1) the production possibilities curve shows:

a.the various combinations of two goods that can be produced when society employs all

of its scarce resources.

b.the minimum outputs of two goods that will sustain a society.

c.the various combinations of two goods that can be produced when some resources are

unemployed.

d.the ideal, but unattainable, combinations of two goods that would maximize consumer

satisfactions.

2) when a pure monopolist is producing its profit -maximizing output, price will:

a.be less than mr

b.equal neither mc nor mr

c.equal mr

d.equal mc

3) Which of the following best describes the main problem faced by farms in the long

run?

A.Lagging technology has decreased the productivity of farmers and therefore resulted

in low farm prices and incomes.

B.The highly inelastic nature of agricultural demand has caused small year-to-year

fluctuations in farm output to result in highly unstable farm incomes.

C.The supply of farm products has increased relative to the demand for them, and,

because demand is inelastic, farm prices and incomes have therefore declined.

D.The demand for farm products has increased relative to their supply, but the highly

elastic nature of agricultural demand has caused these shifts to result in declining farm

incomes.

4) the annual growth of u.s. labor productivity:

a.was greater between 1973 and 1995 than between 1995 and 2007.

b.was greater between 1995 and 2007 than between 1973 and 1995.

c.was negative in the late 1990s.

d.averaged nearly 5 percent in the 1990s.

5) marginal product is:

a.the increase in total output attributable to the employment of one more worker.

b.the increase in total revenue attributable to the employment of one more worker.

c.the increase in total cost attributable to the employment of one more worker.

d.total product divided by the number of workers employed.

6) during periods of full employment the:

a.burden of unemployment is quite evenly distributed among males and females,

african-americans and whites, and young and old workers.

b.unemployment rate for teenagers is below the rate for the labor force as a whole.

c.unemployment rate for women is considerably lower than that for men.

d.unemployment rate for african-americans is about twice the rate for whites.

7) A public good:

A.can be profitably produced by private firms.

B.is characterized by rivalry and excludability.

C.produces no positive or negative externalities.

D.is available to all and cannot be denied to anyone.

8) In the United States:

A.taxes decrease, but transfers increase, income inequality.

B.taxes increase, but transfers reduce, income inequality.

C.both taxes and transfers decrease income inequality.

D.both taxes and transfers increase income inequality.

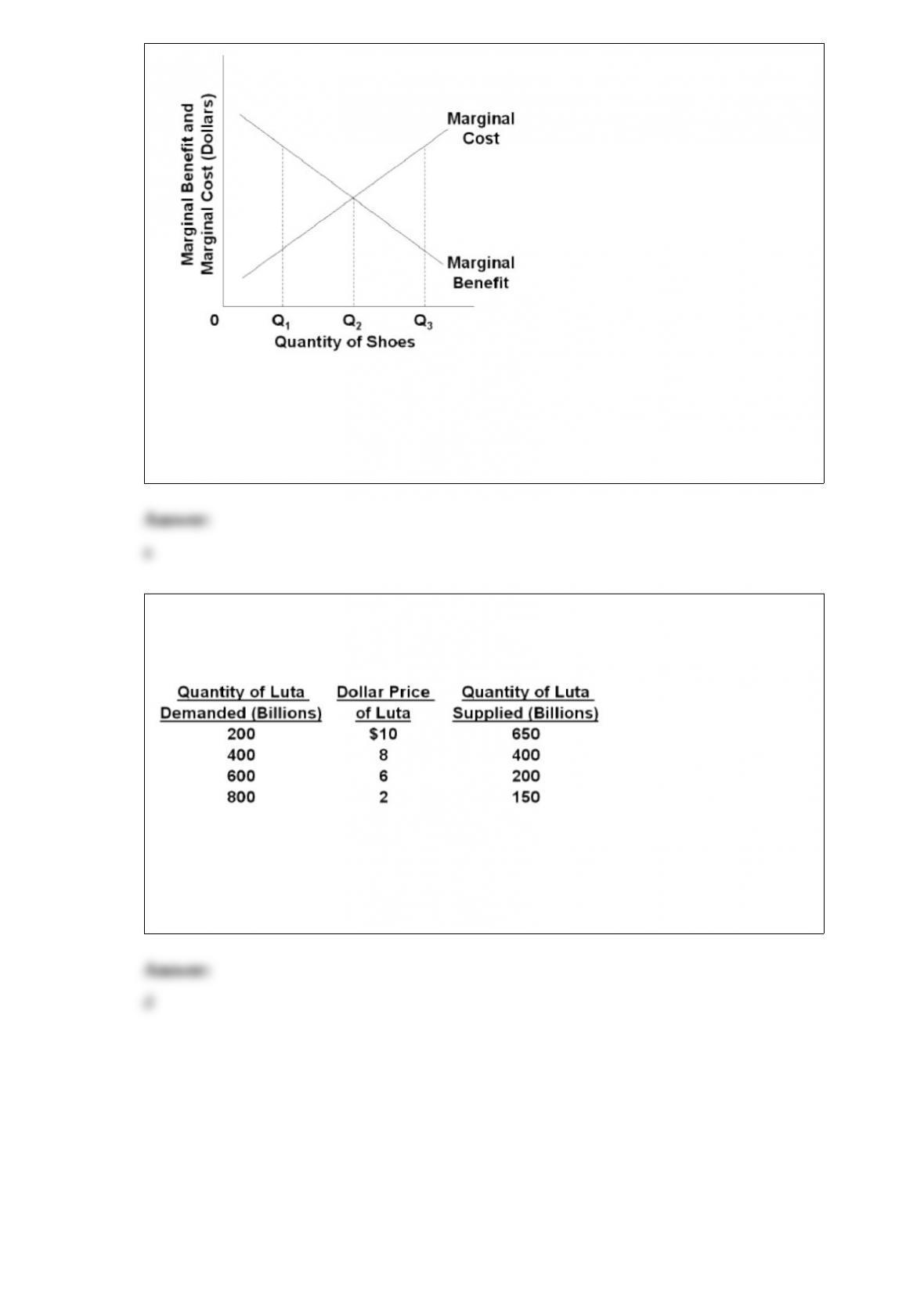

9)

refer to the above diagram for athletic shoes. if the current output of shoes is q3, then:

a.society should produce fewer shoes to achieve the optimal allocation of resources.

b.society should produce more shoes to achieve the optimal allocation of resources.

c.resources are being allocated efficiently to the production of shoes.

d.shoes are more valuable to society than alternative products

10) the following table which indicates the dollar price of luta, the currency used in the

hypothetical economy of luteland:

refer to the above table. the exchange rate in this market is:

a.8 luta for one dollar.

b.0.60 luta for one dollar.

c.6 luta for one dollar.

d.0.125 luta for one dollar.