Under FASB 157, Level _______ assets valuation are based on observable market

prices for similar assets or liabilities.

a. 1

b. 2

c. 3

d. 4

e. 5

Answer:

Under FASB 157, Level _______ assets valuation are based on observable market

prices for the identical instrument.

a. 1

b. 2

c. 3

d. 4

e. 5

Answer:

Which of the following was a goal of the Depository Institutions Deregulation and

Monetary Control Act of 1980?

a. To reduce the range of banking services offered.

b. To allow banks to pay market rates on deposits.

c. To allow banks to make long-term mortgage loans.

d. To allow banks to offer Money Market Deposit Accounts.

e. To reduce the number of leveraged buyouts.

Answer:

Which of the following is not considered a volatile liability?

a. Jumbo CDs

b. Deposits in foreign offices

c. Repurchase agreements

d. Federal funds sold

e. All of the above are considered volatile liabilities

Answer:

A bank currently owns a municipal bond paying a tax-exempt rate of 8%. If the banks

marginal tax rate is 39%, what is the taxable equivalent yield?

a. 11.12%

b. 4.88%

c. 13.11%

d. 5.76%

e. 9.32%

Answer:

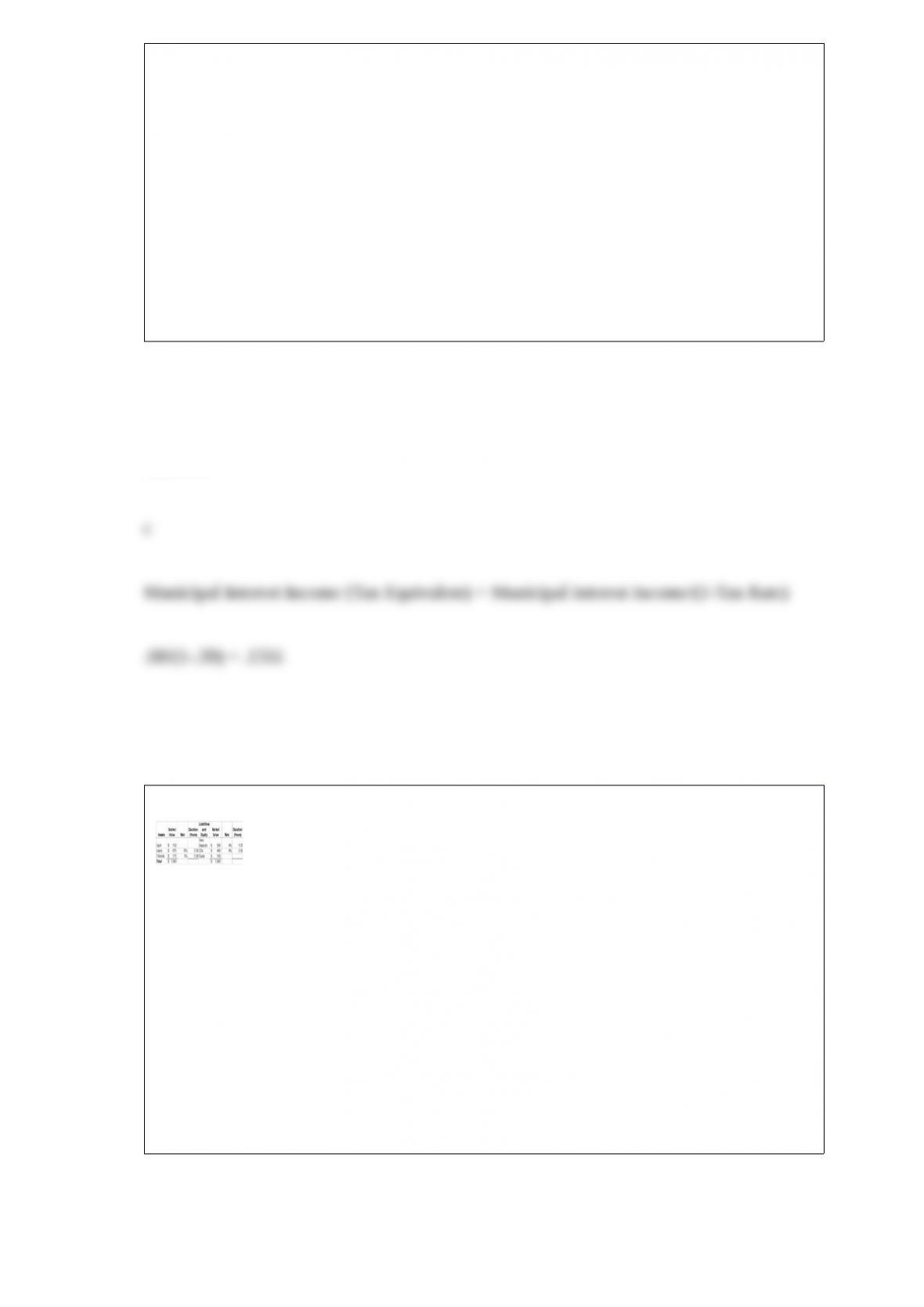

Use the following bank information.

If interest rates rise 1% for all assets and liabilities, what is the approximate expected

change in the economic value of equity?

a. –$2.56

b. $5.84

c. –$5.84

d. $6.78

e. -$6.78

Answer:

____________ of financial futures contracts require physical delivery.

a. Nearly 100%

b. Approximately 75%

c. Approximately 50%

d. Approximately 25%

e. Less than 1%

Answer:

To be classified as a non-current loan, payments must be past due a minimum of how

many days?

a. 30 days

b. 60 days

c. 90 days

d. 120 days

e. 158 days

Answer:

For a bank that has a positive duration gap, an increase in interest rates will cause a(n)

_______ in the economic value of assets, that is _______ than the _________ in the

economic value of liabilities, and a(n) _______ in the economic value of equity.

a. increase, greater, decrease, increase

b. increase, less, increase, decrease

c. increase, greater, increase, increase

d. decrease, less, decrease, increase

e. decrease, greater, decrease, decrease

Answer:

Which of the following is not a weakness of risk-based capital standards?

a. They ignore interest rate risk.

b. They ignore the value of deposit insurance.

c. They ignore changes in the market value of assets.

d. They ignore credit risk.

e. They ignore the value of a bank’s charter.

Answer:

The Helping Families Save Their Homes Act of 2009 included provisions:

a. intended to prevent mortgage foreclosures.

b. to enhance the availability of mortgage credit.

c. to protect renters living in foreclosed homes.

d. All of the above are correct.

e. Only a. and b. are correct.

Answer:

Redlining is a lending practice of not extending credit:

a. to minimum wage earners.

b. to finance low-income housing.

c. to students.

d. to targeted minority groups.

e. within a geographic area that is believed to be deteriorating.

Answer:

Duration:

a. is always greater than maturity.

b. rises as the coupon payment rises.

c. measures how bond prices change with changes in maturity.

d. is a measure of total return.

e. is a measure of how price sensitive a bond is to a change in interest rates.

Answer:

Use the following information.

A London based firm has a subsidiary located in New York. The subsidiary has $1,000

in assets and $750 in liabilities. The current spot rate is $1.60/£.

If the spot rate changes to $1.50/£,

a. The U.S. firm’s stockholders’ equity would increase.

b. The U.S. firm’s stockholders’ equity would decrease.

c. The U.S. firm’s stockholders’ equity would not be impacted.

d. The U.S. firm would have to report the change in earnings.

e. Both a. and d.

Answer:

Widespread use of credit scoring:

a. standardizes the perceived quality of different loan types.

b. decreases the supply of credit.

c. increases market interest rates.

d. reduces the costs of the associated loans.

e. all of the above.

Answer:

Which of the following characteristics should collateral have?

a. The value of the collateral should not exceed the value of the loan.

b. The collateral claim must be legal and clear.

c. The lender must have a ready market for the collateral.

d. a. and b. only.

e. b. and c. only.

Answer:

Short-term working capital loans are generally repaid with funds from:

a. investing cash flows.

b. issuing new debt.

c. reductions in inventory and receivables.

d. issuing new equity

e. redeeming marketable securities.

Answer:

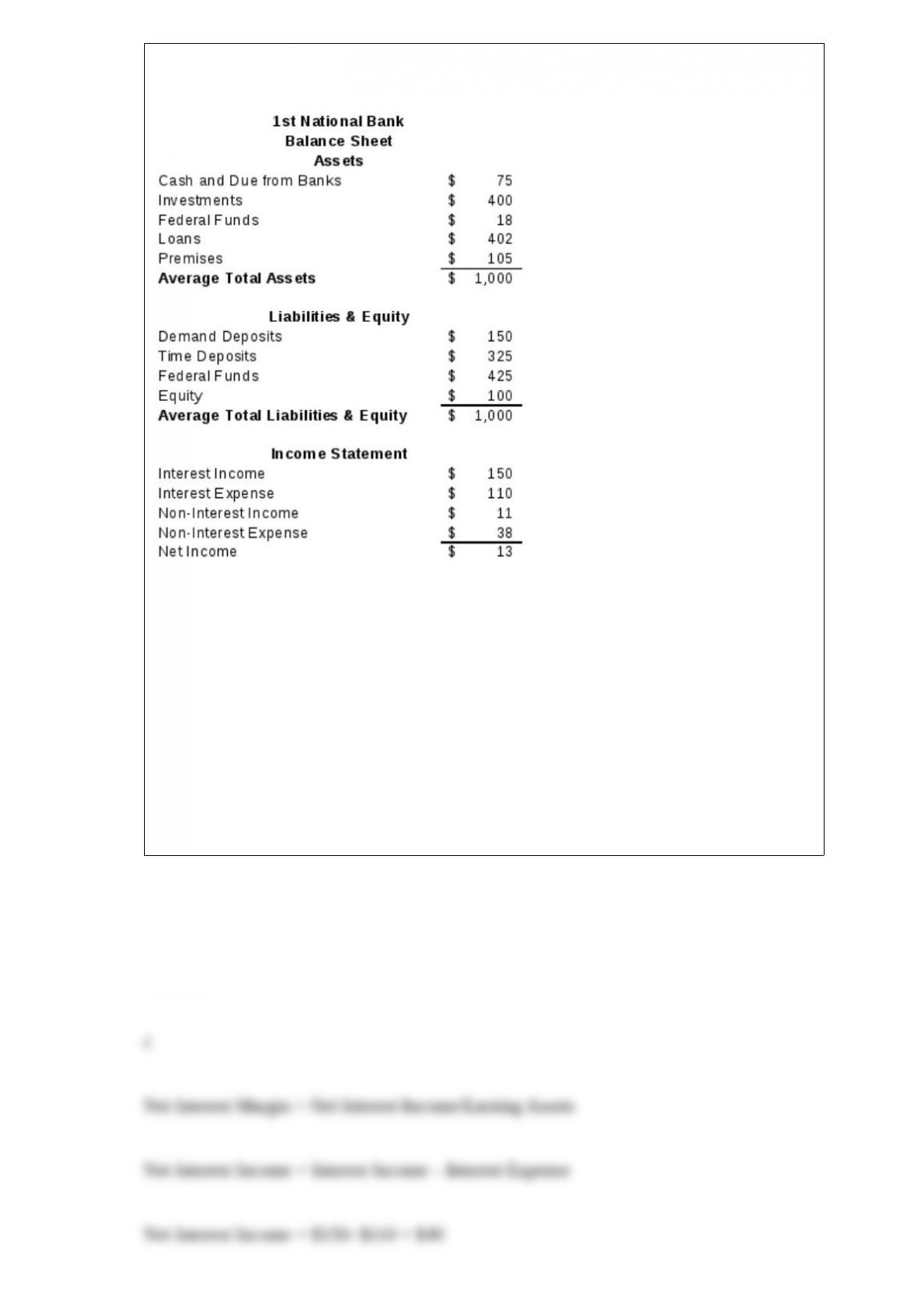

Use the following information.

What is 1st State’s net interest margin?

a. 0.6%

b. 3.8%

c. 4.9%

d. 8.2%

e. 9.8%

Answer:

Everything else the same, financial leverage works to a bank’s advantage when:

a. the return on assets is positive.

b. the return on assets is negative.

c. fixed assets are high.

d. fixed assets are low.

e. a. and d.

Answer:

__________ is not a measure of bank productivity?

a. Assets per employee

b. Average personnel expense

c. Loans per employee

d. Net income per employee

e. Number of customers per employee

Answer:

Securities that require unrealized gains or losses to be recorded as a change in

stockholder’s equity are called:

a. held-to-maturity securities.

b. trading account securities.

c. available-for-sale securities.

d. revenue securities.

e. repurchase agreements

Answer:

When a bank lends in a narrow geographic area, they are subject to:

a. country risk.

b. concentrated risk.

c. historical risk.

d. charge-off risk.

e. portfolio risk.

Answer:

A bond that has an annual coupon rate of 11% has three years to maturity. If the current

discount rate is 16%, what is the bond’s Macaulay’s duration?

a. 3.00 years

b. 2.991. years

c. 2.89 years

d. 2.79 years

e. 2.69 years

Answer:

Which of the following is false regarding duration gap analysis?

a. Duration gap analysis does not classify assets as rate-sensitive.

b. Duration gap analysis indicates the potential change in a bank’s net interest income.

c. Duration gap accounts for bank leverage.

d. Duration gap accounts for the present value of cash flows associated with all

liabilities.

e. Duration gap analysis indicates the potential change in a bank’s market value of

equity.

Answer:

The _________ mandated that the FDIC take prompt corrective action in dealing with

bank failures.

a. Depository Institutions Act (Garn-St. Germain)

b. Competitive Equality Banking Act

c. Financial Institutions Reform, Recovery and Enforcement Act

d. Federal Deposit Insurance Corporation Improvement Act

e. Depository Institutions Deregulation and Monetary Control Act

Answer:

Which of the following is the primary emphasis of a values-driven credit culture?

a. Annual bank profit

b. Bank soundness and stability

c. Loan volume

d. Loan growth

e. Short-term earnings

Answer:

Most checks clear in no more than _____ days.

a. 1

b. 2

c. 3

d. 4

e. 5

Answer:

Which of the following is the receiver of a failed depository institution?

a. Federal Reserve

b. Federal Deposit Insurance Corporation

c. Office of the Comptroller of the Currency

d. Office of Thrift Supervision

e. Federal Savings and Loan Insurance Corporation

Answer:

Unsecured liabilities created from the exchange of immediately available funds are

known as:

a. federal funds purchased.

b. repurchase agreements.

c. federal funds sold.

d. pledged securities.

e. brokered deposits.

Answer:

Salomon Brothers’ collateralized automobile receivables securities are labeled:

a. AUTOs.

b. CARDs.

c. VANs.

d. CARs.

e. RACs.

Answer:

Savings and loans have historically specialized in:

a. commercial loans.

b. auto loans.

c. mutual loan.

d. real estate loans.

e. demand deposit accounts.

Answer:

An asset would normally be classified as rate-sensitive if:

a. it matures during the examined time period.

b. it represents a partial principal payment.

c. the outstanding principal on a loan can be re-priced when the base rate changes.

d. All of the above.

e. a. and c. only

Answer:

Interest rate risk:

a. varies inversely with a bank’s GAP.

b. can be measured by the volatility of a bank’s net interest income given changes in the

level of interest rates.

c. can be eliminated by matching fixed rate assets with variable rate liabilities.

d. rarely has an impact on bank earnings.

e. All of the above

Answer: