Chapter 9: Receivables

119.

Harper Company lends Hewell Company $40,000 on March 1, accepting a four-month, 6% interest note.

Harper

Company prepares financial statements on March 31. What adjusting entry should be made before

the financial

statements can be prepared?

a.

Cash 200

Interest Revenue 200

b. Interest Receivable

Interest Revenue

800

800

c. Interest Receivable

Interest Revenue

200

200

d. Note Receivable

Cash

40,000

40,000

120.

On August 1, Kim Company accepted a 90-day note receivable as payment for services provided to Hsu

Company. The terms of the note were $20,000 face value and 6% interest. On October 30, the journal

entry to

record the collection of the note should include a

a.

credit to Notes Receivable for $20,300

b.

debit to Interest Receivable for $300

c.

credit to Interest Revenue for $300

d.

debit to Notes Receivable for $20,000

Chapter 9: Receivables

121.

Current assets are usually listed in order

a.

of the due date

b.

of the size

c.

alphabetically

d.

of liquidity

122.

The accounts receivable turnover measures

a.

how frequently during the year the accounts receivable are converted to cash

b.

the number of days of accounts receivable outstanding

c.

the fair market value of accounts receivable

d.

the efficiency of the accounts payable function

123.

The number of days’ sales in receivables

a.

is an estimate of the length of time the receivables have been outstanding

b.

measures the number of times the receivables turn over each year

c.

is net credit sales divided by average receivables

d.

is not meaningful and therefore is not used

Chapter 9: Receivables

124.

Given the following information, compute accounts receivable turnover:

Gross sales

$150,000

Accounts receivable, beginning of year

$18,000

Sales

135,000

Accounts receivable, end of year

22,000

a. 6.75

b. 7.50

c. 6.13

d. 6.82

125.

At the end of the current year, Accounts Receivable has a balance of $550,000; Allowance for Doubtful

Accounts

has a credit balance of $5,500; and sales for the year total $2,500,000. An analysis of receivables

estimates

uncollectible receivables as $25,000.

Determine the amount of the adjusting entry for bad debt expense and the adjusted balance of

Allowance of

Doubtful Accounts, respectively.

a. $19,500 and $25,000 b. $30,500 and $525,000

c. $19,500 and $525,000 d. $30,500 and $25,000

Chapter 9: Receivables

126.

At the end of the current year, Accounts Receivable has a balance of $550,000; Allowance for Doubtful

Accounts

has a credit balance of $5,500; and sales for the year total $2,500,000. An analysis of receivables

estimates

uncollectible receivables as $25,000.

Determine the net realizable value of accounts receivable after adjustment. (Hint: Determine the amount of

the

adjusting entry for bad debt expense and the adjusted balance of Allowance of Doubtful Accounts.)

a. $550,000 b. $544,500

c. $525,000 d. $575,000

127.

Other than Accounts Receivable and Notes Receivable, name other receivables that might be

included in the

general ledger.

128.

Discuss the similarities and differences between accounts receivable, notes receivable, and other receivables.

Chapter 9: Receivables

129.

List at least three indicators that a receivable may be uncollectible.

130.

Discuss the two methods for recording bad debt expense. What type of company uses each method?

Chapter 9: Receivables

131.

Journalize the following transactions using the direct write-off method of accounting for uncollectible

receivables.

April 1 Sold merchandise on account to Jim Dobbs, $7,200. The cost of the merchandise is $5,400.

June 10 Received payment for one-third of the receivable from Jim Dobbs and wrote off the remainder.

Oct. 11 Reinstated the account of Jim Dobbs for and received cash in full payment.

132.

Stephanie Roe utilizes the direct write-off method of accounting for uncollectible receivables. On September

15 she

is notified by the attorneys for Jacob Marley that Jacob Marley is bankrupt and no cash is expected in

the

liquidation of Jacob Marley. Write off the $675 of accounts receivable due from Jacob Marley.

Chapter 9: Receivables

133.

Journalize the following transactions using the direct write-off method of accounting for uncollectible

receivables:

Feb. 20 Received $1,000 from Andrew Warren and wrote off the remainder owed of $4,000 as uncollectible.

May 10 Reinstated the account of Andrew Warren and received $4,000 cash in full payment.

134.

The following journal entries would be used in one of the two methods of accounting for

uncollectible

receivables. Identify each.

(a)

Bad Debt Expense 900

Accounts Receivable, Billings 900

(b)

Allowance for Doubtful Accounts 900

Accounts Receivable, Grover 900

Chapter 9: Receivables

135.

Determine the amount to be added to Allowance for Doubtful Accounts in each of the following cases and

indicate

the ending balance in each case.

(a)

Credit balance of $300 in Allowance for Doubtful Accounts just prior to adjustment. Analysis of

Accounts Receivable indicates uncollectible receivables of $8,500.

(b)

Credit balance of $500 in Allowance for Doubtful Accounts just prior to adjustment. Uncollectible

receivables are estimated at 2% of credit sales, which totaled $1,000,000 for the year.

136.

Journalize the following transactions using the allowance method of accounting for uncollectible

receivables.

April 1 Sold merchandise on account to Jim Dobbs, $7,200. The cost of the merchandise is $5,400.

June 10 Received payment for one-third of the receivable from Jim Dobbs and wrote off the remainder.

Oct. 11 Reinstated the account of Jim Dobbs and received cash in full payment.

Chapter 9: Receivables

137.

At the end of the current year, Accounts Receivable has a balance of $700,000; Allowance for Doubtful

Accounts

has a credit balance of $5,500; and sales for the year total $3,500,000. Bad debt expense is

estimated at 1/2 of

1% of sales.

Determine (a) the amount of the adjusting entry for bad debt expense; (b) the adjusted balances of Accounts

Receivable, Allowance for Doubtful Accounts, and Bad Debt Expense; and (c) the net realizable value of

accounts

receivable.

138.

At the end of the current year, Accounts Receivable has a balance of $750,000; Allowance for Doubtful

Accounts

has a debit balance of $6,200; and sales for the year total $3,500,000. Bad debt expense is

estimated at 1/2 of

1% of sales.

Determine (a) the amount of the adjusting entry for bad debt expense; (b) the adjusted balances of Accounts

Receivable, Allowance for Doubtful Accounts, and Bad Debt Expense; and (c) the net realizable value of

accounts

receivable.

139.

At the end of the current year, Accounts Receivable has a balance of $90,000; Allowance for Doubtful

Accounts

has a credit balance of $850; and sales for the year total $300,000. Bad debt expense is estimated

at 2.5% of

sales.

Determine (a) the amount of the adjusting entry for uncollectible accounts; (b) the adjusted balances of

Accounts

Receivable, Allowance for Doubtful Accounts, and Bad Debt Expense; and (c) the net realizable

value of

accounts receivable.

140.

At the end of the current year, Accounts Receivable has a balance of $550,000; Allowance for Doubtful

Accounts

has a credit balance of $5,500; and sales for the year total $2,500,000. An analysis of receivables

estimates

uncollectible receivables as $25,000.

Determine (a) the amount of the adjusting entry for bad debt expense; (b) the adjusted balances of Accounts

Receivable, Allowance for Doubtful Accounts, and Bad Debt Expense; and (c) the net realizable value of

accounts

receivable.

Chapter 9: Receivables

141.

At the end of the current year, Accounts Receivable has a balance of $675,000; Allowance for Doubtful

Accounts

has a debit balance of $5,400; and sales for the year total $3,000,000. An analysis of receivables

indicates the

uncollectible receivables are estimated to be $45,000.

Determine (a) the amount of the adjusting entry for bad debt expense; (b) the adjusted balances of Accounts

Receivable, Allowance for Doubtful Accounts, and Bad Debt Expense; and (c) the net realizable value of

accounts

receivable.

142.

Discount Mart utilizes the allowance method of accounting for uncollectible receivables. On December 12

the

company receives a $550 check from Chad Thomas in settlement of Thomas’s $1,100 outstanding

accounts

receivable. Due to Thomas’s failing health he is closing his company and is expecting to make no

further payments

to Discount Mart. Journalize this declaration.

Chapter 9: Receivables

143.

On June 30 (the end of the period), Brown Company has a credit balance of $2,275 in Allowance for

Doubtful

Accounts. An evaluation of accounts receivable indicates that the proper balance should be

$30,025. Journalize the

appropriate adjusting entry.

Chapter 9: Receivables

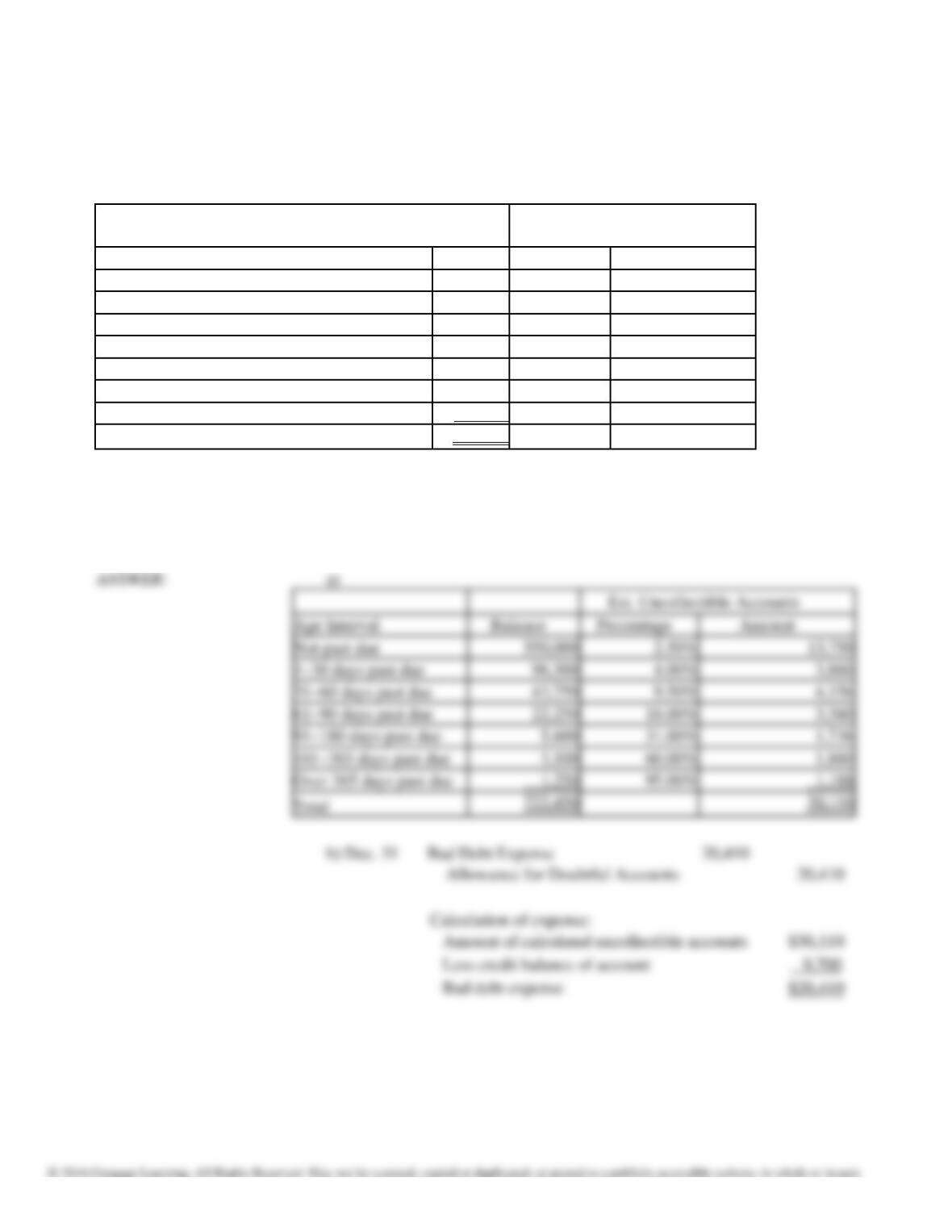

144.

a) The aging of Torme Designs’ accounts receivable is shown below. Calculate the amount of each

periodicity

range that is deemed to be uncollectible.

Est. Uncollectible Accts

Age Interval:

Balance:

Percentage:

Amount:

Not past due

850,000

3.50%

1~30 days past due:

47,500

5.00%

31~60 days past due:

21,750

10.00%

61~90 days past due:

11,250

20.00%

91~180 days past due:

5,065

30.00%

181~365 days past due:

2,500

50.00%

Over 365 days past due:

1,145

95.00%

Total:

939,210

b) If the Allowance for Doubtful Accounts has a credit balance of $1,135.00, record the adjusting entry

for

the bad debt expense for the year.

Est. Uncollectible Accts

Age Interval:

Amount:

Not past due

850,000

1~30 days past due:

47,500

31~60 days past due:

21,750

61~90 days past due:

11,250

91~180 days past due:

181~365 days past due:

Over 365 days past due:

Chapter 9: Receivables

145.

For each of the following scenarios, indicate the amount of the adjusting journal entry for bad debt

expense to be

recorded, the balance in allowance for doubtful accounts after adjustment at December 31,

and the net realizable

value of accounts receivable at December 31.

a) Based on an analysis of Simmon’s Company’s $380,000 balance in Accounts Receivable at December

31, it was estimated that $15,500 will be uncollectible. There is a credit balance of $1,200 in Allowance

for Doubtful

Accounts before adjustment.

b)

Blake Company had net credit sales of $900,000 at year-end, and has an Accounts Receivable balance of

$425,000 at December 31, and an Allowance for Doubtful Accounts credit balance of $11,000 before

adjustment. Blake estimates bad debt expense as 3/4 of 1% of net credit sales.

c)

Hidgon Inc. has a balance of $812,000 in Accounts Receivable at December 31. An analysis of those

receivables shows $24,000 will probably not be collected. Before adjusting entries are prepared, the

Allowance

for Doubtful Accounts has a debit balance of $750.

Chapter 9: Receivables

146.

A partially competed aging of receivables schedule for Lindy Designs’ is shown below. Calculate the amount

that is estimated to be uncollectible.

a)

Determine the amount estimated to be uncollectible by completing the aging of receivables schedule.

Round

calculations to the nearest dollar.

Est. Uncollectible

Accounts

Age Interval

Balance

Percentage

Amount

Not past due

550,000

2.50%

1~30 days past due

96,500

4.00%

31~60 days past due

43,750

9.50%

61~90 days past due

22,250

16.00%

91~180 days past due

5,600

31.00%

181~365 days past due

3,100

60.00%

Over 365 days past due

1,250

95.00%

Total

722,450

b)

If the Allowance for Doubtful Accounts has a credit balance of $9,700, record the adjusting entry for

the bad

debt expense for the year.

c)

If the Allowance for Doubtful Accounts has a debit balance of $9,700, record the adjusting entry for

the bad

debt expense for the year.

Total

Chapter 9: Receivables

147.

Discuss the (1) focus and (2) financial statement emphasis of (a) the percent of sales and (b) the

analysis of

receivables methods of estimating bad debts.

Chapter 9: Receivables

148.

Morry Company wrote off the following accounts receivable as uncollectible for the first year of its

operations

ending December 31:

Required:

Customer

Amount

J. Jackson

$10,000

L. Stanton

9,500

C. Barton

13,100

S. Fenton

2,400

Total

$35,000

(1)

Journalize the write-offs for the current year under the direct write-off method.

(2)

Journalize the write-offs for the current year under the allowance method. Also,

journalize the adjusting entry for uncollectible receivables assuming the

company made $2,400,000 of credit sales during the year and the industry

average for uncollectible

receivables is 1.50% of credit sales.

(3)

How much higher or lower would Morry Company’s net income have been under the direct write-off

method than under the allowance method?

Chapter 9: Receivables

149.

Fellows Corporation has determined that the $2,700 accounts receivable due from Andrew Stevens is

uncollectible. Compare the journal entry that is required under the direct write-off method to the journal

entry that

is required using the allowance method.

150.

For a business that uses the allowance method of accounting for uncollectible receivables:

(a)

Journalize the entries to record the following:

(1)

Record the adjusting entry at December 31, the end of the first fiscal year, to

record the bad debt expense. The accounts receivable account has a balance of

$800,000,

and the contra asset account before adjustment has a debit balance of

$600. Analysis

of the receivables indicates uncollectible receivables of

$18,000.

(2)

In March of the next year, the $350 owed by Fronk Co. on account is written

off as

uncollectible.

(3)

In November of the next year, $200 of the Fronk Co. account is reinstated

and

payment of that amount is received.

(4)

In December of the next year, $400 is received on the $600 owed by Dodger

Co. and

the remainder is written off as uncollectible.

(b)

Redo the entries in steps (2), (3), and (4) assuming the company uses the direct

write-off

method.

Chapter 9: Receivables

Chapter 9: Receivables

151.

Sunshine Service Center received a 120-day, 6% note for $40,000, dated April 12 from a customer on account.

a.

Determine the due date of the note.

b.

Determine the maturity value of the note.

c.

Journalize the entry to record the receipt of the payment of the note at maturity.

152.

Fill in the blanks related to the characteristics of a promissory note.

1.

The party promising to pay the note is called the .

2.

The amount for which the note is written is called the amount.

3.

The date the note is to be paid is the date.

4.

The time between the date when a note is written and the time it must be paid is called the of the

note