The government makes all economic decisions in a market economy.

The level of output at which all economies of scale have been exhausted is known as

A) constant returns to scale.

B) minimum efficient scale.

C) the economically efficient output level.

D) optimal economic size.

If the production possibilities frontier is ________, then opportunity costs are constant

as more of one good is produced.

A) bowed out

B) bowed in

C) non-linear

D) linear

If a firm in a perfectly competitive industry experiences persistent losses, in the long

run it should

A) shut down temporarily and wait for market conditions to change.

B) exit the industry.

C) raise its price to cover average total cost.

D) continue to operate if it can raise the demand for its product through advertising and

quality improvements.

If buyers of a monopolistically competitive product feel the products of different sellers

are strongly differentiated, then the demand for each seller’s product is

A) perfectly inelastic.

B) perfectly elastic.

C) relatively inelastic.

D) relatively elastic.

In a modern mixed economy, who decides what goods and services will be produced?

A) only the producers

B) only consumers

C) only the government

D) all of the above

The natural resources used in production are made available in the

A) goods and services market.

B) product market.

C) government market.

D) factor market.

Suppose the governor of California has proposed increasing toll rates on California’s

toll roads, and has presented two possible scenarios to implement these increases.

Following are projected data for the two scenarios for the California toll roads:

Scenario 1: Toll rate in 2015: $10.00. Toll rate in 2019: $22.50

For every 100 cars using the toll roads in 2015, only 81.6 cars will use the toll roads in

2019.

Scenario 2: Toll rate in 2015: $10.00. Toll rate in 2019: $17.50

For every 100 cars using the toll roads in 2015, only 96.2 cars will use the toll roads in

2019.

a. Using the midpoint formula, calculate the price elasticity of demand for Scenario 1

and Scenario 2.

b. Assume 10,000 cars use California toll roads every day in 2015. What would be the

daily total revenue received for each scenario in 2015 and in 2019?

c. Is demand under Scenario 1 and under Scenario 2 price elastic, inelastic, or unit

elastic. Briefly explain.

(For above questions, assume that nothing other than the toll change occurs during the

time frame listed that would affect consumer demand.)

Suppose the demand curve for a product is vertical and the supply curve is upward

sloping. If a unit tax is imposed in the market for this product

A) sellers bear the entire burden of the tax.

B) buyers bear the entire burden of the tax.

C) the tax burden will be shared equally between buyers and sellers.

D) buyers share the burden of the tax with government.

How are the fundamental economic questions answered in a market economy?

A) The government alone decides the answers.

B) Individuals, firms, and the government interact in markets to decide the answers to

these questions.

C) Households and firms interact in markets to decide the answers to these questions.

D) Large corporations alone decide the answers.

Cost-plus pricing may be a reasonable way to determine price when

A) marginal cost and average fixed cost are roughly equal.

B) marginal cost and average cost are about the same.

C) marginal cost differs significantly from average cost.

D) marginal cost is very low.

As a percentage of GDP, exports are greater than imports for which of the following

countries?

A) the United Kingdom

B) France

C) the United States

D) China

The firm’s gain in profit from hiring another worker is

A) the marginal revenue product of the extra worker.

B) the difference between marginal revenue product and the wage of the worker.

C) the extra output of the extra worker.

D) the reduction in costs from hiring another worker.

Both monopolistically competitive firms and perfectly competitive firms maximize

profits

A) by producing where price equals average total cost.

B) by producing where marginal revenue equals average revenue.

C) by producing where marginal revenue equals marginal cost.

D) by producing where price equals average variable cost.

Which of the following demonstrates the endowment effect?

A) Whelan inherits a cottage in Cape Cod from his grandfather and is unwilling to sell

it for sentimental reasons.

B) Chris Hemsworth commands a premium in the movie industry because he is

endowed with dashing looks.

C) Isabella was not willing to part with her “Chris Hemsworth” poster although she was

offered $100 for it, a sum greater than what it costs to purchase another such poster.

D) If you received a good as a gift, you are less likely to attach a monetary value to the

good.

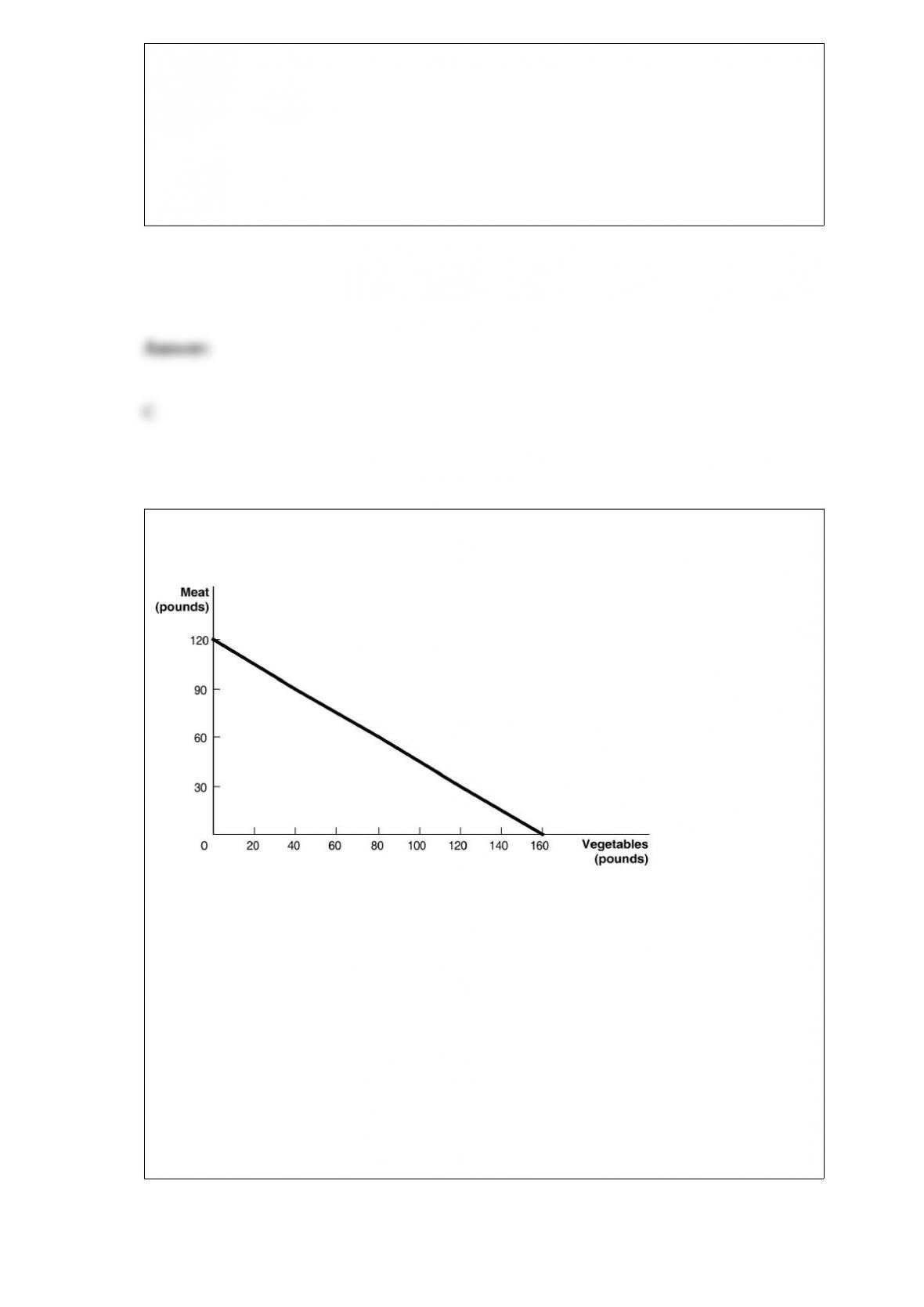

Figure 2-2

Figure 2-2 above shows the production possibilities frontier for Mendonca, an agrarian

nation that produces two goods, meat and vegetables.

Refer to Figure 2-2. The linear production possibilities frontier in the figure indicates

that

A) Mendonca has a comparative advantage in the production of vegetables.

B) Mendonca has a comparative disadvantage in the production of meat.

C) the tradeoff between meat and vegetables is constant.

D) it is progressively more expensive to produce meat.

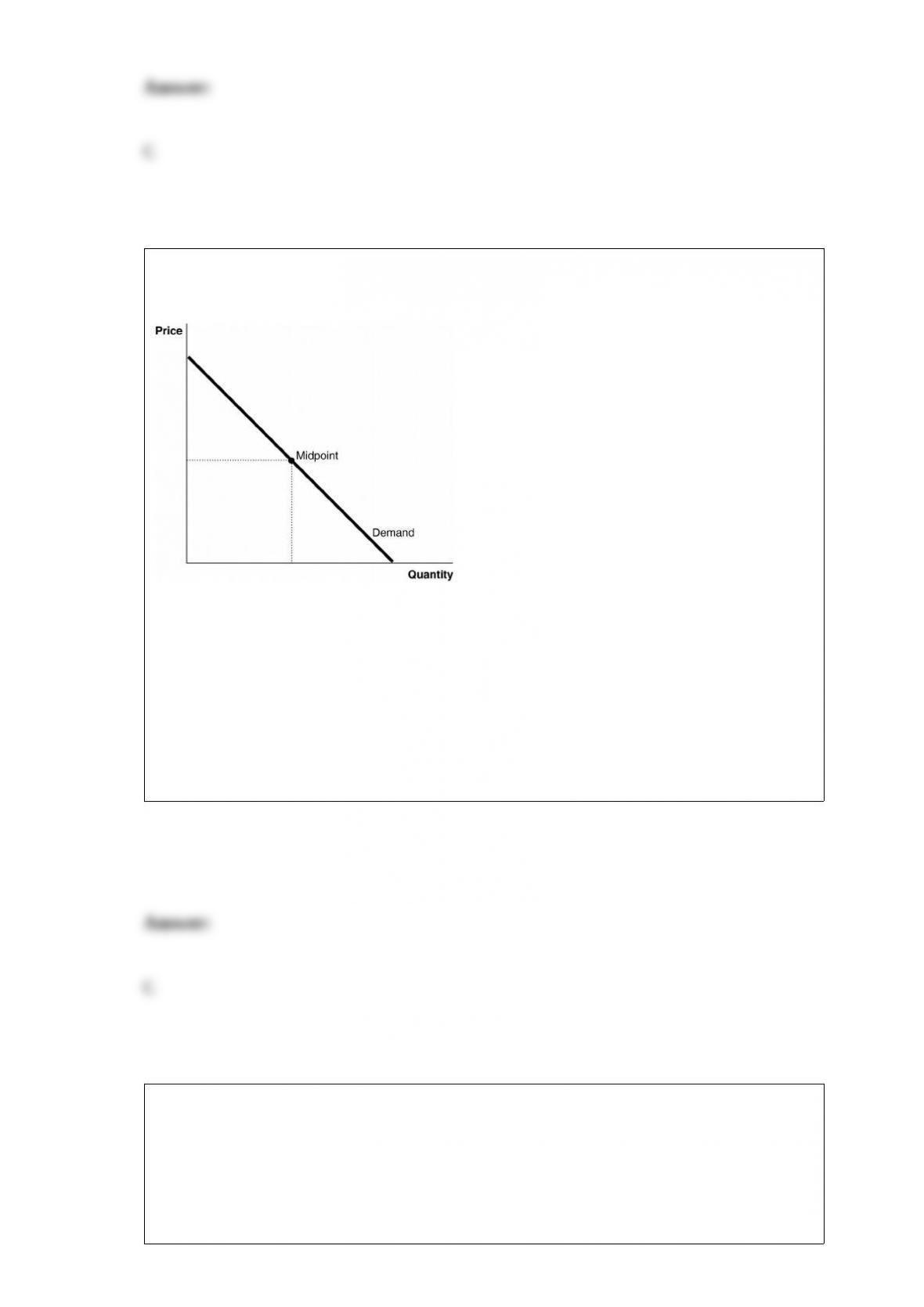

Figure 6-4

Refer to Figure 6-4. The inelastic segment of the demand curve

A) is coincident with the horizontal axis.

B) is coincident with the vertical axis.

C) lies below the midpoint of the curve.

D) lies above the midpoint of the curve.

A major difference between monopolistic competition and perfect competition is

A) the number of sellers in the markets.

B) the degree by which the market demand curves slope downwards.

C) that products are not standardized in monopolistic competition unlike in perfect

competition.

D) the barriers to entry in the two markets.

If firms differentiate their products in different ways and charge different price because

of these differentiation factors, then

A) the law of one price is not violated.

B) transactions costs are being ignored.

C) the firm must not be maximizing profit.

D) demand must be perfectly elastic.

What is the voting paradox?

A) the observation that less than 60 percent of those eligible to vote actually vote

B) the observation that majority voting may not always result in consistent choices

C) the idea that wealthy corporations are able to sway politicians to act in ways contrary

to the desires of the majority

D) people are aware that their votes will not change the political outcome since these

outcomes are predetermined by a group of influential politicians

If, at the firm’s projected sales level, the marginal cost is $40, the average cost is $50

and the markup is 30 percent, then its selling price is

A) $40.

B) $50.

C) $52.

D) $65.

An external cost is created when you

A) graduate from college.

B) buy flowers for your mother on Mother’s Day.

C) litter on the side of the road.

D) buy a sandwich for lunch.

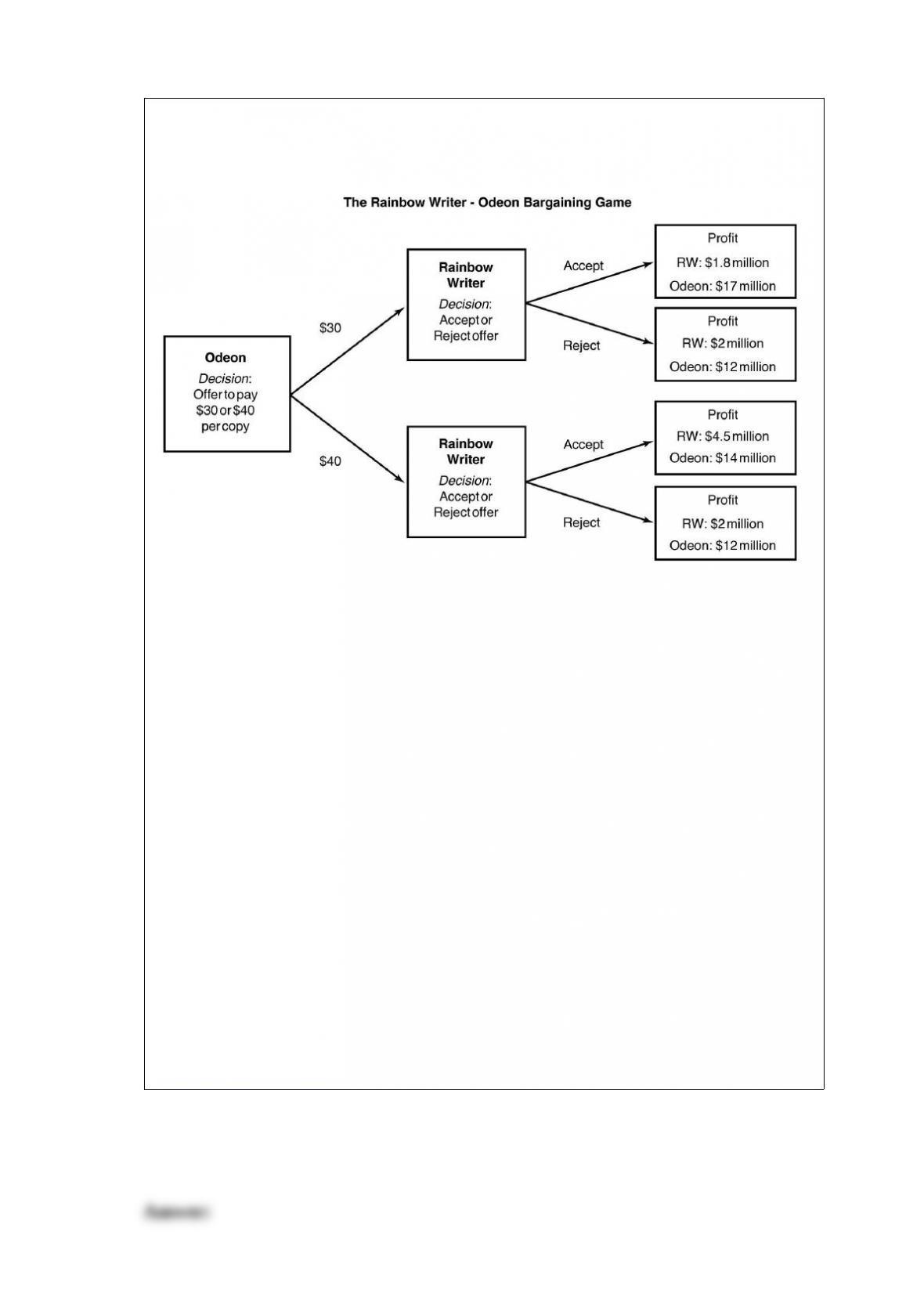

Figure 14-3

Rainbow Writer (RW) is a small online company selling a highly rated software

package for engraving words onto objects produced by 3D printers. The firm currently

earns a profit of $2 million per year selling its package exclusively on its Website.

Odeon, the producer of the most popular 3D printers has expressed interest in bundling

Rainbow Writer’s product with its printers. Odeon expects that bundling would further

boost its sales and allow it to sell its printers at a higher price, thus raising its profits

beyond its current profit of $12 million. Figure 14.3 shows the decision tree for the

Rainbow Writer-Odeon bargaining game.

Refer to Figure 14-3. What is the equilibrium outcome in this game and is this a

subgame-perfect equilibrium?

A) Odeon’s offer of $40 per copy of the software package is accepted and this is a

subgame-perfect equilibrium.

B) In the equilibrium, Odeon offers $40 per copy of the software package and is

accepted but this is not a subgame-perfect equilibrium.

C) In the equilibrium, Odeon offers $30 per copy of the software package and is

rejected, and this is a subgame-perfect equilibrium.

D) There is no equilibrium in this game.

Standard economic theory asserts that sunk costs are irrelevant in making economic

decisions, yet studies conducted by behavioral economists reveal that sunk costs often

affect economic decisions. Which of the following could explain this observation?

A) People measure the value of a good in terms of its purchase price.

B) Even though sunk costs cannot be recovered, it has been incurred and therefore

should be treated as part of the product’s value.

C) If consumers maximize their utility, it makes sense to consider the full purchase

price of a product in their consumption decisions.

D) Sunk costs have a higher opportunity cost than costs that can be recovered.

Excess capacity is a characteristic of monopolistically competitive firms. What does

excess capacity mean?

A) It means that firms do not produce the output level that corresponds to the minimum

point on their average total cost curves.

B) It means that firms hire more than the minimum number of workers needed to

produce the profit-maximizing level of output.

C) It means that firms produce with inefficient combinations of resources.

D) It means that firms build plants that are not large enough to achieve minimum

efficient scale.

Which of the following describes how output changes in the short run? Because of

specialization and the division of labor, as more workers are hired

A) output will first increase at an increasing rate, then output will increase at a

decreasing rate.

B) output will first decrease at an increasing rate, then increase at a decreasing rate.

C) the marginal product of labor will first decrease, then increase at a decreasing rate.

D) the marginal product of labor will first be negative and then will be positive.

If a firm lowered the price of the product it sells and found that total revenue did not

change, then the demand for its product is

A) perfectly inelastic.

B) perfectly elastic.

C) unit elastic.

D) relatively elastic.

You have just opened a new Italian restaurant in your hometown where there are three

other Italian restaurants. Your restaurant is doing a brisk business and you attribute your

success to your distinctive northern Italian cuisine using locally grown organic produce.

What is likely to happen to your business in the long run?

A) Your competitors are likely to change their menus to make their products more

similar to yours.

B) Your success will invite others to open competing restaurants and ultimately your

profits will be driven to zero.

C) If your success continues, you will be likely to establish a franchise and expand your

market size.

D) If you continue to maintain consistent quality, you will be able to earn profits

indefinitely.

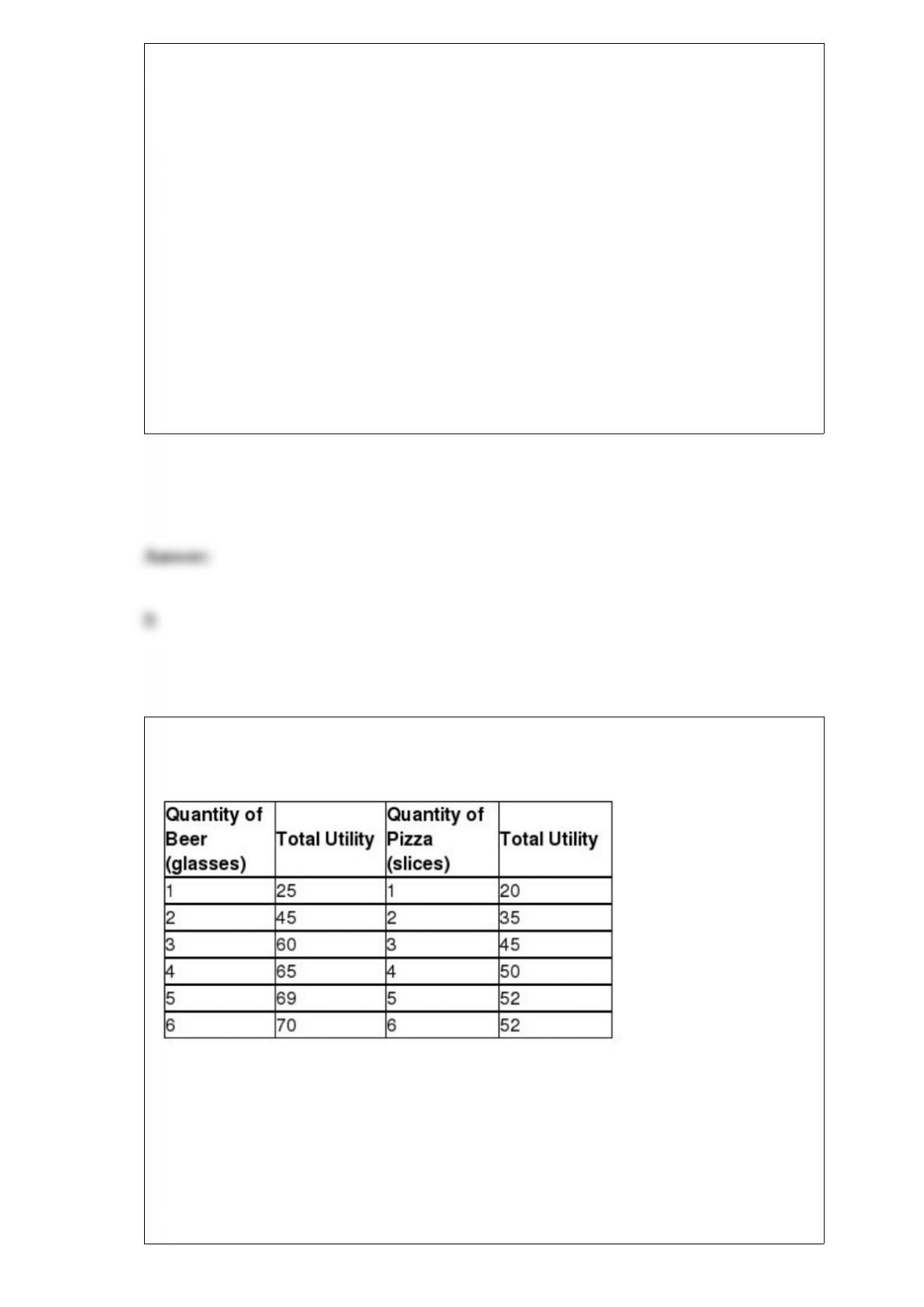

Table 10-7

Table 10-7 shows Antonio’s utility from beer and pizza.

Refer to Table 10-7. Suppose Antonio has $10 to spend and the price of beer = $2 per

glass and the price of pizza = $2 per slice. How many of each good will he consume

when he maximizes his utility?

A) 2 glasses of beer, 1 slice of pizza

B) 2 glasses of beer, 3 slices of pizza

C) 3 glasses of beer, 2 slices of pizza

D) 4 glasses of beer, 5 slices of pizza

Suppose the labor market is in equilibrium. Which of the following statements is false?

A) The equilibrium wage rate is equal to the marginal revenue product of labor.

B) At the equilibrium wage, the quantity of labor demanded equals the quantity of labor

supplied.

C) Some workers will earn more than the equilibrium wage.

D) At the equilibrium wage, the demand for labor is equal to the supply of labor.

Cost-price pricing typically does not result in profit-maximization. As a result,

economists have two views of cost-plus pricing. One of these views is

A) cost-plus pricing is more likely to lead to profit-maximization for large firms than

for small firms.

B) cost-plus pricing is a good way to approximate the profit-maximizing price when

marginal revenue or marginal cost is difficult to determine.

C) cost-plus pricing is more likely to lead to profit-maximization for monopolistically

competitive firms than for oligopoly firms.

D) cost-plus pricing is more likely to result in profit-maximization the more elastic the

firm’s demand curve is.

A demand curve shows

A) the willingness of consumers to buy a product at different prices.

B) the willingness of consumers to substitute one product for another product.

C) the relationship between the price of a product and the demand for the product.

D) the relationship between the price of a product and the total benefit consumers

receive from the product.

For the monopolistically competitive firm

A) Price (P) = Marginal Revenue (MR) = Average Revenue (AR).

B) P = MR > AR.

C) P = AR > MR.

D) P > MR = AR.

Describe the main factors economists believe cause inequality of income.

What is perfect price discrimination and why do economists believe that no firm is able

to practice perfect price discrimination?

What are the key factors that determine the profitability of a firm in a monopolistically

competitive market?

Goods differ on the basis of whether their consumption is rival and excludable. Explain

the terms “rivalry” and “excludability” as they are used to define goods. List the four

categories of goods, and define these categories in terms of rivalry and excludability.

Suppose the current price of oil is $90 a barrel and the quantity supplied is 800 million

barrels per day. If the price elasticity of supply for oil in the short run is estimated at

0.5, use the midpoint formula to calculate the percentage change in quantity supplied

when the price of oil rises to $98 a barrel.

What is the difference between between total costs, variable costs, and fixed costs?

What are the four main sources of comparative advantage? Briefly explain each source

and provide examples.

What is the difference between ‘shutting down temporarily” and “exiting the industry”?

What is a private cost of production? What is a social cost of production? When is the

private cost of production equal to the social cost of production?

Explain the differences between total revenue, average revenue, and marginal revenue.

What shape does a production possibilities frontier take if it displays increasing

opportunity costs? What shape does a production possibilities frontier take if it displays

constant opportunity costs? Which shape is most common in production situations?

What is an externality?

How does the demand curve for an oligopoly firm differ from the demand curves for

firms in competitive market structures?

What is an isoquant? What is the slope of an isoquant?

What is opportunity cost?

What is economic growth?

Define a partnership.

Explain the economic concept of price elasticity of supply. How is price elasticity of

supply calculated?

What is the difference between the voting paradox and the Arrow impossibility

theorem?