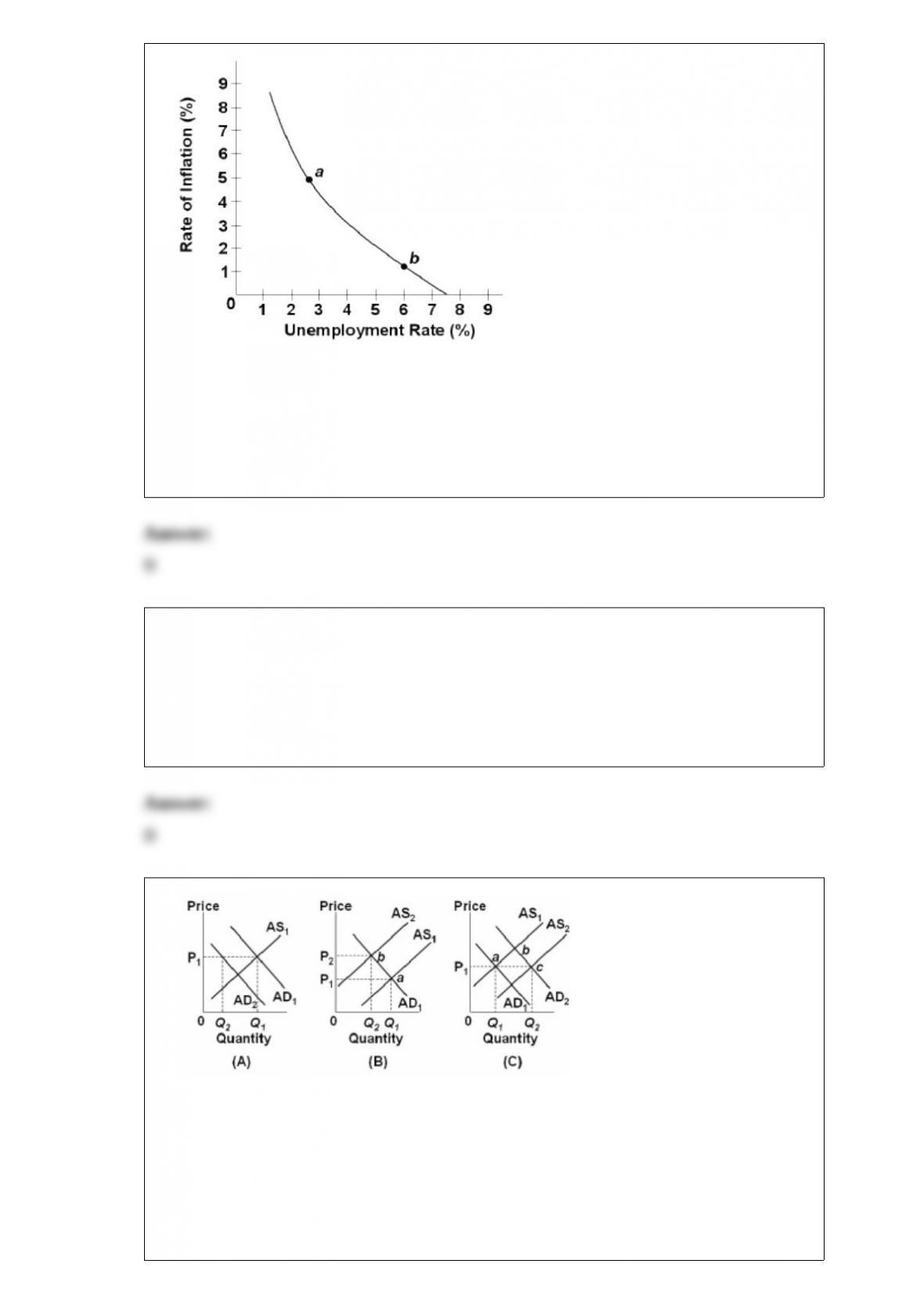

4)

Refer to the above diagram for a specific economy. A reduction in structural

unemployment or bottleneck problems in labor markets will:

A.shift this curve to the right.

B.shift this curve to the left.

C.move this economy southeast along the curve.

D.move this economy northwest along the curve.

5) The transactions demand for money is most closely related to money functioning as

a:

A.unit of account.

B.medium of exchange.

C.store of value.

D.measure of value.

6)

Refer to the above diagrams, in which AD1 and AS1 are the “before” curves and AD2

and AS2 are the “after” curves. Other things equal, an increase in investment spending

is depicted by:

A.panel (A) only.

B.panel (B) only.

C.panel (C) only.

D.panels (B) and (C).

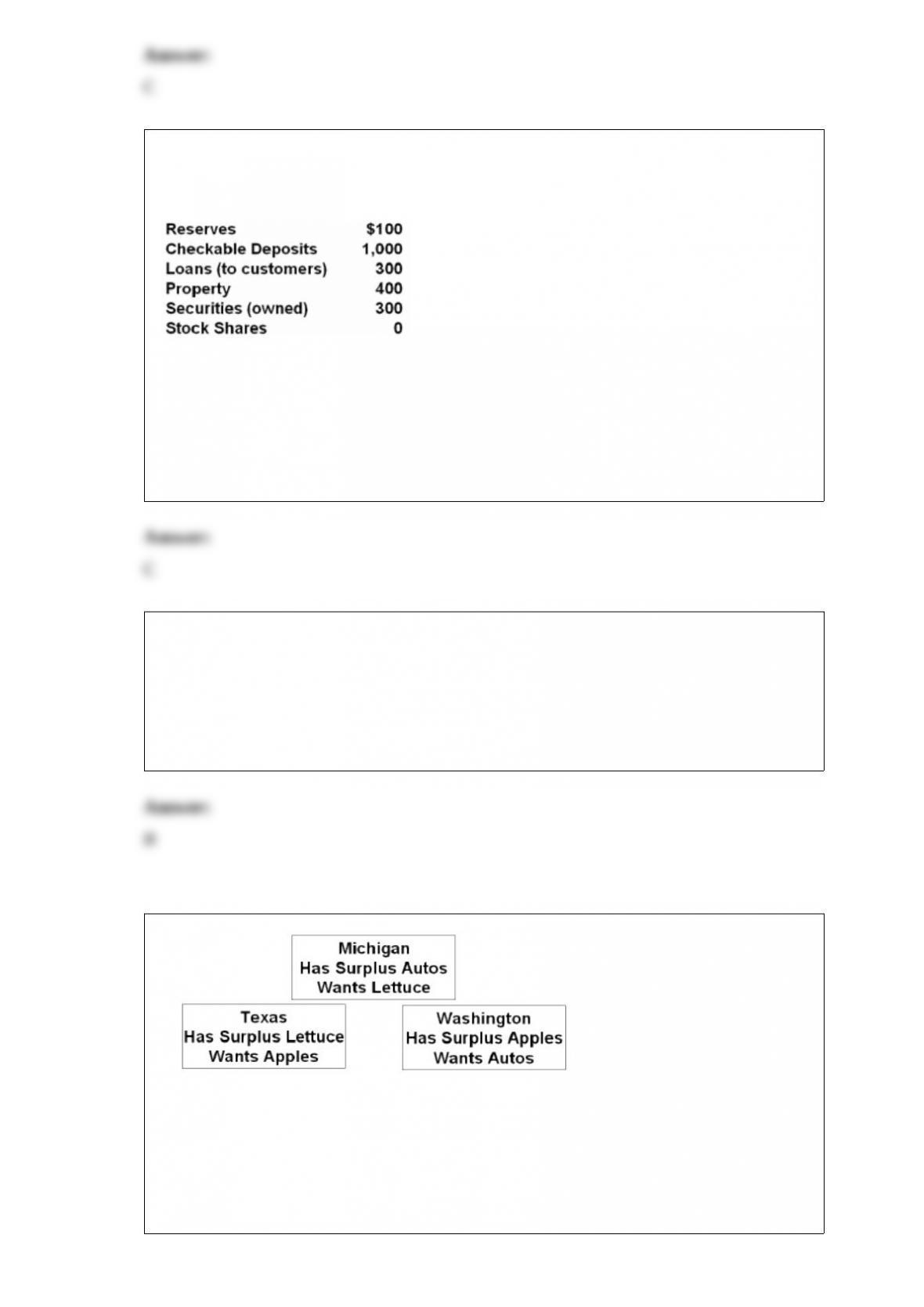

7) The following information for the Moolah Bank.

Assume that the listed amounts constitute this bank’s complete set of accounts.

Moolah’s:

A.assets are $1000.

B.liabilities are $300.

C.net worth is $100.

D.annual profit is $200.

8) Which of the following statements is correct?

A.Interest rates and bond prices vary directly.

B.Interest rates and bond prices vary inversely.

C.Interest rates and bond prices are unrelated.

D. Interest rates and bond prices vary directly during inflations and inversely during

recessions.

9)

on the basis of the above information and assuming trade occurs between the three

states we can expect:

a.washington to exchange apples with texas and receive money in return.

b.washington to exchange apples with michigan and receive money in return.

c.texas to exchange lettuce with michigan and receive autos in return.

d.texas to trade lettuce directly for washington apples.

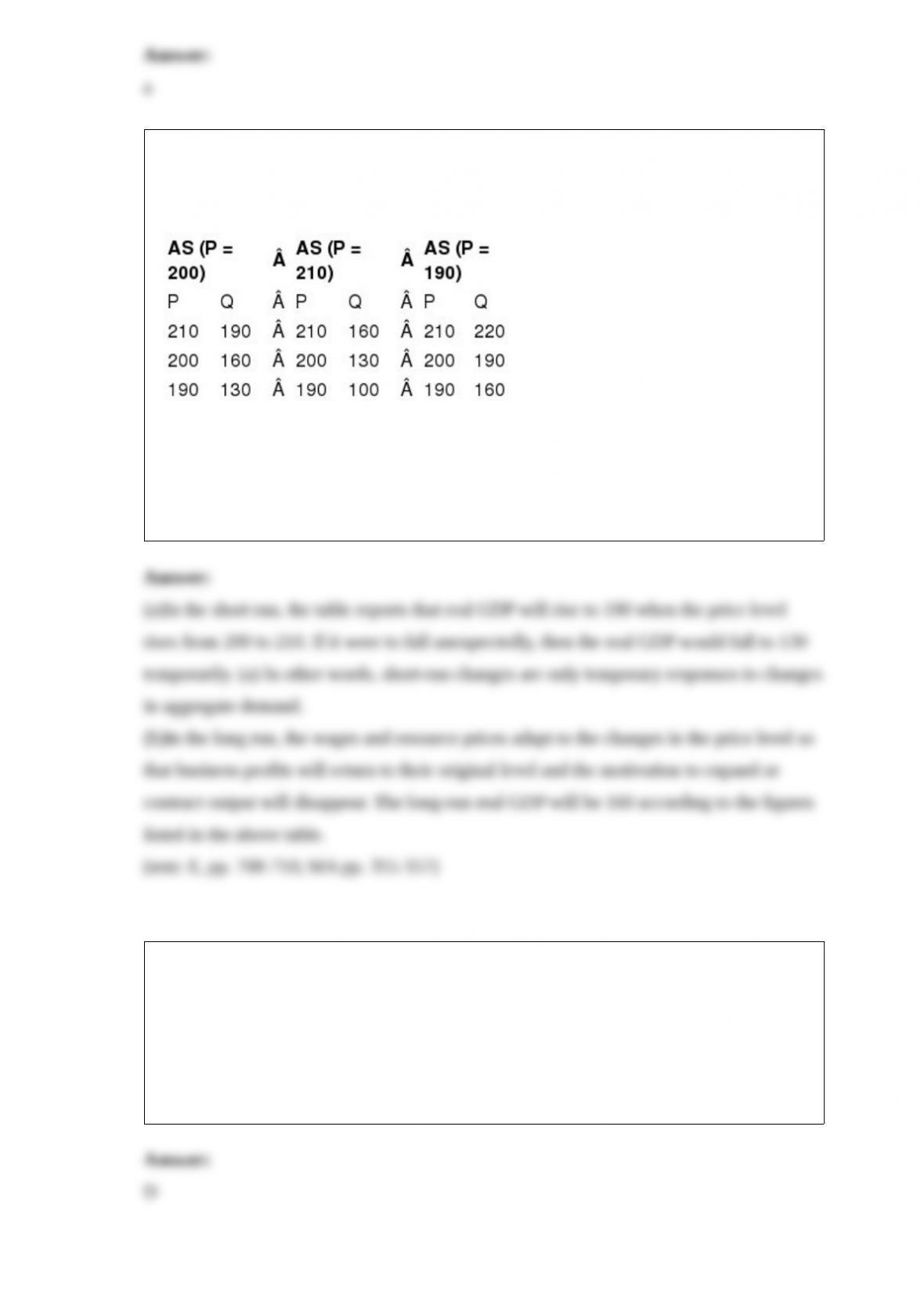

10) Suppose the potential level of real domestic output (Q) for a hypothetical economy

is $160 and the price level (P) initially is 200. Use the following short-run aggregate

supply schedules to answer the questions.

(a)What will be the short-run level of real GDP if the price level rises unexpectedly

from 200 to 210 because of an increase in aggregate demand? Falls unexpectedly from

200 to 190 because of a decrease in aggregate demand? Explain each situation.

(b)What will be the long-run level of real GDP when the price level rises from 200 to

210? Falls from 200 to 190? Explain each situation.

11) The basic economic argument for greater income equality is that:

A.an equal distribution of income is the logical outcome of any tax-transfer program.

B.because citizens enjoy political equality, they are also entitled to economic equality.

C.a more equal distribution of income will tend to maximize incentives to work, invest,

and assume risk.

D.a more equal distribution of a given amount of income will increase the total utility

of consumers.

12) suppose the nominal annual interest rate on a two year loan is 8 percent and lenders

expect inflation to be 5 percent in each of the two years. the annual real rate of interest

is:

a.6 percent.

b.8 percent.

c.2 percent.

d.3 percent.

13) in terms of the circular flow diagram, households make expenditures in the _____

market and receive income through the _____ market.

a.product; financial

b.resource; product

c.product; resource

d.capital; product

14) Identify the ways in which each of the following determinants would have to

change if each was causing a decrease in aggregate demand: consumer wealth,

consumer expectations, business taxes, national income in countries abroad, exchange

rates.

15) What has been the general approach to the enforcement of antitrust laws based on

the type of mergers and price fixing among firms?

16) How do uncertainty and expectations influence economic behavior?

17) Define a sequential game.

18) Why is there a supply curve in pure competition but no supply curve in pure

monopoly?

19) Explain how monopoly causes an inefficient allocation of resources when the

competitive firm does not, even when both seek to maximize profits.

20) Why is the marginal revenue product schedule a demand schedule for the individual

firm in a purely competitive resource market and selling output in a purely competitive

product market?