If a firm operating in monopolistic competition is producing a quantity that generates

MC = MR, then the marginal decision rule tells us that profit:

A) is maximized.

B) can be increased by decreasing production.

C) can be increased by decreasing the price.

D) is maximized only if MC = P.

A progressive tax:

A) takes a larger share of the income of high-income taxpayers than of low-income

taxpayers.

B) takes a smaller share of the income of high-income taxpayers than of low-income

taxpayers.

C) takes the same share of the income of high-income taxpayers as it does of

low-income taxpayers.

D) has no deadweight loss.

Suppose that each of the two firms in a duopoly has the independent choice of

advertising or not advertising. If neither advertises, each gets $10 million in profit; if

both advertise, their profits will be $5 million each; and if one advertises while the

other does not, the advertiser gets profit of $15 million and the other gets profit of $2

million. According to game theory, the Nash equilibrium is:

A) both may or may not advertise.

B) one will advertise and the other will not.

C) both will advertise.

D) neither will advertise.

After graduation from college, you might have an increase in your income from a new

job. If as a result you decide that you will purchase more T-bone steak and less

hamburger, then for you hamburger is a(n) _____ good.

A) normal

B) substitute

C) complementary

D) inferior

A perfectly competitive industry with constant costs initially operates in long-run

equilibrium. When demand increases:

A) in the short run, prices and profits will be higher, but in the long run, price will fall

back to its original level and firms will again earn zero economic profit.

B) in the long run and the short run, prices and profits will be higher than before the

demand increase.

C) in the short run, prices and profits will fall, but in the long run, price will rise back to

its initial level, as will profits.

D) in the long run and the short run, prices and profits will be lower than before the

demand increase.

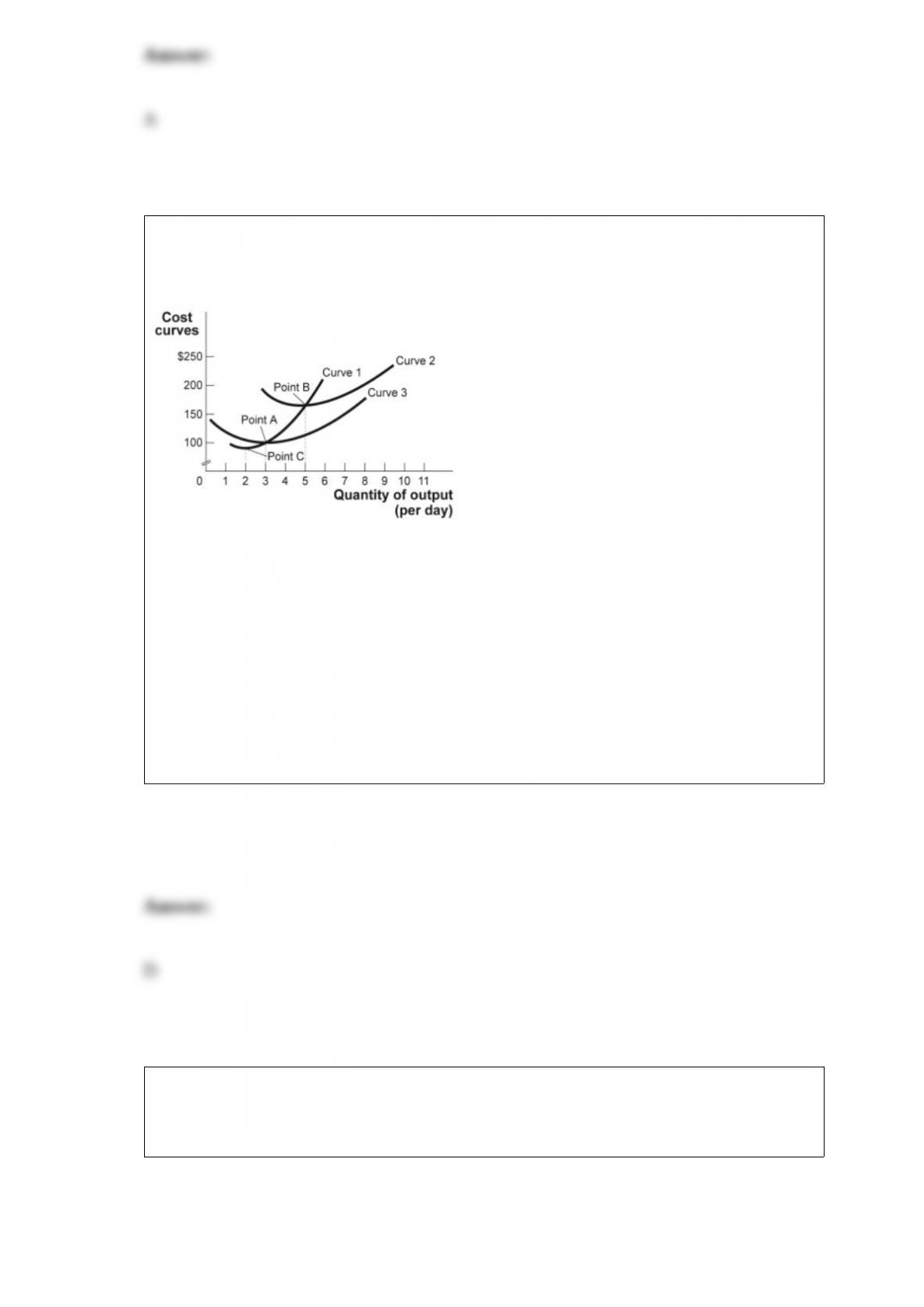

Figure: Short-Run Costs II

(Figure: Short-Run Costs II) Look at the figure Short-Run Costs II. Curve 3 is the

_____ cost curve.

A) average total

B) total

C) marginal

D) average variable

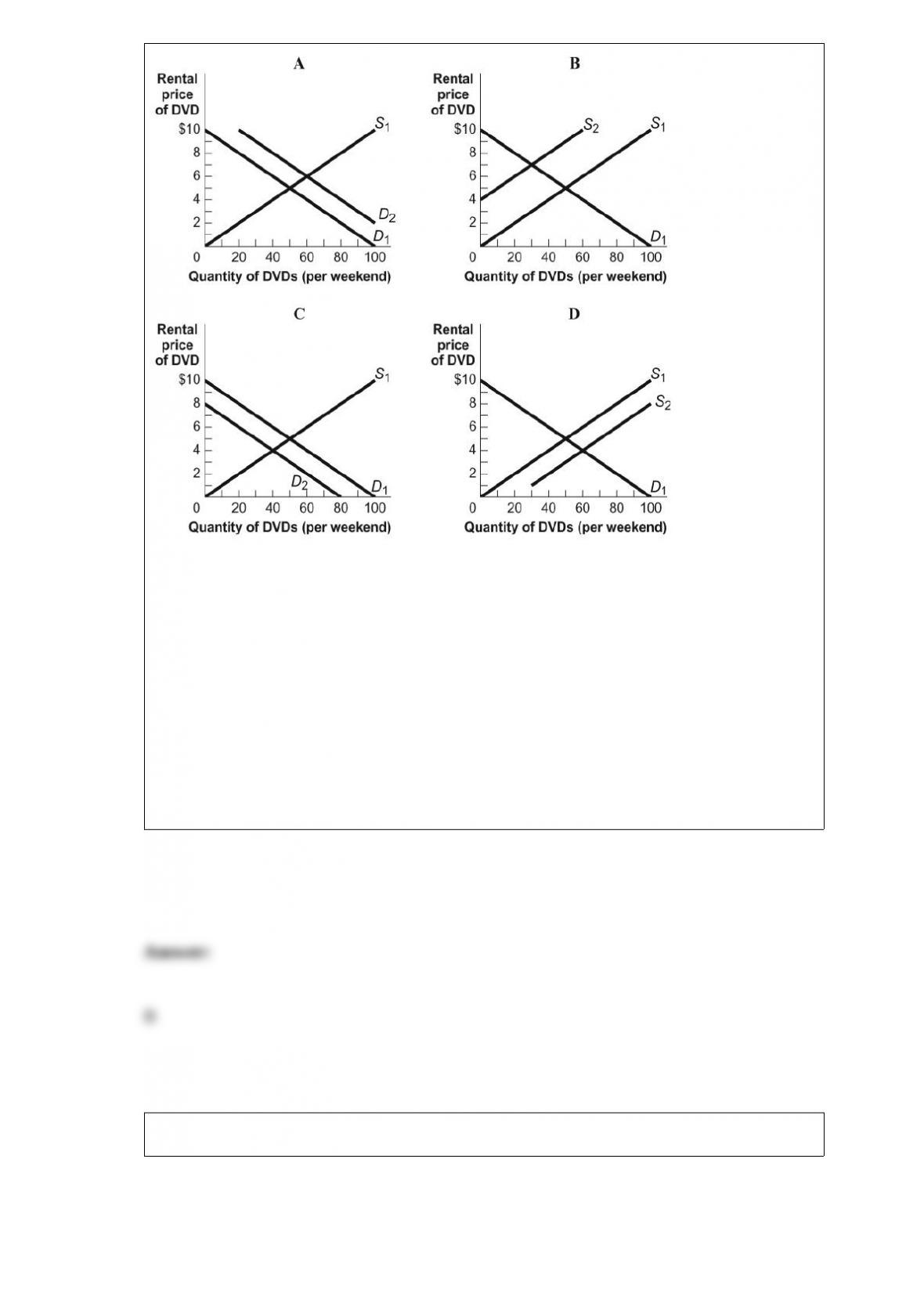

Figure: Four Markets for DVDs

(Figure: Four Markets for DVDs) Look at the figure Four Markets for DVDs. Which of

the graphs shows what may happen if D1 or S1 is the original curve and D2 or S2 is the

new curve and if some of the stores that rent DVDs close?

A) A

B) B

C) C

D) D

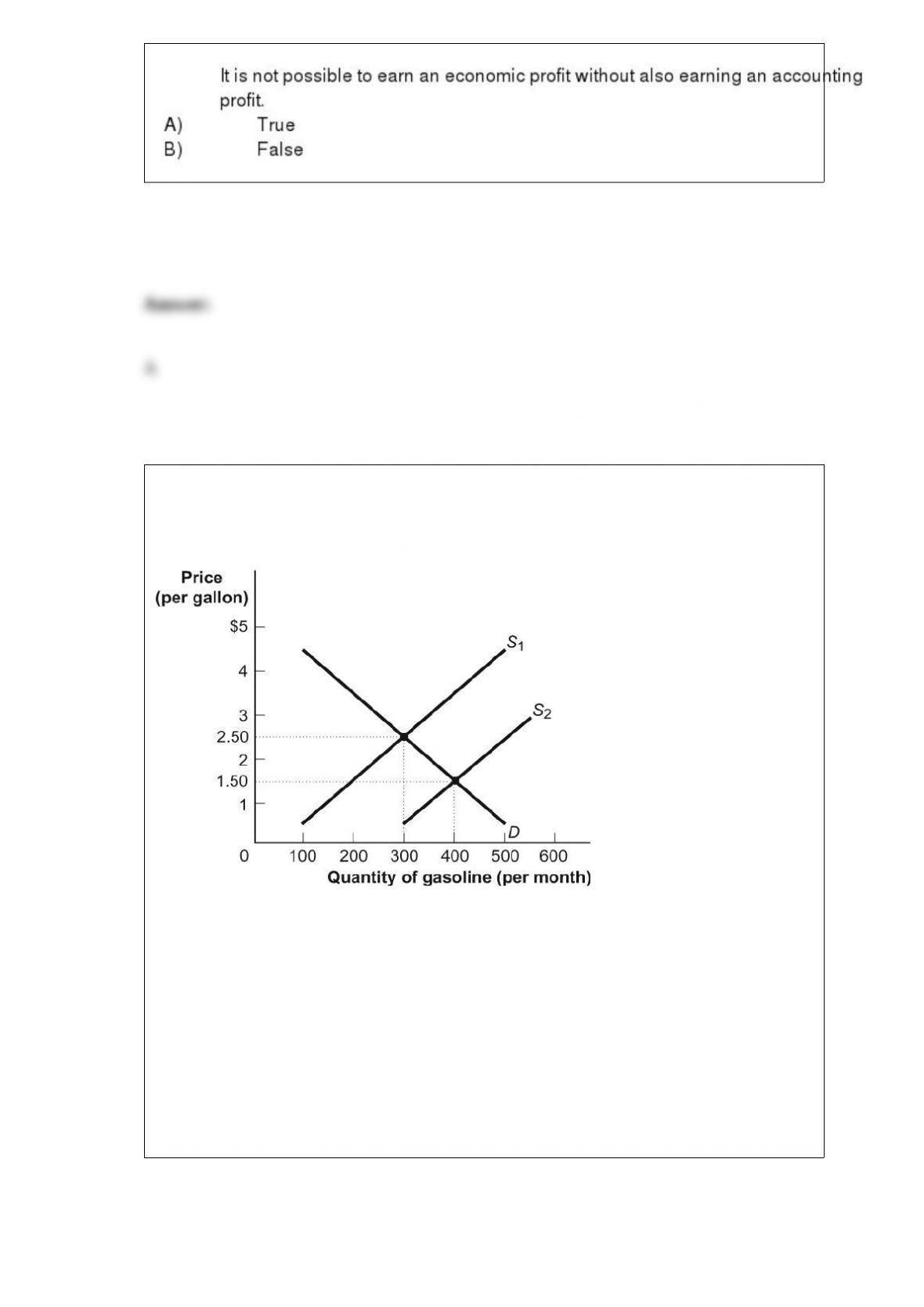

Figure: Demand and Supply of Gasoline

(Figure: Demand and Supply of Gasoline) Look at the figure Demand and Supply of

Gasoline. A factor that may have changed supply from S1 to S2 is:

A) better technology in the production of gasoline.

B) increased demand.

C) lower labor productivity in gasoline production.

D) increased prices of substitutes in production for gasoline.

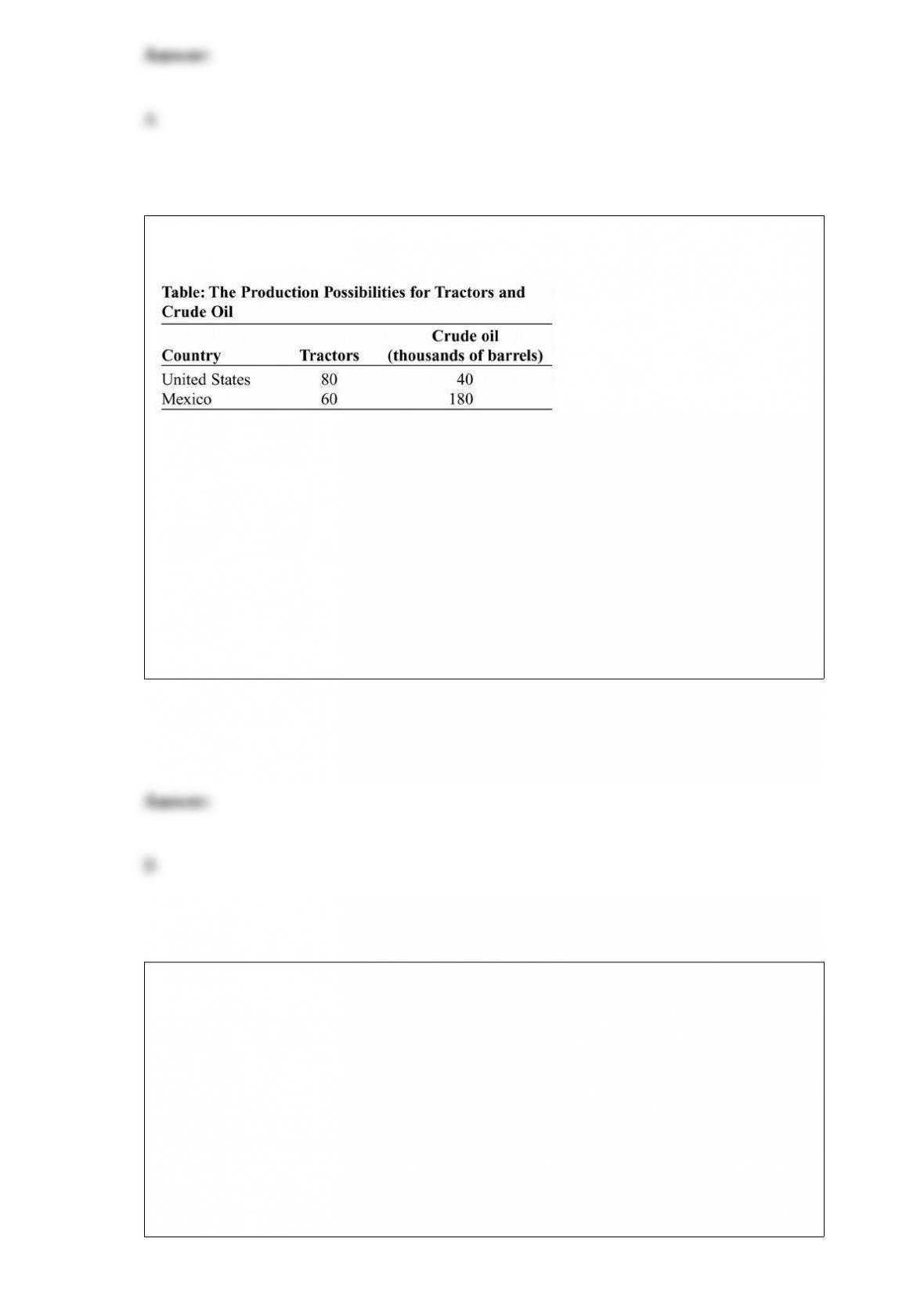

(Table: The Production Possibilities for Tractors and Crude Oil) Look at the table The

Production Possibilities for Tractors and Crude Oil. Which of the following is TRUE?

A) The opportunity cost of crude oil is lower in the United States than in Mexico.

B) The opportunity cost of crude oil is higher in the United States than in Mexico.

C) Crude oil costs are the same in the United States and in Mexico.

D) Tractor costs are the same in the United States and in Mexico.

If the opportunity cost of manufacturing machinery is higher in the United States than

in Britain and the opportunity cost of manufacturing sweaters is lower in the United

States than in Britain, then the United States will:

A) export both sweaters and machinery to Britain.

B) import both sweaters and machinery from Britain.

C) export sweaters to Britain and import machinery from Britain.

D) import sweaters from Britain and export machinery to Britain.

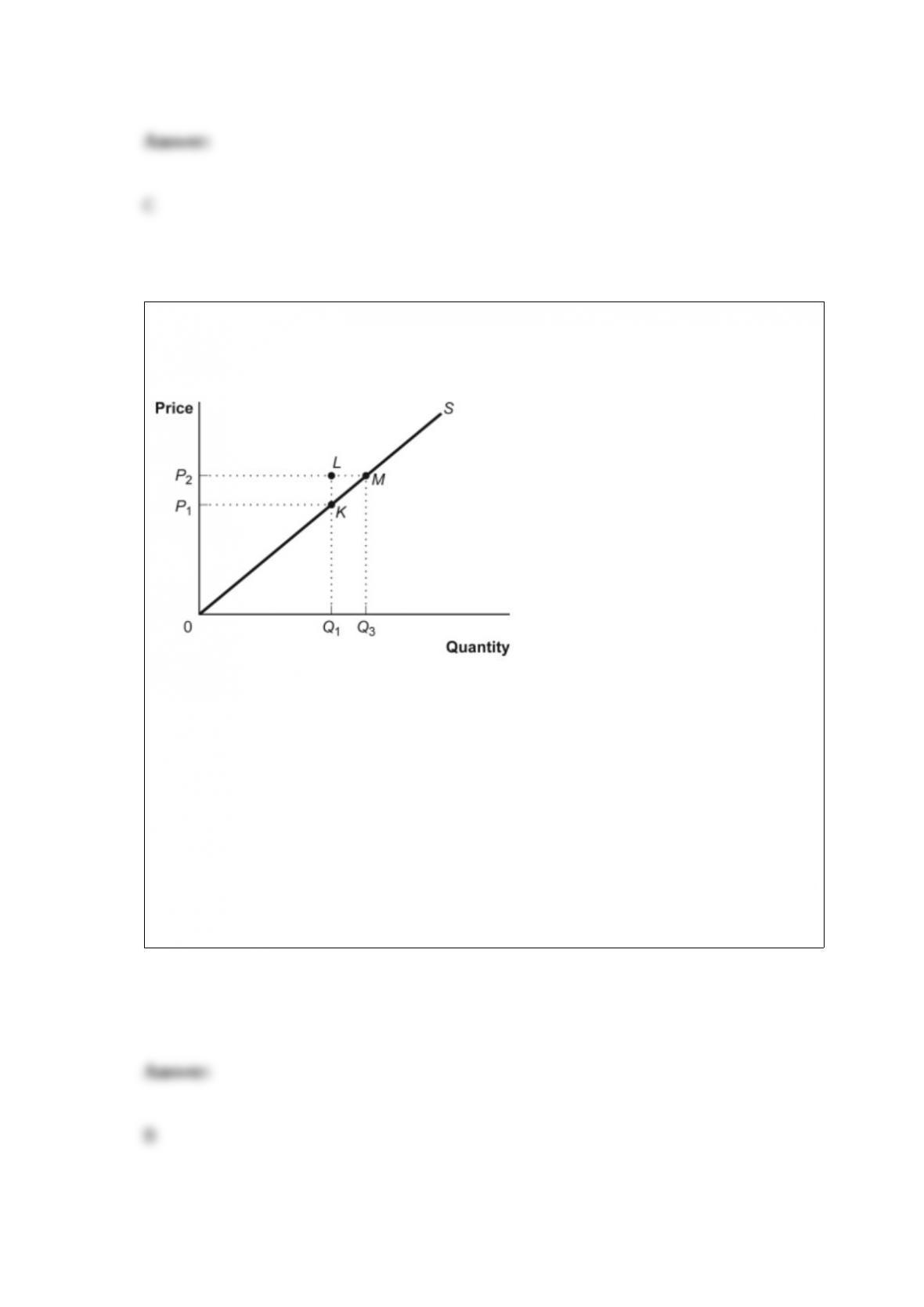

Figure: Producer Surplus II

(Figure: Producer Surplus II) Look at the figure Producer Surplus II. At a price of P1,

producer surplus equals the area:

A) LMK.

B) P1K0.

C) P2M0.

D) P2P1KM.

Which of the following is a systematic mistake that leads to irrational decisions?

A) risk aversion

B) bounded rationality

C) maximizing profit rather than minimizing costs

D) overconfidence

In the United States just after the turn of the twenty-first century, approximately _____

of total income in the economy took the form of compensation of employees.

A) 50%

B) 9%

C) 90%

D) 70%

A price ceiling below equilibrium will cause a larger shortage when demand is _____

and supply is _____.

A) elastic; inelastic

B) inelastic; inelastic

C) elastic; elastic

D) perfectly inelastic; elastic

Which of the following statements is TRUE?

A) Some very talented people have a comparative advantage in everything they do.

B) Some very untalented people have a comparative advantage in nothing they do.

C) Some very talented people have a very low opportunity cost in everything they do.

D) It is possible to have an absolute disadvantage but a comparative advantage in

something.

Scenario: A Small-Town Monopolist

A monopolist sells cable subscriptions in a small town and finds that it can sell 100

subscriptions when the price is $15 a week and an additional 75 subscriptions when the

price is $10 a week. The MC for the provision of the cable is $5 a week. There are no

fixed costs.

(Scenario: A Small-Town Monopolist) Look at the scenario A Small-Town Monopolist.

If the company is allowed to offer different prices for its good, what is the maximum

amount of profit this company can earn?

A) $1,000

B) $750

C) $1,375

D) $1,520

A plastics manufacturing plant dumps pollution into the Big River. This leads to higher

costs and disruption for fishermen on the river, for which they are not compensated. In

this situation:

A) too little of society’s resources is being used to produce plastic.

B) too much of society’s resources is being used to produce plastic.

C) the ideal amount of society’s resources is being used to produce plastic.

D) there is an external benefit to society from plastic production.

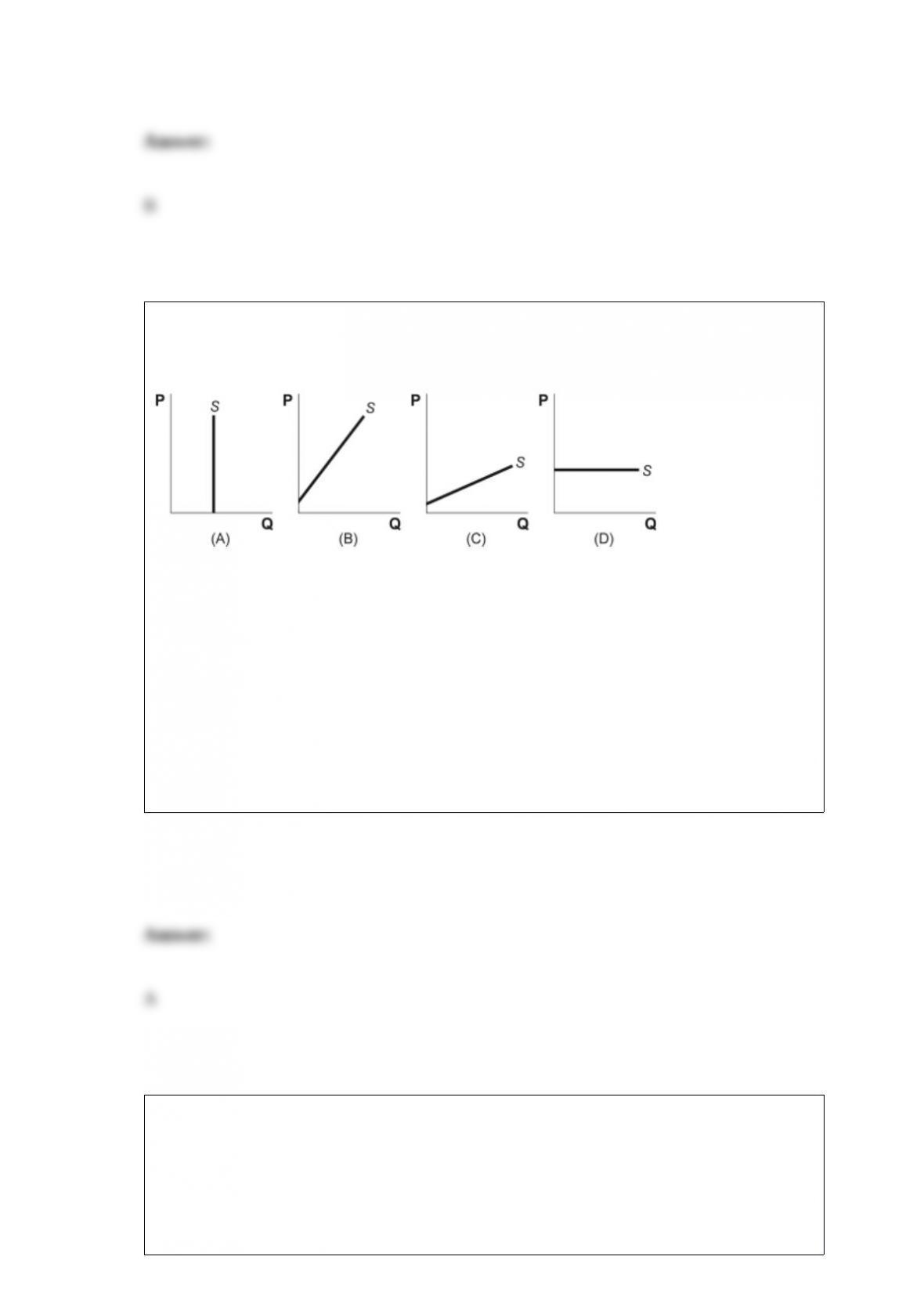

Figure: Supply Curves

(Figure: Supply Curves) Look at the figure Supply Curves. Which graph shows a

perfectly inelastic supply curve?

A) A

B) B

C) C

D) D

Since the terrorist attacks of September 11, 2001, the Federal Aviation Agency has

added a small security fee to every airplane ticket purchased. This is an example of:

A) the benefits principle of tax fairness.

B) a lump-sum tax.

C) the ability-to-pay principle of tax fairness.

D) a profits tax.

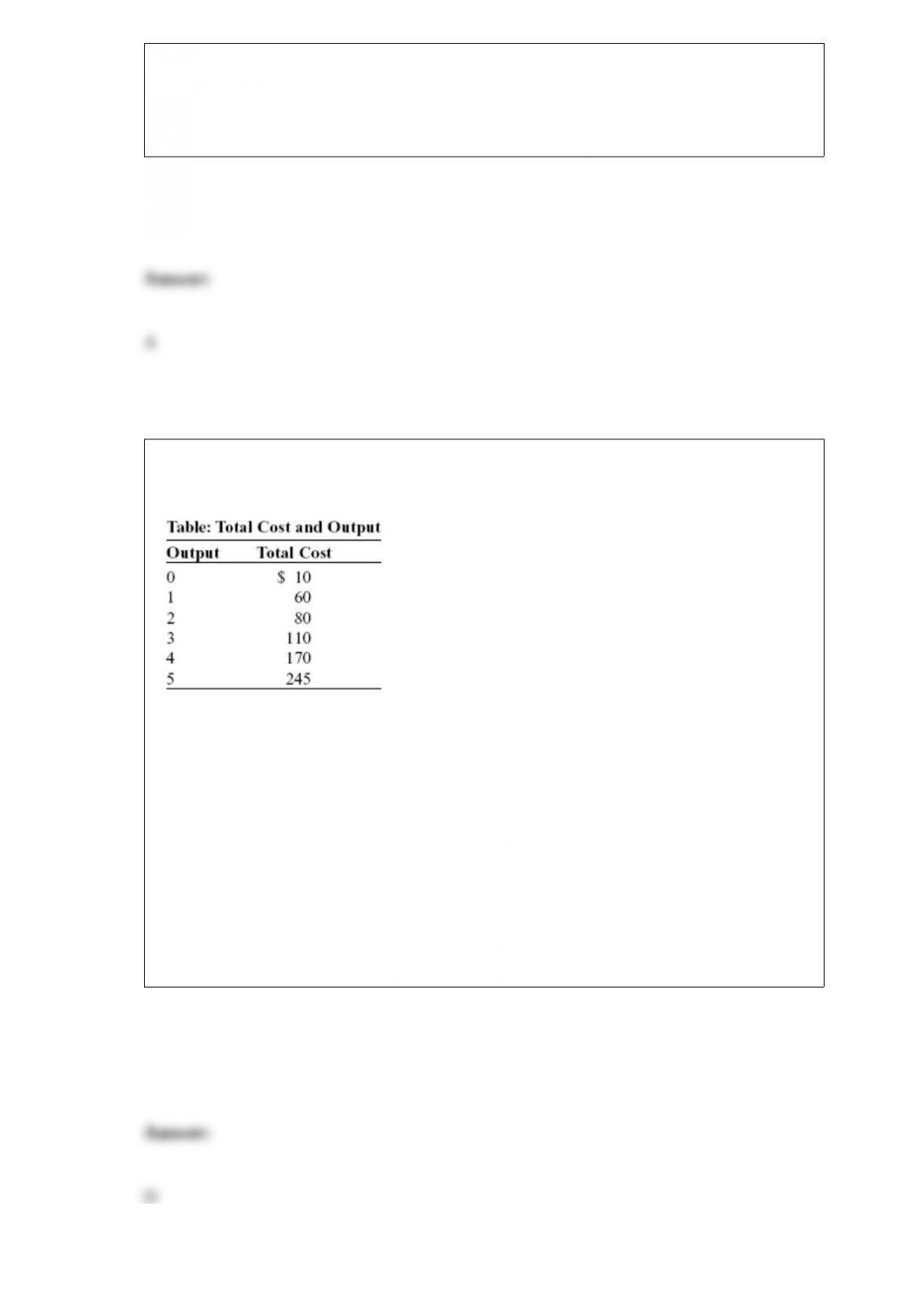

(Table: Total Cost and Output) Look at the table Total Cost and Output, which describes

Sergei’s costs for his perfectly competitive all-natural ice cream firm. If the market price

of a tub of ice cream is $67.50, how many tubs of ice cream will Sergei’s firm produce?

A) 1

B) 2

C) 3

D) 4

The licenses that can be bought and sold by polluters and that enable the holder to

pollute up to a specified amount during a given period are called:

A) emissions taxes.

B) Pigouvian taxes.

C) tradable emissions permits.

D) environmental standards.

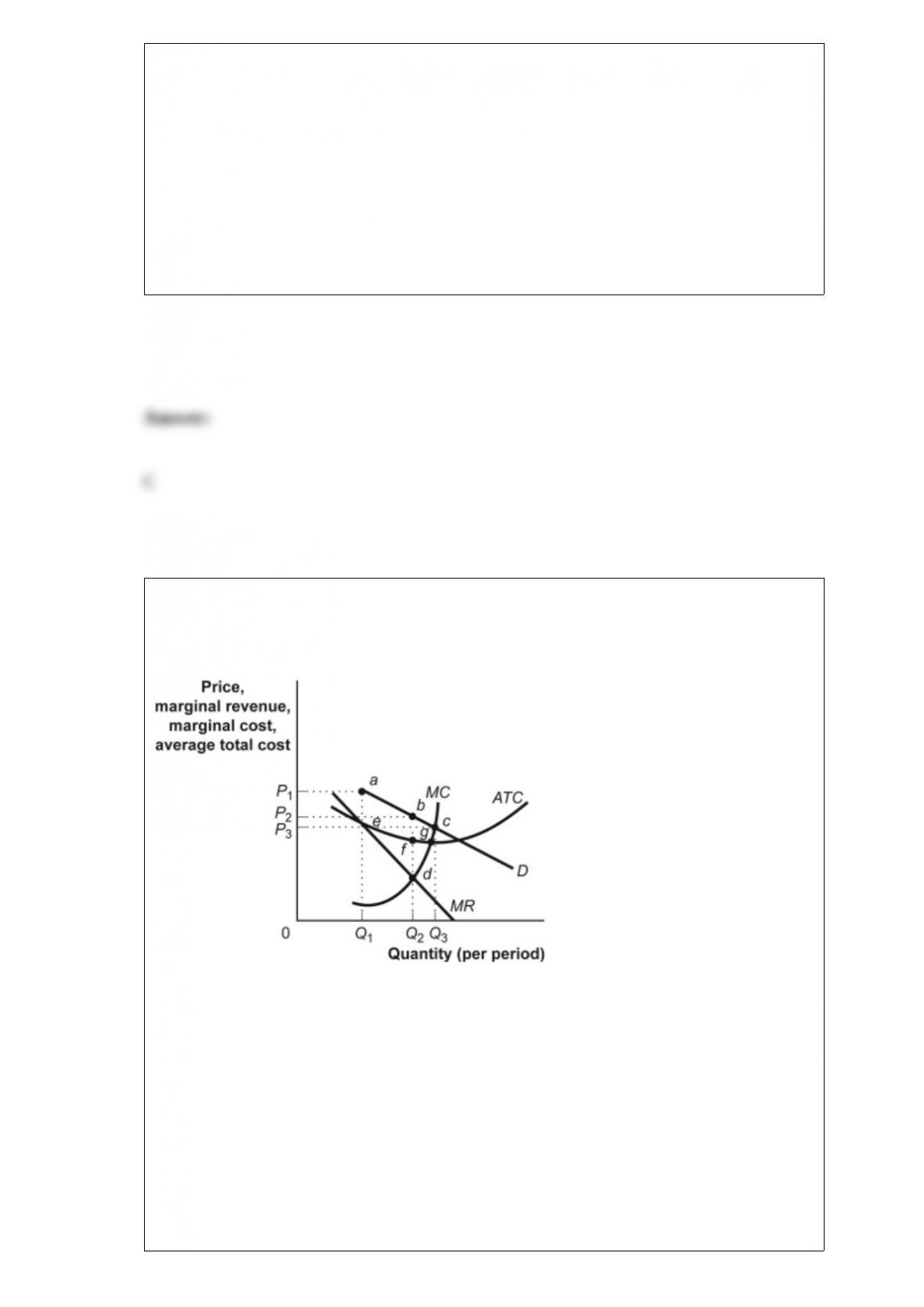

Figure: The Restaurant Market

(Figure: The Restaurant Market) The figure The Restaurant Market shows curves facing

a typical restaurant. Assume that many firms, differentiated products, and easy entry

and exit characterize the restaurant market. For the restaurant shown here, the profit per

unit is:

A) ae.

B) fd.

C) bf.

D) bd.

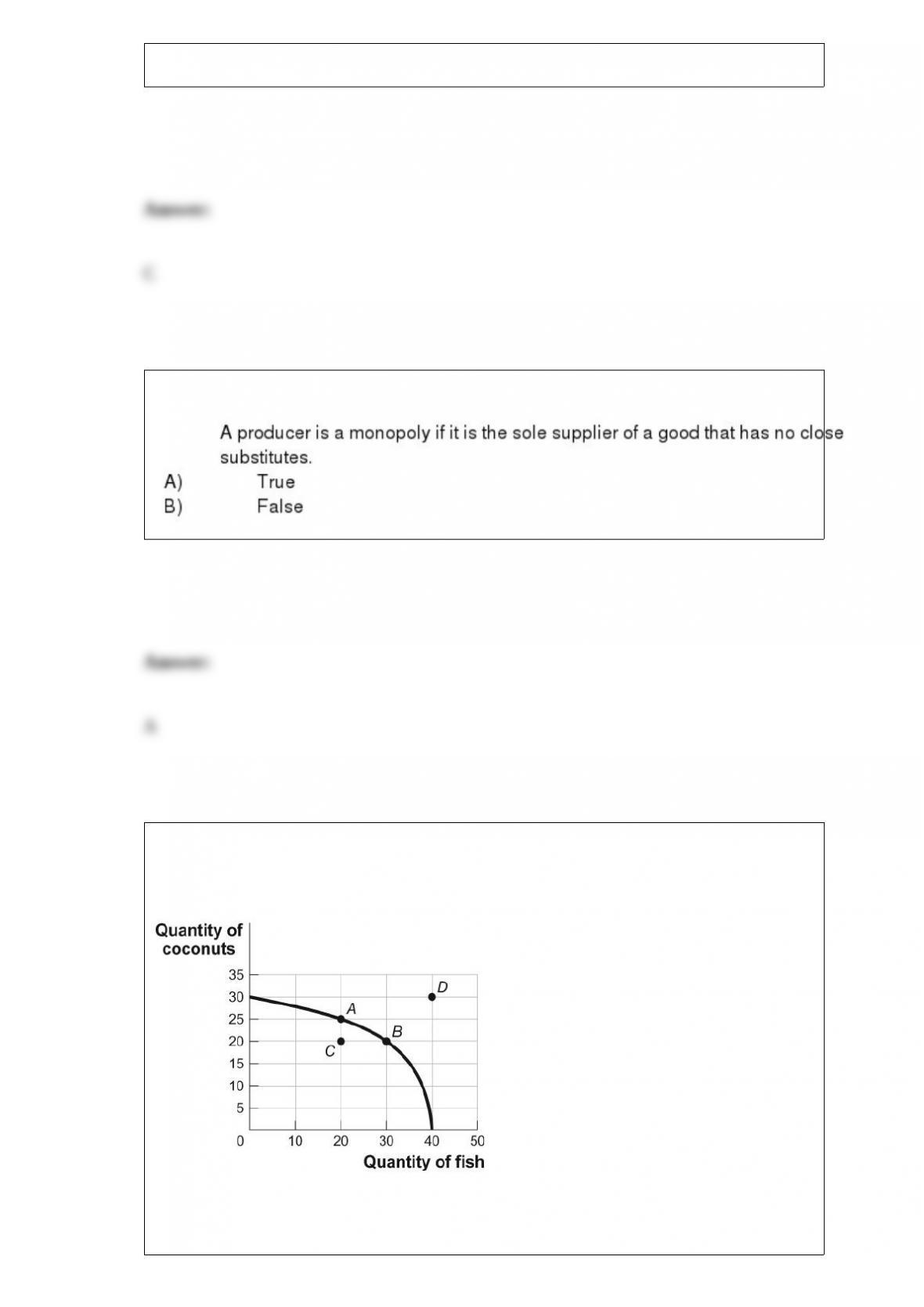

Figure: Tom’s Production Possibilities

(Figure: Tom’s Production Possibilities)

Look at the figure Tom’s Production Possibilities. Which point or points represent(s) a

feasible combination of coconuts and fish?

A) A only

B) A and B

C) A, B, and C

D) D only

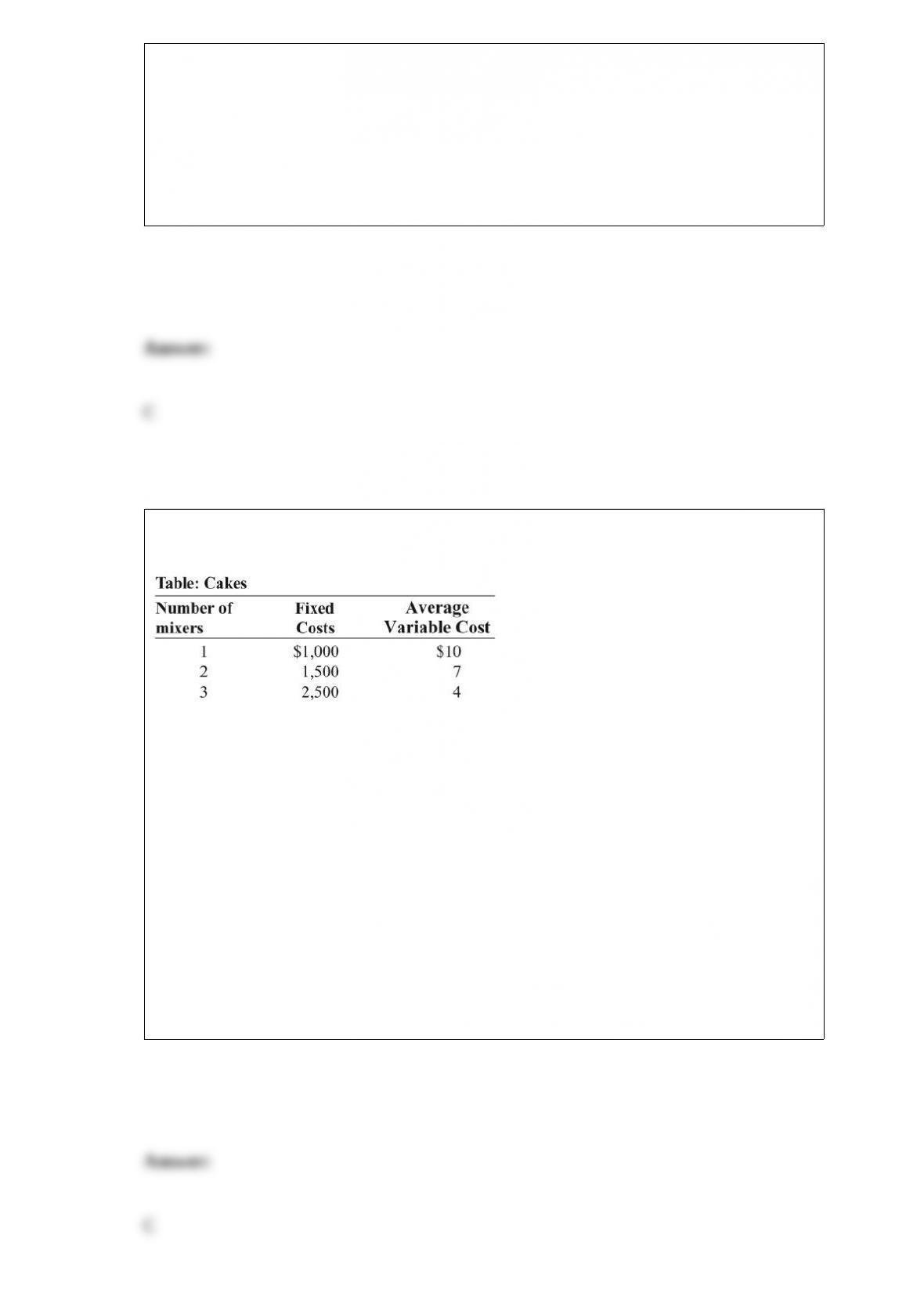

(Table: Cakes) Look at the table Cakes. Pat is opening a bakery to make and sell special

birthday cakes. She is trying to decide how many mixers to purchase. Her estimated

fixed and average variable costs if she purchases one, two, or three mixers are shown in

the table. Assume that average variable costs do not vary with the quantity of output. If

Pat purchases two mixers and bakes 100 cakes per day, what is her average fixed cost?

A) $10,000

B) $1,000

C) $15

D) $10

When a firm adds physical capital, in the short run fixed costs will:

A) increase.

B) decrease.

C) remain the same.

D) decrease at first and then increase.

Table: Utility from Oranges and Star Fruit Pounds of Oranges Total Utility from

Oranges Pounds of Star Fruit Total Utility 0 0 0 0 1 24 1 70 2 44 2 130 3 60 3 180 4

72 4 220 5 80 5 250 6 84 6 270 7 84 7 280

(Table: Utility from Oranges and Star Fruit) Look at the table Utility from Oranges and

Star Fruit. Oranges cost $2 per pound and star fruit costs $5 per pound. Calvin has $26

to spend. If Calvin buys 2 pounds of star fruit, how many pounds of oranges can he

buy?

Pounds of Oranges Total Utility from Oranges Pounds of Star Fruit Total Utility

0 0 0 0

1 24 1 70

2 44 2 130

3 60 3 180

4 72 4 220

5 80 5 250

6 84 6 270

7 84 7 280

A) 6

B) 7

C) 8

D) 9

Suppose that the market for candy canes operates under conditions of perfect

competition, that it is initially in long-run equilibrium, that the price of each candy cane

is $0.10, and that the market demand curve is downward-sloping. The price of sugar

rises, increasing the marginal and average total cost of producing candy canes by $0.05;

there are no other changes in production costs. In the long run we will observe:

A) firms leaving the industry.

B) firms entering the industry.

C) some firms entering and some firms leaving.

D) neither entry to nor exit from the industry.

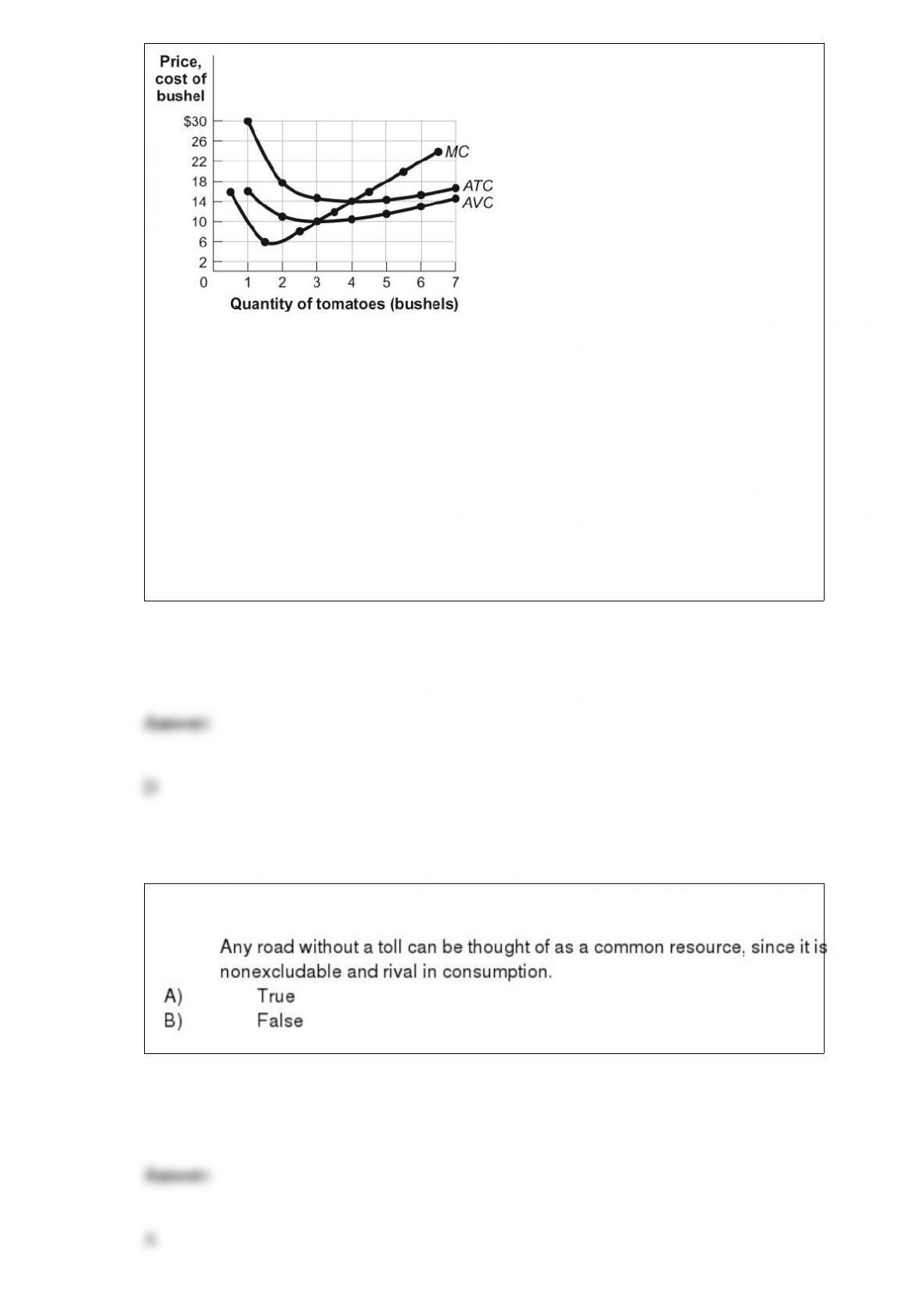

Figure: Revenues, Costs, and Profits for Tomato Producers III

(Figure: Revenues, Costs, and Profits for Tomato Producers III) Look at the figure

Revenues, Costs, and Profits for Tomato Producers III. The market for tomatoes is

perfectly competitive. If the market price of a bushel of tomatoes is $18, this farm will:

A) minimize its losses by shutting down.

B) minimize its losses by continuing to produce.

C) break even.

D) earn an economic profit.

Assume that the United States imposes an import quota on Scottish wool suits. Relative

to the equilibrium price that would prevail in the absence of quotas, the equilibrium

price of suits in the United States will most likely _____ and the equilibrium price of

suits in Scotland will most likely _____.

A) remain the same; decrease

B) remain the same; increase

C) increase; increase

D) increase; decrease