Chapter 09 Test Bank Key

1. The equilibrium price in a competitive market

A. Ensures that anyone who wants the good can get it.

2. To determine the market supply, the quantities

A. Demanded at each price by each demander are added together.

3. The market supply curve in a perfectly competitive market is usually

A. Downward-sloping.

4. Which of the following is a determinant of market supply but not the supply curve of an individual firm?

5. Which of the following is true about a competitive market supply curve?

6. If the price of ricotta cheese, an ingredient in lasagna, increases, then

7. If a new sushi restaurant opens, then

8. If someone invents a better way to produce frozen pizzas, then

9. If catfish farmers expect catfish prices to fall in the future, then right now

10. Marginal cost is the increase in total cost associated with a one-unit

A. Increase in production.

11. Which of the following is an investment decision in a competitive market?

12. Investment decisions are made on the basis of the relationship of price to

13. In making an investment decision, an entrepreneur

14. Which of the following is characteristic of a perfectly competitive market?

15. For a competitive market in the long run,

A. Economic losses induce firms to shut down.

16. If economic profits are earned in a competitive market, then over time

17. If long-run economic losses are being experienced in a competitive market,

18. In a competitive market, economic profits will

19. In a competitive market where firms are earning economic profits, which of the following should be expected

as the industry moves to long-run equilibrium, ceteris paribus?

A. A higher price and fewer firms.

20. In a competitive market where firms are earning economic losses, which of the following should be expected

as the industry moves to long-run equilibrium, ceteris paribus?

21. The entry of firms into a market

A. Increases the equilibrium price.

22. Other things being equal, as more firms enter a market, the market supply curve

A. Becomes more inelastic.

23. The entry of firms into a market, ceteris paribus,

24. The exit of firms from a market, ceteris paribus,

25. The exit of firms from a market, ceteris paribus,

26. Examples of barriers to entry

include A. Price taking.

27. Which of the following is not a barrier to entry?

28. Which of the following is not a barrier to entry?

29. Perfectly competitive firms cannot individually affect market price because

A. There is an infinite demand for their goods.

30. Which of the following is characteristic of a perfectly competitive market?

31. Which of the following is characteristic of a perfectly competitive market?

A. Long-run economic profit.

32. Which of the following is not a characteristic of a perfectly competitive

market? A. Zero economic profit in the long run.

33. If the products of two firms are homogeneous, then they

A. Are perfect substitutes.

34. If two products are homogeneous, then they

35. The behavior expected in a competitive market includes

36. In a perfectly competitive industry, economic profit:

A. Can persist in the long run because of barriers to entry.

37. In a competitive market,

38. Suppose a perfectly competitive firm is experiencing zero economic profits. In an effort to increase profits, the

firm decides to initiate an advertising campaign for its product. The most likely short-run result of this campaign,

ceteris paribus, would be

39. The market structure of the computer industry

40. The competitive market model is important because

A. It characterizes all the markets in the U.S. economy.

41. Which of the following is a production decision?

A. Whether to enter or exit an industry.

42. To maximize profits, a competitive firm will seek to expand output until

43. If a firm finds that its marginal cost is greater than its price, it

A. Should reduce production.

44. Profit per unit is equal to

45. Profit per unit is maximized when the firm produces the output where

A. The ATC is minimized.

46. A profit-maximizing producer seeks to

47. Which of the following characterizes a firm that is in long-run perfectly competitive equilibrium where profits

are maximized?

48. For a perfectly competitive market, long-run equilibrium is characterized by all of the following but which one?

49. Which of the following is consistent with long-run equilibrium for a perfectly competitive market?

A. Average total costs of production are maximized.

50. If a firm decides to make the investment decision to expand its capacity, then it must have discovered that

51. In long-run perfectly competitive equilibrium, marginal cost

52. In a perfectly competitive market, when price is equal to the

53. In a perfectly competitive market in the long run, which of the following is not correct?

A. Firms are attempting to maximize profit.

54. In which of the following cases would a firm enter a market?

55. If price is above the long-run competitive equilibrium level,

56. In which of the following cases would entry and exit cease?

57. If price is below the long-run competitive equilibrium level, there will be

58. In which of the following cases would a firm exit from a market?

59. In a competitive market, if the market price is equal to the minimum point of the firm’s ATC curve, the firm may

seek to earn economic profits by

60. A competitive market creates strong pressure for technological innovation that

61. Technological improvements cause

62. Technological improvements cause

A. New firms to enter but existing firms to continue producing their old output levels.

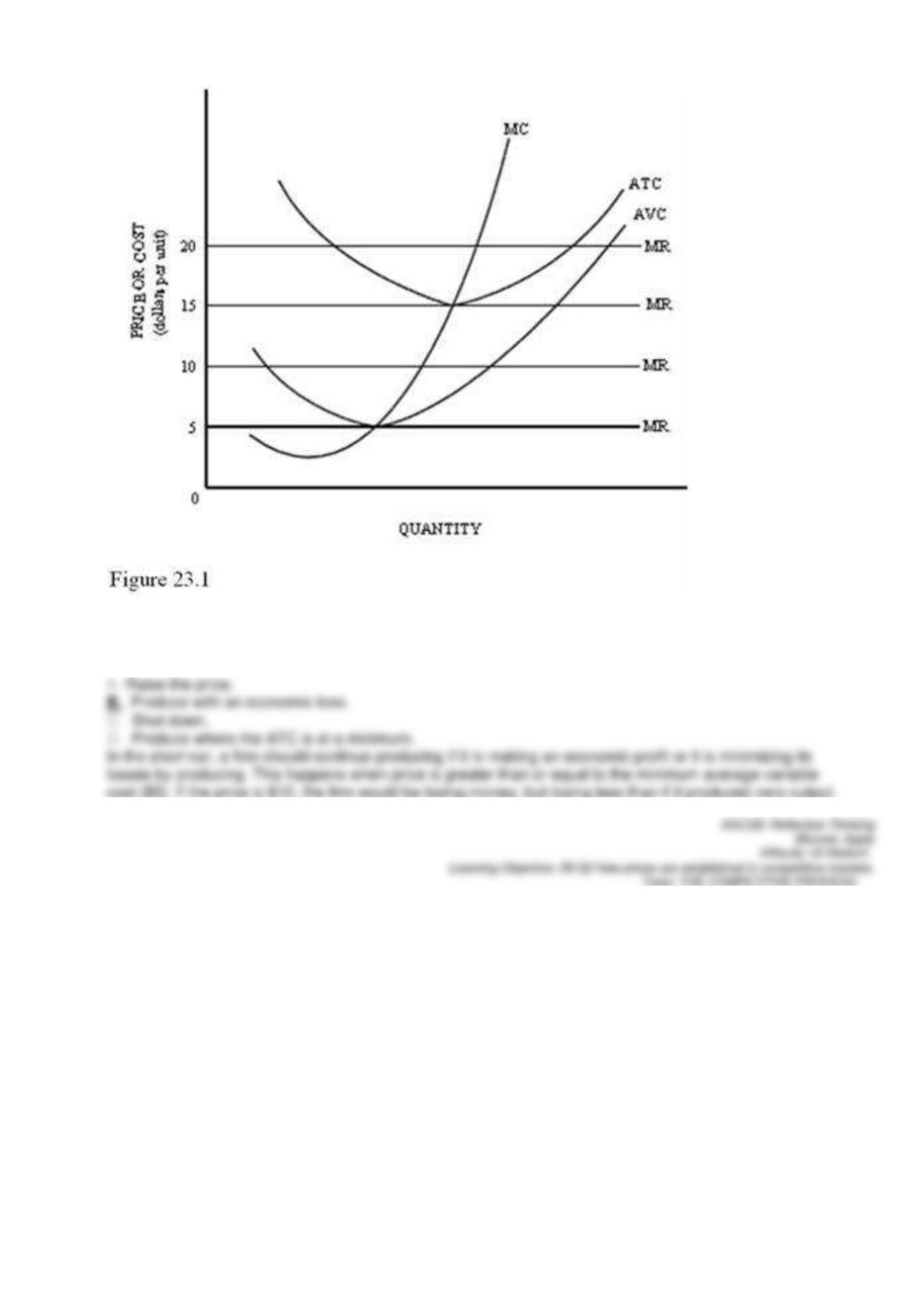

63. A firm should shut down production when

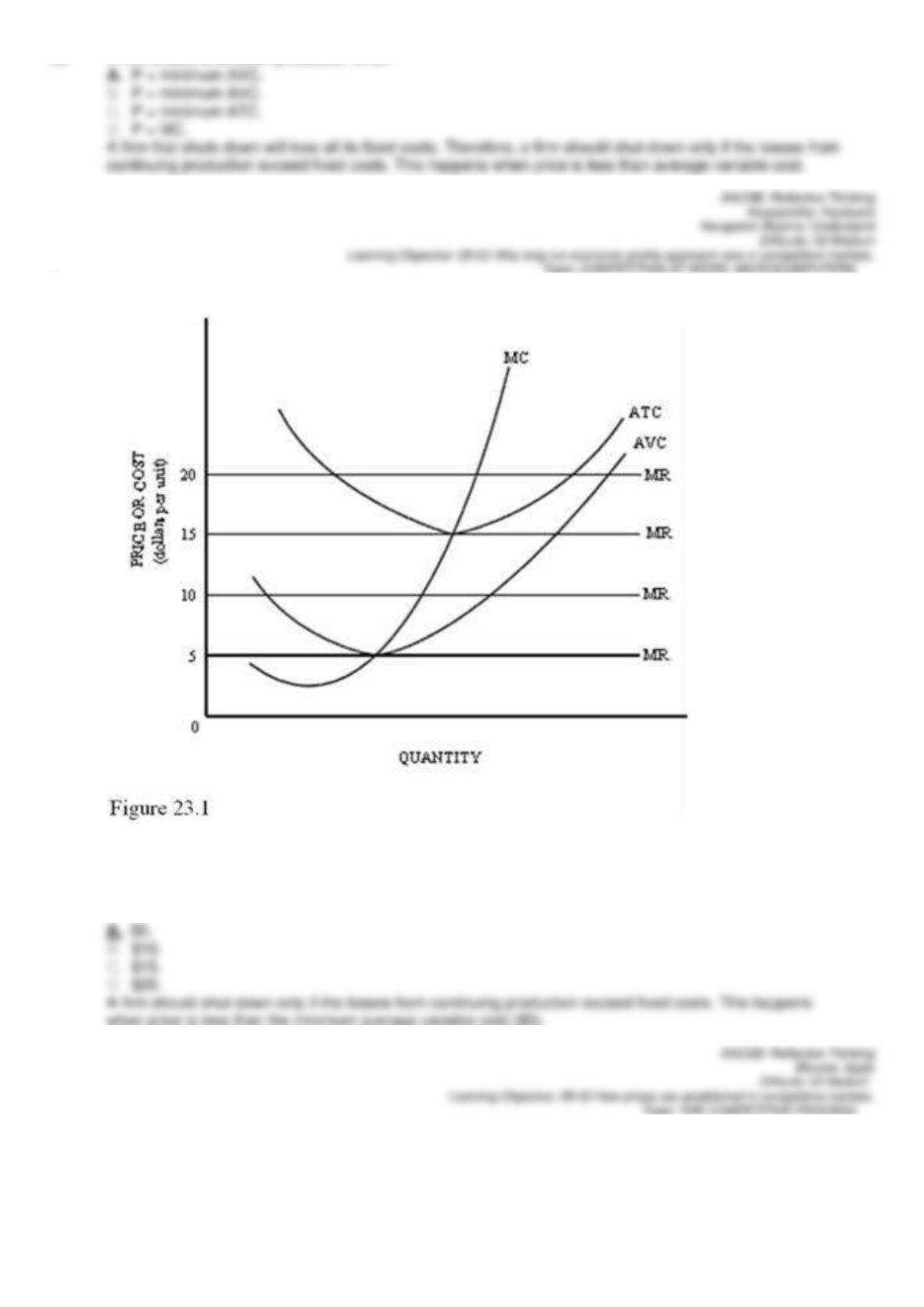

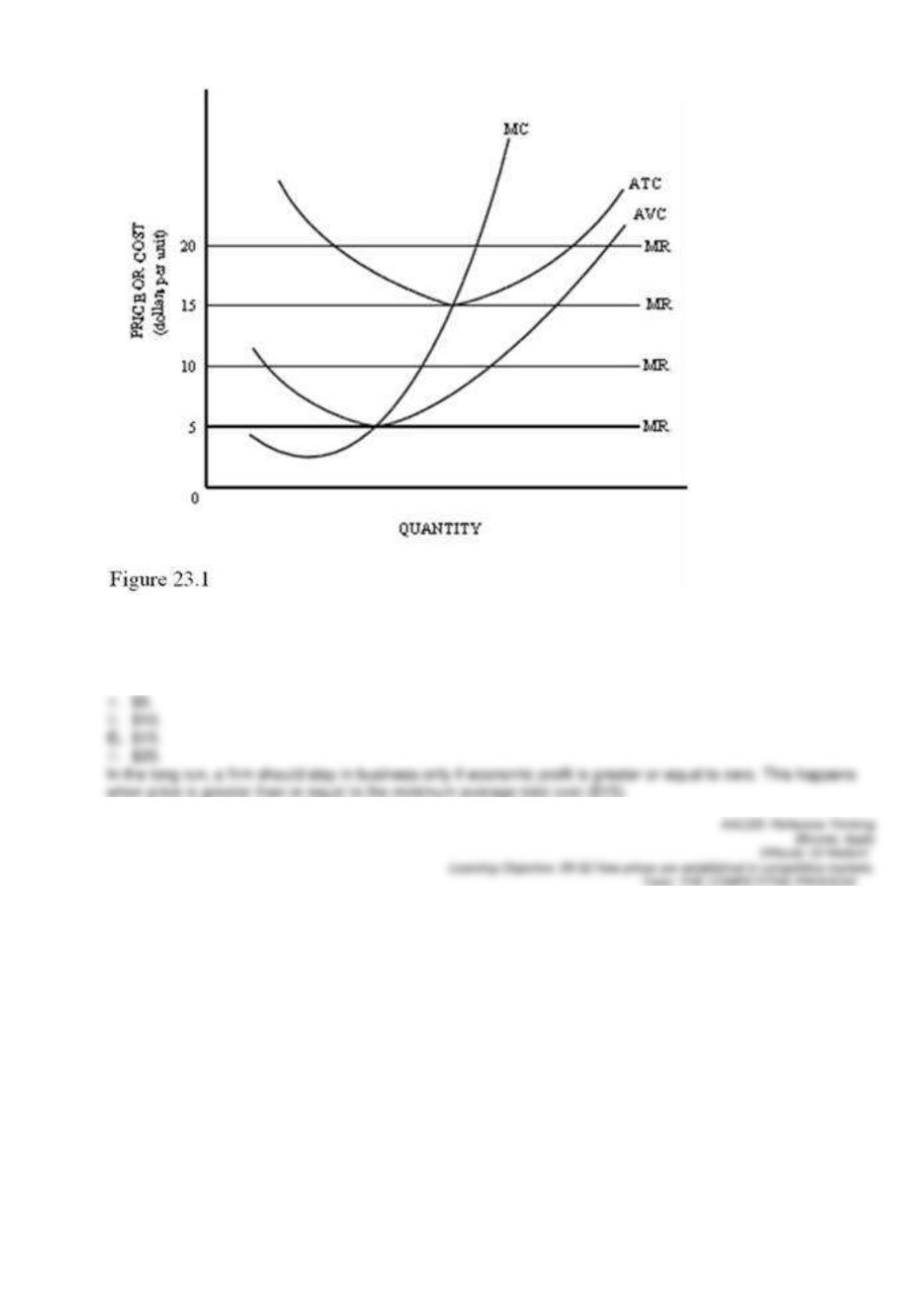

64.

Refer to Figure 23.1 for a perfectly competitive firm. This firm should shut down in the short run if the market

price is below

65.

Refer to Figure 23.1 for a perfectly competitive firm. In the long run, this firm would stay in this market only if the

market price was equal to or higher than

66.

Refer to Figure 23.1. If the market price equaled $10, in the short run this firm should

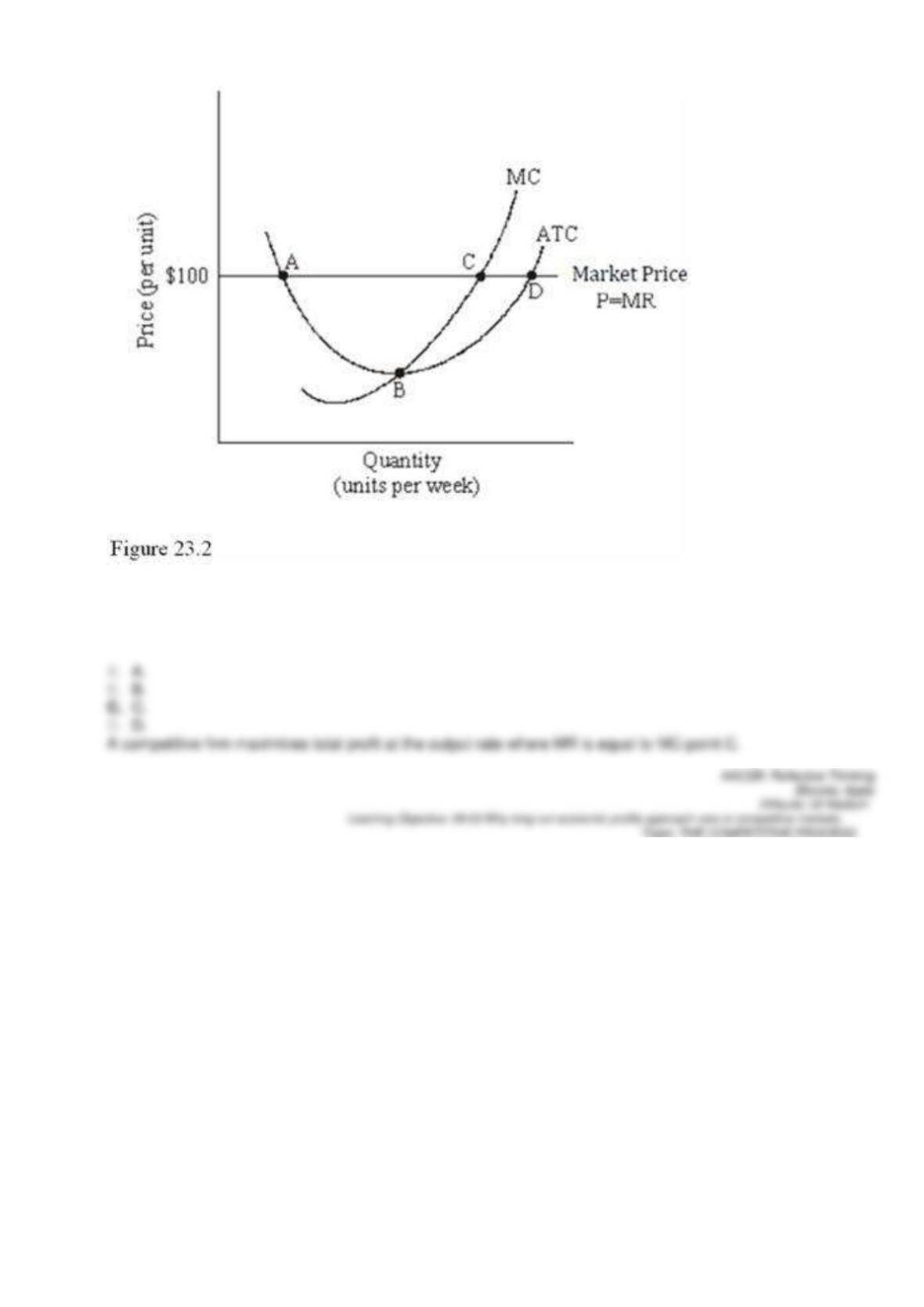

67.

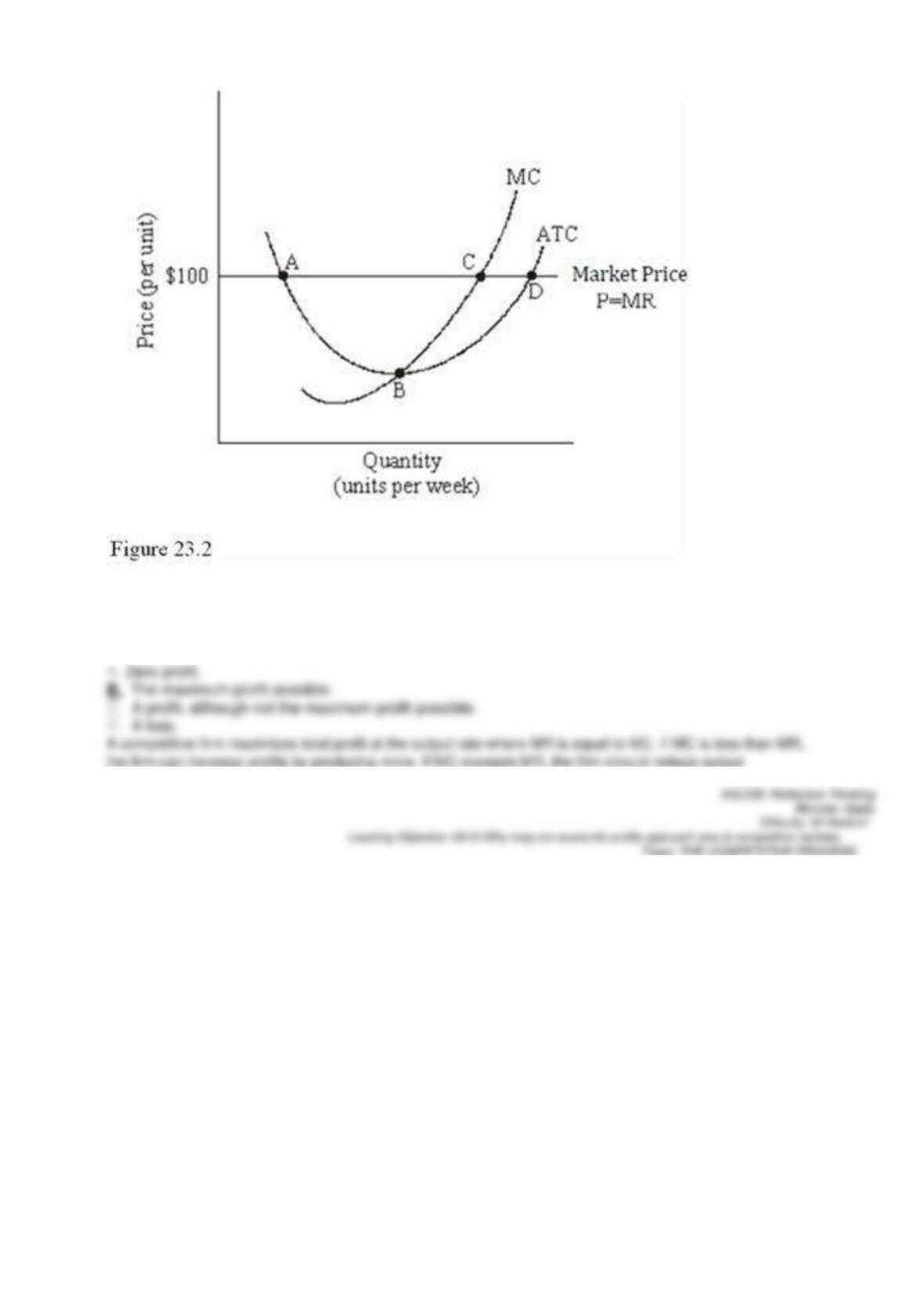

Refer to Figure 23.2 for a perfectly competitive firm. This firm will maximize profits by producing the level of

output that corresponds to point

68.

Refer to Figure 23.2 for a perfectly competitive firm. If this firm produces the level of output corresponding to

point C in the short run, it will earn

69.

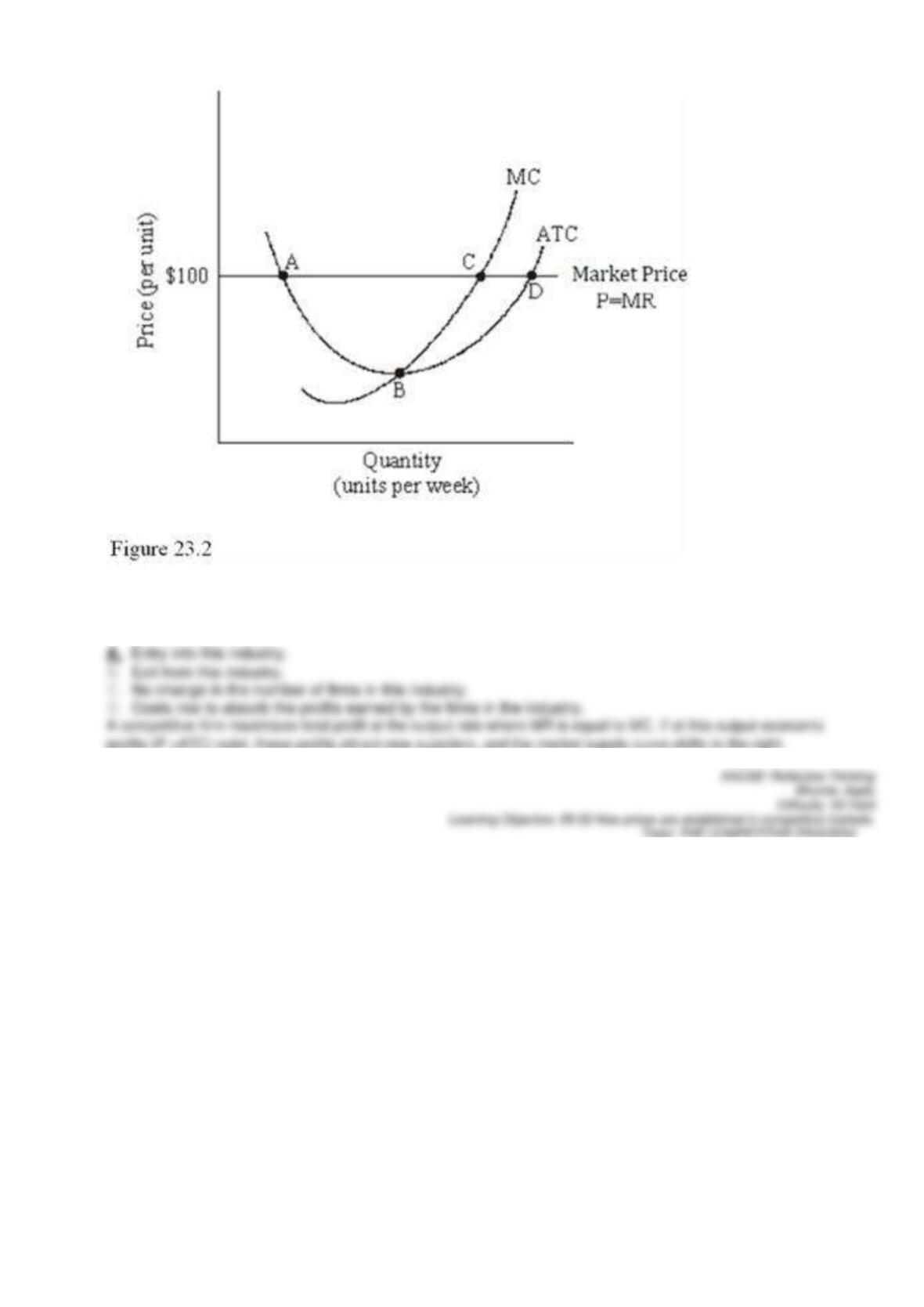

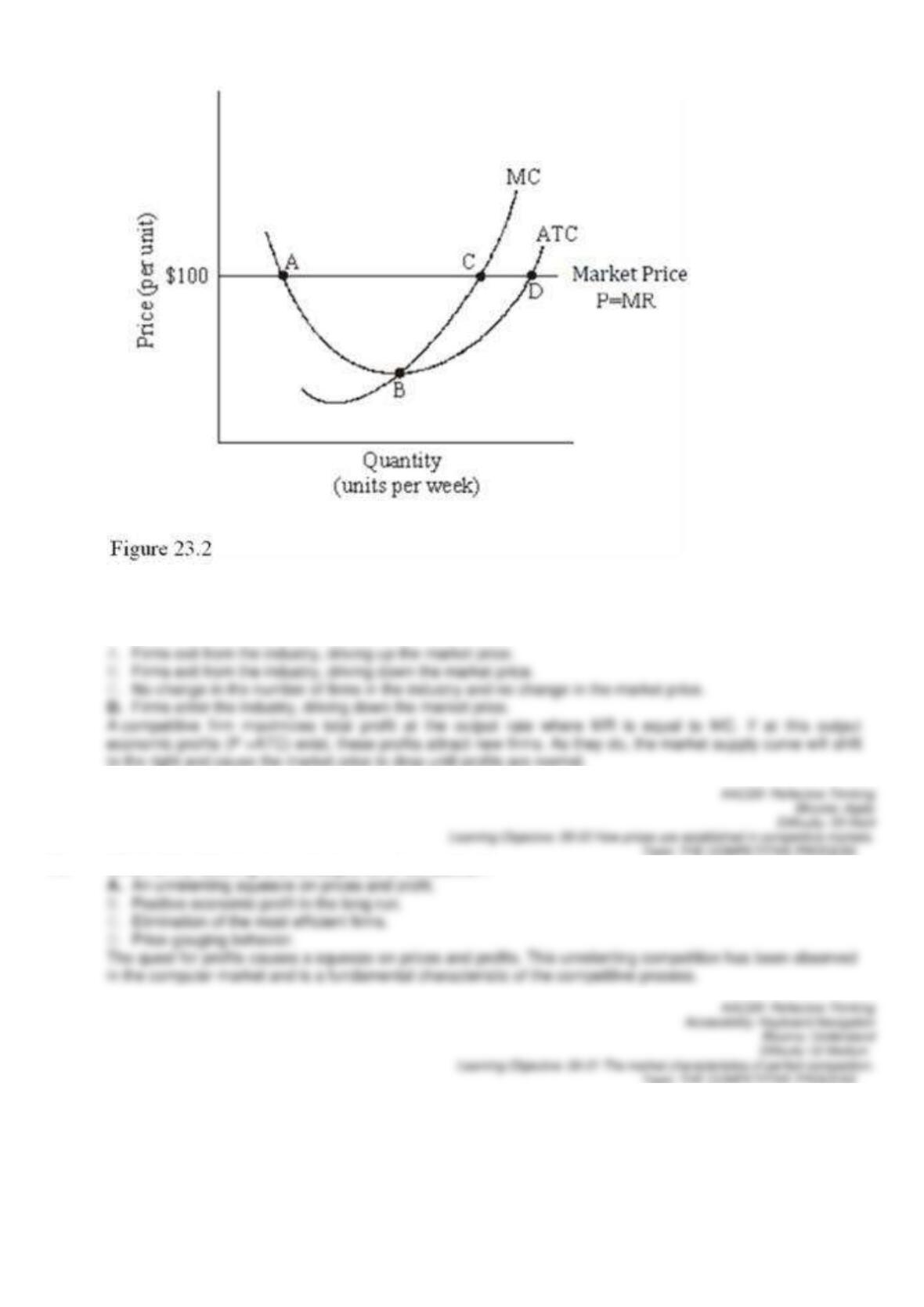

Refer to Figure 23.2 for a perfectly competitive firm. Given the current market price of $100, we expect to see

70.

Refer to Figure 23.2 for a perfectly competitive firm. Given the current market price of $100, we expect to see

71. Which of the following is a consequence of competition?