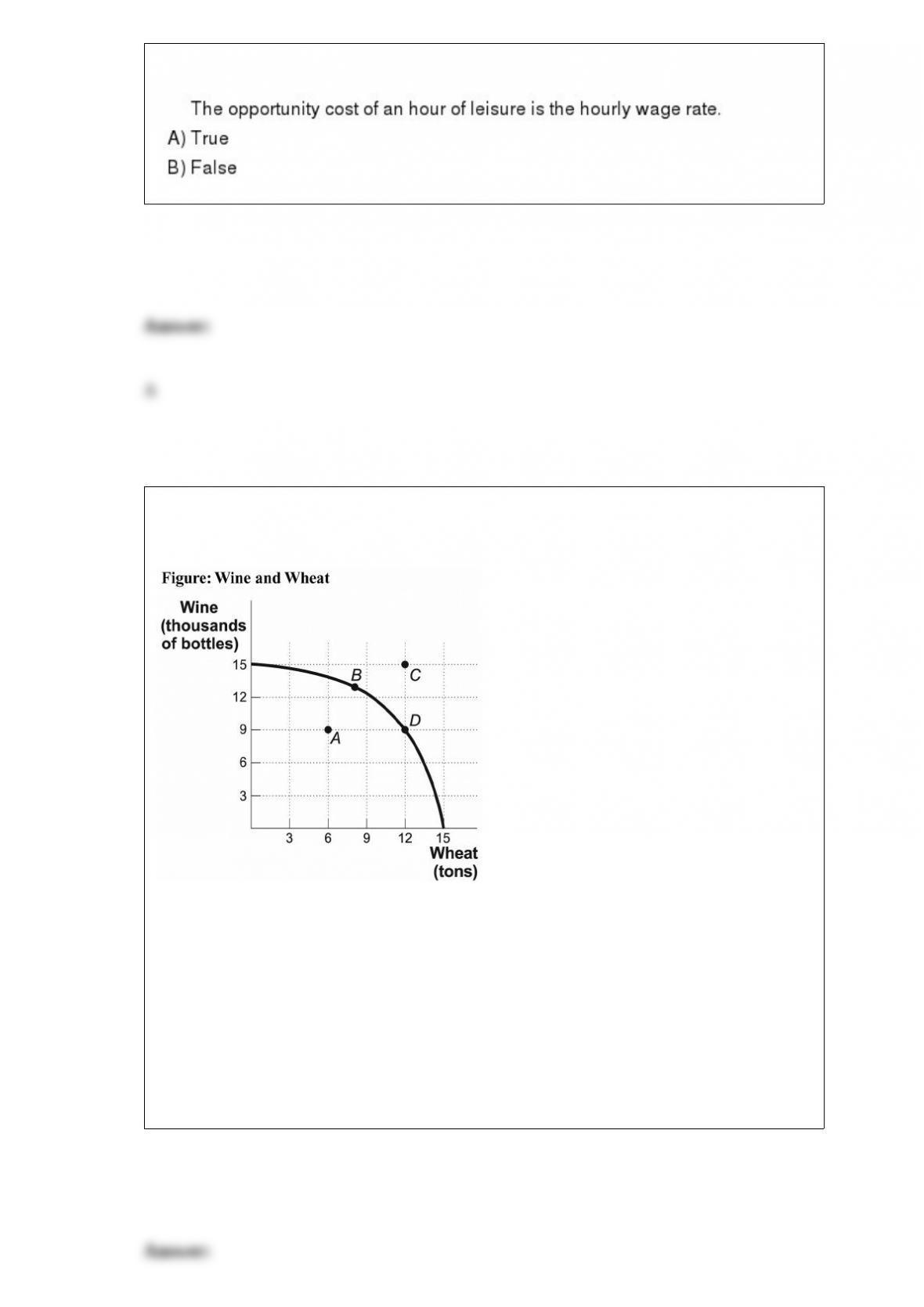

(Figure: Wine and Wheat) Look at the

figure Wine and Wheat. The opportunity cost of moving from producing ONLY wheat

to producing at point D is _____ tons of wheat.

A) 3

B) 6

C) 9

D) 15

When some people know things that other people don’t know, there is _____; it can

_____ economic decisions.

A) risk aversion; facilitate

B) blind strategy; delay

C) private information; distort

D) blind trust; diversify

The marginal revenue received by a firm in a perfectly competitive market:

A) is unrelated to the market price.

B) is less than the market price.

C) is greater than the market price.

D) is the change in total revenue divided by the change in output.

Smedley, a careful utility maximizer, consumes peanut butter and ice cream. Assume

that both peanut butter and ice cream are normal goods. He had just achieved the

utility-maximizing solution in his consumption of the two goods when the price of ice

cream increased. As he adjusted to this event, he consumed _____ peanut butter and

_____ ice cream.

A) more; more

B) less; less

C) more; less

D) less; more

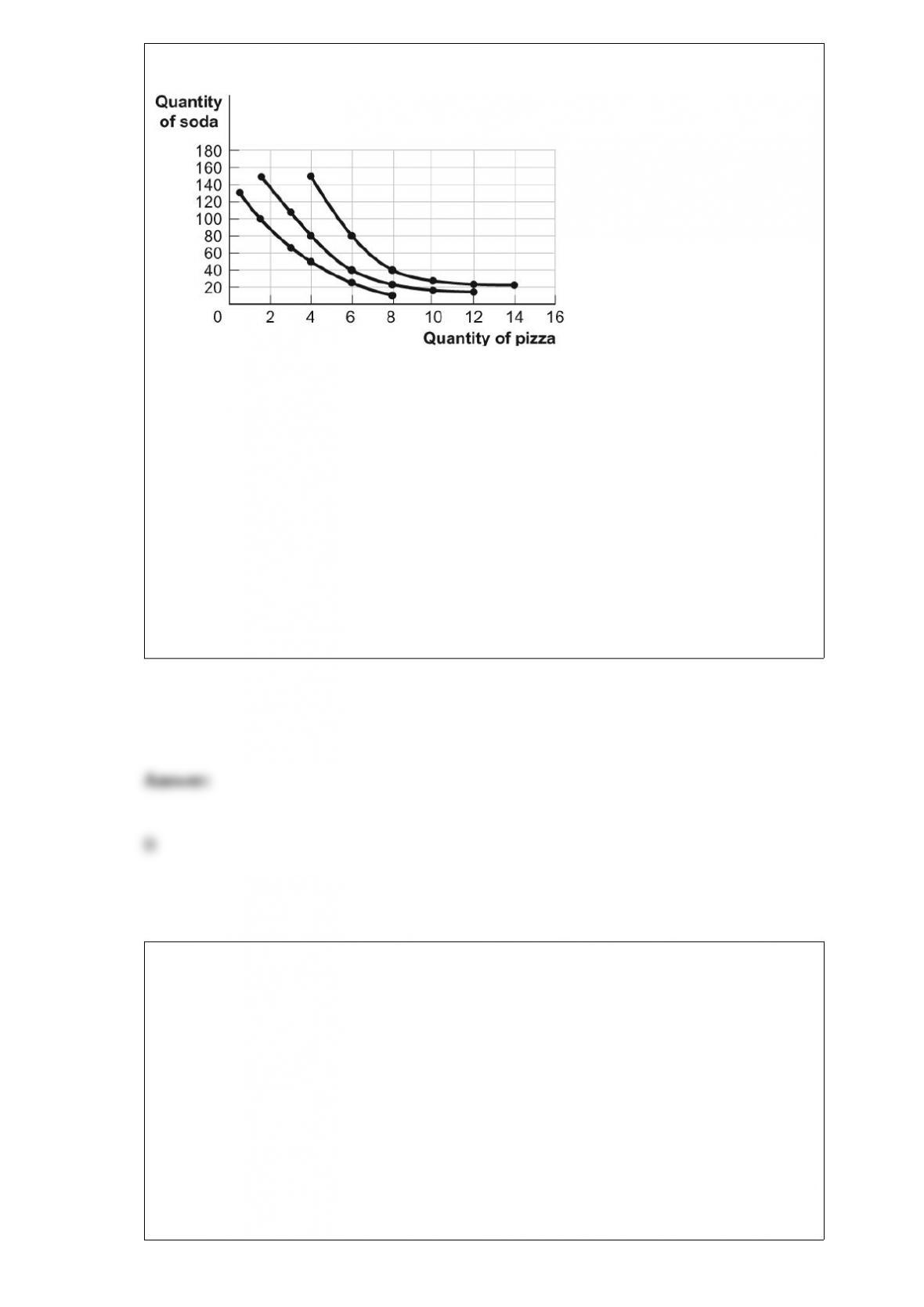

Figure: Consumer Equilibrium I The figure shows three of Owen’s indifference

curves for pizza and soda per week. Owen has $180 per month to spend on the two

goods. The price of a pizza is $20, and the price of a soda is $1.50.

(Figure: Consumer Equilibrium I) Look at the figure Consumer Equilibrium I. If Owen

consumes 1.5 pizzas and 100 sodas, which of the following describes the relationship

between his marginal rate of substitution of pizza for soda and the price of pizza in

terms of soda?

A) The marginal rate of substitution equals the relative price.

B) The marginal rate of substitution is greater than the relative price.

C) The marginal rate of substitution is less than the relative price.

D) It is impossible to determine, given the information available.

If the several companies in the tobacco industry produce similar products but have very

different marginal costs:

A) they are less likely to engage in tacit collusion than firms with similar costs.

B) they are more likely to engage in tacit collusion than firms with similar costs.

C) prices for tobacco products are more likely to be near the monopoly level than in an

industry whose firms have similar costs.

D) output of tobacco products is more likely to be near the monopoly level than in an

industry whose firms have similar costs.

The models used in economics:

A) are always limited to variables that are directly related.

B) are essentially not reliable because they are not testable in the real world.

C) are of necessity unrealistic and not related to the real world.

D) emphasize basic relationships by abstracting from complexities in the everyday

world.

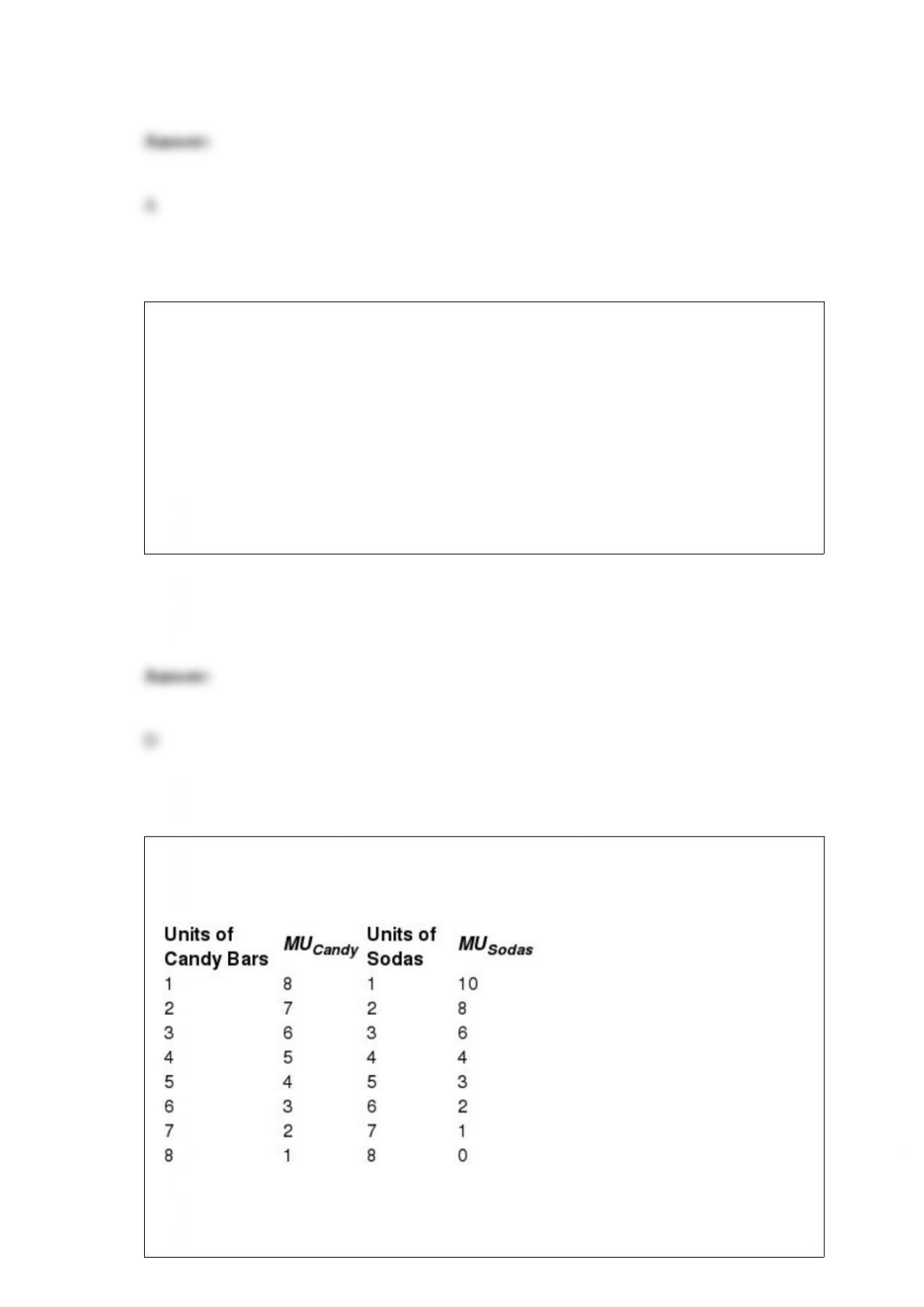

Table: Utility from Candy Bars and Sodas

(Table: Utility from Candy Bars and Sodas) Look at the table Utility from Candy Bars

and Sodas. If Stan consumes two candy bars and two sodas, his total utility will be

_____ utils.

A) 15

B) 33

C) 18

D) 78

A newspaper typically consumes a smaller fraction of a consumer’s budget than a home

entertainment system. Therefore, you would expect the demand for:

A) a home entertainment system to be more price-elastic.

B) a home entertainment system to be more price-inelastic.

C) newspapers to be more price-elastic.

D) the two to be equally price-elastic.

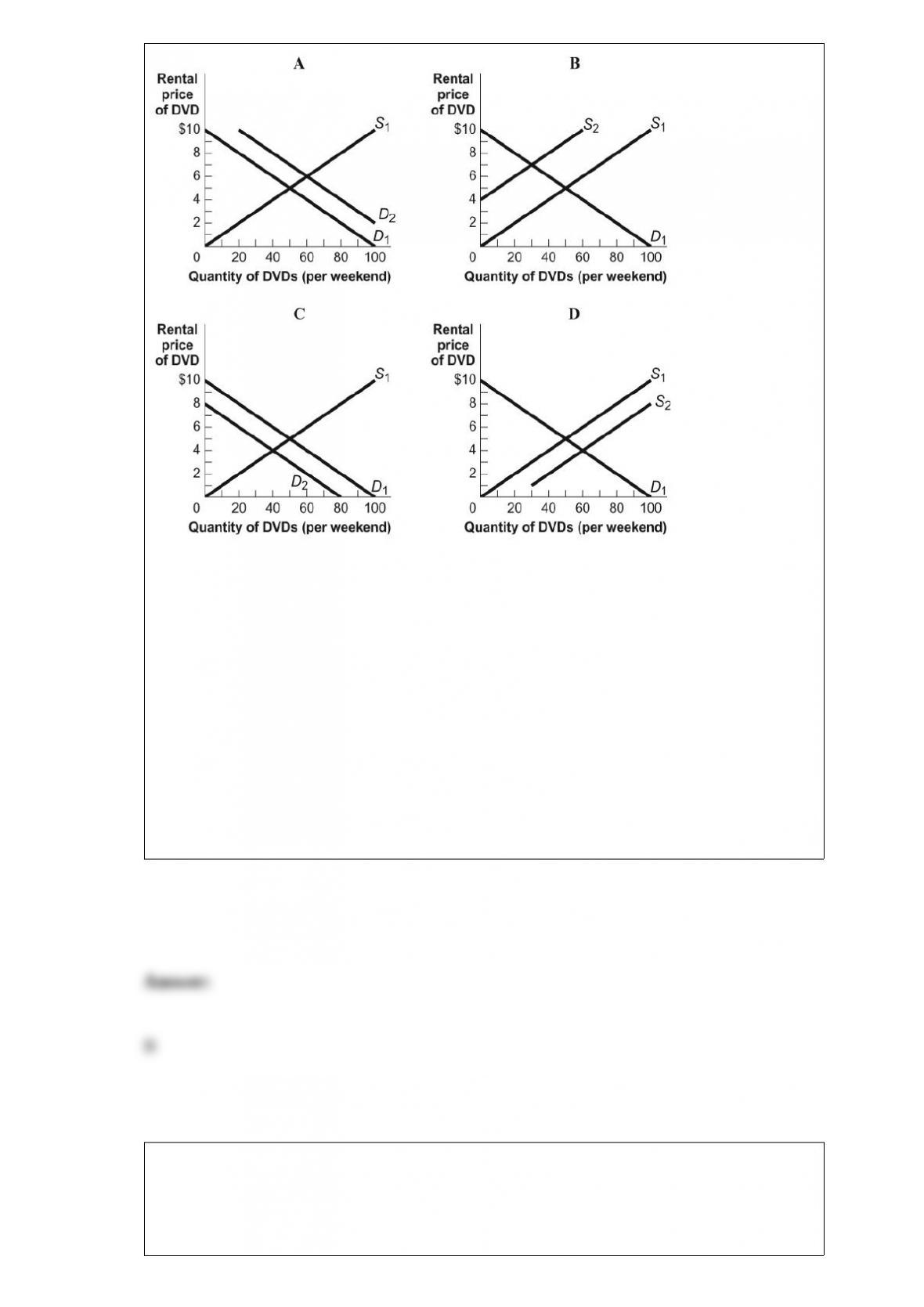

Figure: Four Markets for DVDs

(Figure: Four Markets for DVDs) Look at the figure Four Markets for DVDs. Which of

the graphs shows what may happen in the market for DVDs if D1 or S1 is the original

curve and D2 or S2 is the new curve and if the cost of producing DVD players

increases?

A) A

B) B

C) C

D) D

For a normal demand curve, the price elasticity of demand will be:

A) always positive.

B) always greater than 1.

C) usually equal to 1.

D) always negative.

In the short run, a perfectly competitive firm produces output and breaks even if the

firm produces the quantity at which:

A) P < ATC.

B) P = ATC.

C) P > ATC.

D) P = (TR / Q + TC / Q) × Q.

To say that you can’t have too much of a good thing means that for any good that you

enjoy (for example, pizza):

A) higher consumption will always lead to higher utility.

B) higher consumption will cause utility to decrease at an increasing rate.

C) higher consumption will increase utility, but only up to a point; after that utility will

start to decrease.

D) it is valid to measure utility in utils.

If the marginal social benefit received from pollution is less than its marginal social

cost:

A) society’s well-being can be improved if the quantity of pollution increases.

B) society’s well-being can be improved if the quantity of pollution decreases.

C) society has achieved its socially optimal level of pollution.

D) the market is producing too little pollution.

Although most citizens have access to police protection, they also take measures, such

as putting locks on their doors, to protect themselves. For most citizens police

protection is a(n) _____ good, while self-protection is a(n) _____ good.

A) public; private

B) public; artificially scarce good

C) common resource; private

D) artificially scarce good; common resource

The demand for a good will increase if:

A) there is a decrease in the price of the good.

B) the price of inputs needed in the production of the good decrease.

C) there is an increase in the number of consumers in this market.

D) the price of a complementary good increases.

An emissions tax will:

A) ensure that the marginal benefit of pollution is equal for all sources of pollution.

B) set standards to which all producers must adhere regardless of their production costs.

C) cause all polluters to reduce emissions by the same amount.

D) increase pollution, but not in the most efficient cost-saving way.

Mary goes ahead and buys a new car because she expects to receive a 10% increase in

her salary next year. What type of behavior does this best represent?

A) status quo bias

B) overconfidence

C) misperception of opportunity costs

D) risk aversion

The marginal cost curve intersects the average variable cost curve at:

A) its lowest point.

B) its maximum.

C) its end point.

D) no point; the curves don’t intersect.

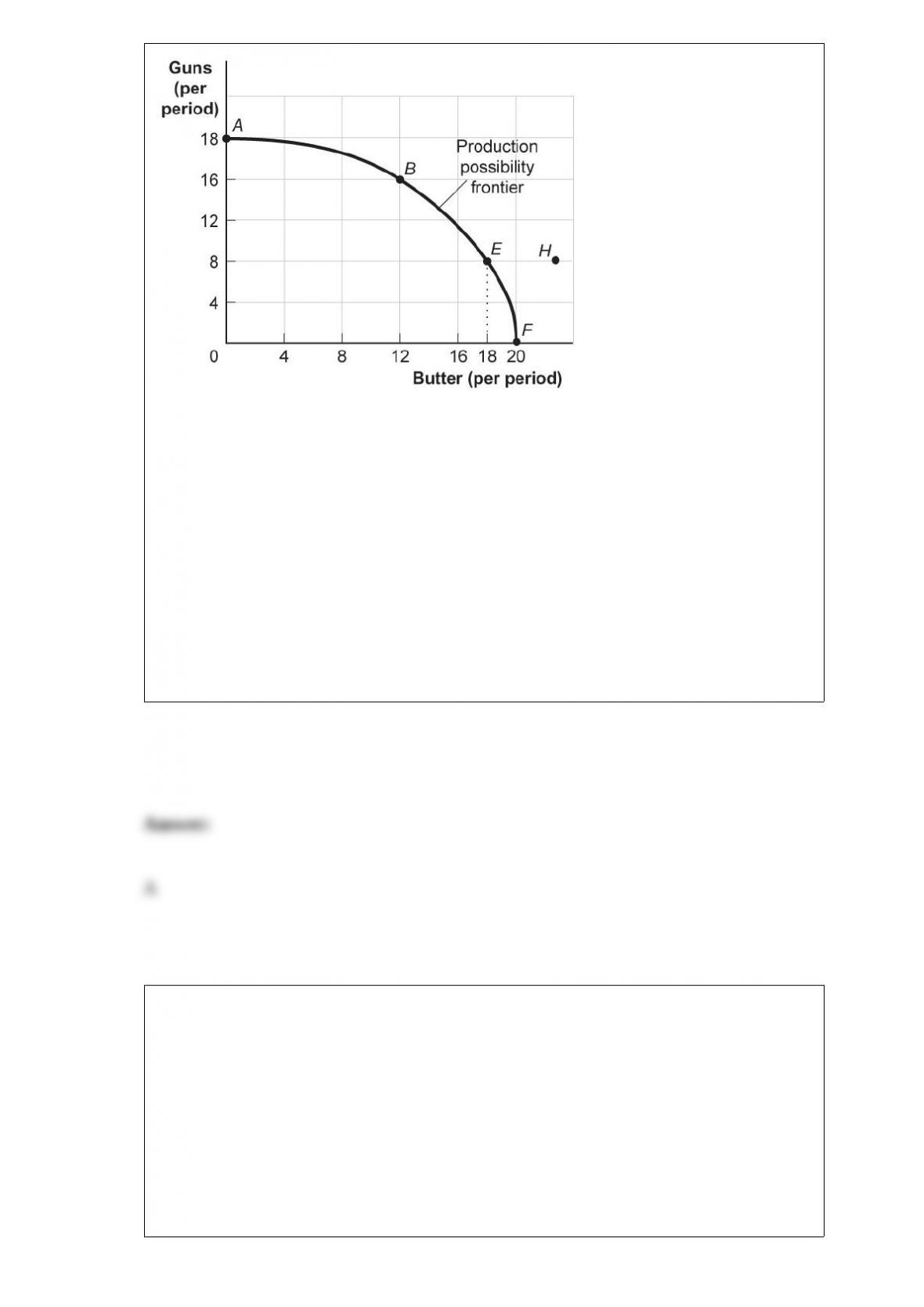

Figure: Guns and Butter

(Figure: Guns and Butter) Look at the figure Guns and Butter. On this figure, points A,

B, E, and F:

A) indicate combinations of guns and butter that society can produce using all of its

factors efficiently.

B) indicate increasing opportunity costs for guns but decreasing opportunity costs for

butter.

C) indicate that society wants butter more than it wants guns.

D) indicate constant opportunity costs for guns and increasing costs for butter.

Which of the following is TRUE if the insurance market is efficient?

A) The deductibles eliminate moral hazard.

B) Society as a whole engages in less risky behavior.

C) It transfers risk from those who most want to get rid of it to those least bothered by

the risk.

D) Premiums are always kept to the level of a fair insurance policy.

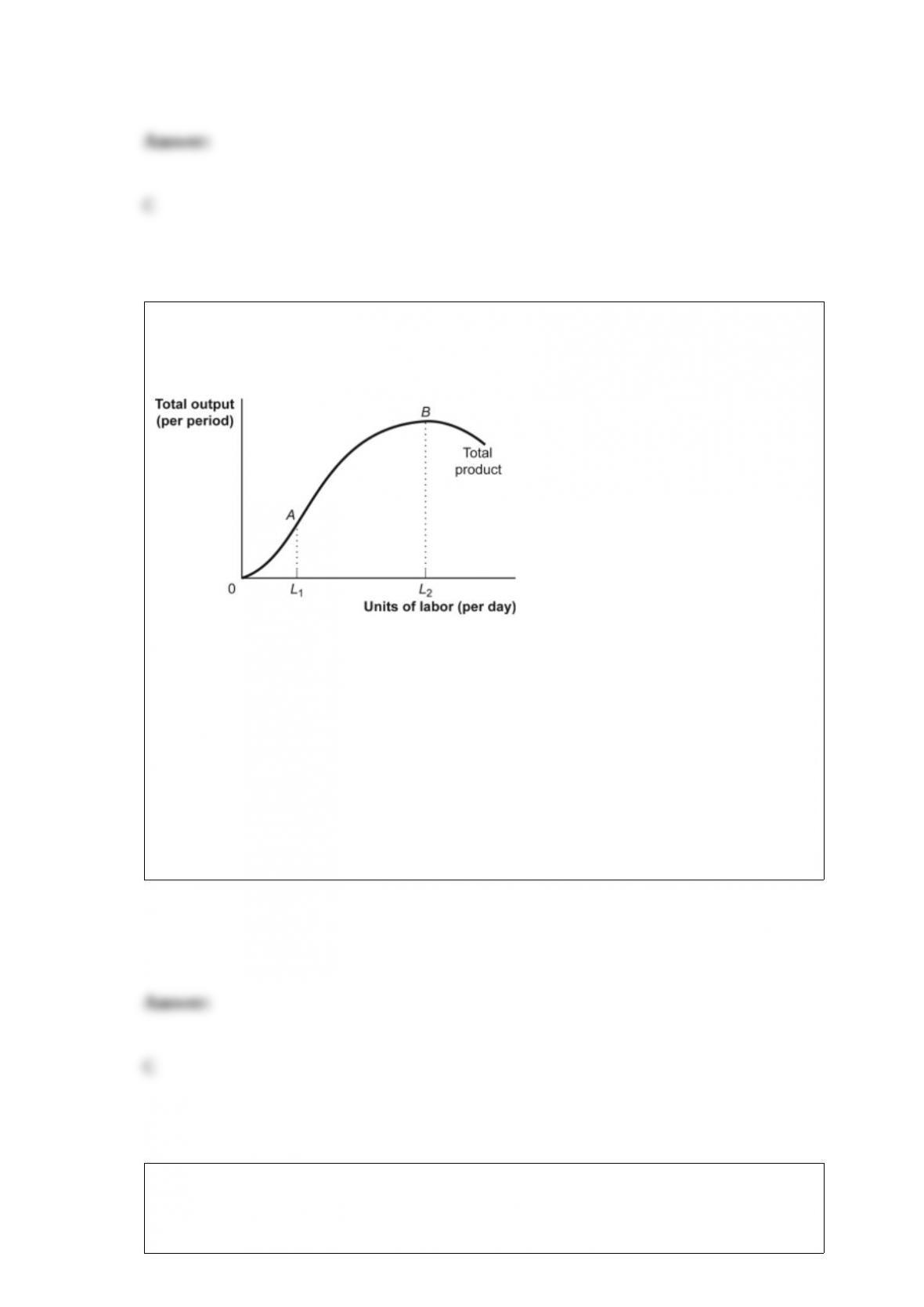

Figure: The Total Product

(Figure: The Total Product) Look at the figure The Total Product. Between points A and

B the marginal product of labor is:

A) increasing.

B) zero.

C) falling.

D) infinite.

A choice made _____ is a choice whether to do a little more or a little less of

something.

A) at the front end

B) in the beginning

C) at the margin

D) ceteris paribus

Pigouvian taxes:

A) tax the profits of polluting firms.

B) are designed to reduce external costs.

C) are essentially the same as emissions standards.

D) are tradable emissions permits.

If the price of chocolate-covered peanuts decreases from $1.15 to $1.05 and the

quantity demanded increases from 190 bags to 220 bags, then the price elasticity of

demand (by the midpoint method) is:

A) 0.5.

B) 1.

C) 2.

D) greater than 1.

A factor of production whose quantity CANNOT be changed during the short run is

a(n) _____ factor of production.

A) marginal

B) fixed

C) incremental

D) variable

In the short run, the price elasticity of supply for foods low in carbohydrates is lower

than it will be in the long run because:

A) in the short run, inputs are more available to produce these foods than in the long

run.

B) in the short run, food producers do not have much time to respond to changes in

demand.

C) in the short run, prices tend to stay constant.

D) in the long run, the price elasticity of supply tends to be perfectly inelastic.

All points outside the production possibility frontier are:

A) efficient.

B) inefficient.

C) infeasible.

D) economic growth.

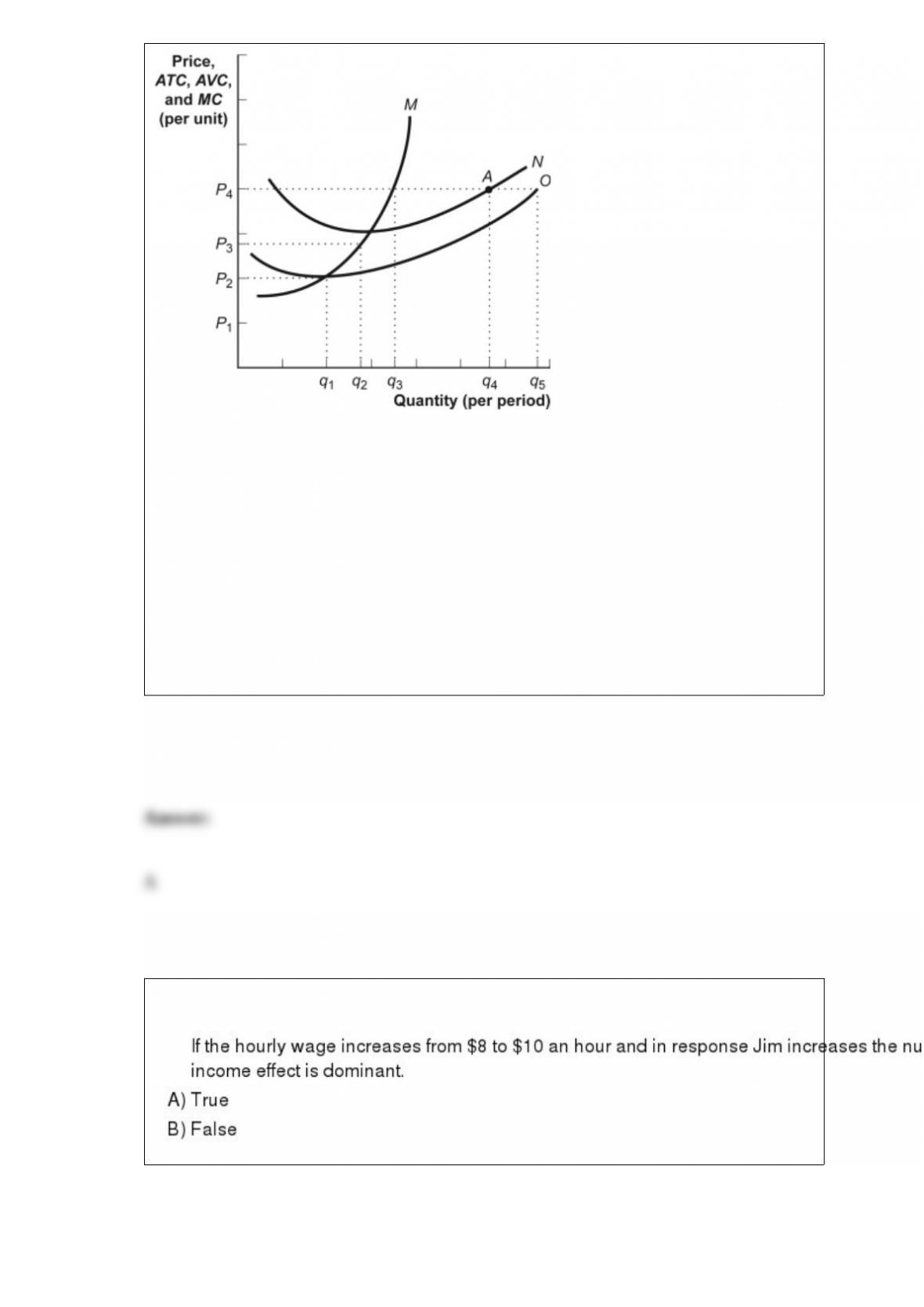

Figure: The Profit-Maximizing Firm in the Short Run

(Figure: The Profit-Maximizing Firm in the Short Run) Look at the figure The

Profit-Maximizing Firm in the Short Run. If the market price is P4, marginal revenue:

A) and price are the same.

B) is less than P4.

C) is greater than P4.

D) and price are unrelated.