Which of the following non-linear adjustments CANNOT be accommodated using

OLS?

a.) including an independent variable that has been raised to a power

b.) taking a logarithmic transformation of the dependent variable

c.) including a binary indicator variable

d.) raising parameters to a power

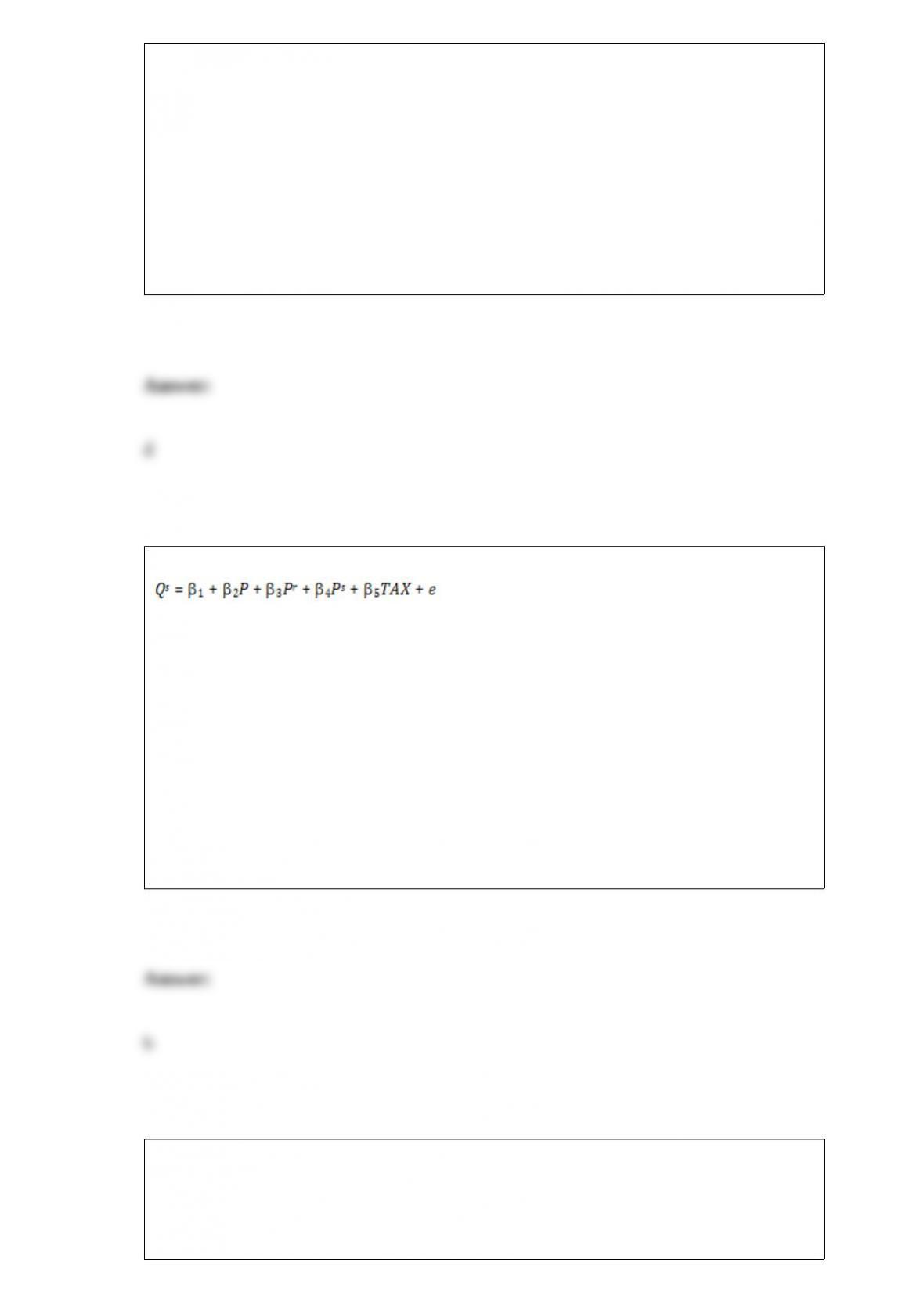

Refer to the following equation:

where Q is annual quantity supplied, P is the price of the product, P is the price of

resources, P is the price of goods that are substitutes in production, and TAX is the

excise tax on the product. This equation is

a.) an economic model

b.) an econometric model

c.) a market model

d.) a non-linear model

What hypothesis is tested when using the Jarque-Berra test ?

a.) H0: The model is correctly specified as estimated

b.) H0: The error terms are normally distributed

c.) H0: The error terms are uncorrelated with x

d.) H0: The error terms are random

Using the notation ARDL(p,q) what does q represent?

a.) the number of lagged dependent variables included as explanatory variables

b.) the number of lagged explanatory variables included

c.) the frequency of the time series

d.) the degree or integration in the error term

What type of model shows how series react dynamically to shocks?

a.) a VAR model

b.) an impulse response function

c.) variance decomposition

d.) an ARDL model

Under the Gauss-Markov Theorem when assumptions SR1 – SR5 are met, what

estimators of and b2 may have smaller variances than 1 and 2?

a.) none

b.) a non-linear estimator

c.) a normally distributed estimator

d.) an estimator derived from economic theory

You estimate a simple linear regression model using a sample of 62 observations and

obtain the following results (estimated standard errors in parentheses below coefficient

estimates):

y = 97.25 + 33.74 *x

(3.86) (9.42)

What are the endpoints of the interval estimator for with a 95% interval estimate?

a.) (14.90, 52.58)

b.) (24.32, 43.16)

c.) (-3.58, 3.58)

d.) (30.16,37.32)

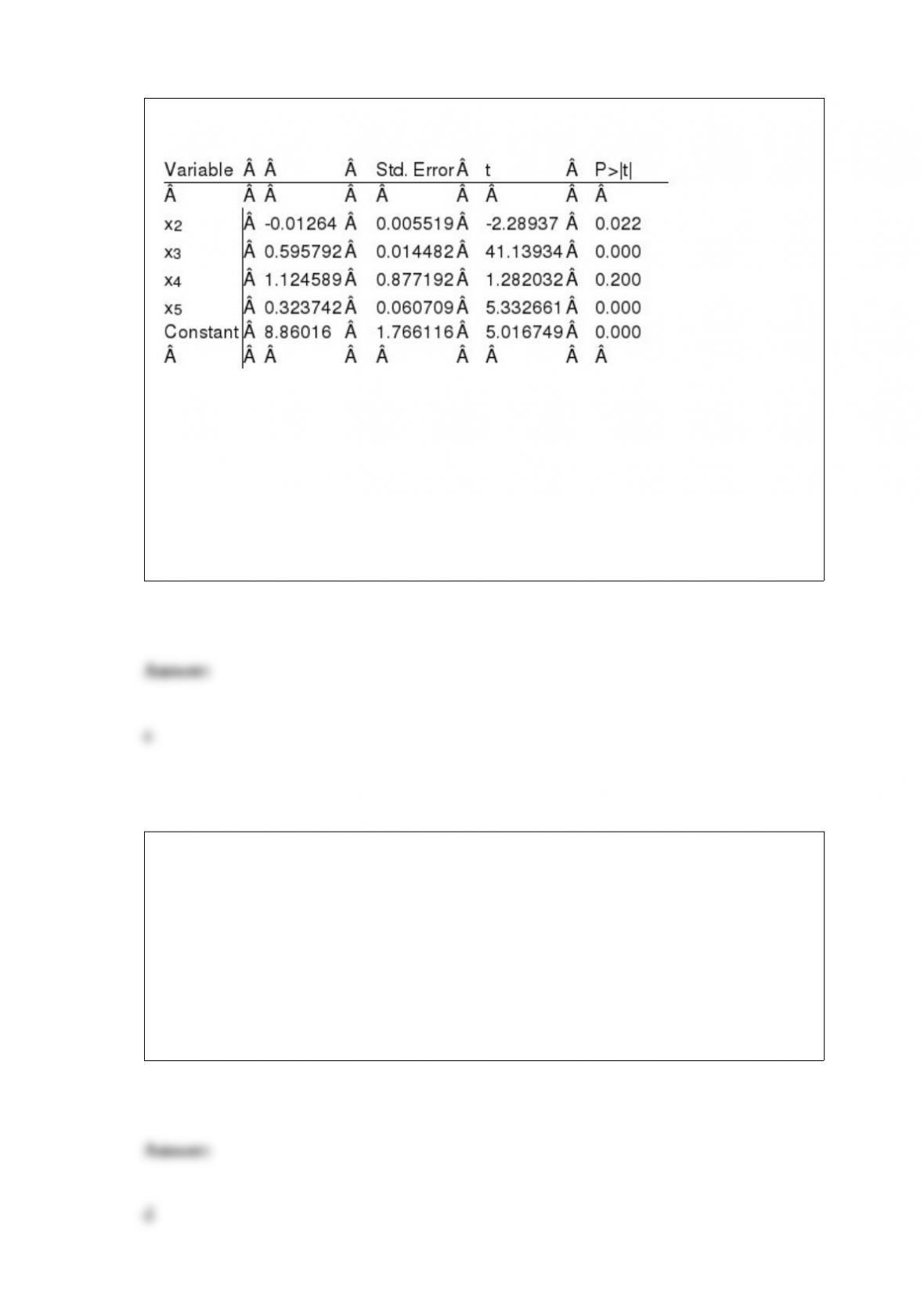

A model estimated using a dataset with 65 observations generates the following results.

What are the endpoints for the 99% confidence interval for b5? a.) (0.1623, 0.4852)

b.) (-5.0089 , 5.6564)

c.) (0.2630 , 0.3845)

d.) (0.1786 , 0.4688)

Which type of model has coefficients that vary with i and t?

a.) pooled model

b.) fixed effects

c.) random effects

d.) none of these

How does the least squares estimator perform on a simultaneous equation model with

an endogenous regressor?

a.) unbiased and consistent in large samples

b.) unbiased but inconsistent in all sample sizes

c.) biased but consistent in large samples

d.) biased and inconsistent for structural equations, but unbiased and consistent for

reduced form equations

What are the implications for 2SLS estimators if reduced form parameter estimates are

statistically insignificant?

a.) still consistent in large samples, but no longer BLUE

b.) there will be correlation in the structural equations, causing estimators to be

inconsistent

c.) there are no consequences, only structural parameters matter

d.) small sample properties no longer hold, but asymptotic properties still apply

Why is the variance of the forecast y larger than the variance of the expected value of

y?

a.) the estimated forecast variance includes an estimate of ŝ2

b.) the estimated forecast variance includes weighted covariance terms of all paired

variables

c.) the Gauss-Markov theorem does not apply to forecast of a single observation

d.) the expected value of confidence intervals rely on the standard normal distribution

while forecast use a t distribution.

If you reject the null hypothesis when testing for ARCH effects, what should you

conclude?

a.) the variance changes over time

b.) the variance is constant

c.) the mean is constant

d.) the mean varies over time

Which regional Federal Reserve Bank provides access to large amounts of economic

data through FRED?

a.) Boston

b.) New York

c.) San Francisco

d.) St. Louis

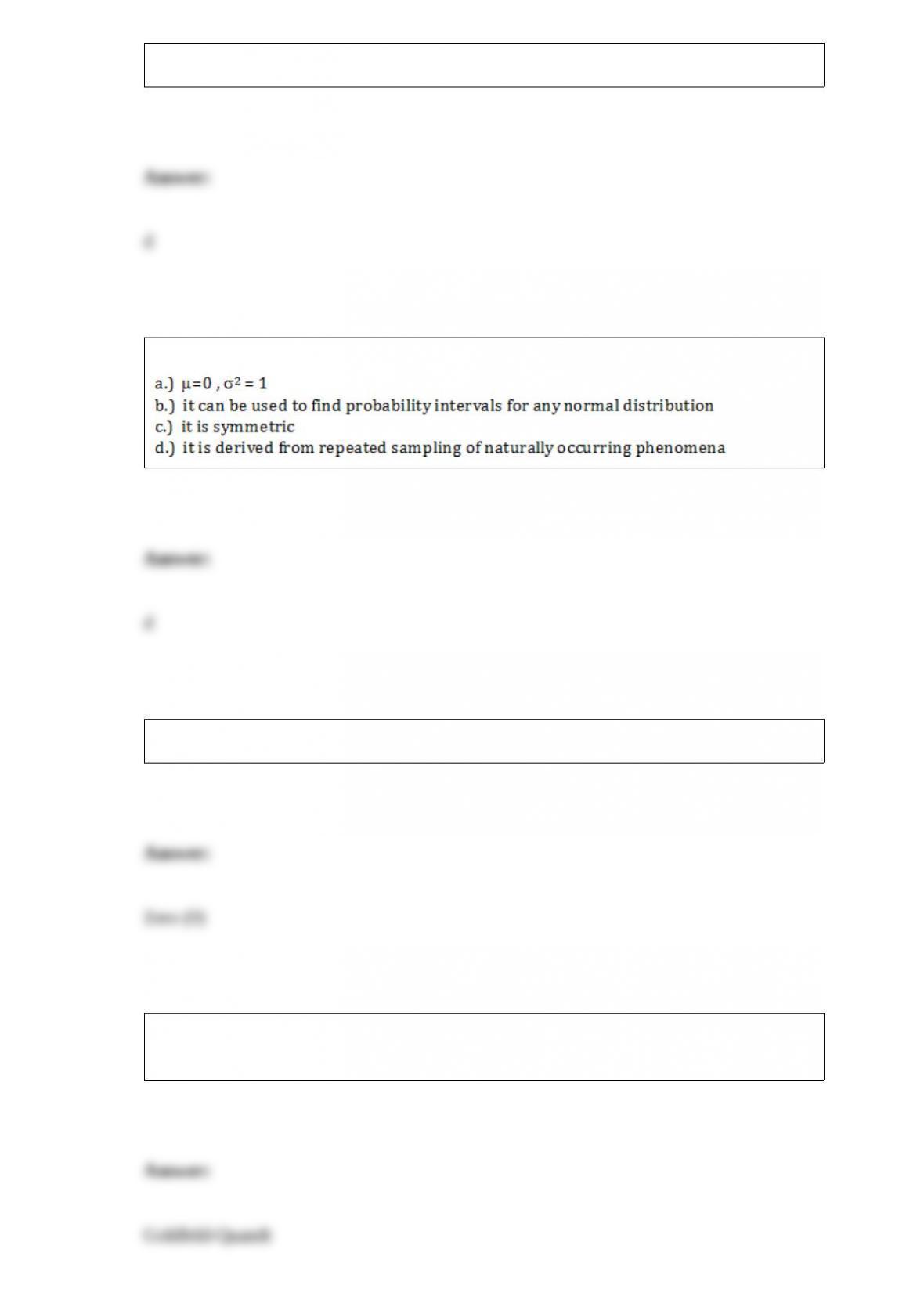

Which of the following statements about the standard normal distribution is NOT true?

What is the skewness of the normal distribution?

What test for heteroskedasticity should be used if you suspect the error terms have

different variances by category?

A measure of the symmetry of a distribution is ________________________.

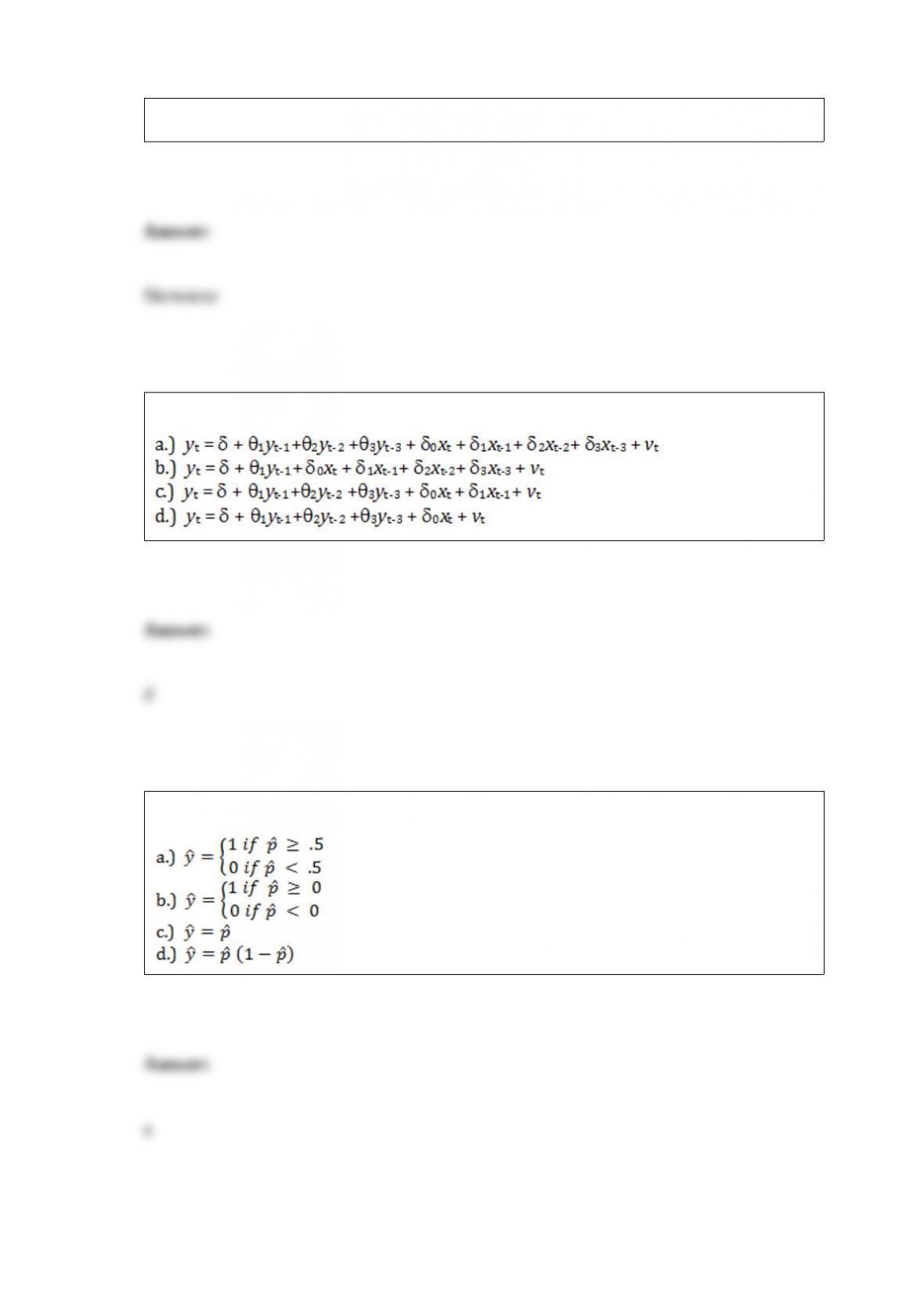

Which of the following is an ARDL(2,0) model?

How are choices predicted in a binary choice model?

) The difference between a pdf and cdf is ___________________________.