119. Mulligan Company uses standard costing for direct materials and direct labor. Management would like to

use standard costing for variable and fixed overhead.

The following monthly cost functions were developed for manufacturing overhead items:

Overhead Item

Cost Function

Indirect materials

$1.00 per DLH

Indirect labor

$1.25 per DLH

Utilities

$0.50 per DLH

Insurance

$10,000

Depreciation

$40,000

The cost functions are considered reliable within a relevant range of 20,000 to 40,000 direct labor hours. The company expects to operate at 25,000

direct labor hours per month.

Information for the month of June is as follows:

Actual overhead costs incurred:

Indirect materials

$ 20,000

Indirect labor

30,000

Utilities

12,000

Insurance

11,000

Depreciation

40,000

Total

$113,000

Actual direct labor hours worked:

24,000

Standard direct labor hours allowed for production achieved:

27,000

Required:

a.

Calculate the following standard manufacturing overhead rates based upon expected capacity:

Variable manufacturing overhead

Fixed manufacturing overhead rate

Total manufacturing overhead rate

b.

Calculate the following variances:

Variable overhead spending variance

Variable overhead efficiency variance

Fixed overhead spending variance

Fixed overhead volume variance

c.

Prepare the journal entries to record and apply overhead costs.

120. United Carborundum Company manufactures 100-pound bags of chemicals that have the following unit

standard costs for direct materials and direct labor:

Direct materials (100 lbs. @ $1.00 per lb.)

$100.00

Direct labor (0.5 hours at $24 per hour)

12.00

Total standard direct cost per 100 lb. bag

$112.00

The following activities were recorded for October:

•

1,000 bags were manufactured.

•

95,000 lbs. of materials costing $76,000 were purchased.

•

102,500 lbs. of materials were used.

•

$12,000 was paid for 475 hours of direct labor.

There were no beginning or ending work-in-process inventories.

Required:

a.

Compute the direct materials variances.

b.

Compute the direct labor variances.

c.

Give possible reasons for the occurrence of each of the preceding variances.

a.

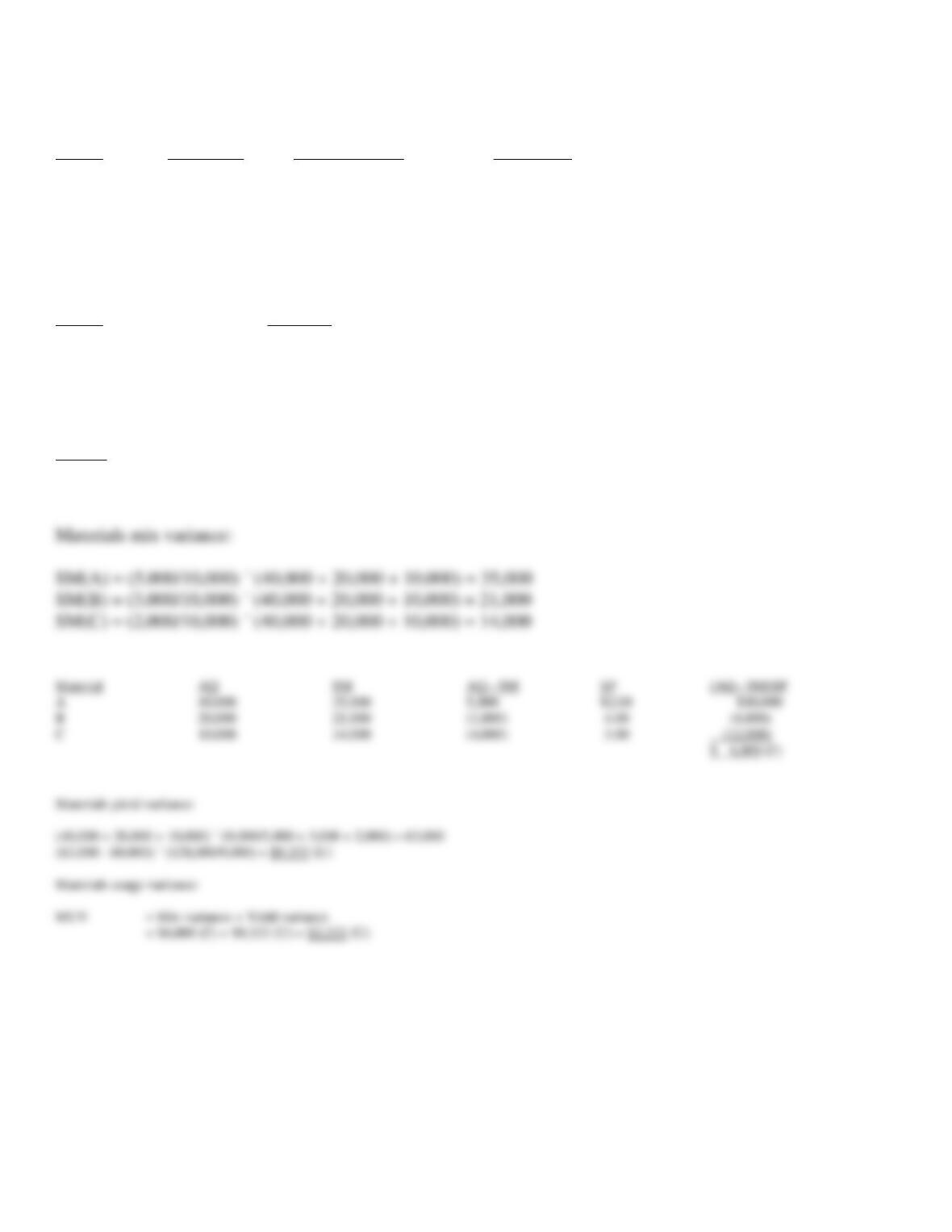

Material price variance:

[$76,000 – (95,000 ´ $1.00)] = $19,000 F

Material usage variance

[102,500 – 1,000(100)] ´ $1.00 = $2,500 U

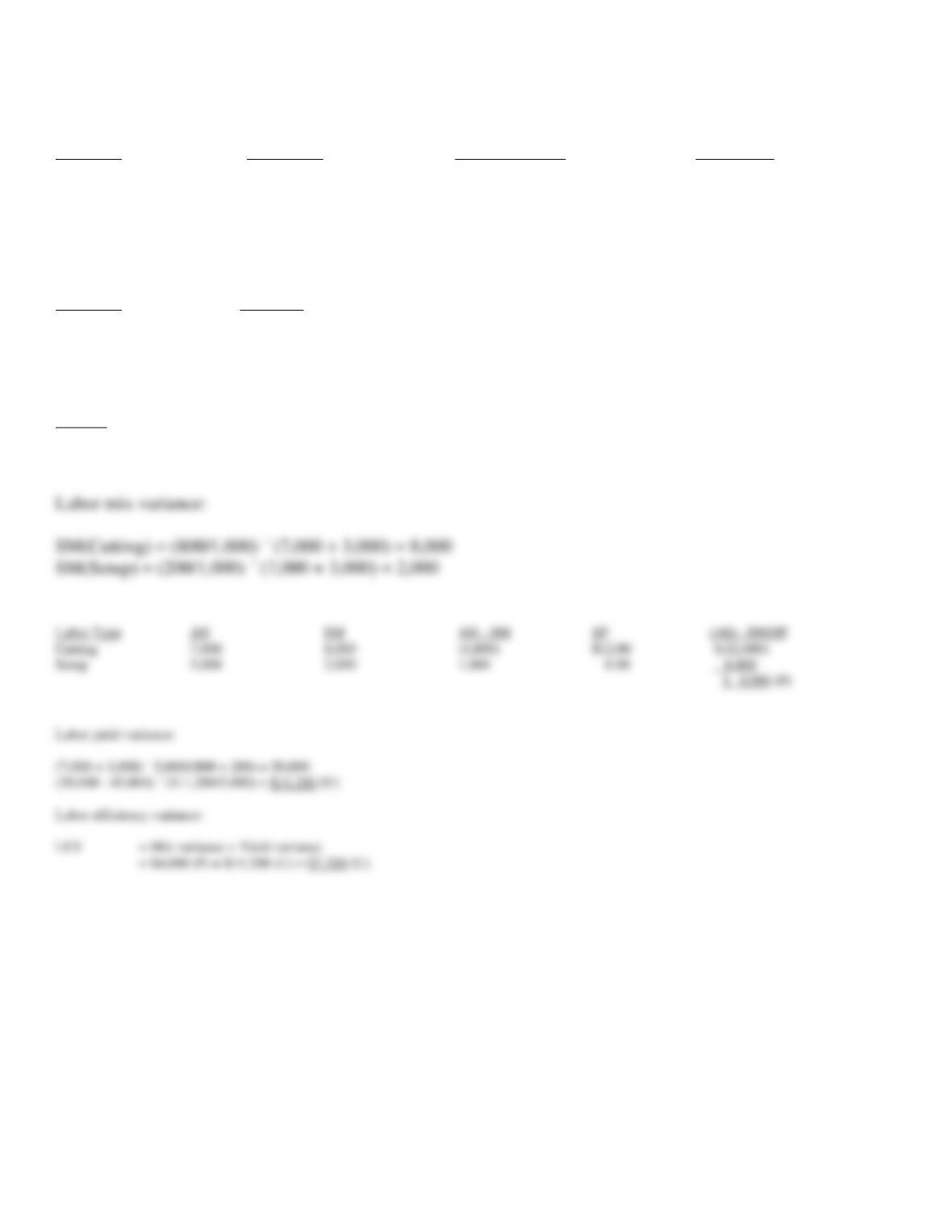

Labor rate variance

[$12,000 – (475 hrs. ´ $24)] = $600 U

Labor efficiency variance

[(0.5 ´ 1,000) – 475 hrs.]$24 = 600 F

Material usage variance:

Low-quality materials; lower skilled workers; less efficient machines; low employee morale.

Labor rate variance:

Higher skilled workers; longer tenured workers with higher wages.

The firm could be using a more experienced work force than desired.

121. Glenville Company manufactures a single product that has a standard materials cost of $20 (4 units of

materials at $5 per unit), standard direct labor cost of $9 (1 hour per unit), and standard variable overhead cost

of $4 (based on direct labor hours). Fixed overhead is budgeted at $17,000 per month. The following data

pertain to operations for May 2014:

Materials purchased:

8,000 units costing $39,400

Materials used in production of 1,500 units of finished product:

6,200 units of materials

Direct labor used:

1,500 hours costing $15,000

Variable overhead costs incurred:

$5,960

Fixed overhead costs incurred:

$17,500

Required:

a.

Prepare a performance report for Glenville for May using the following headings:

1. Actual Production Costs

2. Flexible Budget Costs

3. Flexible Budget Variances

b.

Compute the following variances (show calculations):

1. Materials usage variance

2. Labor rate variance

3. Labor efficiency variance

4. Variable overhead spending variance

5. Variable overhead efficiency variance

6. Fixed overhead budget variance

c.

Give one possible explanation for each of the six variances computed in part (b).

122. Stammer Company uses three materials in the production of their product. The materials, A, B, and C,

have the following standards:

Material

Standard Mix

Standard Unit Price

Standard Cost

A

5,000 units

$2.00 per unit

$10,000

B

3,000 units

4.00 per unit

$12,000

C

2,000 units

3.00 per unit

$ 6,000

Yield

9,000 units

During April, the following actual production information was provided:

Material

Actual Mix

A

40,000 units

B

20,000 units

C

10,000 units

Yield 60,000 units

Required:

Calculate the materials usage, mix, and yield variances.

Material

(AQ – SM)SP

A

40,000

35,000

5,000

$2.00

$10,000

B

20,000

21,000

(1,000)

4.00

(4,000)

C

10,000

14,000

(4,000)

3.00

(12,000)

$ 6,000 (F)

MUV

= Mix variance + Yield variance

= $6,000 (F) + $9,333 (U) = $3,333 (U)

123. Compare and contrast mix and yield variances.

124. LaPointe Corporation uses two different types of labor to manufacture its product. The types of labor,

Cutting and Setup, have the following standards:

Labor Type

Standard Mix

Standard Unit Price

Standard Cost

Cutting

800 hours

$12.00 per unit

$9,600

Setup

200 hours

8.00 per unit

$1,600

Yield

5,000 units

During January, the following actual production information was provided:

Labor Type

Actual Mix

Cutting

7,000 hours

Setup

3,000 hours

Yield

45,000 units

Required:

Calculate the labor efficiency and mix and yield variances.

Labor Type

(AQ – SM)SP

Setup

3,000

2,000

1,000

8.00

8,000

$ 4,000 (F)

= Mix variance + Yield variance

= $4,000 (F) + $11,200 (U) = $7,200 (U)

125. The following information is provided about three materials utilized in the production of a product:

Material

Standard Mix

Standard Unit Price

Standard Cost

X

2,500 units

$3.00 per unit

$7,500

Y

1,500 units

5.00 per unit

$7,500

Z

1,000 units

4.00 per unit

$4,000

Yield 4,500 units

During May, the following actual production information was provided:

Material

Actual Mix

X

20,000 units

Y

10,000 units

Z

5,000 units

Yield 30,000 units

Required:

Calculate the materials mix and yield variances.

Material

(AQ – SM)SP

X

20,000

17,500

2,500

$3.00

$7,500

Y

10,000

10,500

(500)

5.00

(2,500)

Z

5,000

7,000

(2,000)

4.00

(8,000)

$ 3,000 (F)

126. Organics Corporation uses two different types of labor to manufacture its product. The types of labor,

Cutting and Setup, have the following standards:

Labor Type

Standard Mix

Standard Unit Price

Standard Cost

Cutting

400 hours

$6.00 per unit

$2,400

Setup

100 hours

4.00 per unit

$ 400

Yield 2,500 units

During July, the following actual production information was provided:

Labor Type

Actual Mix

Cutting

3,500 hours

Setup

1,500 hours

Yield 22,500 units

Required:

Calculate the labor mix and yield variances.

Labor Type

(AQ – SM)SP

Setup

1,500

1,000

4.00

2,000

$ 1,000 (F)

127. Production of a product utilizes materials D, E, and F. The following are their standards:

Material

Standard Mix

Standard Unit Price

Standard Cost

D

6,000 units

$1.00 per unit

$6,000

E

4,000 units

2.00 per unit

$8,000

F

2,000 units

1.50 per unit

$ 3,000

Yield 8,000 units

During August, the following actual production information was provided:

Material

Actual Mix

D

37,000 units

E

17,000 units

F

7,000 units

Yield 50,000 units

Required:

Calculate the materials mix, yield, and usage variances.

Material

(AQ – SM)SP

D

37,000

30,500

6,500

$1.00

$6,500

E

17,000

20,333

(3,333)

2.00

(6,666)

F

7,000

10,167

(3,167)

1.50

(4,751)

$ 4,917 (F)

MUV

= Mix variance + Yield variance

= $4,917 (F) + $19,833 (F) = $24,750 (F)

128. Mozambique Industries uses two different types of labor to manufacture its product. The types of labor,

Cutting and Setup, have the following standards:

Labor Type

Standard Mix

Standard Unit Price

Standard Cost

Cutting

200 hours

$12.00 per unit

$2,400

Setup

800 hours

8.00 per unit

$6,400

Yield 4,000 units

During September, the following actual production information was provided:

Labor Type

Actual Mix

Cutting

7,000 hours

Setup

3,000 hours

Yield 42,000 units

Required:

Calculate the labor mix and yield variances.

Labor Type

(AQ – SM)SP

Setup

3,000

8,000

(5,000)

8.00

$(40,000)

$ 20,000 (U)

129. The Stronghold Corporation uses two materials and two types of labor to manufacture a product. The

following are their standards:

Material

Standard Mix

Standard Unit Price

Standard Cost

P

5,500 units

$2.00 per unit

$ 8,000

Q

4,500 units

5.00 per unit

$22,500

Yield

5,000 units

Labor Type

Standard Mix

Standard Unit Price

Standard Cost

Grinding

300 hours

$8.00 per unit

$2,400

Polishing

150 hours

6.00 per unit

$ 900

Yield

6,000 units

During the month of November, the following actual production information was provided:

Material

Actual Mix

P

30,000 units

Q

20,000 units

Yield

30,000 units

Labor Type

Actual Mix

Grinding

4,500 hours

Polishing

2,500 hours

Yield

30,000 units

Required calculations:

a. Material mix variance

b. Material yield variance

c. Labor mix variance

d. Labor yield variance

Material

(AQ – SM)SP

P

30,000

27,500

2,500

$2.00

$ 2,500

Q

20,000

22,500

$(2,500)

5.00

(12,500)

$10,000 (F)