Chapter 9

The Case for International Diversification

Note: In the sixth edition of Global Investments, the exchange rate quotation symbols differ from previous

editions. We adopted the convention that the first currency is the quoted currency in terms of units

of the second currency.

For example, €:$ = 1.4 indicates that one euro is priced at 1.4 dollars. In previous editions we used

the reversed convention $/€ = 1.4, meaning 1.4 dollars per euro.

All problems in this test bank still use the old convention and have not been adapted to reflect the

new quotation symbols used in the 6th edition.

◼ Questions and Problems

1. The annualized performance, in U.S. dollars, of the United States and EAFE stock indices are:

ReturnUS = 12%

US = 15.5%

ReturnEAFE = 14.6%

EAFE = 18.2%

Correlation = 0.47

a. What would be the return and risk of a portfolio invested half in the U.S. market and half in the

EAFE index?

b. What if the correlation increases to 0.6?

Solution

2. The annualized performance, in U.S. dollars, of the U.S. and European stock indices are:

ReturnUS = 10%

US = 16%

Returneurope = 11%

europe =18%

Correlation = 0.60

106 Solnik/McLeavey • Global Investments, Sixth Edition

a. What would be the return and risk of a portfolio invested half in the U.S. market and half in the

European index?

b. What if the correlation increases to 0.8?

3. Here are the expected returns and risks of two assets:

E(R1) = 10%

1 = 16%

E(R2) = 14%

2 = 16%

a. Assume a correlation of 0.5 and draw all the portfolios made up of the two assets in an Expected

Return/Risk graph.

b. Same question assuming successively a correlation of −1, 0, and +1.

c. Looking at the four graphs, what do you conclude about the importance of correlation in

risk-reduction?

Solution

Chapter 9 The Case for International Diversification 107

108 Solnik/McLeavey • Global Investments, Sixth Edition

4. Try to find some reasons why:

a. Stock and bond markets should be strongly correlated and,

b. Stock and bond markets should be weakly correlated.

5. The French stock market has a sigma of 20%, when computed in euros. The U.S. stock market has a

sigma of 16% in US$ and the €/US$ exchange rate has a sigma of 6%.

a. Assuming that the correlation between stock market and currency movements is zero, what is the

sigma of the U.S. stock market when expressed in €.

b. Using this number, calculate the sigma, in €, of a portfolio made up of 50% of French stocks and

50% of U.S. stocks (zero-correlation between the two markets).

Solution:

6. The Japanese stock market has a sigma of 18%, when computed in yen. The U.S. stock market has a

sigma of 17% in US$ and the US$/¥ exchange rate has a sigma of 6%. The correlation between the

Japanese stock market and $/¥ currency movements is −0.1; in other words, the Japanese stock

market tends to go up when the yen goes down. The correlation between the Japanese and U.S.

stock markets is equal to 0.4, measured either in local currency of in dollars.

a. What is the sigma of the Japanese market when expressed in dollars?

b. Using this number, calculate the sigma, in dollars, of a portfolio made up of 50% of Japanese

stocks and 50% of U.S. stocks.

Chapter 9 The Case for International Diversification 109

Solution

7. Assume that the domestic volatility (standard deviation in yen) of the Japanese stock market is 18%.

The volatility of the yen against the U.S. dollar is 6%.

a. What would the dollar volatility of the Japanese stock market be for a U.S. investor if the

correlation between the Japanese stock market returns and exchange rate movements were zero?

b. Suppose the dollar volatility of the Japanese stock market is 18.4%, what can you conclude about

the correlation between the Japanese stock market movements and exchange rate movements?

Solution

8. Assume that the domestic volatility (standard deviation in yen) of the Japanese bond market is 8%.

The volatility of the yen against the U.S. dollar is 6%.

a. What would the dollar volatility of the Japanese bond market be for a U.S. investor if the

correlation between the Japanese stock market returns and exchange rate movements were zero?

b. Suppose the dollar volatility of the Japanese stock market is 11.35%, what can you conclude

about the correlation between the Japanese bond market movements and exchange rate

movements?

Solution

9. In 1994, the United States was experiencing a fairly strong economic recovery, ahead of other

nations. Fears of an overheating economy led to sudden inflationary fears for the next few years.

a. Would you expect U.S. interest rates to rise or drop?

b. Would you expect the dollar to depreciate or appreciate?

c. Would you expect a foreign bond portfolio to be a good investment compared to a U.S. dollar

portfolio under this scenario?

10. Suppose that you overheard the following statements at a conference for institutional investors:

(A German national): “My money manager knows the German firms very well; why should I

bother to invest in French and American shares? I am not familiar with their names or their

operations, and I will have to pay much higher costs to buy them.”

(A French national): “Why should I buy German and American shares? The foreign brokers will

give preferential treatment to their domestic clients, and I am going to get a lousy deal in terms of

prices and costs. Furthermore, I can’t read the financial statements of these companies, as they

are written in German or English, and with different accounting methods.”

(An American national): “I can’t even pronounce the names of these foreign companies; how

could I defend investing abroad in front of my board of trustees? By the way, what is the capital

of Switzerland: Geneva or Zurich?”

How would you try to convince these people to diversify their portfolios if you were the marketing

representative of a big international money manager?

Chapter 9 The Case for International Diversification 111

11. Assume that the domestic and foreign assets have standard deviations of

d = 16% and

f = 19%,

respectively, with a correlation of

df = 0.6. The risk-free rate is equal to 5% in both countries.

a. The expected returns of the domestic and foreign assets are both equal to 10%, E(Rd) = E(Rf) =

10%. Calculate the Sharpe ratios for the domestic asset, the foreign asset, and an internationally-

diversified portfolio equally invested in the domestic and foreign assets. What do you conclude?

b. Assume now that the expected return on the foreign asset is higher than on the domestic asset,

E(Rd) = 10% but E(Rf) =12%. Calculate the Sharpe ratio for an internationally diversified

portfolio equally invested in the domestic and foreign assets, and compare your findings to those

in Question (a).

Solution

12. You consider investing in an emerging market. Its stock market volatility (standard deviation of

returns measured in U.S. dollars) is 25%. The volatility of the World index of developed markets is

15%. The correlation between the emerging market and the World index is 0.2.

a. What would be the volatility of a portfolio invested 95% in the World index and 5% in this

emerging market?

b. Compare the result found in the previous question with the volatility of the World index and give

an intuitive explanation.

112 Solnik/McLeavey • Global Investments, Sixth Edition

Solution

13. You consider investing in some emerging country. Its recent economic growth rate is around 7%,

well above the average growth rate of developed countries estimated at 2% by the OECD. Its annual

inflation rate is around 10%, well above the average inflation rate of developed countries estimated at

2% by the OECD. The currency of the emerging country has been depreciating at an annual rate of

around 8% against major currencies. While the volatility of the World stock index (standard deviation

of dollar returns) is around 15%, the stock market of this emerging country has a volatility of 25%.

The correlation of this emerging stock market with the World index is only 0.2.

a. Are the high inflation rate and weak currency sufficient reasons to avoid investing in this

emerging country?

b. Is the high volatility of the local market a sufficient reason to avoid investing in this emerging

country?

c. Suggest why you would consider investing in this emerging country.

Solution

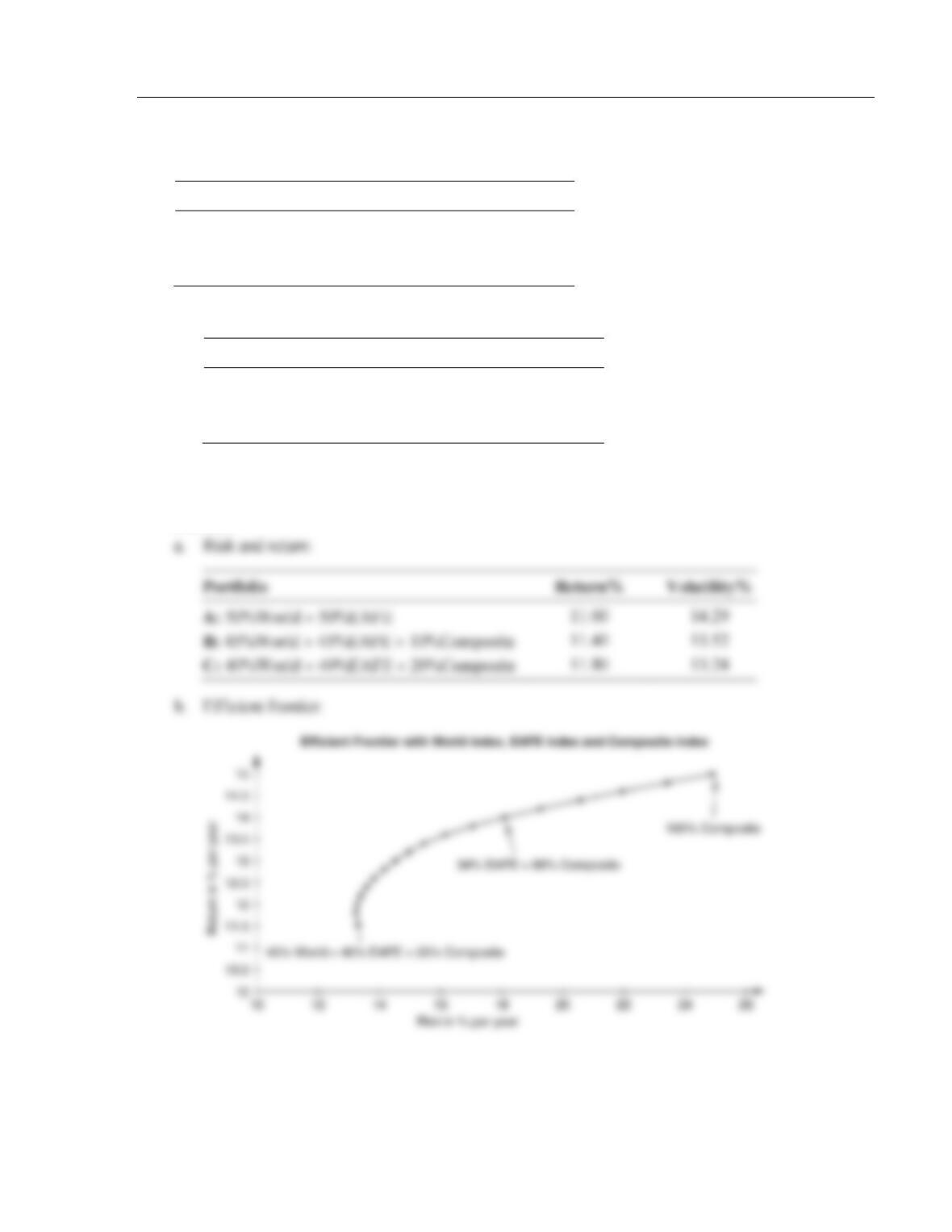

14. You have collected some risk and return estimates for various market indexes. These indexes are the

World stock market index of developed markets, the Morgan Stanley Capital International (MSCI)

Europe, Australasia and Far East (EAFE) index, and the International Finance Corporation (IFC)

Composite index of emerging markets. Here are some risk and return estimates for the future:

Market

Return

Risk

World

10%

16%

EAFE

12%

17%

Composite

15%

25%

Chapter 9 The Case for International Diversification 113

All return and risk measures are calculated in U.S. dollars and are expressed in % per year. The

correlation matrix is given below:

World

EAFE

Composite

World

1.0

0.5

0.2

EAFE

0.5

1.0

0.1

Composite

0.2

0.1

1.0

a. Calculate the return and risk of a portfolio invested in the following proportions:

Portfolio

World

EAFE

Composite

A

50%

50%

0%

B

45%

45%

10%

C

40%

40%

20%

b. Try to derive some estimate of the efficient frontier obtained by using these three indexes

(no short sales are allowed).

Solution

Volatility%

114 Solnik/McLeavey • Global Investments, Sixth Edition

15. The currencies of several emerging countries depreciate at a rapid pace. Does it imply that you should

not invest in their stock markets? For example, the Polish zloty went from 15,767 to 21,444 zlotys per

U.S. dollar in 1993. The Polish stock market went from 1,040 to 12,439 during the same period.

Guess why the zloty depreciated.

16. You consider investing in four very volatile emerging markets. These are small countries just opening

up to foreign investment. You spread your money equally across them. After a year, the following

observations are made on the performance of each market:

Country

Return in

Local Currency

Currency

Depreciation

Comment

A

400%

20%

High inflation, high growth

B

60%

10%

C

0

40%

High inflation, low growth

D

–100%

80%

Foreigners got expropriated

Chapter 9 The Case for International Diversification 115

a. Calculate the return, in dollars, on each market. The currency depreciation is equal to the drop in

the dollar value of one unit of local currency. For example, if the peso moves from 1 dollar per

peso to 0.8 dollar per peso, the depreciation of the peso is measured as 20%.

b. What is the return on a portfolio equally invested in each market?

17. Project: Take monthly values of the stock indexes of a selected group of developed and emerging

stock markets over a period of ten years.

a. Calculate the correlation of returns among them, in local currency.

b. Break the period into two five-year subperiods and compare the calculated correlations over the

two subperiods.

c. Multiply the stock prices by the exchange rate and calculate the correlation of U.S. dollar returns.

Do the figures change dramatically for developed markets? Do the figures change dramatically

for emerging markets?

d. Focus on emerging markets experiencing high inflation. Why is it important to perform the

calculations using a single-base currency when looking at countries with high inflation from a

foreign viewpoint?