Chapter 9 – Profit Planning

1. A strategic plan identifies strategies for future activities and operations, generally covering at least five years.

a.

True

b.

False

True

2. Budgets are financial plans for the future.

a.

True

b.

False

True

3. The master budget is composed of operating budgets and financial budgets.

a.

True

b.

False

True

4. Control is achieved by comparing actual results with budgeted results on a periodic basis.

a.

True

b.

False

True

5. Planning is looking ahead to see what actions should be taken to realize particular goals.

a.

True

b.

False

True

6. Budgets identify objectives and the actions needed to achieve them because they are foresighted financial plans.

a.

True

b.

False

True

7. A firm should develop a strategic plan before preparing a budget.

a.

True

b.

False

True

8. A firm acquires information that can be used to improve decision making from a budgetary system.

a.

True

b.

False

True

9. Comparing actual results with budgeted results on a periodic basis provides control in a budgetary system.

a.

True

b.

False

10. A large difference between actual and planned results is feedback that the system is providing adequate control.

Chapter 9 – Profit Planning

a.

True

b.

False

False

11. Communication and coordination are served by budgets.

a.

True

b.

False

True

12. The master budget is typically a comprehensive financial plan for the organization for the past fiscal year.

a.

True

b.

False

False

13. A continuous budget is a moving 12-month budget.

a.

True

b.

False

True

14. The department manager reviews the budget, provides policy guidelines and budgetary goals, and resolves differences

that arise as the budget is prepared, approves the final budget, and monitors the actual performance of the organization as

the year unfolds.

a.

True

b.

False

False

15. The budget director is the person responsible for directing and coordinating the organization’s overall budgeting

process.

a.

True

b.

False

True

16. The first budget to be prepared is the sales budget.

a.

True

b.

False

True

17. The production budget is prepared in units and in dollars.

a.

True

b.

False

False

The production budget is prepared in units only, not dollars.

18. The direct materials purchases budget is based on the sales budget.

a.

True

b.

False

Chapter 9 – Profit Planning

False

The direct materials purchases budget is based on the production budget.

19. There are as many direct materials purchases budgets as there are products.

a.

True

b.

False

False

20. The direct labor budget includes: units to be produced, direct labor time needed per unit, and total direct labor cost for

the period.

a.

True

b.

False

True

21. The selling and administrative expenses budget is part of the operating budgets.

a.

True

b.

False

True

22. The sales budget is used directly in the development of the production budget.

a.

True

b.

False

True

23. In preparing the direct labor budget, the average wage rate is used to calculate total direct labor cost.

a.

True

b.

False

True

24. The cash budget includes the beginning balance of cash, cash receipts, cash disbursements, and the ending balance of

cash.

a.

True

b.

False

True

25. If the initial cash budget indicates a cash deficiency, the company must go out of business.

a.

True

b.

False

False

26. Cash receipts must be at least as much as sales.

a.

True

b.

False

False

27. Cash budgets are often prepared monthly or even weekly.

Chapter 9 – Profit Planning

a.

True

b.

False

True

28. The output of the cost of goods sold budget is entered into the pro forma balance sheet.

a.

True

b.

False

False

The output of the cost of goods sold budget is entered into the pro forma income statement.

29. Individual behavior that is in basic conflict with the goals of the organization is called goal congruence.

a.

True

b.

False

False

30. Pseudoparticipation is one of the potential problems with participative budgeting.

a.

True

b.

False

True

31. Budgets should be based on ideal standards to encourage everyone to reach for the highest level of performance.

a.

True

b.

False

False

32. Ideally, managers are held accountable for controllable costs.

a.

True

b.

False

True

33. Myopic behavior is one of the advantages of participative budgeting.

a.

True

b.

False

False

34. Monetary incentives include salary increases, bonuses, and promotions.

a.

True

b.

False

True

35. __________________ is looking ahead to see what actions should be taken to realize particular goals.

Planning

36. The ________________ plots a direction for an organization’s future activities and operations; it generally covers at

least five years.

Chapter 9 – Profit Planning

37. Budgets improve _________________.

38. The _________________ is the comprehensive financial plan for the organization as a whole.

39. A __________________ is a moving 12-month budget.

40. The controller of the company usually serves as the __________________.

41. The cash budget and budgeted balance sheet are part of the ________________.

42. The _______________ tells how many units must be produced to meet sales needs and to satisfy ending inventory

requirements.

43. The __________________ shows the expected cost of all production costs other than direct materials and direct labor.

44. Salaries expense, advertising expense and depreciation expense would be included in the ______________________

budget.

45. The basic structure of a ______________ includes cash receipts, cash disbursements, any excess or deficiency of cash,

and financing.

46. _________________ consists of beginning cash balance and the expected cash receipts.

47. The alignment of managerial and organizational goals is often referred to as _______________.

48. ____________________ is individual behavior that is in basic conflict with the goals of the organization.

49. ______________ are the means an organization uses to influence a manager to exert effort to achieve an

organization’s goals.

50. Examples of ________________ include job enrichment, increased responsibility and autonomy, and recognition

programs.

Chapter 9 – Profit Planning

51. _____________________ allows subordinate managers considerable say in how the budgets are established.

Participative budgeting

52. ___________________ exists when a manager deliberately underestimates revenues or overestimates cost in an effort

to make the future period appear less attractive in the budget than they think it will be in reality.

53. When top management assumes total control of the budgeting process and only seeks superficial participation from

lower-level managers this is known as ________________.

54. _________________ are used to ensure that budgeted costs can be realistically compared with costs for actual levels

of activity.

Flexible budgets

55. Which of the following is an advantage of budgeting?

a.

Forces managers to plan.

b.

Provides information useful for control.

c.

Provides information for improved decision making.

d.

Improves communication.

e.

All of these.

56. Which of the following is a use of budgets for control?

a.

Plans can be made for the future.

b.

If conditions change between the formation of the budget and the current time, budgets can be quickly

adapted.

c.

Budgets set a standard against which results can be compared.

d.

Communication is improved.

e.

All of these.

57. Which of the following budgets can be used for control?

a.

Production budget

b.

Cash budget

c.

Budgeted income statement

d.

Selling and administrative expense budget

e.

All of these

58. In a (n) ____, as one month expires, an additional month in the future is added to the budget so that the company

always has a 12-month plan on hand.

a.

continuous budget

b.

financial budget

c.

operational budget

d.

yearly budget

Chapter 9 – Profit Planning

e.

master budget

a

59. The ____ is the person responsible for directing and coordinating the organization’s overall budget process.

a.

budget master

b.

controller

c.

chief financial planner

d.

budget director

e.

chief accountant

60. Looking backward to determine what actually happened and comparing it with the previously planned outcomes is

a.

control.

b.

communicating.

c.

decision making.

d.

strategic planning.

e.

budgeting.

a

61. Budgets are

a.

key components of planning.

b.

financial plans for the future.

c.

an identifier of objectives and the actions needed to achieve them.

d.

used for communication and coordination.

e.

all of these.

e

62. The master budget is

a.

the selective financial plan for the organization as a whole.

b.

typically for a 1-year period corresponding to the fiscal year of the company.

c.

broken down into daily and weekly budgets.

d.

used for misinformation and coordination.

e.

all of these.

63. Which of the following is not true?

a.

The sales forecast is done before the sales budget.

b.

The master budget is the comprehensive plan for the organization as a whole.

c.

The production budget is prepared in units and dollars.

d.

One approach to forecasting sales is the bottom-up approach.

e.

In creating the sales forecast, outside factors such as the state of the economy, should be considered.

c

64. The first step in creating the master budget is the creation of the

a.

production budget.

Chapter 9 – Profit Planning

b.

direct labor budget.

c.

cash budget.

d.

sales budget.

e.

budgeted income statement.

65. The budget that describes how many units must be produced in order to meet sales needs and ending inventory

objectives is the

a.

production budget.

b.

direct materials purchases budget.

c.

cash budget.

d.

budgeted income statement.

e.

none of these.

66. Direct materials needed for production is calculated by

a.

multiplying units to be produced by direct materials per unit.

b.

subtracting units to be produced from direct materials per unit.

c.

dividing units to be produced by direct materials per unit.

d.

adding units to be produced to direct materials per unit.

e.

subtracting direct materials per unit from units to be produced.

67. In preparing the overhead budget, many companies use

a.

activity-based costing.

b.

multiple drivers for a simple budget.

c.

participative costing.

d.

a unit-based driver such as direct labor hours.

e.

none of these.

68. Which of the following statements is true?

a.

The overhead budget is typically composed of variable overhead and fixed overhead.

b.

The direct labor budget uses an average wage rate for direct labor.

c.

The production budget is not converted into dollars.

d.

The sales budget includes both units and dollars.

e.

All of these.

69. The ending finished goods inventory budget supplies information needed for the

a.

sales budget.

b.

cash budget.

c.

budgeted income statement.

d.

cost of goods sold budget.

e.

all of these.

Chapter 9 – Profit Planning

70. Which of the following budgets are needed to calculate a budgeted unit cost?

a.

Direct materials purchases budget

b.

Direct labor budget

c.

Overhead budget

d.

Direct materials purchases budget and overhead budget

e.

Direct materials purchases budget, direct labor budget, and overhead budget

e

71. The selling and administrative expenses budget includes

a.

cost of goods sold.

b.

overhead.

c.

fixed production expense.

d.

variable cost of selling.

e.

all of these.

72. Budgeted operating income includes

a.

budgeted interest expense.

b.

budgeted income taxes.

c.

budgeted cost of goods sold.

d.

budgeted net income.

e.

none of these.

c

73. Depreciation expense on sales equipment appears in a separate line on which of the following budgets?

a.

Cash budget

b.

Selling and administrative expenses budget

c.

Direct labor budget

d.

Production budget

e.

Overhead budget

74. Rodriquez Company budgeted the following sales in units:

January

30,000

February

20,000

March

40,000

Rodriquez’s policy is to have 20% of the following month’s sales in inventory. On January 1, inventory equaled 7,500

units. February production in units is

a.

20,000.

b.

28,000.

c.

40,000.

d.

26,500.

Chapter 9 – Profit Planning

e.

24,000.

Sales

30,000

20,000

+ Desired EI

Units needed

34,000

28,000

Production

26,500

24,000

75. A company has had stable sales and production for several years. Next year, sales are expected to increase by at least

50%. Assuming that the company maintains its policy for desired ending inventories of finished product and direct

materials purchases, what will be the likely effect on the desired ending inventory of finished product?

a.

It will increase

b.

It will decrease

c.

It will stay the same

d.

It will be twice the size of the desired ending inventory of raw materials

e.

None of these

a

76. A company expects the following sales for the coming year:

1st Quarter

2nd Quarter

3rd Quarter

4th Quarter

Units

40,000

30,000

60,000

80,000

Average selling price

$5

$5

$5

$6

Budgeted sales revenue for the year is

a.

$1,050,000

b.

$1,260,000

c.

$1,155,000

d.

$1,130,000

e.

it is impossible to tell from this information

Budgeted sales = [(40,000 + 30,000 + 60,000) × $5] + (80,000 × $6) = $1,130,000

77. A company provided the following information on sales for the coming year:

1st Quarter

2nd Quarter

3rd Quarter

4th Quarter

Units

40,000

40,000

30,000

80,000

Average selling price

$5

$5

$5

$6

Assuming that the beginning inventory is 3,000 units, and that the company policy is to have 25% of the next quarter’s

sales in ending inventory, which quarter will have the lowest production?

a.

Quarter 4

b.

Quarter 3

c.

Quarter 2

d.

Quarter 1

e.

All quarters have the same production

Chapter 9 – Profit Planning

78. Belant Company budgeted 200,000 units of production for June, 210,000 units for July and 300,000 units for August.

Each unit requires 0.25 direct labor hours. How many direct labor hours are budgeted for August?

a.

50,000

b.

5,000

c.

75,000

d.

52,500

e.

300,000

Direct labor hours = 0.25 × 300,000 = 75,000

79. In budgeting direct labor hours for the coming year, it is important to

a.

multiply production in units by the direct labor hours per unit.

b.

divide production in units by the direct labor hours per unit.

c.

subtract production in units from the direct labor hours per unit.

d.

subtract direct labor hours per unit from production in units.

e.

multiply production in units by the labor wage rate.

a

80. Galvern Company provided the following data for July:

Direct materials

$50,000

Direct labor

$25,000

Overhead

$90,000

Beginning finished goods

$15,000

Ending finished goods

$34,000

Production in units

10,000

What is the cost of goods sold?

a.

$165,000

b.

$146,000

c.

$214,000

d.

$184,000

e.

$75,000

Cost of goods sold = $165,000 + $15,000 − $34,000 = $146,000

81. A production budget is most important for which of the following?

a.

retail stores

b.

manufacturing firms

Sales

40,000

40,000

30,000

80,000

+ Desired ending inventory

10,000

20,000

Units needed

50,000

47,500

50,000

Production

47,000

37,500

42,500

Chapter 9 – Profit Planning

c.

not-for-profit agencies

d.

local government agencies

e.

all of these

82. A company requires 200 pounds of plastic to meet the production needs of a product. It currently has 20 pounds of

plastic inventory. The desired ending inventory of plastic is 60 pounds. How many pounds of plastic should be budgeted

for purchasing during the coming period?

a.

200 pounds

b.

240 pounds

c.

260 pounds

d.

280 pounds

e.

160 pounds

Pounds of plastic to purchase = 200 + 60 − 20 = 240

83. A company plans on selling 400 units. The selling price per unit is $5. There are 40 units in beginning inventory, and

the company would like to have 75 units in ending inventory. How many units should be produced for the coming period?

a.

435

b.

400

c.

365

d.

2,000

e.

2,035

Units to produce = 400 + 75 − 40 = 435

84. A company has provided a sales budget for the next four months. It bases its production budget on the sales budget,

and has a policy that each month’s ending inventory of finished product must be equal to 25% of the following month’s

sales needs. The direct materials purchases budget is based on the production budget. The company’s policy for each

month’s ending inventory of raw materials is that they must be equal to 10% of the following month’s production needs for

raw materials. Given this information, the company can prepare direct materials purchases budgets for how many months?

a.

One

b.

Two

c.

Three

d.

Four

e.

Five

85. Which of the following is the most common starting point in the information gathering process for budgeting?

a.

The personnel forecast

b.

The sales forecast

c.

The production forecast

Chapter 9 – Profit Planning

d.

The projected income statement

86. Which of the following is an operating budget?

a.

Budgeted statement of cash flows

b.

Capital expenditures budget

c.

Budgeted income statement

d.

Cash budget

c

87. What is the formula used to compute the units to be produced?

a.

Units produced = Units sold

b.

Units produced = Units sold + Units in beginning inventory + Units in ending inventory

c.

Units produced = Units sold + Units in beginning inventory − Units in ending inventory

d.

Units Produced = Units sold − Units in beginning inventory + Units in ending inventory

88. Candace Company produces and sells pillows. It expects to sell 10,000 pillows in the next year and had 1,000 pillows

in finished goods inventory at the end of the prior year. Candace would like to complete operations next year with at least

1,250 completed pillows in inventory. There is no ending work-in-process inventory. The pillows sell for $5 each. How

many pillows would be produced in the next year?

a.

10,000 pillows

b.

11,000 pillows

c.

11,250 pillows

d.

10,250 pillows

89. Bright Lamp Company manufactures lamps. The estimated number of lamp sales for the last three months of the

current year are as follows:

Month

Sales

October

10,000

November

14,000

December

13,000

Finished goods inventory at the end of September was 3,000 units. Ending finished goods inventory is budgeted to equal

25% of the next month’s sales. Bright Lamp expects to sell the lamps for $25 each. In January of the next year, sales are

projected at 16,000 lamps. How many lamps should be produced in November?

a.

11,000 lamps

b.

10,500 lamps

c.

14,000 lamps

d.

13,750 lamps

90. In going from the sales budget to the production budget, adjustments to the sales budget need to be made for

Chapter 9 – Profit Planning

a.

finished goods inventories.

b.

cash receipts.

c.

factory overhead costs.

d.

selling expenses.

a

91. Watson Corporation manufactures boxes. The estimated numbers of boxes sold for the first three months of the

current year are as follows:

Month

Sales

January

3,000

February

4,200

March

3,900

Finished goods inventory at the end of December was 600 units. Ending finished goods inventory is equal to 20% of the

next month’s sales. Watson Corporation expects to sell the boxes for $5 each. April sales are projected at 4,500 boxes.

How many boxes should be produced in February?

a.

4,140 boxes

b.

4,200 boxes

c.

4,260 boxes

d.

3,900 boxes

SUPPORTING CALCULATIONS:

Figure 9-1.

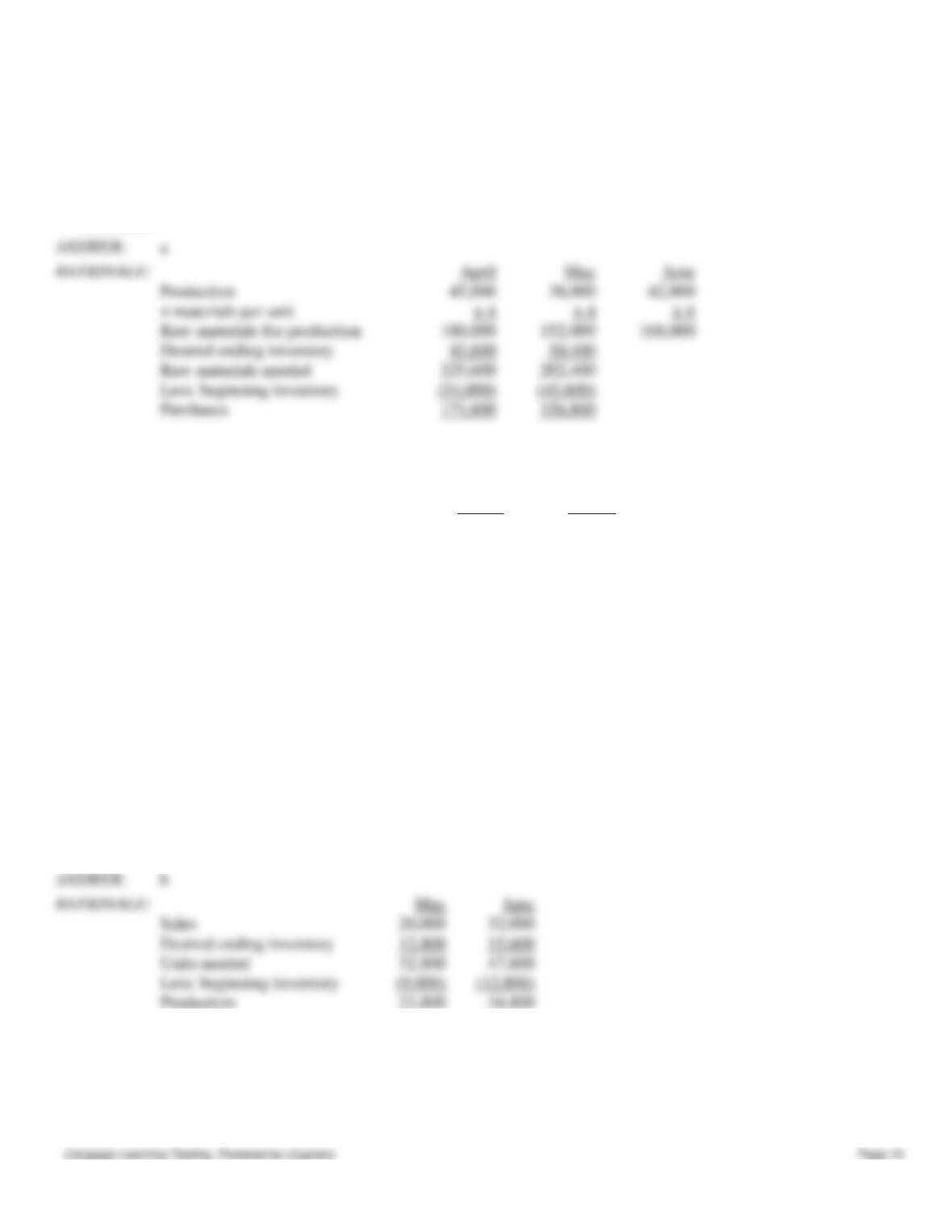

Saphire Company budgeted the following production in units for the second quarter of the year:

April

45,000

May

38,000

June

42,000

Each unit requires four pounds of raw material. Saphire’s policy is to have 30% of the following month’s production needs

for materials in inventory. This policy was met in March.

92. Refer to Figure 9-1. Raw materials purchases budgeted for May in pounds equal:

a.

156,800

b.

202,400

c.

45,600

d.

171,600

e.

225,600

Production

× materials per unit

Raw materials for production

Desired ending inventory

Raw materials needed

Less: beginning inventory

Purchases

Chapter 9 – Profit Planning

93. Refer to Figure 9-1. Desired ending inventory for April in pounds equals:

a.

45,600

b.

11,400

c.

10.500

d.

38,300

e.

54,000

April

Production

× materials per unit

Raw materials for production

Desired ending inventory

Raw materials needed

Less: beginning inventory

Purchases

Figure 9-2.

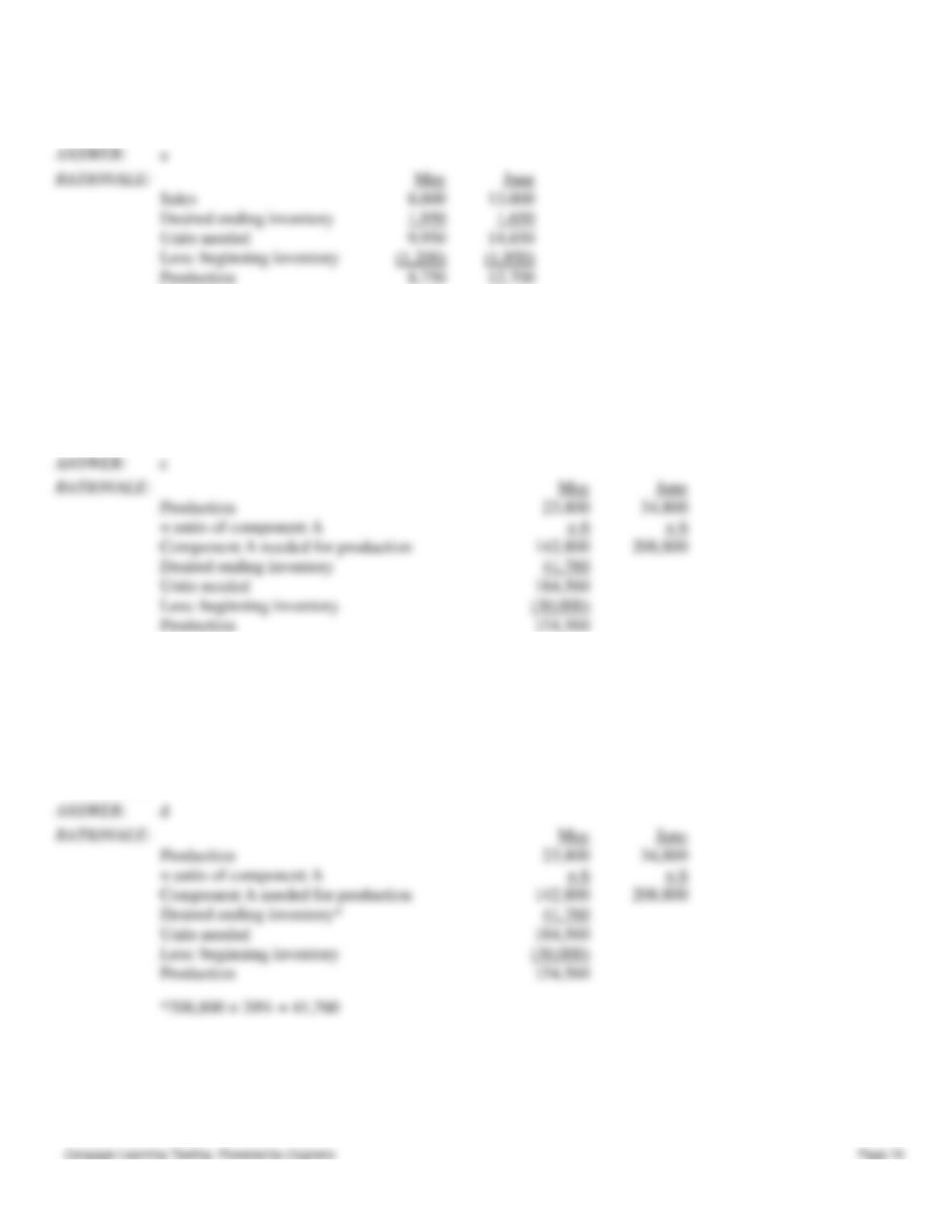

Kenner Company produces two products: SR200 and TX500. Budgeted sales for four months are as follows:

SR200

TX500

May

8,000

20,000

June

13,000

32,000

July

11,000

39,000

August

18,000

46,000

Kenner’s ending inventory policy is that SR200 should have 15% of next month’s sales in ending inventory and TX500

should have 40% of next month’s sales in ending inventory. On May 1, there were 1,200 units of SR200 and 9,000 units of

TX500.

TX500 requires 6 units of component A. (SR200 does not use component A.) There were 30,000 units of component A in

inventory on May 1. Kenner wants to have 20% of the following month’s production needs in inventory for Component A.

94. Refer to Figure 9-2. How many units of TX500 are budgeted for production in June?

a.

47,600

b.

34,800

c.

32,000

d.

45,000

e.

12,800

Sales

Desired ending inventory

Units needed

Less: beginning inventory

Production

95. Refer to Figure 9-2. What is the budgeted production of SR200 for May in units?

a.

8,750

b.

9,950

c.

8,000

Chapter 9 – Profit Planning

d.

1,200

e.

10,500

Sales

Production

96. Refer to Figure 9-2. What is the budgeted amount of component A to be purchased in May?

a.

41,760

b.

142,800

c.

154,560

d.

164,600

e.

66,600

Production

Production

97. Refer to Figure 9-2. What is the desired ending inventory of component A for May?

a.

86,000

b.

180,000

c.

58,500

d.

41,760

e.

30,000

Production

Production

Figure 9-3.

Zion Company manufactures sneakers. Production of their new sneaker for the coming three months is budgeted as

follows:

August

26,000

Chapter 9 – Profit Planning

September

48,000

October

31,000

Each sneaker requires 1.5 hours of direct labor time. Direct labor wages average $13 per hour. Monthly overhead averages

$8 per direct labor hour plus fixed overhead of $4,300.

98. Refer to Figure 9-3. What is the direct labor cost budgeted for September?

a.

$820,000

b.

$750,000

c.

$140,000

d.

$936,000

e.

$625,000

September direct labor cost = 48,000 × 1.50 × $13 = $936,000

99. Refer to Figure 9-3. What is the total overhead budgeted for the month of September?

a.

$680,000

b.

$580,300

c.

$142,100

d.

$460,000

e.

$362,100

Budgeted overhead = ($8 × 48,000 × 1.50) + $4,300 = $580,300

Figure 9-4.

Bickford Company plans to sell 135,000 units in November and 180,000 units in December. Bickford’s policy is that 10%

of the following month’s sales must be in ending inventory. On November 1, there were 14,000 units in inventory.

It takes 30 minutes of direct labor time to make one unit. Direct labor wages average $17 per hour. Variable overhead is

applied at the rate of $5 per direct labor hour. Fixed overhead is budgeted at $56,500 per month.

100. Refer to Figure 9-4. What is the direct labor cost budgeted for November?

a.

$1,181,500

b.

$950,600

c.

$707,600

d.

$2,152,000

e.

$622,800

101. Refer to Figure 9-4. What is the budgeted production in units for November?

a.

100,000

b.

140,000

c.

121,000

Chapter 9 – Profit Planning

d.

125,600

e.

139,000

November production = 135,000 + (0.10 × 180,000) − 14,000 = 139,000 units

102. Refer to Figure 9-4. What is the budgeted overhead for November?

a.

$444,500

b.

$280,700

c.

$404,000

d.

$348,420

e.

$192,920

Figure 9-5.

Sully Company provided the following information for last month.

Production in units

3,000

Direct materials cost

$7,000

Direct labor cost

$10,000

Overhead cost

$9,600

Sales commission per unit sold

$4

Price per unit sold

$29

Fixed selling and administrative expense

$7,000

There were no beginning and ending inventories.

103. Refer to Figure 9-5. What is Sully’s cost of goods sold per unit?

a.

$12.60

b.

$8.87

c.

$10.00

d.

$12.50

e.

$16.60

Direct materials cost

Direct labor cost

Overhead cost

Total manufacturing costs

Units produced

Cost of goods sold per unit

104. Refer to Figure 9-5. What is gross margin for Sully Company last month?

a.

$54,000

b.

$64,600

c.

$32,400

d.

$47,400

Chapter 9 – Profit Planning

e.

$60,400

Sales ($29 × 3,000)

Cost of goods sold ($7,000 + 10,000 + 9,600)

Gross margin

105. Refer to Figure 9-5. What is operating income for Sully Company for last month?

a.

$24,000

b.

$34,600

c.

$49,400

d.

$27,400

e.

$41,400

Sales ($29 × 3,000)

Cost of goods sold ($7,000 + 10,000 + 9,600)

Gross margin

Less: commission ($4 × 3,000)

Less: fixed selling and admin. expense

Operating income

Figure 9-10.

Connor Company produces speaker systems for cars. Estimated sales (in units) in January are 40,000; in February 37,000;

and in March 34,000. Each unit is priced at $60. Connor wants to have 35% of the following month’s sales in ending

inventory. That requirement was met on January 1.

Each speaker system requires 3 boxes and 15 yards of wire. Boxes cost $4 each and wire is $0.60 per yard. Connor wants

to have 20% of the following month’s production needs in ending raw materials inventory. On January 1, Connor had

24,000 boxes and 100,000 yards of wire in inventory.

106. Refer to Figure 9-10. What is Connor’s expected sales revenue for February?

a.

$2,020,000

b.

$1,900,000

c.

$60

d.

$1,125,000

e.

$2,220,000

February revenue = 37,000 × $60 = $2,220,000

107. Refer to Figure 9-10. How many units does Connor expect to produce in February?

a.

25,700

b.

30,500

c.

23,750

d.

35,950

e.

25,000

Sales

Desired ending inventory (35%)

Chapter 9 – Profit Planning

108. Refer to Figure 9-10. How many boxes does Connor expect to purchase in January?

a.

159,650

b.

114,420

c.

214,550

d.

148,500

e.

138,420

Production

× raw materials per unit

Raw materials for production

Desired ending inventory

Units needed

Less: beginning inventory

Purchases in units

Figure 9-11.

Pallen Company estimated sales of 11,000 units at $40 each, unit cost of goods sold of $22, marketing expense of $65,000

and a 10% commission on each unit sold. Administrative expense is budgeted at $50,000.

109. Refer to Figure 9-11. What is total selling expense?

a.

$65,000

b.

$44,000

c.

$84,000

d.

$109,000

e.

$39,000

110. Refer to Figure 9-11. What is Pallen’s budgeted operating income?

a.

$281,000

b.

$39,000

c.

$198,000

d.

$83,000

e.

$440,000

111. Budgets are prepared in which of the following orders?

Units needed

Less: beginning inventory

Production