e.

Increase price and hold output constant.

83. According to the information provided in Exhibit 9-7, if the Rudd Ice Company was a monopoly and

is currently charging a price of $6, what would you advise Rudd to do?

a.

Stay where he is currently operating because he is charging the profit maximizing price.

b.

Increase price and decrease output.

c.

Decrease price and increase output.

d.

Increase output and hold price constant.

e.

Increase price and hold output constant.

84. As shown in Exhibit 9-7, in the short run, the monopoly will:

a.

earn an hourly profit of $240.

b.

earn an hourly profit of $80.

c.

break even (i.e., earn zero economic profit).

d.

suffer an hourly loss of $160.

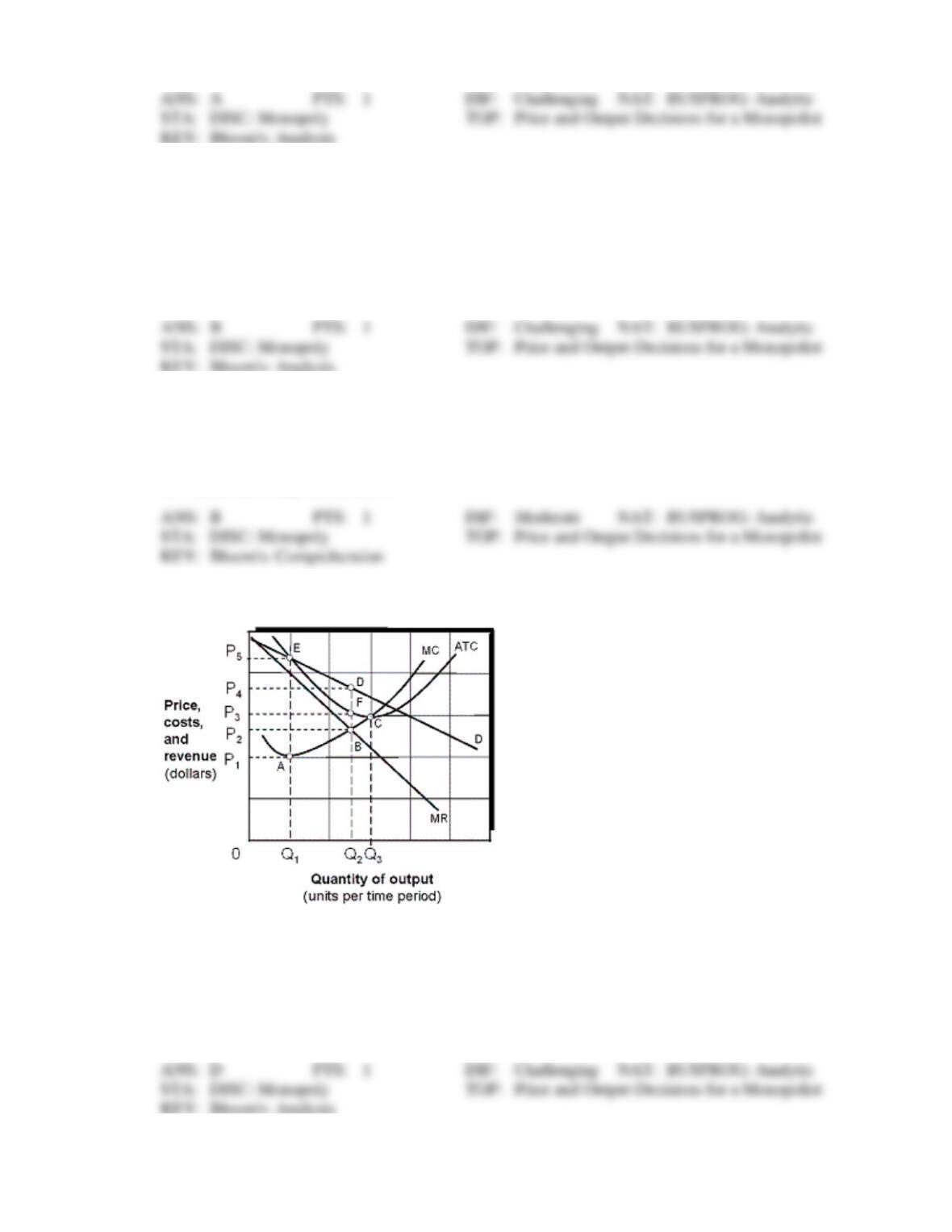

Exhibit 9-8 Profit maximizing for a monopolist

85. As shown in Exhibit 9-8, the profit-maximizing price for the monopolist is:

a.

OP1.

b.

OP2.

c.

OP3.

d.

OP4.

e.

OP5.

86. As shown in Exhibit 9-8, the monopolist’s total cost is which of the following areas?

a.

P1AEP5.

b.

P2BDP4.

c.

P3CDP5.

d.

P4DEP5.

e.

None of these.

87. The profit-maximizing output for the monopolist in Exhibit 9-8 is:

a.

zero.

c.

OQ2

b.

OQ1.

d.

OQ3.

88. As shown in Exhibit 9-8, if the monopolist produces the profit-maximizing output, total revenue is the

rectangular area:

a.

OQAP1.

c.

OQ3CP3.

b.

OQ2BP2.

d.

OQ2DP4.

89. As shown in Exhibit 9-8, the monopolist’s profit maximizing price-quantity point is:

a.

A

b.

B

c.

C

d.

D

e.

E

90. At the level of output where the marginal cost and marginal revenue curves intersect, a monopolist’s

demand curve passes above its average total cost curve. The firm will:

a.

be able to make a pure economic profit.

b.

stay in operation in the short-run, but shut down.

c.

shut down in the short-run.

d.

increase its price.

91. If the average total cost curve is always above the demand curve for a monopolist:

a.

the profits of the monopolist will be large.

b.

the monopolist must be producing inefficiently.

c.

the monopolist will suffer economic losses.

d.

entry will occur, forcing the monopolist to reduce price and expand output.

92. Suppose a monopolist’s demand curve lies below its average variable cost curve. The firm will:

a.

earn an economic profit.

c.

shut down.

b.

stay in operation in the short-run.

d.

none of these.

93. Suppose a monopolist charges a price corresponding to the intersection of the marginal cost and

marginal revenue curves. If this price is between its average variable cost and average total cost

curves, the firm will:

a.

earn an economic profit.

b.

stay in operation in the short-run, but shut down in the long run if demand remains the

same.

c.

shut down.

d.

none of these.

94. A monopolist will operate in the short run if which of the following is above average variable cost?

a.

Marginal cost.

c.

Price.

b.

Marginal revenue.

d.

All of these.

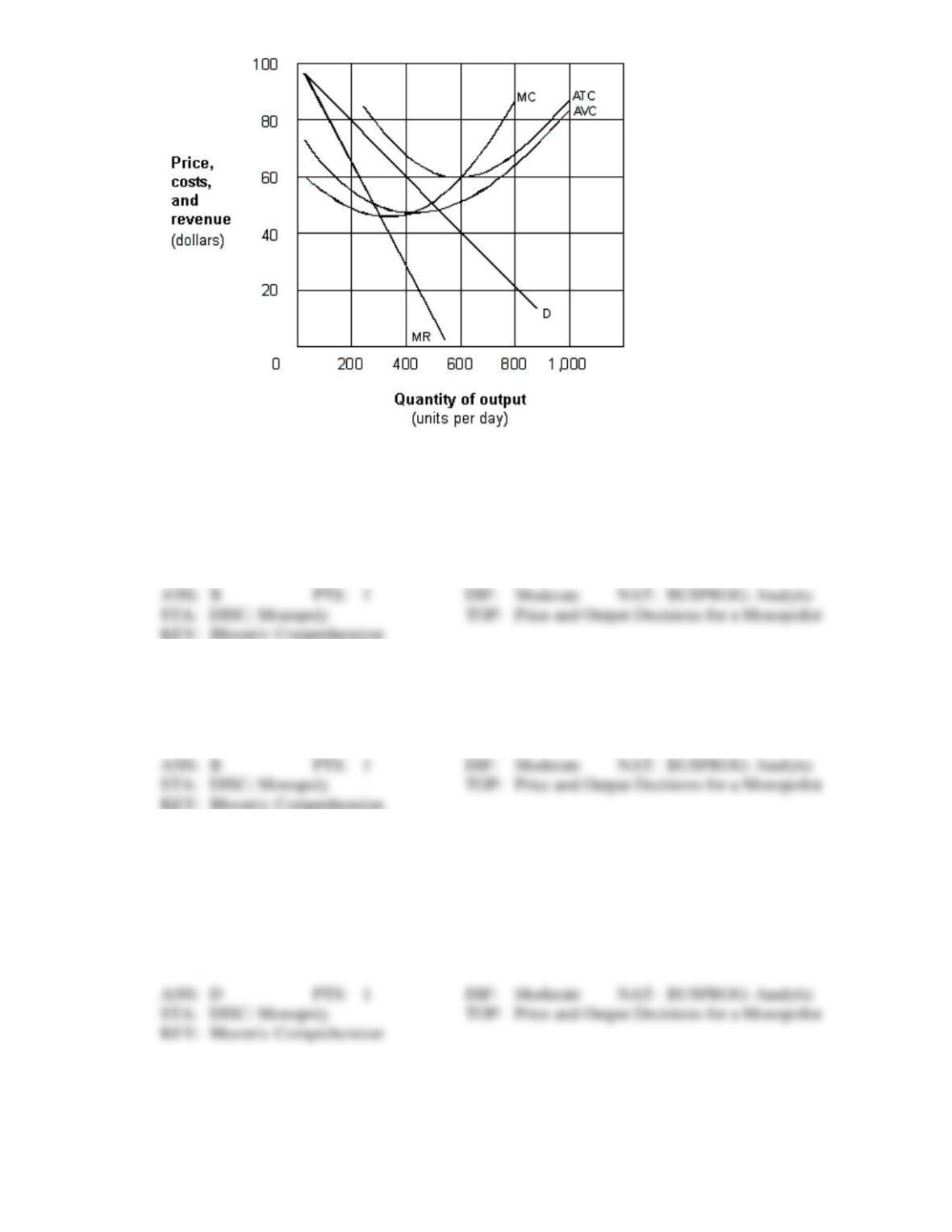

Exhibit 9-9 A monopolist

95. In Exhibit 9-9, the profit-maximizing or loss-minimizing output for the monopolist is:

a.

200 units per day.

b.

300 units per day.

c.

400 units per day.

d.

500 units per day.

e.

600 units per day.

96. In Exhibit 9-9, at the profit-maximizing or loss-minimizing output, the monopolist‘s total economic

profit is:

a.

positive.

c.

zero.

b.

negative.

d.

minimum.

97. In Exhibit 9-9, the monopolist would charge which of the following prices to maximize profit or

minimize its loss?

a.

$20.

b.

$40.

c.

$60.

d.

$70.

e.

$100.

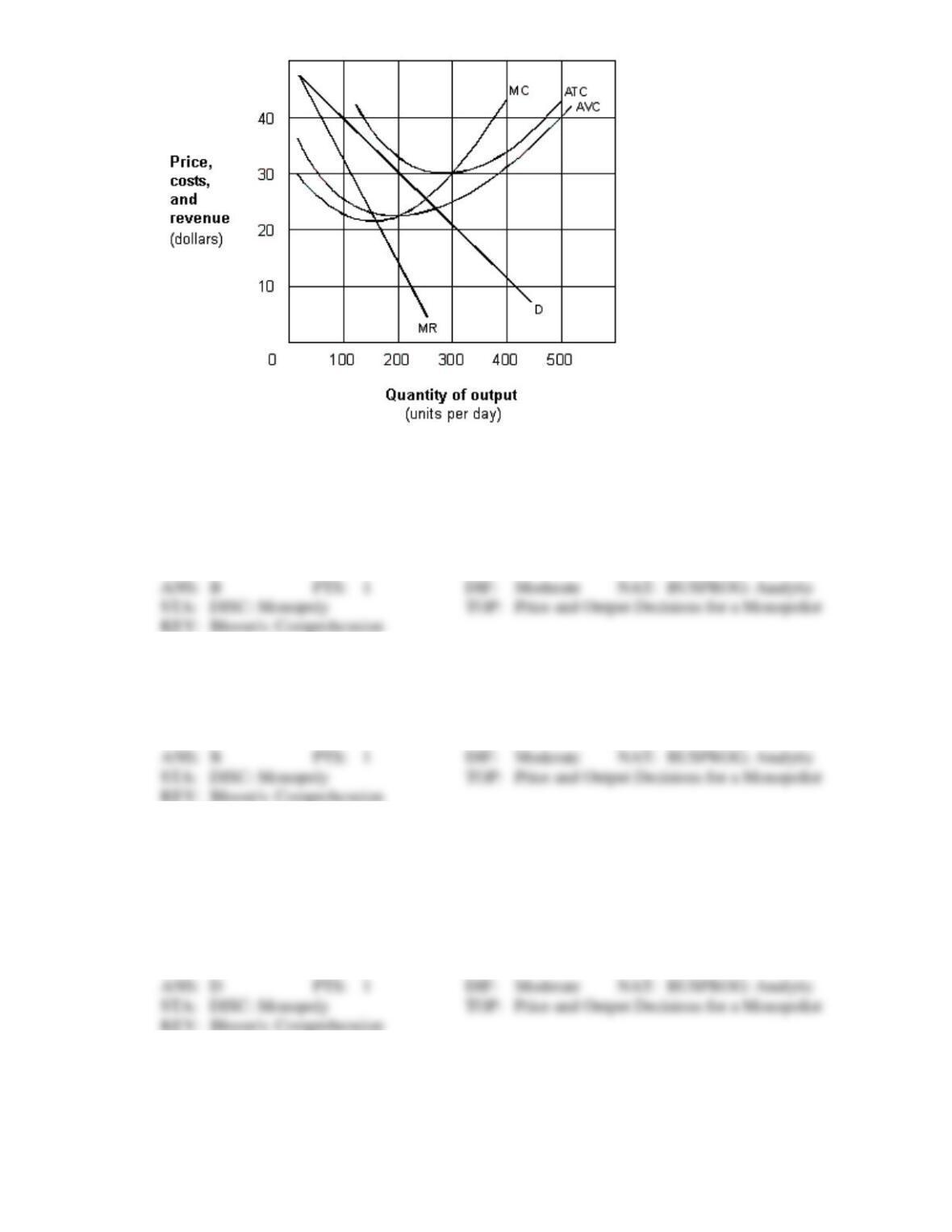

Exhibit 9-10 A monopolist

98. In Exhibit 9-10, the profit-maximizing or loss-minimizing output for the monopolist is:

a.

100 units per day.

b.

150 units per day.

c.

200 units per day.

d.

250 units per day.

e.

300 units per day.

99. In Exhibit 9-10, at the profit-maximizing or loss-minimizing output, the monopolist’s total economic

profit is:

a.

positive.

c.

zero.

b.

negative.

d.

minimum.

100. In Exhibit 9-10, the monopolist would charge which of the following prices to maximize profit or

minimize its loss?

a.

$10.

b.

$20.

c.

$30.

d.

$35.

e.

$50.

101. Which of the following statements best describes the price, output, and profit conditions of monopoly?

a.

Price will equal marginal cost at the profit-maximizing level of output and profits will be

positive in the long run.

b.

Price will always equal average variable cost in the short-run and either profits or losses

may result in the long run.

c.

In the long run, positive economic profit will be eliminated.

d.

None of these.

102. Which of the following is true for the monopolist?

a.

Marginal revenue is less than the price charged.

b.

Economic profit is possible in the long-run.

c.

Profit maximizing or loss minimizing occurs when marginal revenue equals marginal cost.

d.

All of the above.

e.

None of the above.

103. Which of the following correctly describes price discrimination?

a.

Selling different products to different people for the same price.

b.

Selling different products to identical people for different prices.

c.

Selling the same product to different people for different prices.

d.

Selling the same product to the same person for the same price.

104. Price discrimination requires:

a.

a firm to be a competitive firm.

b.

a firm to be able to segment its customers based on different price elasticities of demand.

c.

arbitrage.

d.

that the product can be easily resold.

105. Price discrimination occurs when:

a.

firms maximize their profit by setting price equal to marginal cost.

b.

a seller charges different prices to different consumers of the same product or service.

c.

a seller charges the same price to consumers of a different product or service.

d.

a seller charges different prices to consumers, discriminating by race or gender of the

consumer.

106. The strategy underlying price discrimination is to:

a.

charge higher prices to customers who have better access to substitutes.

b.

charge everyone the same price but limit the quantity they are allowed to buy.

c.

increase total revenue by charging higher prices to those with the most inelastic demand

for the product and lower prices to those with the most elastic demand.

d.

reduce per-unit costs by charging higher prices to those with the most elastic demand and

lower prices to those with the most inelastic demand.

107. For a monopolist to practice price discrimination, one necessary condition is that the product offered

for sale must be:

a.

high quality.

c.

cheap.

b.

expensive.

d.

impossible or difficult to resell.

108. Which of the following is a necessary condition for price discrimination?

a.

The seller must be able to divide the markets according to the different price elasticities of

demand.

b.

It must be difficult for one buyer to resell to another buyer.

c.

Both a and b.

d.

Neither a nor b.

109. The act of buying a commodity in one market at a lower price and selling it in another market at a

higher price is known as:

a.

buying long.

c.

a tariff.

b.

selling short.

d.

arbitrage.

110. One necessary condition for effective price discrimination is:

a.

identical tastes among buyers.

b.

difference in the price elasticity of demand among buyers.

c.

a single, homogeneous market.

d.

two or more markets with easy resale of products between them.

111. An example of price discrimination is the price charged for:

a.

an economics textbook at a campus bookstore.

b.

gasoline.

c.

theater tickets that offer lower prices for children.

d.

a postage stamp.

112. An example of price discrimination is the price charged for:

a.

a postage stamp.

b.

theater tickets that offer lower prices for children.

c.

an economics textbook at a campus bookstore.

d.

Any of these.

113. An example of price discrimination is the price charged for:

a.

troll dolls.

c.

textbooks.

b.

college admission.

d.

diamonds.

114. For a monopolist to practice effective price discrimination, one necessary condition is:

a.

identical price elasticity among groups of buyers.

b.

differences in the price elasticity of demand among groups of buyers.

c.

that the product is homogeneous market.

d.

none of these.

115. A price-discriminating monopoly charges the lowest price to the group that:

a.

has the most elastic demand.

c.

engages in the most arbitrage.

b.

purchases the largest quantity.

d.

is least responsive to price changes.

116. For a monopoly to successfully price discriminate, its customers must:

a.

feel that the product is a necessity.

c.

be unable to resell the product.

b.

have identical demands.

d.

actively engage in arbitrage.

117. One of the necessary conditions for price discrimination to occur is that:

a.

buyers in different markets have different elasticities of demand.

b.

the demand curve is upward sloping.

c.

buyers must be allowed to resell the good at a higher price elsewhere.

d.

all of these are necessary for price discrimination to occur.

118. Which of the following represents an arbitrage transaction?

a.

Traders buy silks where they are abundant and cheap, and haul them along a trail to

another place where they would be quite scarce and valued.

b.

A trader buys a block of government bonds in one market where it is temporarily priced

below where it can be immediately resold in a different market.

c.

Someone buys a block of Final Four tickets and scalp them at the game.

d.

A senior citizen buys a block of theater tickets at a senior discount and scalps them to

teenagers behind the theater.

e.

All of the above are example of arbitrage.

119. ____ is the act of buying a commodity in one market at a lower price and selling it in another market at

a higher price.

a.

Buying short.

c.

Tariffing.

b.

Discounting.

d.

Arbitrage.

120. Which of the following best explains an economic criticism of unregulated monopolists?

a.

Monopolists do not try to minimize their costs of production.

b.

Monopolists produce where marginal revenue is greater than marginal costs.

c.

Monopolists attempt to produce too many products, and as a result, their prices are high,

and consumer’s waste time trying to choose between too many options.

d.

Monopolists restrict output, and as a result, they fail to produce units that are valued more

than the marginal cost of producing them.

121. Because monopolists are protected by high barriers to entry, they:

a.

may be able to earn long-run economic profits.

b.

will not minimize the per-unit cost of producing their output.

c.

will price their product at the highest possible price.

d.

seek economic profit; however, they are not able to earn it in the long run.

122. Which of the following statements accurately describes a difference between a firm that is a

monopolist and one that is a competitive price taker?

a.

Marginal revenue and market price are equal for the competitive price taker but not for the

monopolist.

b.

The monopolist does not always produce the output that equates marginal cost and

marginal revenue; the competitive price taker does.

c.

The monopolist charges the highest price possible; the competitive price taker charges a

price equal to its per-unit cost.

d.

A monopolist can earn economic profit in the short run; a competitive price taker cannot.

123. Under both perfect competition and monopoly, a firm:

a.

is a price taker.

b.

is a price maker.

c.

will shut down in the short-run if price falls short of average total cost.

d.

always earns a pure economic profit.

e.

sets marginal cost equal to marginal revenue.

124. Which of the following is true about a monopoly?

a.

A monopoly charges a higher price and produces a lower output level than if the market

were competitive.

b.

A monopoly is guaranteed an economic profit.

c.

A monopoly charges the highest possible price.

d.

A monopoly will shut down whenever losses are incurred.

e.

All of these.

125. A monopoly sets a market price that is higher than the marginal cost of production. This fact implies

that a monopoly’s allocation of resources is:

a.

unfair.

c.

discriminatory.

b.

inefficient.

d.

excessive.

126. Under both perfect competition and monopoly, a firm:

a.

is a price taker.

b.

maximizes profit by setting marginal cost equal to marginal revenue.

c.

will shut down in the short-run if price falls short of average total cost.

d.

always earns a pure economic profit.

127. In contrast to a perfectly competitive firm, a monopolist operates in the long run at a quantity of output

at which:

a.

P = MC.

c.

P = ATC.

b.

MR = MC.

d.

P > MR.

128. Compared to a perfectly competitive firm, a monopolist:

a.

charges a higher price.

b.

produces lower output.

c.

fails to achieve an efficient allocation of resources.

d.

all of these.

129. In contrast to a perfectly competitive firm, a monopolist earns:

a.

negative economic profit in the long run.

b.

zero economic profit in the long run.

c.

positive economic profit in the long run.

d.

positive economic profit in the short run.

130. Monopolists are criticized because they are inefficient. What is meant by this statement?

a.

Monopolists charge too high a price.

b.

Monopolists don’t innovate enough to control pollution.

c.

Monopolists produce a large quantity of waste.

d.

Monopolists usually don’t produce at the minimum of the ATC.

e.

Monopolists could use their resources better elsewhere.

131. The monopolist, unlike the perfectly competitive firm, can continue to earn an economic profit in the

long run because of:

a.

collusive agreements with competitors.

b.

price leadership.

c.

cartels.

d.

a dominant firm.

e.

extremely high barriers to entry.

132. Suppose a monopolist and a perfectly competitive firm have the same cost curves. The monopolistic

firm would:

a.

charge a lower price than the perfectly competitive firm.

b.

charge a higher price than the perfectly competitive firm.

c.

charge the same price as the perfectly competitive firm.

d.

refuse to operate in the short run unless an economic profit could be made.

e.

refuse to operate in the short run if an economic loss was present.

133. Compared to a perfectly competitive firm with the same cost structure, a monopoly firm will charge a:

a.

higher price and sell more.

b.

lower price and sell more.

c.

higher price and sell less.

d.

lower price and sell less.

e.

similar price and sell the same.

134. If pizza used to be produced in a perfectly competitive market, and now the pizza market has become a

monopoly, we can expect:

a.

less pizza to be sold at a higher price.

b.

more pizza to be sold at a higher price.

c.

less pizza to be sold at a lower price.

d.

more pizza to be sold at a lower price.

e.

the same amount of pizza to be sold at the same price.

135. Compared to a perfectly competitive industry, a monopolist with the same marginal cost and demand

curve will charge:

a.

a higher price and produce a higher volume of output.

b.

a lower price and produce a higher volume of output.

c.

a lower price and produce a lower volume of output.

d.

a higher price and produce a lower volume of output.

e.

the same price and produce the same volume of output.

TRUE/FALSE

1. The two theoretical extremes of the market structure spectrum are occupied at one end by perfect

competition and on the other end by monopoly.

2. A monopoly market is characterized by a single seller of a product which has few, if any, suitable

substitutes.

3. A perfectly competitive firm is a price taker, but a monopoly is a price maker.

4. A monopolist is a price searcher because it has the ability to select the price along its demand curve of

its product.

5. A natural monopoly exists whenever economies of scale are very extensive.

6. In a natural monopoly, the long-run average cost curve declines and therefore average cost is lower

when there is only one seller.

7. Costs in a natural monopoly are lower because there is only one producer.

8. A natural monopoly maximizes profits at the point at which price equals minimum average total cost.

9. In order for a monopolist to earn an economic profit in short-run equilibrium, marginal revenue must

be equal to zero.

10. A monopolist maximizes total revenue.

11. A monopolist will charge a lower price and produce more output than if it was operating in a

competitive market.

12. The monopolist faces the market demand curve.

13. A monopolist always earns an economic profit.

14. A monopoly earns the most profit by charging a price where demand is inelastic.

15. A monopolist that maximizes total revenue earns maximum economic profit.

16. Regardless of the demand for its product, a monopolist will be able to earn positive economic profits.

17. In order for a monopolist to earn a pure economic profit in short-run equilibrium, price must exceed

average total cost.

18. To earn an economic profit in the short-run, a monopolist sets marginal revenue equal to zero.

19. A profit maximizing monopolist sets price and output so that it always operates on the elastic portion

of its straight-line demand curve when in equilibrium.

20. Pure economic profit must be at a maximum for a monopolist who has a level of output in which total

revenue is at a maximum.

21. A monopolist always selects a price on the elastic portion of its demand curve.

22. A monopolist will be able to earn positive pure economic profits regardless of the price elasticity of

demand.

23. A monopolist will charge a lower price and produce more output than if it was operating in a

competitive market.

24. The monopolist faces the market demand curve.

25. For a monopoly, price always equals marginal revenue.

26. Monopolies may earn economic losses in the long run.

27. An argument in favor of price discrimination is that this pricing strategy permits some consumers who

otherwise would be excluded from a market to buy a good or service.

28. A monopoly can successfully price discriminate as long as there are no close substitutes for its

product.

29. When a monopoly price discriminates, it charges the highest price to the group of buyers with the least

elastic demand.

30. Price discrimination often permits some consumers who otherwise would be excluded from a market

to buy a good or service.

ESSAY

1. What is a natural monopoly? Why is government justified in regulating a natural monopoly?

2. What is the shut-down rule for any firm?

3. Under what conditions might a monopoly lose money?

4. Why can a monopoly earn economic profits in the long run?

5. What are the conditions for price discrimination?