A switch to marketable pollution permits will decrease abatement costs because

high-cost firms do most of the abating.

A contestable market is one where there are few if any barriers to entry.

Monopolistic competition is characterized by barriers to entry.

Symmetric information occurs when both buyers and sellers have imperfect

information.

Diminishing marginal returns occur in the short run.

The marginal cost curve always intersects the average total cost curve at the minimum

of average total cost.

One would expect people who work the night shift to have higher wages than their

day-shift counterparts.

Basically, the marginal principle teaches us to evaluate the factors involved in taking an

action to decide if the action it is worth the effort.

The official poverty line in the U.S. is determined by a minimum food budget times

five.

Mergers can sometimes be good for a market by allowing firms to take advantage of

economies of scale.

As more high-risk consumers enter the health insurance market, the average cost of

health insurance service decreases.

Complementary goods are goods that are normally consumed together.

The APEC (Asia Pacific Economic Cooperation) has more members than the EU.

Monopolistically competitive industries are characterized by no barriers to entry.

Economics tells us what to choose given the tradeoffs.

As the volume of waste decreases (holding the amount of paper produced constant), the

production cost per ton of paper increases at a decreasing rate because the firm must use

increasingly sophisticated abatement equipment to decrease the volume of waste.

Recall the application about the Got Milk? advertising. the generic, non-brand

advertising campaign is benefits all the milk firms so they share the cost and the

benefits of the Got Milk? campaign.

Prior to the Hart-Scott-Rodino Act, antitrust laws did not apply to proprietorships.

Monopolistically competitive firms offer consumers more variety than perfectly

competitive firms.

People will buy more of a normal good when their income decreases.

If the quantity supplied is infinitely responsive to any change in price, the supply curve

has a price elasticity of supply equal to infinity.

Recall Application 2, “What Have Been the Local Effects of Chinese Imports?” to

answer the following questions:

According to the Application, Chinese Imports have only been disadvantageous to U.S.

local communities.

A tax or charge equal to the external cost per unit of pollution is called abatement.

Patents encourage firms to engage in innovation.

An average-cost pricing policy allows natural monopolies to earn positive economic

profits.

Repair guarantees are a sign the seller thinks they have a lemon.

From a business perspective, the main problem with predatory pricing is that it never

ends and the firm must repeatedly lose money to drive out new competitors.

A firm with total revenue of $500, total cost of $700, and variable cost of $400 should

continue to operate its production facility.

Discrimination in the U.S. workplace is not a determinant of income inequality.

Waiters in countries where it’s customary to tip waiters will tend to have lower wages

than will waiters in countries where tipping is not customary.

The long-run marginal cost is the additional cost incurred by the firm when producing

one more unit of output, holding the amount of capital constant.

Price discrimination can be profitable if consumers can resell the product.

The reason why economists do not need details regarding the topography of a region

when determining driving directions is because economics is because economics

desires unrealistic assumptions.

Public goods are always provided by the government because private markets do not

have an incentive to provide them.

Which of the following is NOT an example of natural monopoly?

A) water systems

B) electricity transmission

C) local telephone services

D) farm products

A table that shows the price of a product and the quantity of that product that a seller is

willing to sell is called the:

A) supply schedule.

B) supply curve.

C) demand schedule.

D) demand curve.

When a second firm enters a monopolist’s market, the initial demand curve facing the

monopolist will:

A) shift to the left.

B) shift to the right.

C) remain the same.

D) none of the above

In monopolistic competition, the firm can increase price and still sell some output

because:

A) there is no free entry.

B) they are producing a product for which there is no close substitute.

C) they are colluding with other firms to set price.

D) they are producing a product that has some degree of differentiation.

Marginal revenue is equal to price for a perfectly competitive firm because:

A) total revenue increases by the price of the good when an additional unit is sold.

B) total revenue increases by less than the price of the good when an additional unit is

sold.

C) firms need to lower price to increase the quantity sold.

D) firms can increase price and still increase the quantity sold.

A residential cleaning company has total costs of $45,000 and total variable costs of

$25,000. The cleaning company has total fixed costs that equal to:

A) $45,000.

B) $20,000.

C) $70,000.

D) indeterminate because the firm’s output level is not known.

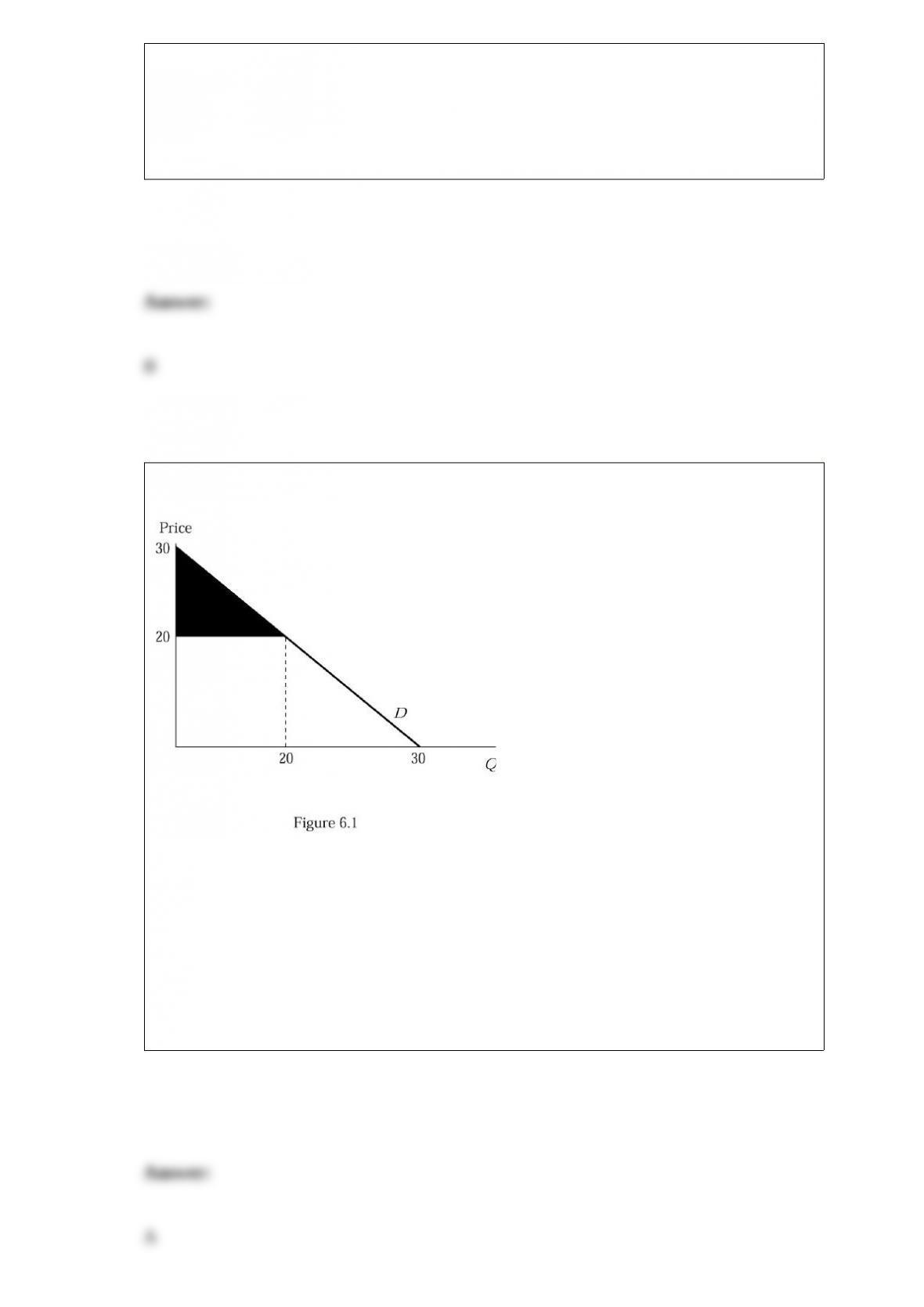

If the good in Figure 6.1 were free:

A) consumer surplus would equal $450 and consumer expenditure would be $0.

B) consumer surplus and consumer expenditure would both be maximized.

C) consumer surplus and consumer expenditure would both be zero.

D) consumer surplus would be maximized but consumer expenditure would be

impossible to calculate.

When two firms in an industry become one firm, they are engaged in:

A) a trust agreement.

B) a merger.

C) predatory pricing.

D) none of the above.

Recall the Application. If the external costs of drivers on average could be internalized

by a vehicle mileage traveled tax of 4.4 cents per mile, then you would expect that to

fully internalize the external costs of accident by drivers older than 70 to be:

A) 4.4 cents per mile.

B) lower than 4.4 cents per mile.

C) higher than 4.4 cents per mile.

D) zero as there are no externalities in driving.

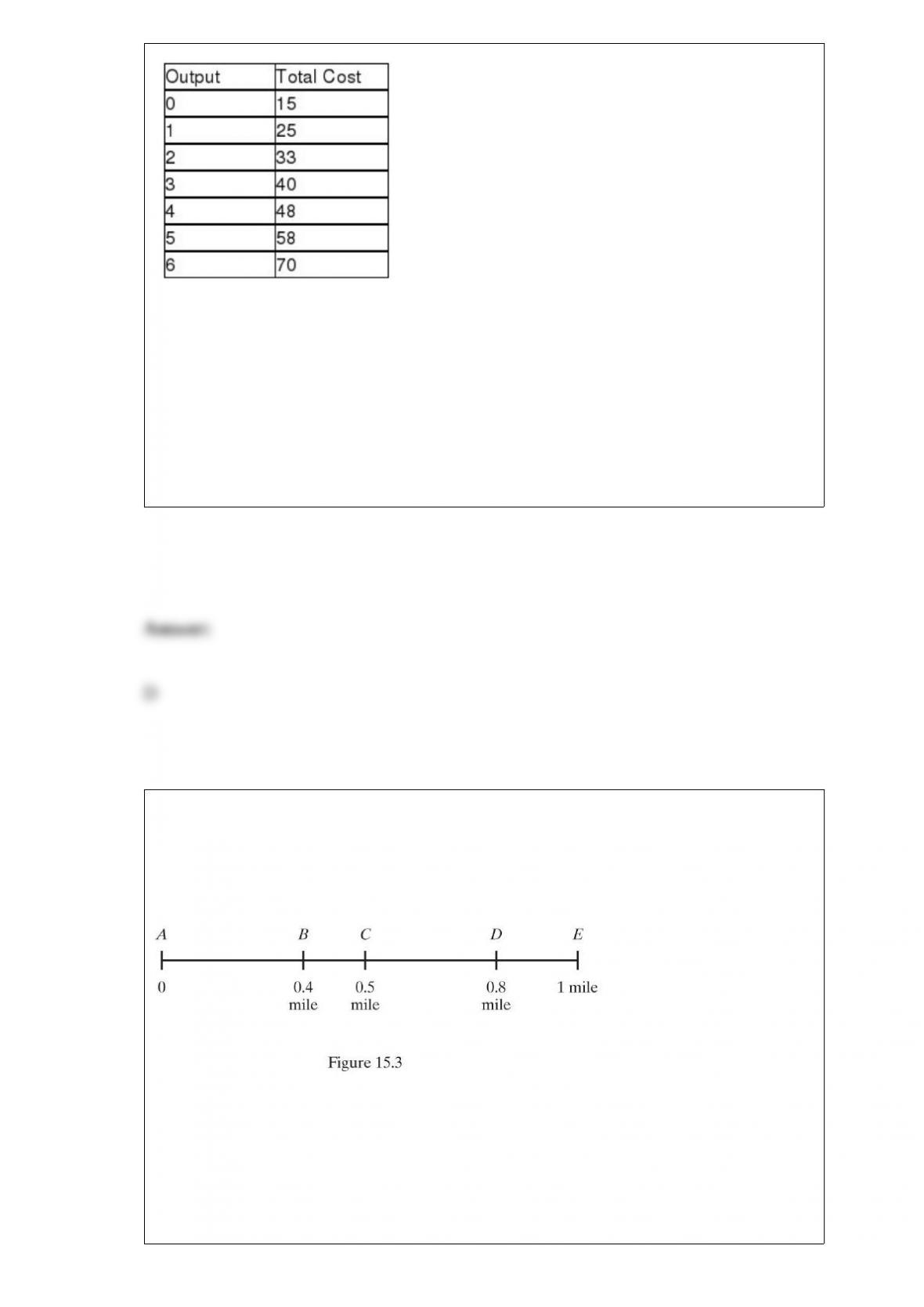

Refer to Table 8.5. The firm experiences diminishing returns beginning with the

________ unit.

Table 8.5

A) first

B) second

C) third

D) fourth

Figure 15.3 depicts a one-mile stretch of beach with 100 swimmers distributed evenly

along the beach. There are two ice cream vendors – 1 and 2 – on the beach selling an

identical product. Assume that each swimmer buys only one ice cream cone and that

they prefer to buy ice cream from the nearer vendor. If vendor 1 is at A while vendor 2

is at D, vendor 1 has an incentive to move:

A) to the left of its current location.

B) to the right of vendor 2’s location.

C) toward the median location.

D) none of the above

Based on the strength of their gut feelings, consumers with relatively active ________

are reluctant to spend money.

A) prefrontal cortexes

B) amygdalas

C) Nucleus Accumbens

D) insulas

In some monopolistically competitive markets, differentiation is obtained simply by

location. Which of the followings is NOT a good sample of differentiation by location?

A) gas stations

B) movie theaters

C) music stores

D) restaurants

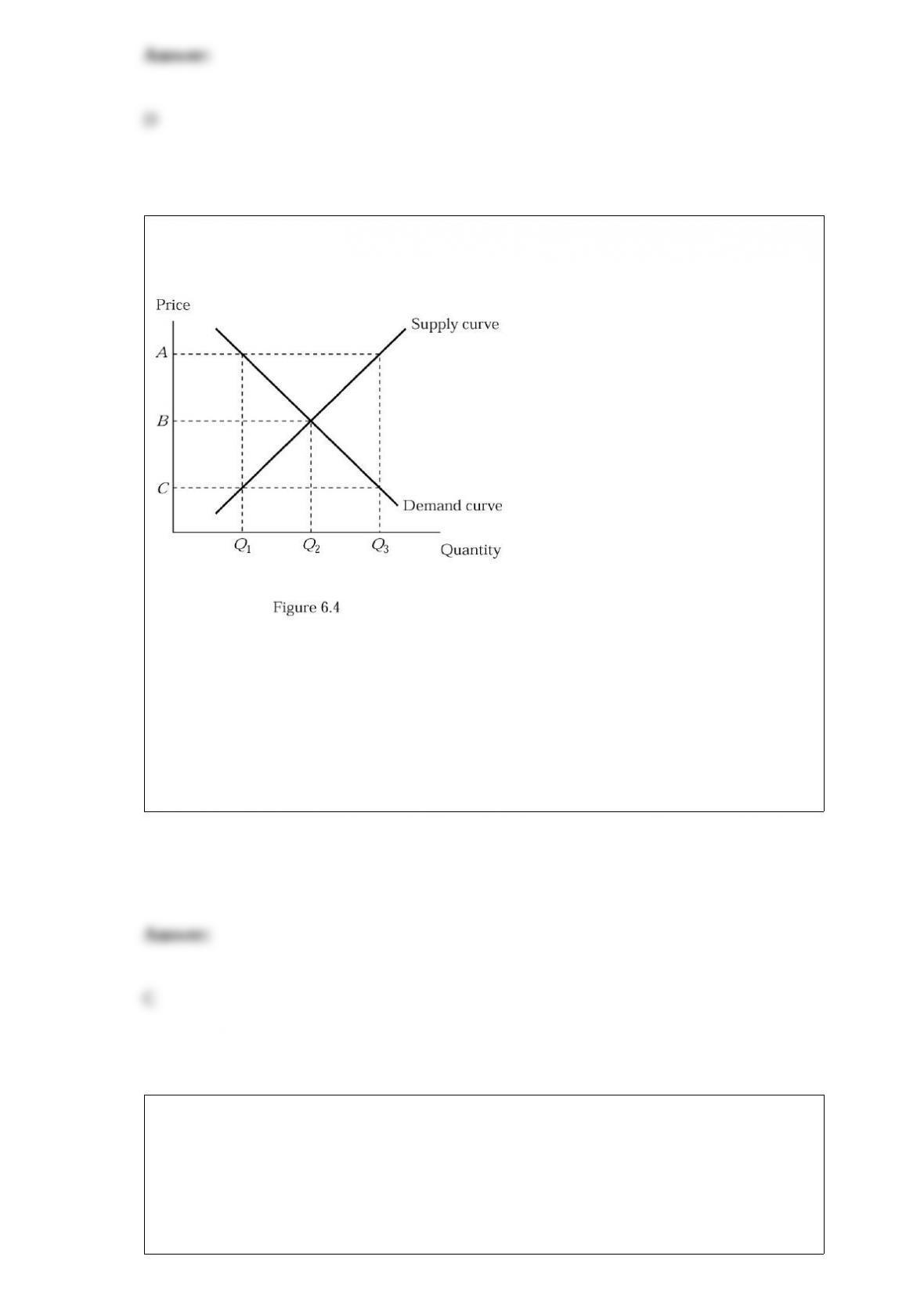

Refer to Figure 6.4. If consumers currently gain at the expense of producers, a

maximum price must have been set at:

A) A.

B) B.

C) C.

D) There is not sufficient information.

In which of the following market structures can you find differentiated products?

A) monopoly

B) perfect competition

C) oligopoly

D) monopolistic competition and oligopoly

Recall the Application. Suppose a firm that produces trampolines has a linear demand

curve for its product, with a vertical intercept of $1,500. If the firm does NOT want the

demand for its product to be price-inelastic, the minimum price it should charge is:

A) $500.

B) $750.

C) $1,000.

D) $1,500.

Empirical studies indicate that entry:

A) increases price and profits.

B) decreases price, but increases profits.

C) decreases price and profits.

D) increases price, but decreases profits.

Suppose a product suddenly loses popularity and the firms producing the product begin

to realize large losses. In response, entrepreneurs would:

A) enter the market and increase production.

B) enter the market and decrease production.

C) exit the market and decrease production.

D) exit the market and increase production.

The Motor Carrier Act of 1980 removed the government’s restriction on:

A) entry into the trucking industry.

B) the size of trucks used to transport goods and services.

C) entry into the industry that produces delivery trucks.

D) entry into parcel delivery.

The additional output produced by hiring an additional unit of labor is known as:

A) the productivity of labor.

B) the marginal product of labor.

C) diminishing returns.

D) the derived demand for labor.

In long-run equilibrium for a competitive firm economic profits:

A) will be positive.

B) will be negative

C) will be zero.

D) may be positive, negative, or zero.

Sarah has a savings account with a $1000 balance that earns 3% APY. She decides to

withdraw the entire balance to buy a laptop computer, what will be her opportunity if

her buying the laptop?

A) the cost of the laptop

B) the forgone interest

C) the forgone interest and the cost of the laptop

D) the cost of the laptop minus the forgone interest

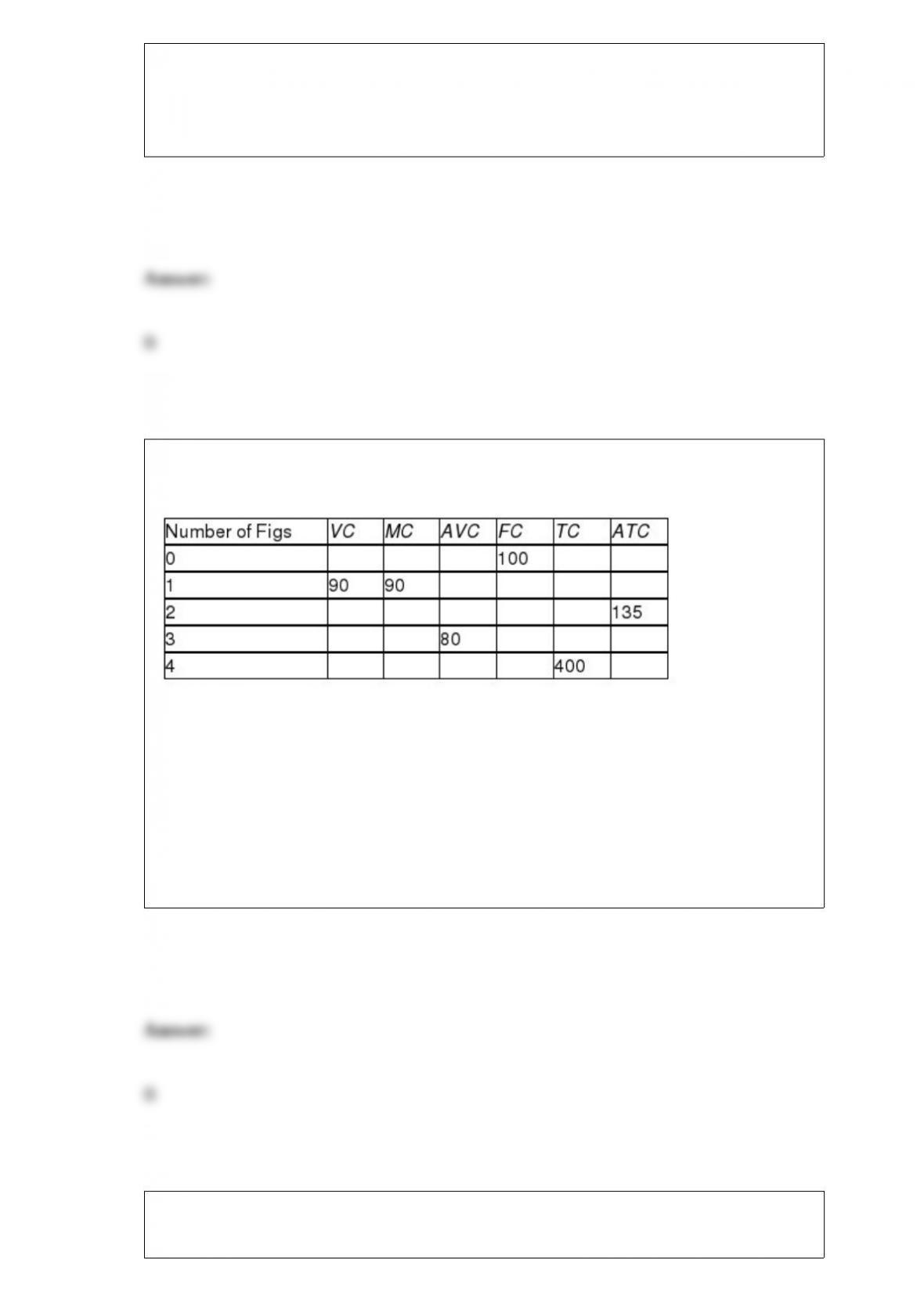

Table 8.4 presents the cost schedule for David’s Figs. If David produces two figs,

David’s average variable costs are:

Table 8.4

A) $80.

B) $85.

C) $90.

D) $170.

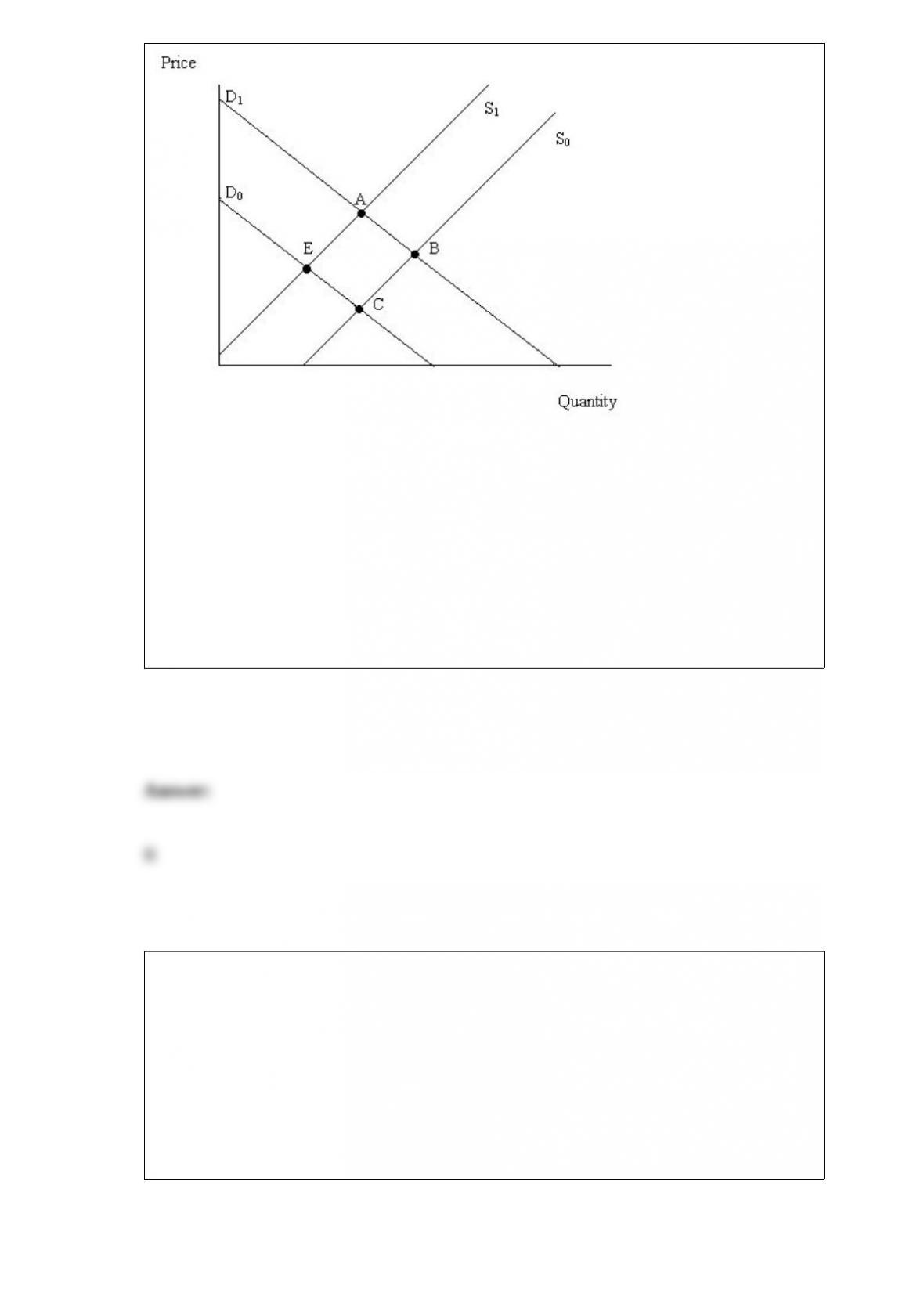

Figure 4.6 illustrates a set of supply and demand curves for a product. When the market

moves from point A to point B, there has been:

Figure 4.6

A) an increase in supply and an increase in demand.

B) an increase in supply and an increase in quantity demanded.

C) an increase in quantity supplied and an increase in demand.

D) an increase in quantity supplied and an increase in quantity demanded.

Insurance:

A) specifies the term of exchange facilitating exchange between strangers.

B) reduces the risk of entrepreneurs.

C) provides the public with reliable information about the performance of a firm.

D) increases the risk faced by entrepreneurs.

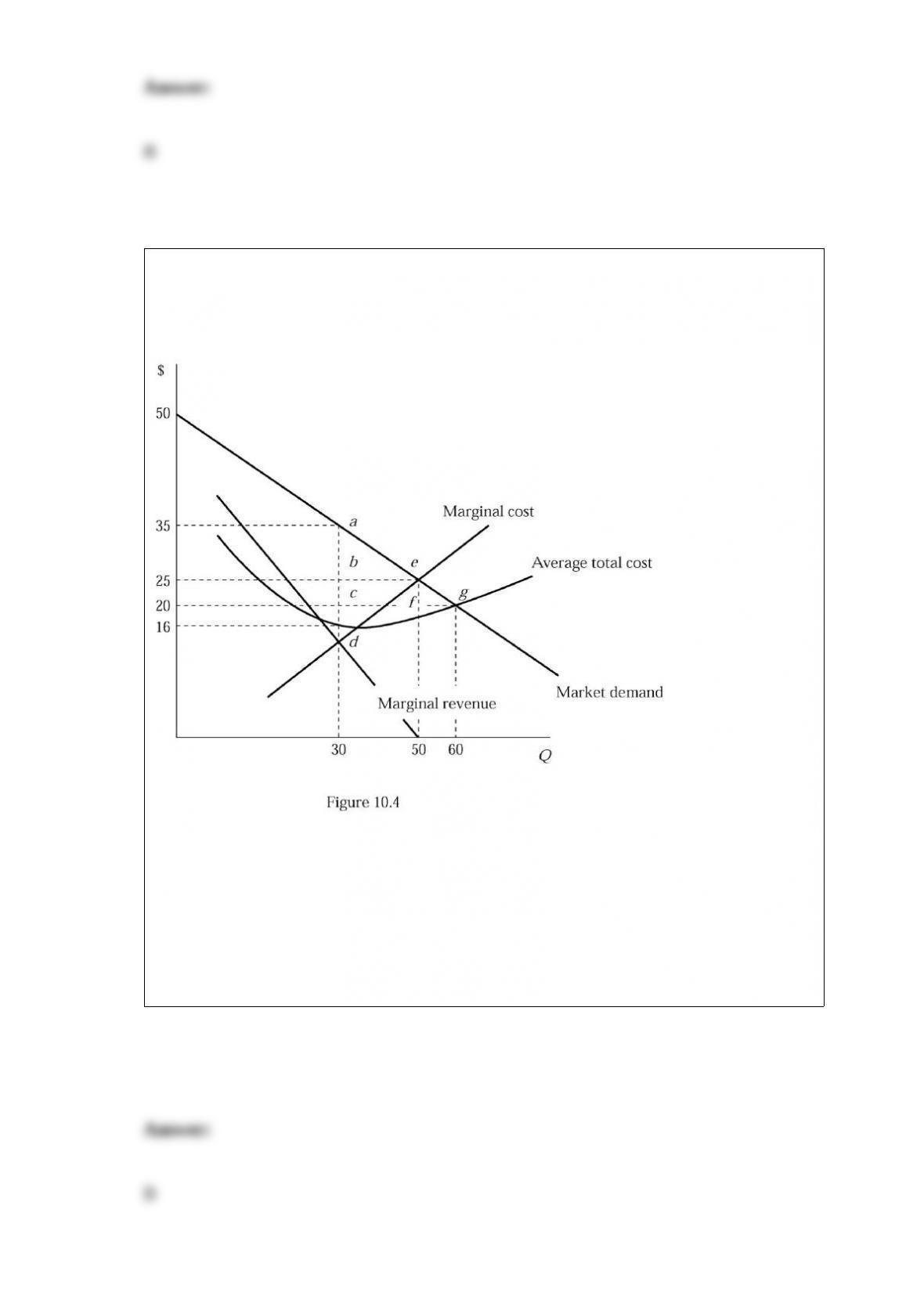

Suppose that Figure 10.4 shows an industry’s market demand, its marginal revenue, and

the production costs of a representative firm. If the industry was perfectly competitive,

a representative firm would charge a price of:

A) $35.

B) $25.

C) $20.

D) $16.

In a constant cost industry, a decrease in price causes:

A) some firms to exit the industry.

B) quantity supplied to remain constant.

C) some firms to enter the industry.

D) price controls.

Jerome has a “C” average in his philosophy course and a “B” average in his economics

course. He decides to study an extra hour for his philosophy exam. This is an example

of:

A) thinking at the margin.

B) using assumptions to simplify.

C) ceteris paribus.

D) caveat emptor.

Recall the Application about Jasper Johns and house painting to answer the

following question(s). In this Application, it is assumed that Johns can earn $5,000

per day by painting works of art, and therefore should hire a house painter who

charges $150 per day, and takes 10 days, to paint his house. Jasper Johns’ daily

earnings are 33.33 times more than the house painter’s daily earnings. If Jasper Johns’

earnings per day were only twice as much as the house painter’s earnings, what should

he do?

A) He should still hire the house painter to paint his house.

B) He should paint his house himself.

C) He should hire a less productive house painter.

D) He should remain indifferent as to who paints the house, for the difference in daily

earnings would now be much less significant.

According to the Application, the demand for gasoline is:

A) less elastic in the long run because consumers have less opportunity to change their

behavior.

B) more elastic in the long run because consumers have time to respond to changes in

price.

C) inelastic in the long run and in the short run.

D) elastic in the short run.

In the short run, the marginal cost of the first unit of output is $20, the average variable

cost of producing three units of output is $16, and the marginal cost of producing the

second unit of output is $16. What is the marginal cost of producing the third unit of

output?

A) $12

B) $16

C) $20

D) $48

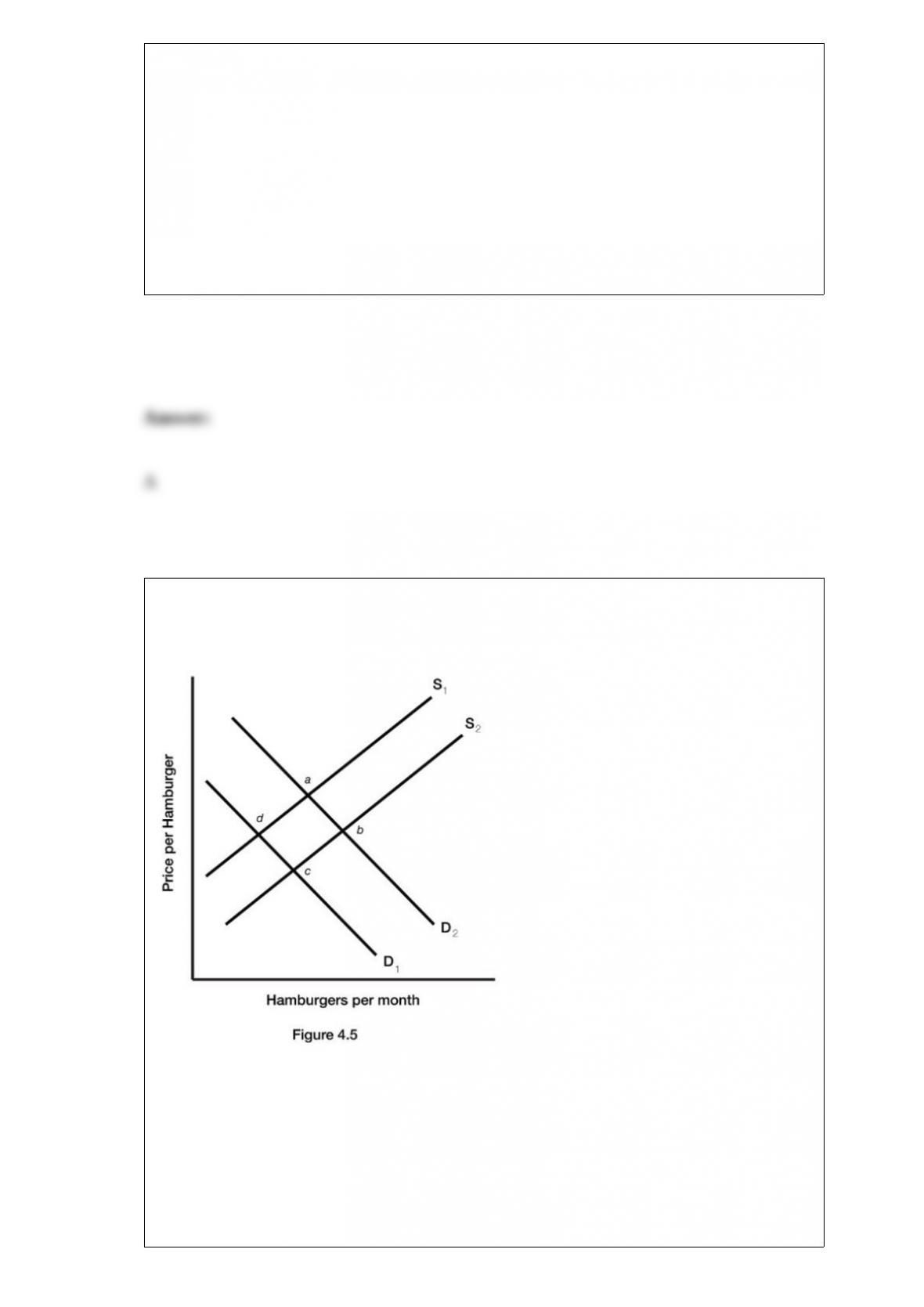

Figure 4.5 illustrates a set of supply and demand curves for hamburgers. A decrease in

demand and a decrease in quantity supplied are represented by a movement from:

A) point c to point a.

B) point a to point c.

C) point b to point c.

D) point d to point b.

Which of the following is a characteristic of an oligopoly market?

A) control over price

B) diseconomies of scale in production

C) firms act independently without regard to each other

D) all of the above

In a market system, self-interest motivates most people to:

A) avoid paying insurance premiums.

B) remain self-sufficient.

C) provide products for other people.

D) rely on government central planning.

Politicians are often heard saying that tuition at state universities should be kept low “to

make education equally accessible to all residents of the state, regardless of income.”

Assuming that state funding for the universities is held constant, what condition will

prevail if tuition is held below equilibrium price? Will education really be “equally

accessible” under these conditions?

What do economists mean when they say that there is “no such thing as a free lunch”?

What is a discovered price?

Why might the market supply of workers increase when wages increase in a particular

occupation or location?

Explain the output effect of an increase in the wage rate.

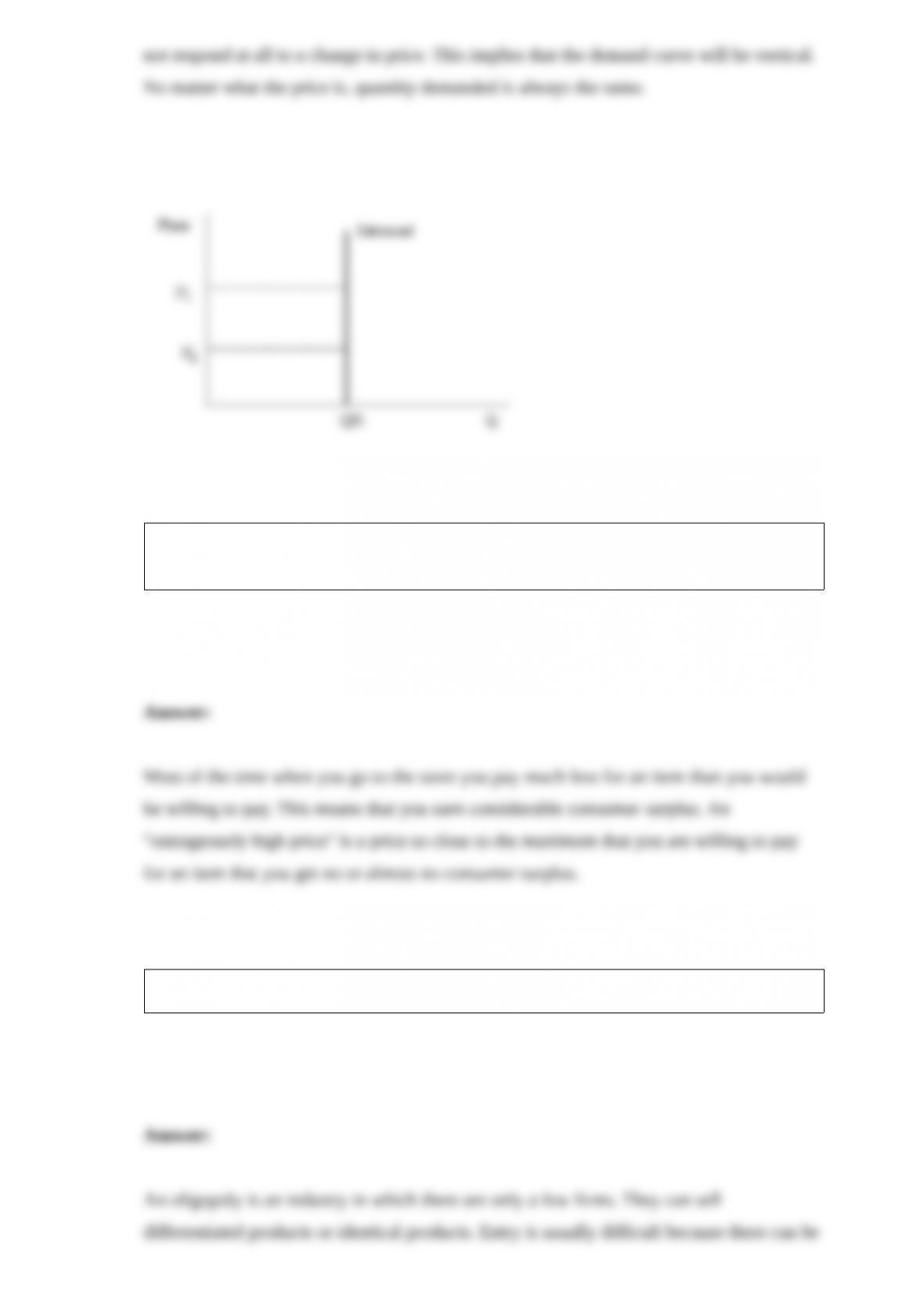

What does it mean for a good to have a perfectly inelastic demand? Draw a demand

curve of this type. Explain why it has the shape that it does.

People often complain about paying “outrageously high prices.” Define an

“outrageously high price” in terms of consumer surplus.

What are the key characteristics of an oligopoly?

How do economies of scale affect the shape of the long-run average cost curve?

Would an economist consider clean air a scarce resource? Explain.

What does elasticity measure?

Why do existing firms earn smaller profits as new firms enter an industry?

Explain the difference between private and public goods.

What are the main differences between adverse selection and moral hazard in the

insurance market?

Explain what means-tested programs are and how they affect the poverty rate in the

U.S.

Explain how patents have been beneficial for markets.

Explain why featherbedding may or may not increase the demand for labor.

Suppose that the U.S. has comparative advantage on cars while Japan has comparative

advantage on TVs. Assume that both countries produce both goods in autarky. If both

countries open their economies to trade, identify the workers in each country who will

be hurt by free trade.

Suppose that A Cleaner World invents a new type of laundry detergent that has an

ingredient that stops stains from setting into clothes. If the laundry detergent market is

monopolistically competitive, explain what will happen to the price of its product in the

short run. What will happen in the long run?