16. Speedy Printing purchased a new printing press for $80,000. It depreciates the press over a five-year

period, using the double-declining-balance method of depreciation. If the press has an $8,000

estimated residual value, calculate depreciation expense for each of the five years. (Show your work.)

17. Present two arguments in favor of the use of accelerated depreciation.

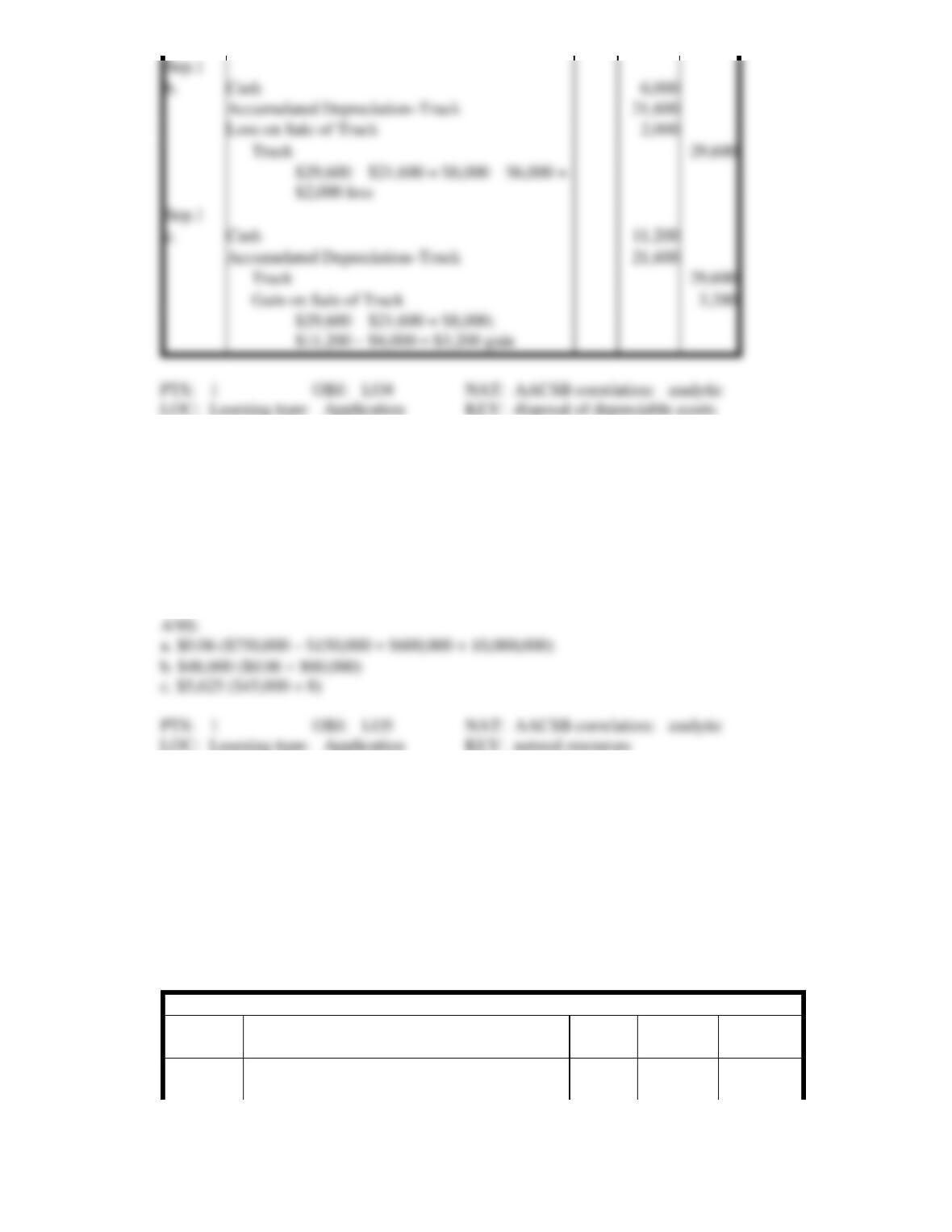

18. On November 1, 2008, Rob’s Auto Repair purchased diagnostic equipment for $18,000. The

equipment had an estimated residual value of $3,000 and a five-year life and was sold on May 1, 2010.

Assuming that the company depreciates the asset on a straight-line basis and reports on a calendar-year

basis, journalize the following independent transactions in the journal provided. (Omit explanations.)

a. The entry to update depreciation to May 1, 2010

b. The entry to record the sale for $15,000

c. The entry to record the sale instead for $11,000

d. The entry to record the sale instead for $13,500

General Journal

Page 1

Date

Description

Post.

Ref.

Debit

Credit

19. On October 1, 2008, Racie’s Auto Repair purchased diagnostic equipment for $13,600. The equipment

had an estimated residual value of $4,000 and an eight-year life and was sold on April 1, 2010.

Assuming that the company depreciates the asset on a straight-line basis and reports on a calendar-year

basis, journalize the following independent transactions in the journal provided. (Omit explanations.)

a. The entry to update depreciation to April 1, 2010

b. The entry to record the sale for $12,000

c. The entry to record the sale instead for $8,600

d. The entry to record the sale instead for $11,800

General Journal

Page 1

Date

Description

Post.

Ref.

Debit

Credit

[($13,600 – $4,000) ÷ 8 = $1,200 3/12]

20. Under what circumstances will a loss be recorded on the sale of equipment, and what effect will the

loss have on stockholders’ equity?

21. A truck that cost $20,000 and on which $8,000 of depreciation had been recorded was disposed of for

$11,600. Indicate whether a gain or loss should be recorded, and for what amount.

22. A machine that cost $36,000 and on which $26,000 of depreciation had been recorded was disposed of

for $10,400. Indicate whether a gain or a loss should be recorded, and for what amount.

23. In 20xx, Minneapolis Mining purchased a mineral deposit for $12,000,000. It is estimated that

15,000,000 tons can be extracted from the mine. Calculate depletion expense during 20xx when

700,000 tons were extracted and sold.

24. In 20xx, Massachusetts Mining purchased a mineral deposit for $36,000,000. It is estimated that

15,000,000 tons can be extracted from the mine. Calculate depletion expense during 20xx when

800,000 tons were extracted and sold.

25. For each of the following descriptions, provide the name of the intangible asset that is being described.

_______________ 1. Exclusive right to use a name or symbol

_______________ 2. Exclusive right to sell photographic reproductions of a painting

_______________ 3. Excess paid for a business over the fair market value of the net

assets purchased

_______________ 4. Long-term exclusive right to use certain property

_______________ 5. A right to an exclusive territory or market

_______________ 6. Exclusive right to use an invention to sell or manufacture a certain

product or use a specific process

ANS:

26. What is goodwill and when may it be recorded?

27. Indicate whether each of the following expenditures should be classified as land (L), land

improvements (LI), buildings (B), equipment (E), or none of these (X).

_____ 1. Clearing costs

_____ 2. Driveway cost

_____ 3. Computer installation cost

_____ 4. Architect’s fee for building plans

_____ 5. Surveying costs

_____ 6. Cost of assembly line trial run

_____ 7. Property taxes paid after purchase

_____ 8. Grading costs

_____ 9. Insurance and freight on computer purchased

_____ 10. Cost of lighting for parking lot

_____ 11. Landscaping cost

_____ 12. Material and labor costs incurred to construct factory

_____ 13. Cost of tearing down a warehouse on land just purchased

_____ 14. Utilities cost during first year

_____ 15. Cost of building wing

_____ 16. Sales tax on file cabinets purchased

_____ 17. Real estate commissions on land purchased

_____ 18. Contractor’s fee for building construction

_____ 19. Cost to put up chain-link fence

_____ 20. Accrued taxes on land purchased

ANS:

28. In the journal provided, prepare entries for the following independent transactions. (Omit

explanations.)

a. Purchased land and a building on the land for $960,000. The appraised values of the land and

building are $350,000 and $650,000, respectively.

b. Paid $5,000 for a sewage system, $15,000 for a parking lot, $1,000 to tear down a shack on land just

purchased, and $10,000 for a block wall.

c. Purchased a truck two years ago for $18,000 with an original six-year estimated useful life and

$3,000 residual value. After a full two years of use, revised the residual value to $4,000 and the useful

life to a total of seven years. Record depreciation for year 3, assuming the straight-line method.

d. Purchased a machine on May 1, 2010 (assume a calendar-year accounting period) for $15,000. The

machine has an estimated life of 10,000 hours and no salvage value. Record depreciation for 2010

under the production method, assuming that the machine was used 2,000 hours.

General Journal

Page 1

Date

Description

Post.

Ref.

Debit

Credit

29. On January 1, 2009, Pung Manufacturing Company purchased for $94,000 a machine that will produce

an estimated 75,000 units of Product X. The machine has an estimated useful life of five years and an

estimated residual value of $4,000. Calculate the following amounts: (a) the carrying value of the

machine after it has been used for three and one-half years, under the straight-line method; (b)

depreciation expense for 2010, under the production method (assume that 13,000 units were produced

that year); and (c) accumulated depreciation at the end of 2010, under the double-declining-balance

method. (Show your work.)

30. On January 1, 2005, Mal’s Pizza purchased for $24,000 a delivery truck that will be driven an

estimated 120,000 miles. The truck has an estimated useful life of eight years and an estimated

residual value of $6,000. Calculate the following amounts: (a) depreciation expense for 2010, under

the production method (assume that 17,000 miles were driven that year); (b) the accumulated

depreciation after the truck has been used for five and one-half years, under the straight-line method;

and (c) depreciation expense for 2007, under the double-declining-balance method.

31. On January 2, 2009, Topanga Company purchased a machine for $90,000. The machine has a

five-year estimated useful life and a $6,000 estimated residual value. In addition, the company expects

to use the machine 200,000 hours. Assuming that the machine was used 35,000 hours during 2010,

complete the following chart. If a figure cannot be determined, indicate so by placing an X in the box.

(Show your work.)

Method

Depreciation Expense for

2010

Carrying Value at 12/31/10

Straight-line

Production

Double-declining-balance

32. On January 2, 2009, Vanowen Company purchased a machine for $80,000. The machine has an

eight-year estimated useful life and an $8,000 estimated residual value. In addition, the company

expects to use the machine 200,000 hours. Assuming that the machine was used 35,000 hours during

2010, complete the following chart. If a figure cannot be determined, indicate so by placing an X in the

box. (Show your work.)

Method

Depreciation Expense for

2010

Carrying Value at 12/31/10

Straight-line

Production

Double-declining-balance

33. Al’s Car Wash purchased a piece of equipment on October 1, 2008, for $27,000. The equipment has an

estimated life of four years or 40,000 units of production and an estimated residual value of $2,000.

Compute depreciation for 2008, 2009, and 2010 using the following methods: (a) straight-line, (b)

production, and (c) double-declining-balance. Assume that the company’s fiscal year corresponds to

the calendar year and that 3,000, 12,000, and 8,000 units were produced in the respective years. (Show

your work.)

34. On January 1, 2008, North Side Manufacturing Company purchased for $40,000 a machine that will

produce an estimated 75,000 units of Product X. The machine has an estimated useful life of four years

and an estimated residual value of $8,000. Calculate the following amounts, rounding answers to the

nearest dollar: (a) the carrying value of the machine after it has been used for three and one-half years,

under the straight-line method; (b) depreciation expense for 2010, under the production method

(assume that 13,000 units were produced that year); and (c) accumulated depreciation at the end of

2009, under the double-declining-balance method. (Show your work.)

Method

Straight-line

Production

Double-declining-balance

35. On January 1, 2005, Town Spa Pizza purchased for $16,000 a delivery truck that will be driven an

estimated 100,000 miles. The truck has an estimated useful life of ten years and an estimated residual

value of $5,000. Calculate the following amounts: (a) depreciation expense for 2010, under the

production method (assume that 17,000 miles were driven that year); (b) the accumulated depreciation

after the truck has been used for five and one-half years, under the straight-line method; and (c)

depreciation expense for 2007, under the double-declining-balance method. (Show your work.)

36. Bob Quinn is in the gravel business and has engaged you to assist in evaluating his company, Quinn

Gravel Company. Your first step is to collect the facts about the company’s operations. On January 3,

2010, Bob purchased a piece of property with gravel deposits for $3,155,000. He estimated that the

gravel deposits contained 4,700,000 cubic yards of gravel. The gravel is used for making roads. After

the gravel is gone, the land, which is in the desert, will be worth only about $100,000.

The equipment required to extract the gravel cost $726,000. In addition, Bob had to build a small

frame building to house the mine office and a small dining hall for the workers. The building cost

$76,000 and will have no residual value after its estimated useful life of ten years. It cannot be moved

from the mine site. The equipment has an estimated useful life of six years (with no residual value) and

also cannot be moved from the mine site.

Trucks for the project cost $154,000 (estimated life, six years; residual value, $10,000). The trucks, of

course, can be used at a different site.

Bob estimated that in five years all the gravel would be mined and the mine would be shut down.

During 2010, 1,175,000 cubic yards of gravel were mined. The average selling price during the year

was $1.33 per cubic yard, and at the end of the year 125,000 cubic yards remained unsold. Operating

expenses were $426,000 for labor and $116,000 for other expenses.

a. Prepare adjusting entries to record depletion and depreciation for the first year of operation (2010).

Assume that the depreciation rate is equal to the percentage of the total gravel mined during the year,

unless the asset is movable. For movable assets, use the straight-line method. (Omit explanations.)

General Journal

Page 1

Date

Description

Post.

Ref.

Debit

Credit

b. Prepare an income statement for 2010 for Quinn Gravel Company.

Quinn Gravel Company

Income Statement

For the Year Ended December 31, 2010

c. What is your evaluation of the company’s operations? Explain your evaluation and offer

suggestions. Ignore income tax effects.

37. Starsky Manufacturing Company purchased three machines during the year:

Feb. 10

Machine 1

$ 1,800

July 26

Machine 2

12,000

Oct. 11

Machine 3

21,600

Each machine is expected to last six years and have no residual value. The company’s fiscal year

corresponds to the calendar year. Using the straight-line method, compute the depreciation charge for

each machine for the year. Round amounts to the nearest dollar.

38. A truck that cost $40,000 and on which $30,000 of accumulated depreciation had been recorded was

disposed of on July 1, the first day of the new fiscal year. Prepare entries in journal form (without

explanation) to record the disposal under each of the following assumptions:

a. It was discarded as having no value.

b. It was sold for $7,200 cash.

c. It was sold for $13,500 cash.

General Journal

Page 1

Date

Description

Post.

Ref.

Debit

Credit

Accumulated Depreciation–Truck

$40,000 – $30,000 = $10,000 loss

Cash

Accumulated Depreciation–Truck

Truck

July1

Accumulated Depreciation–Truck

Gain on Sale of Truck

39. A truck that cost $29,600 and on which $21,600 of accumulated depreciation had been recorded was

disposed of on September 1, the first day of the new fiscal year. Prepare entries in journal form

without explanation to record the disposal under each of the following assumptions:

a. It was discarded as having no value.

b. It was sold for $6,000 cash.

c. It was sold for $11,200 cash.

General Journal

Page 1

Date

Description

Post.

Ref.

Debit

Credit

40. Leroy Mining Company purchased land containing an estimated 10,000,000 tons of ore for a cost of

$750,000. The land without the ore is estimated to be worth $150,000 (the residual value). Buildings

costing $45,000 with an estimated useful life of 20 years were erected on the site. Because of the

remote location, the buildings have no residual value. The company expects that all the usable ore can

be mined in eight years. During its first year of operation, the company mined 1,000,000 tons of ore

and at the end of the year had an inventory of 200,000 tons. Determine the following amounts for the

first year: (a) depletion charge per ton; (b) depletion expense for year; and (c) depreciation expense for

buildings, using the straight-line method. (Show your work.)

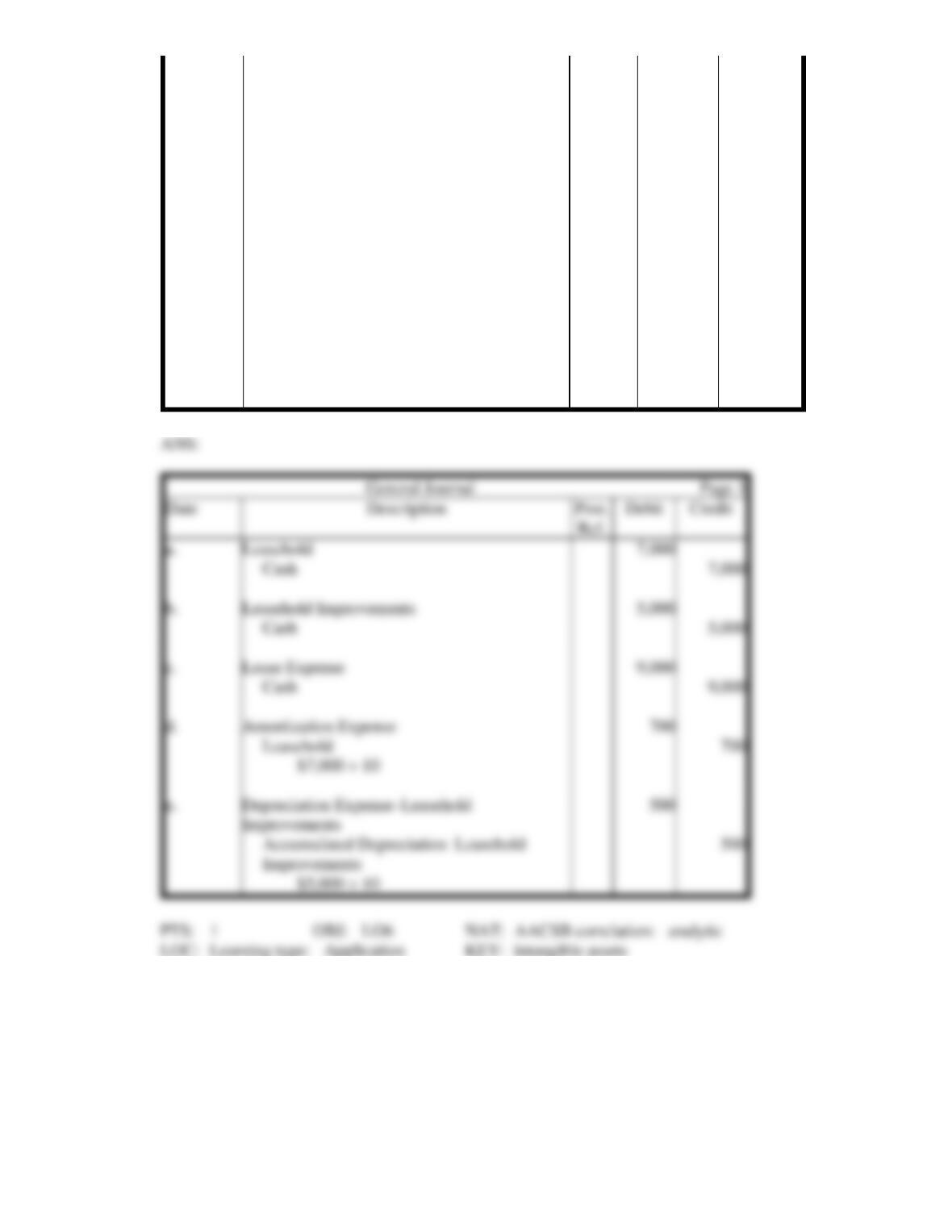

41. Bob Jefferson obtained a ten-year sublease on a busy corner to open a used car business. To obtain the

sublease, he had to pay $7,000 to the current tenant, who had 12 years to go on his lease. The annual

cost of the lease is $9,000. In addition to paying for the sublease, Bob paid $5,000 to pave the lot. The

paving will have no residual value after its useful life of ten years. Prepare entries in journal form to

record the following (omit explanations):

a. The payment for the sublease

b. The payment for the paving

c. The lease payment for the first year

d. The expense, if any, associated with the sublease for the first year

e. The expense, if any, associated with the paving, using the straight-line method for the first year

General Journal

Page 1

Date

Description

Post.

Ref.

Debit

Credit

42. Match each of the following terms with the descriptions below by supplying the letter of the correct

term.

a. Leasehold

f. Goodwill

b. Trademark

g. Software

c. Copyright

h. Noncompete covenant

d. Patent

i. Franchise

Leasehold

Cash

Leasehold Improvements

Cash

Lease Expense

Cash

Amortization Expense

Leasehold

$7,000 ÷ 10

e. Customer list

j. Research and development

___ 1. The amount paid for a business in excess of its fair market value

___ 2. A registered symbol or name to identify a product or service

___ 3. An exclusive right for 20 years to produce a particular product

___ 4. A contract restricting the rights of others to operate in a specific industry

___ 5. A right to occupy land or buildings under a long-term rental contract

___ 6. An exclusive right to sell literary, artistic, or musical works and computer software

___ 7. Capitalized costs associated with computer programs developed for sale, lease, or

internal use

___ 8. A right to an exclusive territory or market

___ 9. A planned search for a new product, as well as pure research

___ 10. Access to the names of subscribers or patrons

ANS: