132. What is the cost of the land, based upon the following data?

Land purchase price

$178,000

Broker’s commission

15,000

Payment for the demolition

and removal of existing building

5,000

Cash received from the sale of materials

salvaged from the demolished building

2,000

133. Comment on the validity of the following statements. “As an asset loses its ability to provide services,

cash needs to be set aside to replace it. Depreciation accomplishes this goal.”

134. On April 15, Compton Co. paid $2,800 to upgrade a delivery truck and $125 for an oil change. Journalize

the entries for the upgrade to delivery truck and oil change expenditures.

April 15

Delivery Truck

2,800

Cash

2,800

Repairs and Maintenance Expense

Cash

135. Computer equipment was acquired at the beginning of the year at a cost of $65,000 that has an estimated

residual value of $3,800 and an estimated useful life of 8 years. Determine the (a) depreciable cost, (b)

straight-line rate, and (c) annual straight-line depreciation.

(a)

$61,200

(b)

12.5%

(c)

$7,650

136. A double-declining balance rate for calculating depreciation expense is determined by doubling the

straight-line rate. Assuming that an asset has a useful life of 25 years, determine the rate to be used if using the

double-declining balance method.

137. Copy equipment was acquired at the beginning of the year at a cost of $72,000 that has an estimated

residual value of $9,000 and an estimated useful life of 5 years. It is estimated that the machine has an

estimated 1,000,000 copies. This year 315,000 copies were made. Determine the (a) depreciable cost, (b)

depreciation rate, and (c) the units-of-production depreciation for the year.

138. A machine costing $57,000 with a 6-year life and $54,000 depreciable cost was purchased January 1,

2015. Compute the yearly depreciation expense using straight-line depreciation.

139. A machine costing $85,000 with a 5-year life and $5,000 residual value was purchased January 2,

2011. Compute depreciation for each of the five years, using the declining-balance method at twice the

straight-line rate.

140. Computer equipment was acquired at the beginning of the year at a cost of $63,000 that has an estimated

residual value of $3,000 and an estimated useful life of 5 years. Determine the (a) depreciable cost (b) double–

declining-balance rate, and (c) double-declining-balance depreciation for the first year.

141. An asset was purchased for $58,000 and originally estimated to have a useful life of 10 years with a

residual value of $3,000. After two years of straight line depreciation, it was determined that the remaining

useful life of the asset was only 2 years with a residual value of $2,000.

a) Determine the amount of the annual depreciation for the first two years.

b) Determine the book value at the end of the 2nd year.

c) Determine the depreciation expense for each of the remaining years after revision.

142. Equipment was acquired at the beginning of the year at a cost of $75,000. The equipment was depreciated

using the straight-line method based upon an estimated useful life of 6 years and an estimated residual value of

$7,500.

a)

What was the depreciation expense for the first year?

b)

Assuming the equipment was sold at the end of the second year for $59,000, determine the gain or loss on sale of the equipment.

c)

Journalize the entry to record the sale.

Equipment

75,000

Gain on Sale of Asset

6,500

143. On the first day of the fiscal year, a new walk-in cooler with a list price of $58,000 was acquired in

exchange for an old cooler and $44,000 cash. The old cooler had a cost of $25,000 and accumulated

depreciation of $16,000.

Assume the transaction has commercial substance.

a)

Determine the gain to be recorded on the exchange.

b)

Journalize the entry to record the exchange.

144. Solare Company acquired mineral rights for $60,000,000. The diamond deposit is estimated at 6,000,000

tons. During the current year, 2,300,000 tons were mined and sold.

a.

Determine the depletion rate.

b.

Determine the amount of depletion expense for the current year.

c.

Journalize the adjusting entry to recognize the depletion expense.

a)

$10 per ton

b)

$23,000,000

List price

$58,000

Book value of old cooler

9,000

Cash paid

44,000

53,000

Gain on exchange

$5,000

Equipment (new)

58,000

Accum. Depreciation

16,000

Equipment

25,000

Gain on Exchange of Assets

5,000

Cash

44,000

145. Falcon Company acquired an adjacent lot to construct a new warehouse, paying $40,000 and giving a

short-term note for $410,000. Legal fees paid were $13,275, delinquent taxes assessed were $14,500, and fees

paid to remove an old building from the land were $15,800. Materials salvaged from the demolition of the

building were sold for $6,800. A contractor was paid $890,000 to construct a new warehouse. Determine the

cost of the land to be reported on the balance sheet and show your work.

146. Convert each of the following estimates of useful life to a straight-line depreciation rate, stated as a

percentage.

(1)

2 years

(2)

8 years

(3)

10 years

(4)

20 years

(5)

25 years

(6)

40 years

(7)

50 years

Plus:

Legal fees

13,275

Delinquent taxes

14,500

Demolition of building

15,800

43,575

$493,575

Less:

Salvage of materials

6,800

Cost of land

$486,775

147. Prior to adjustment at the end of the year, the balance in Trucks is $300,900 and the balance in

Accumulated Depreciation-Trucks is $88,200. Details of the subsidiary ledger are as follows:

Truck No.

Cost

Estimated Residual Value

Estimated Useful Life

Accumulated Depreciation at

Beginning of Year

Miles Operated During

Year

1

$100,000

$13,000

300,000

—

30,000

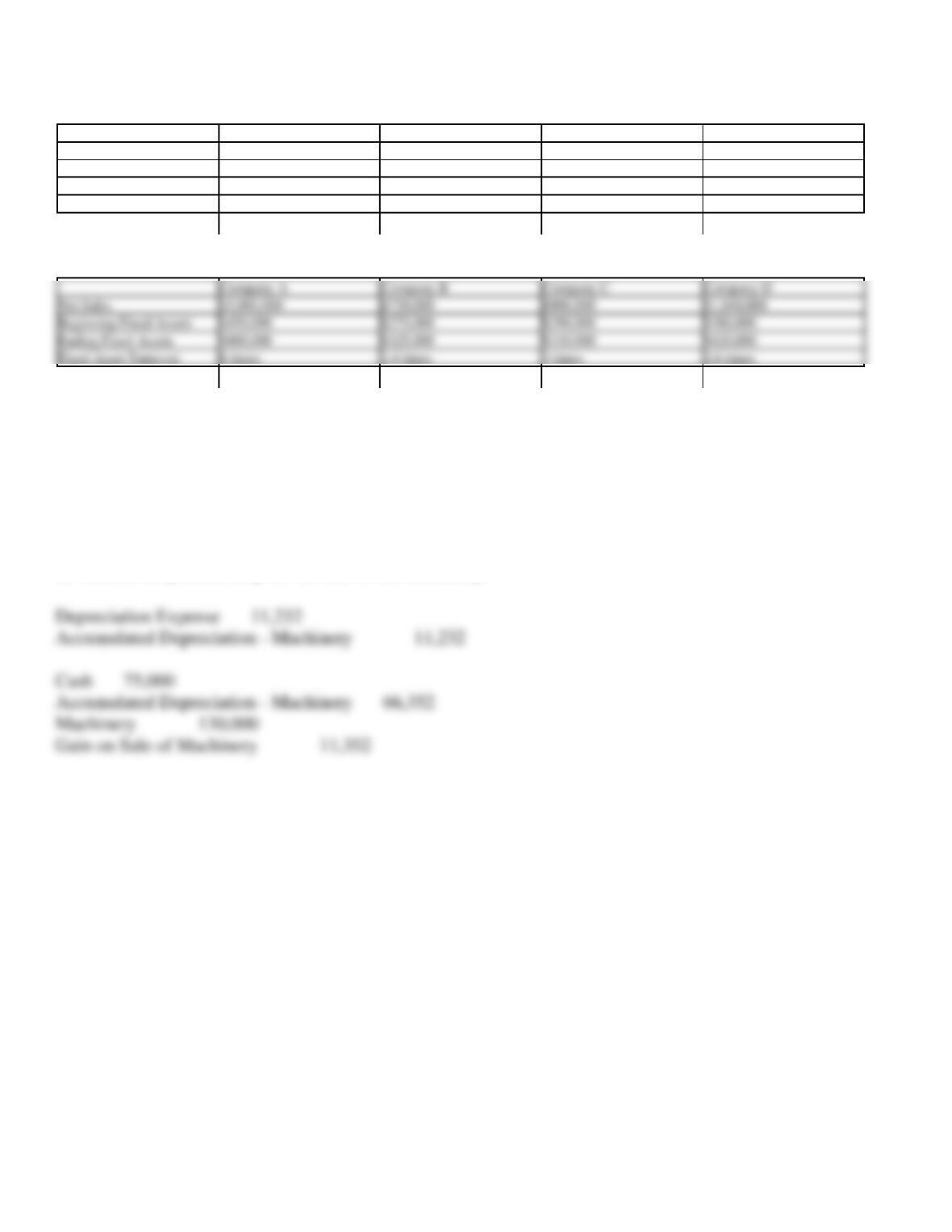

2

72,900

9,900

300,000

$60,000

25,000

3

38,000

3,000

200,000

8,050

45,000

4

90,000

13,000

200,000

20,150

40,000

Required:

(1)

Determine the depreciation rates per mile and the amount to be credited to the accumulated depreciation section of each of the

subsidiary accounts for the miles operated during the current year.

(2)

Journalize the entry to record depreciation for the year.

Truck No.

Rate per Mile

Miles Operated

Depreciation

1

29.0 cents

30,000

$8,700

2

21.0

25,000

3,000*

3

17.5

45,000

7,875

4

38.5

40,000

15,400

Total

34,975

$9,900, its residual value.

(2)

Depreciation Expense—Trucks

34,975

Accumulated Depreciation—Trucks

34,975

148. Champion Company purchased and installed carpet in its new general offices on March 30 for a total cost

of $18,000. The carpet is estimated to have a 15-year useful life and no residual value.

a.

Prepare the journal entries necessary for recording the purchase of the new carpet.

b.

Record the December 31 adjusting entry for the partial-year depreciation expense for the carpet assuming that Champion Company

uses the straight-line method.

a.

Mar.

Carpet

18,000

Cash

18,000

Accumulated Depreciation

Carpet depreciation

[($18,000/15 years) ´ 9/12].

149. Equipment acquired on January 2, 2011 at a cost of $273,500 has an estimated useful life of eight years

and an estimated residual value of $35,500.

Required:

(1)

What was the annual amount of depreciation for the years 2011, 2012, and 2013, assuming the straight-line method of

depreciation is used?

(2)

What was the book value of the equipment on January 1, 2014?

(3)

Assuming that the equipment was sold on January 2, 2014, for $170,500, journalize the entry to record the sale.

(4)

Assuming that the equipment had been sold on January 2, 2014, for $189,000 instead of $168,500, journalize the entry to record

the sale.

(1)

2011 depreciation expense: $29,750 [($273,500 – $35,500)/8]

2012 depreciation expense: $29,750

2013 depreciation expense: $29,750

(2)

$184,250 [$273,500 – ($29,750 ´ 3)]

(3)

Cash

170,500

Accumulated Depreciation—Equipment

89,250

Loss on Disposal of Fixed Assets

13,750

Equipment

273,500

(4)

Cash

189,000

Accumulated Depreciation—Equipment

89,250

Equipment

273,500

Gain on Disposal of Fixed Assets

4,750

150. Chasteen Company acquired mineral rights for $9,100,000. The mineral deposit is estimated at 65,000,000

tons. During the current year, 18,375,000 tons were mined and sold.

Required:

(1)

Determine the amount of depletion expense for the current year.

(2)

Journalize the adjusting entry to recognize the depletion expense.

151. Icon Company acquired patent rights on January 1, 2009 for $1,125,000. The patent has a useful life equal

to its legal life of 15 years. On January 2, 2012, Icon successfully defended the patent in a lawsuit at a cost of

$90,000.

Required:

(1)

Determine the patent amortization expense for the current year ended December 31, 2012.

(2)

Journalize the adjusting entry to recognize the amortization.

(1)

$9,100,000/65,000,000 tons = $0.14 depletion per ton

18,375,000 ´ $0.14 = $2,572,500 depletion expense

(2)

Depletion Expense

2,572,500

Accumulated Depletion

2,572,500

152. The following information was taken from a recent annual report of Harrison Company: (in millions)

2012

2011

Land and buildings

$726

$361

Machinery, equipment, and internal-use software

595

470

Office furniture and equipment

94

81

Other fixed assets related to leases

760

569

Accumulated depreciation and amortization

894

644

Required:

(1)

Compute the book value of the fixed assets for the 2012 and 2011 and explain the differences, if any.

(2)

Would you normally expect the book value of fixed assets to increase or decrease during the year?

(1)

Property, Plant, and Equipment (in millions):

Current

Year

Land and buildings

$726

Machinery, equipment, and internal-use software

595

Office furniture and equipment

94

Other fixed assets related to leases

760

$2,175

Less accumulated depreciation

894

Book value

$1,281

153. On October 1, Sebastian Company acquired new equipment with a fair market value of

$458,000. Sebastian received a trade-in allowance of $92,000 on the old equipment of a similar type and paid

cash of $366,000. The following information about the old equipment is obtained from the account in the

equipment ledger: Cost, $336,000; accumulated depreciation on December 31, the end of the preceding fiscal

year, $220,000; annual depreciation, $20,000. Assuming the exchange has commercial substance, journalize

the entries to record: (a) the current depreciation of the old equipment to the date of trade-in and (b) the

exchange transaction on October 1.

154. On December 31, Bowman Company estimated that goodwill of $80,000 was impaired. In addition, a

patent with an estimated useful economic life of 10 years was acquired for $252,000 on June 1.

Required:

(1) Journalize the adjusting entry on December 31 for the impaired goodwill.

(2) Journalize the adjusting entry on December 31 for the amortization of the patent rights.

155. For each of the following fixed assets, determine the depreciation expense and the book value for the dates

requested:

Disposal date is N/A if asset is still in use.

Method: SL = Straight Line; DDB = Double Declining Balance

Assume the estimated life was 5 years for each asset.

Item

Cost

Residual Value

Purchase Date

Disposal date

Depr Method

Depr Expense 2011

A

$40,000

$4,000

7/1/2011

N/A

SL

B

$50,000

$5,000

1/1/2009

8/31/2011

SL

C

$60,000

$2,000

10/1/2011

N/A

DDB

D

$80,000

$10,000

1/1/2010

4/1/2011

DDB

156. Financial Statement data for the years ended December 31 for Parker Corporation is as follows:

2012 2011

Net Sales $2,595,600 $2,409,498

Fixed Assets:

Beginning of the year $ 901,070 $820,000

End of the year 829,330 901,070

Item

Cost

Residual Value

Purchase Date

Disposal Date

Depr Method

Depr Expense 2011

A

$40,000

$4,000

7/1/2011

N/A

SL

$3,600

B

$50,000

$5,000

1/1/2009

8/31/2011

SL

$6,000

C

$60,000

$2,000

10/1/2011

N/A

DDB

$6,000

D

$80,000

$10,000

1/1/2010

4/1/2011

DDB

$4,800

157. Fill in the missing numbers using the formula for Fixed Asset Turnover:

Company A

Company B

Company C

Company D

Net Sales

$5,000,000

$720,000

$900,000

?

Beginning Fixed Assets

$450,000

$275,000

?

$380,000

Ending Fixed Assets

$800,000

?

$310,000

$420,000

Fixed Asset Turnover

?

2.4 times

3 times

2.6 times

158. Williams Company acquired machinery on July 1, 2009, at a cost of $130,000. The estimated useful life

of the machinery was 10 years and the estimated residual value was $10,000. Williams uses the double-

declining-balance method of depreciation. On October 1, 2012, Williams sold the equipment for $75,000.

1) Record the journal entry for the depreciation on this machinery for 2012.

2) Record the journal entry for the sale of the machinery.

Company A

Company B

Company C

Company D

Net Sales

$5,000,000

$720,000

$900,000

$1,040,000

Beginning Fixed Assets

$450,000

$275,000

$290,000

$380,000

Ending Fixed Assets

$800,000

$325,000

$310,000

$420,000

Fixed Asset Turnover

8 times

2.4 times

3 times

2.6 times

159. Equipment was purchased on January 5, 2011, at a cost of $90,000. The equipment had an estimated

useful life of 8 years and an estimated residual value of $8,000.

After using the equipment for 3 years, the useful life was revised to a total of 10 years and the residual value

was reduced to $2,004.

Determine the straight-line depreciation expense for the year 2014 and following years.

160. Identify each of the following expenditures as chargeable to (a) Land, (b) Land Improvements, (c)

Buildings, (d) Machinery and Equipment, or (e) other account.

(1)

Cost of paving parking area for employees and customers.

(2)

Insurance during construction of building.

(3)

Interest incurred on loan during construction of building.

(4)

Fee paid for installation of equipment.

(5)

Special foundation for new equipment acquired.

(6)

Insurance on new equipment while in transit.

(7)

Freight charges on new equipment.

(8)

Cost of repairing vandalism damage to equipment during installation.

(9)

Sales tax on new equipment.

(10)

Cost incurred in repairing damage resulting from installation of new equipment.

(11)

Cost of land fill for building site.

(12)

Cost of lubricating oil purchased for periodic oil changes for equipment.

(13)

Parking lot lighting.

(14)

Installing a fence around the parking lot.

(15)

Repainting the trim on a building.

(16)

Special assessment paid to city for extension of water main to property.

(17)

Cost of razing and removing the old building on property acquired for a building site.

(18)

Delinquent real estate taxes assumed by purchaser on property acquired for a building site.

(19)

Attorney’s fee for title search.

(20)

Architect’s fee for building plans and supervision of construction.

161. Identify the following as a Fixed Asset (FA), or Intangible Asset (IA), or Natural Resource (NR), or

Neither (N)

(a)

computer

(b)

patent

(c)

oil reserve

(d)

goodwill

(e)

U. S. Treasury note

(f)

land used for employee parking

(g)

gold mine

(a) (f)

(b) (d)

(c) (g)

N

(e)

(a)

11, 16, 17, 18, 19

(b)

1, 13, 14

(c)

2, 3, 20

(d)

(e)

8, 10, 12, 15

162. A number of major structural repairs completed at the beginning of the current fiscal year at a cost of

$1,000,000 are expected to extend the life of a building 10 years beyond the original estimate. The original

cost of the building was $6,552,000, and it has been depreciated by the straight-line method for 25

years. Estimated residual value is negligible and has been ignored. The related accumulated depreciation

account after the depreciation adjustment at the end of the preceding fiscal year is $4,550,000.

(a)

What has the amount of annual depreciation been in past years?

(b)

What was the original life estimate of the building?

(c)

To what account should the $1,000,000 be debited?

(d)

What is the book value of the building after the extraordinary repairs have been made?

(e)

What is the expected remaining life of the building after the extraordinary repairs have been made?

(f)

What is the amount of straight-line depreciation for the current year, assuming that the repairs were completed at the very beginning of

the current year? Round to the nearest dollar.

163. Journalize each of the following transactions:

(a)

A wing costing $2,345,000 was added to the building. A new mortgage was issued for the cost.

(b)

Equipment was upgraded to increase its capacity to produce widgets. The upgrade cost of $11,500 was paid in cash.

(c)

A major overhaul costing $8,000 on a machine increased the useful life by 4 years. The payment was made in cash.

(a)

Building

2,345,000

Mortgage Payable

2,345,000

(b)

Equipment

11,500

Cash

11,500

(c)

Accumulated Depreciation-Machinery

8,000

Cash

8,000

$182,000 ($4,550,000 25)

36 years ($6,552,000 $182,000)

(c)

Accumulated Depreciation – Building

(d)

$3,002,000 ($6,552,000 + $1,000,000 – $4,550,000)

(e)

21 years (36 – 25 + 10)

$142,952 ($3,002,000 21)