In the short run, marginal product of labor increases at first and then falls because

A) as more labor is hired, they are not as skilled as the first ones hired.

B) there are fewer opportunities for division of labor and specialization when fewer

workers are hired.

C) managerial inefficiency sets in when a firm gets too large.

D) the new workers do not have as much experience as those who have been with the

firm for a long time and therefore are not as productive.

A firm’s demand for labor curve is also called its

A) marginal revenue product of labor curve.

B) marginal factor cost of labor curve.

C) marginal valuation curve.

D) marginal benefit of labor curve.

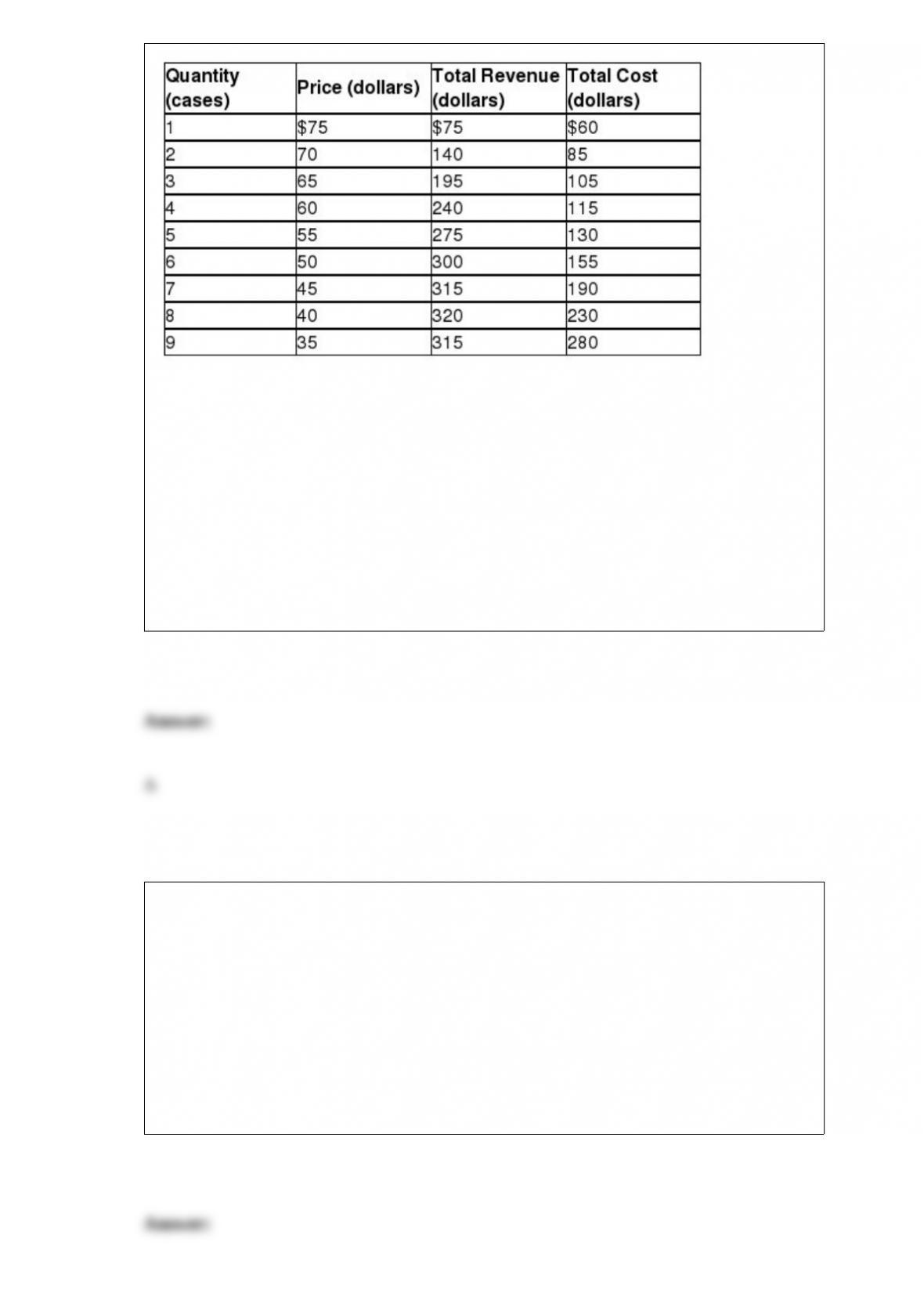

Table 13-2

Eco Energy is a monopolistically competitive producer of a sports beverage called

Power On. Table 13-2 shows the firm’s demand and cost schedules. What is likely to

happen to the product’s price in the long run?

A) It will fall.

B) It will increase.

C) It will remain constant.

D) This cannot be determined without information on its long-run demand curve.

All of the following policies are ways for a country to promote long-run economic

growth except

A) increasing vaccinations against infectious diseases.

B) undergoing political reform to decrease corruption.

C) enacting stronger laws to protect property rights.

D) imposing stricter regulations to limit foreign direct investment.

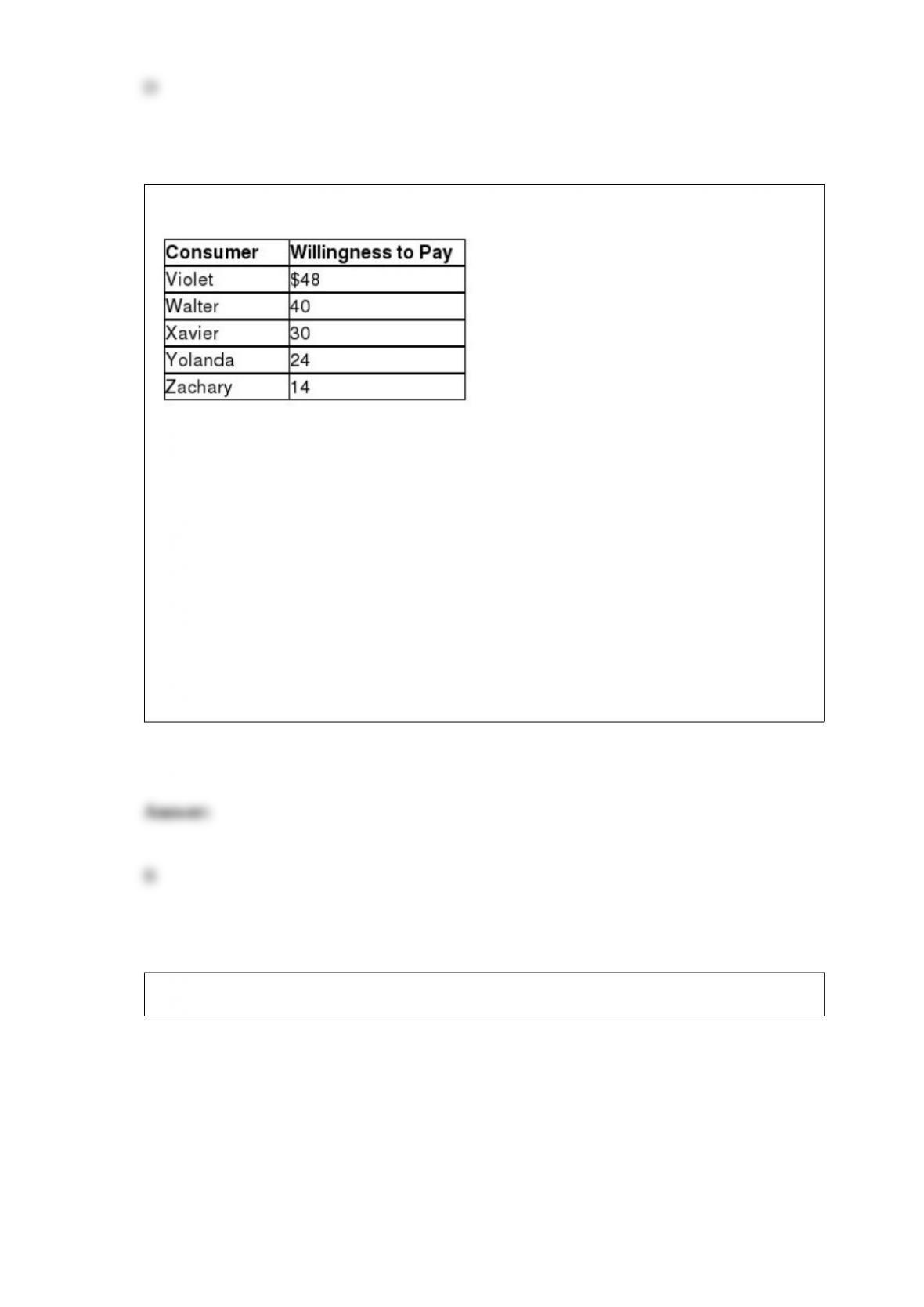

Table 4-5

The table above lists the highest prices five consumers are willing to pay for a concert

ticket. If the price of one of the tickets is $36,

A) Violet and Walter will each buy two tickets.

B) Walter will receive $4 of consumer surplus from buying one ticket.

C) Violet and Walter receive a total of $52 of consumer surplus from buying one ticket

each. No one else will buy a ticket.

D) Xavier, Yolanda, and Zachary will receive a total of $68 of consumer surplus since

they will buy no tickets.

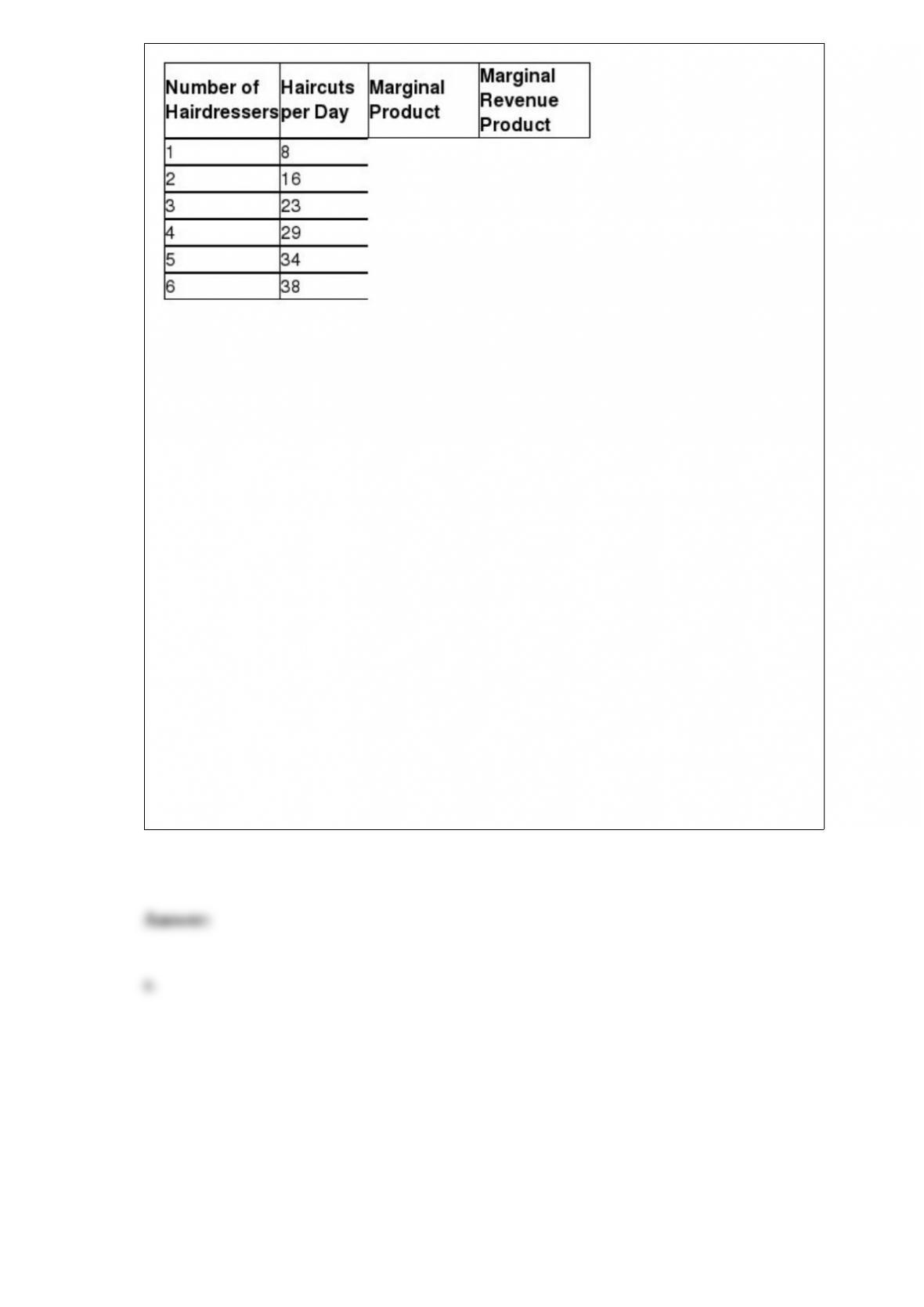

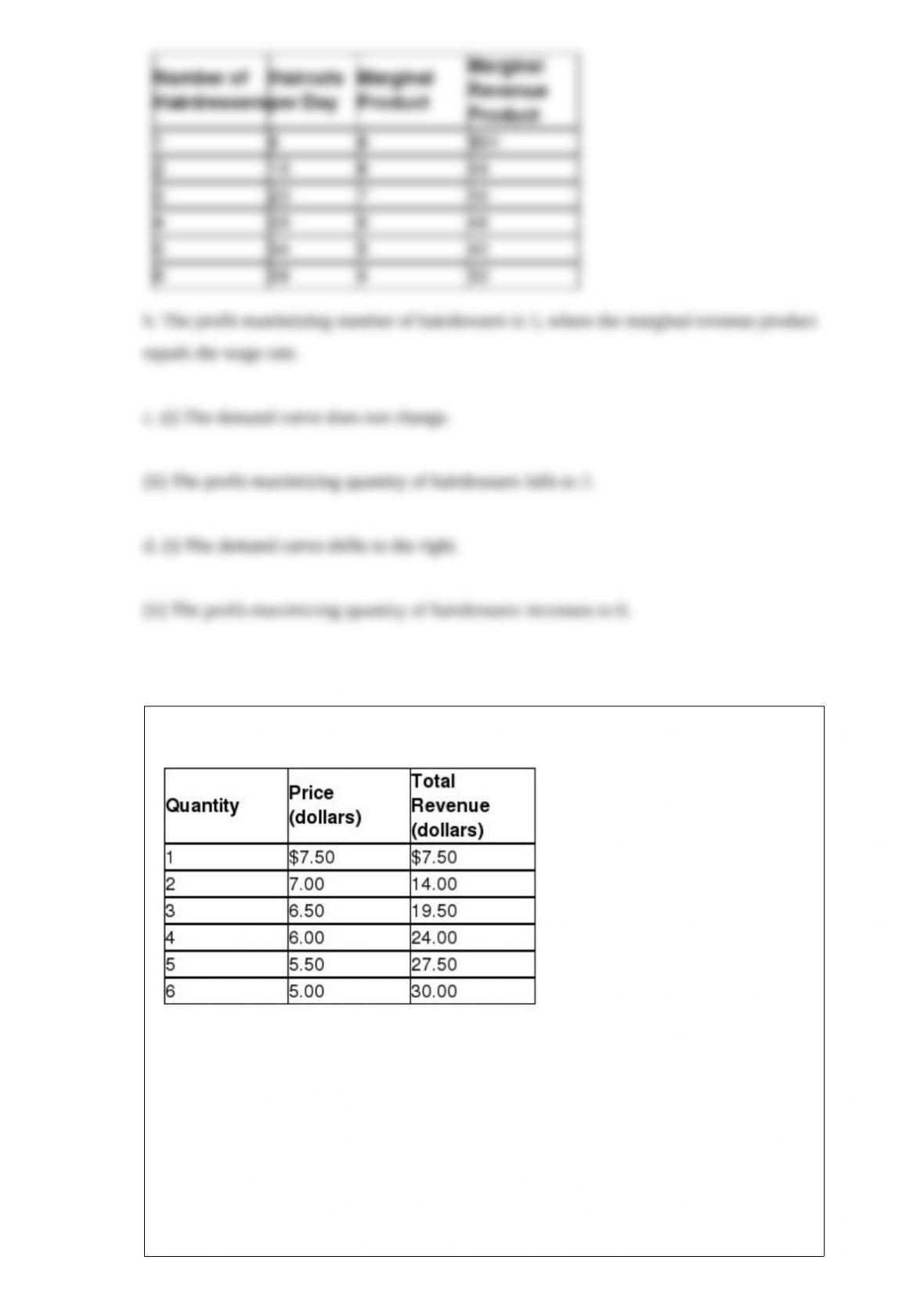

Table 17-6

The Hair Cuttery, a new hair salon, is ready to start hiring. The table above shows the

relationship between the number of hairdressers the firm hires and the quantity of

haircuts it produces.

a. Suppose the price of haircuts is $8. Complete the table by filling in the values for

marginal product and marginal revenue product.

b. The Hair Cuttery is an input price-taker. Suppose the wage paid to hairdressers is $40

per day. What is the profit-maximizing number of hairdressers?

c. Suppose the wage rate rises to $60 per day.

(i) What happens to the firm’s demand curve for hairdressers?

(ii) What happens to the profit-maximizing quantity of hairdressers?

d. Suppose the wage rate is $40 per day and the price of haircuts is now $10.

(i) What happens to the firm’s demand curve for hairdressers?

(ii) What happens to the profit-maximizing quantity of hairdressers?

Table 13-1

The Table shows

A) an elastic segment of the demand curve.

B) an inelastic segment of the demand curve.

C) a demand curve with an elastic segment of the demand curve from $7.50 to $6.50

followed by an inelastic segment.

D) a demand curve with an inelastic segment of the demand curve from $7.50 to $6.50

followed by an elastic segment.

By making exchange ________, money allows for ________ and higher ________.

A) harder; specialization; costs

B) easier; specialization; productivity

C) harder; generalization; productivity

D) easier; specialization; costs

Wall Street, in the borough of Manhattan in New York City, is the heart of the U.S.

financial system, where banks, brokerage houses, other financial firms, and the New

York Stock Exchange are all located. What is the reason for New York City’s

comparative advantage in the financial market?

A) the development of superior information technology

B) an abundant supply of skilled labor

C) New York City has one of the largest sea ports in the world.

D) external economies

Consumption spending is $5 million, planned investment spending is $8 million, actual

investment spending is $8 million, government purchases are $10 million, and net

export spending is $2 million. Based on this information, which of the following is

true?

A) There was an unplanned change in inventories.

B) Aggregate expenditure is equal to GDP.

C) Aggregate expenditure is greater than GDP.

D) Aggregate expenditure is less than GDP.

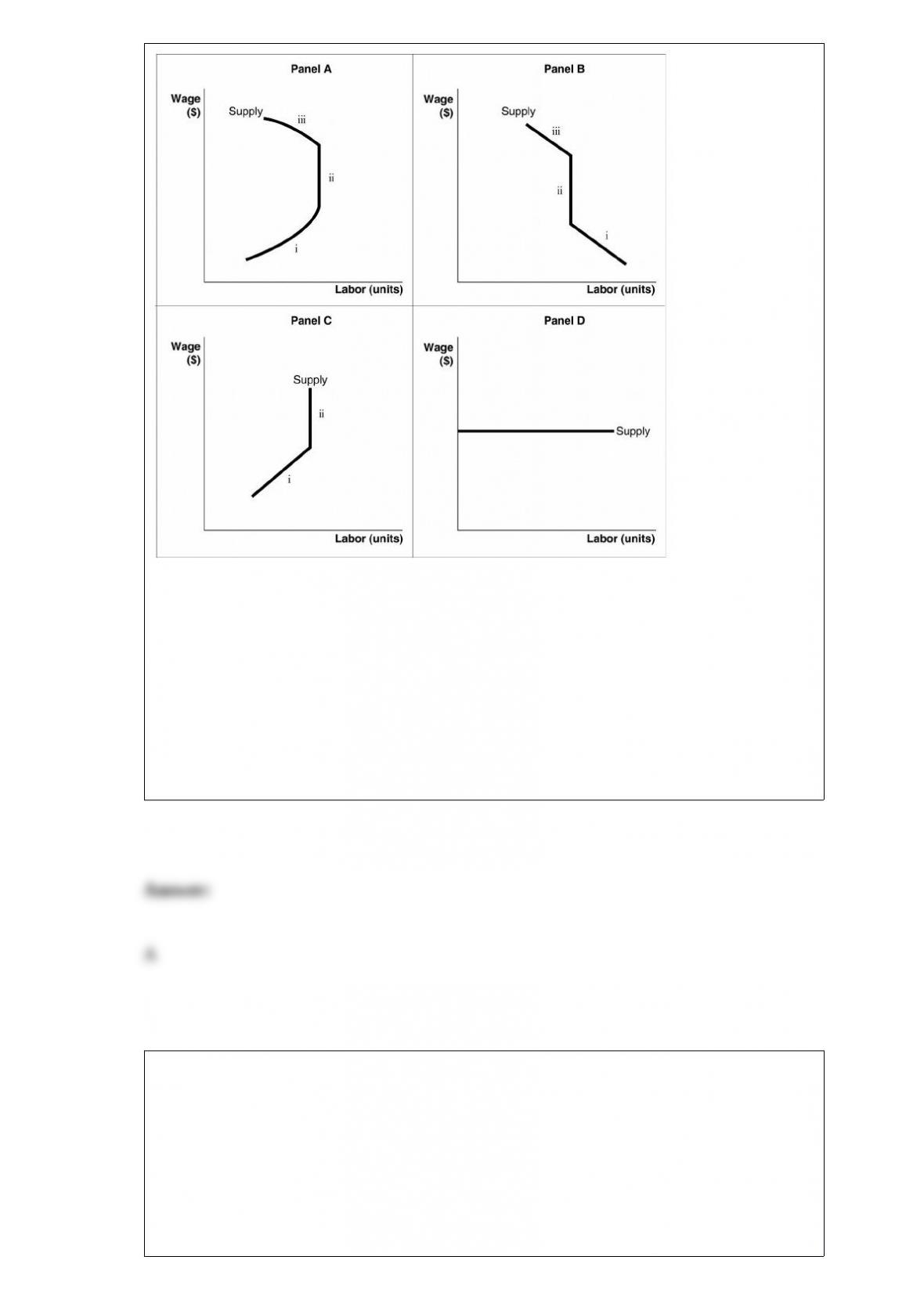

Figure 17-3

Which of the panels in the diagram best represents an individual’s labor supply curve?

A) Panel A

B) Panel B

C) Panel C

D) Panel D

If the price of pineapple juice was $4.50 a gallon and it is now $5.75 a gallon, what is

the percentage change in price?

A) 7.8 percent

B) 12.5 percent

C) 27.7 percent

D) 57.5 percent

Because of diminishing returns, an economy can continue to increase real GDP per hour

worked only if

A) there are decreases in human capital.

B) the per-worker production function shifts downward.

C) there continue to be decreases in capital per hour worked.

D) there is technological change.