63. Tyson Construction Inc.

Use the information provided for Tyson Construction Inc. to answer the following question(s) using the

effective interest method.

On January 2, 2012, Tyson Construction Inc. issued $1,000,000, 10-year bonds for $1,135,915. The bonds pay

interest on June 30 and December 31. The stated rate is 10% and the market rate is 8%.

Refer to the information provided for Tyson Construction Inc. What amount besides the interest payment

would Tyson repay its bondholders on the maturity date?

64. Flounder Inc.

Use the information provided for Flounder Inc. to answer the question(s) using the effective interest method.

On January 1, 2012, Flounder Inc. issued $800,000, 10-year, 9% bonds for $662,356. The bonds pay interest on

June 30 and December 31. The market rate is 12%.

Refer to the information provided for Flounder Inc. The interest expense on the bonds at June 30, 2012, is:

65. Flounder Inc.

Use the information provided for Flounder Inc. to answer the question(s) using the effective interest method.

On January 1, 2012, Flounder Inc. issued $800,000, 10-year, 9% bonds for $662,356. The bonds pay interest on

June 30 and December 31. The market rate is 12%.

Refer to the information provided for Flounder Inc. The interest payment on June 30, 2012, is:

66. Flounder Inc.

Use the information provided for Flounder Inc. to answer the question(s) using the effective interest method.

On January 1, 2012, Flounder Inc. issued $800,000, 10-year, 9% bonds for $662,356. The bonds pay interest on

June 30 and December 31. The market rate is 12%.

Refer to the information provided for Flounder Inc. What is the carrying value of the bonds after the first

interest payment is made on June 30, 2012?

67. Flounder Inc.

Use the information provided for Flounder Inc. to answer the question(s) using the effective interest method.

On January 1, 2012, Flounder Inc. issued $800,000, 10-year, 9% bonds for $662,356. The bonds pay interest on

June 30 and December 31. The market rate is 12%.

Refer to the information provided for Flounder Inc. What is the carrying value of the bonds at the end of the

68. With the effective interest method of amortization, the amortization of a bond discount results in a(n):

69. With the effective interest method of amortization, the amortization of a bond premium results in a(n)

70. On January 2, 2012, Golden Corporation sold $800,000 of bonds for $785,000. The bonds will mature in 10

years and pay interest annually on December 31. Golden properly recorded the payment of interest and

amortization of the discount using the effective interest method. Which of the following statements is true about

the carrying value of the bonds and/or the unamortized discount at the end of 2012?

71. Creative Products Company

The following question(s) are based on items that might appear on the balance sheet of a company like the

Creative Products Company. Identify how each item would be most likely classified on its balance sheet.

Refer to the information provided for Creative Products Company. Premium on Bonds Payable will appear as:

72. Creative Products Company

The following question(s) are based on items that might appear on the balance sheet of a company like the

Creative Products Company. Identify how each item would be most likely classified on its balance sheet.

Refer to the information provided for Creative Products Company. Current portion of long-term debt will

appear as a:

73. On January 1, 2012, Upgrade Co. issued $1,000,000 of 10 percent bonds at face value. These bonds are due

in five years with interest payable annually on December 31.

Required:

A)

Provide the journal entry necessary to recognize the interest expense on December 31, 2012-2016.

B)

Provide the journal entry to record the repayment of the loan principal on December 31, 2016.

74. On January 1, 2012, Investor Corporation issued $10,000,000, 10-year, 5% bonds at 85. Interest payments

are made annually.

Required:

A)

Give the journal entry to record the issuance of the bonds on January 1, 2012.

B)

Give the journal entry necessary to recognize the interest expense for 2012 under the straight-line amortization method.

C)

Give the journal entry to record the repayment of the loan principal on December 31, 2021.

A)

January 1, 2012

Cash

8,500,000

Bonds Payable

10,000,000

Discount on Bonds Payable

150,000

Cash

500,000

Cash

10,000,000

Cash

100,000

Cash

1,000,000

75. On January 1, 2012, Lead Inc. issues $10,000,000, five-year, 9 percent bonds at 98. The discount at the time

of sales is $200,000. Interest is paid semiannually on June 30, and December 31.

Required:

A)

Provide the journal entry to record the issuance of the bonds on January 1, 2012.

B)

Provide the journal entry to recognize the interest expense on June 30 and December 31, 2012-2016 using straight-line amortization.

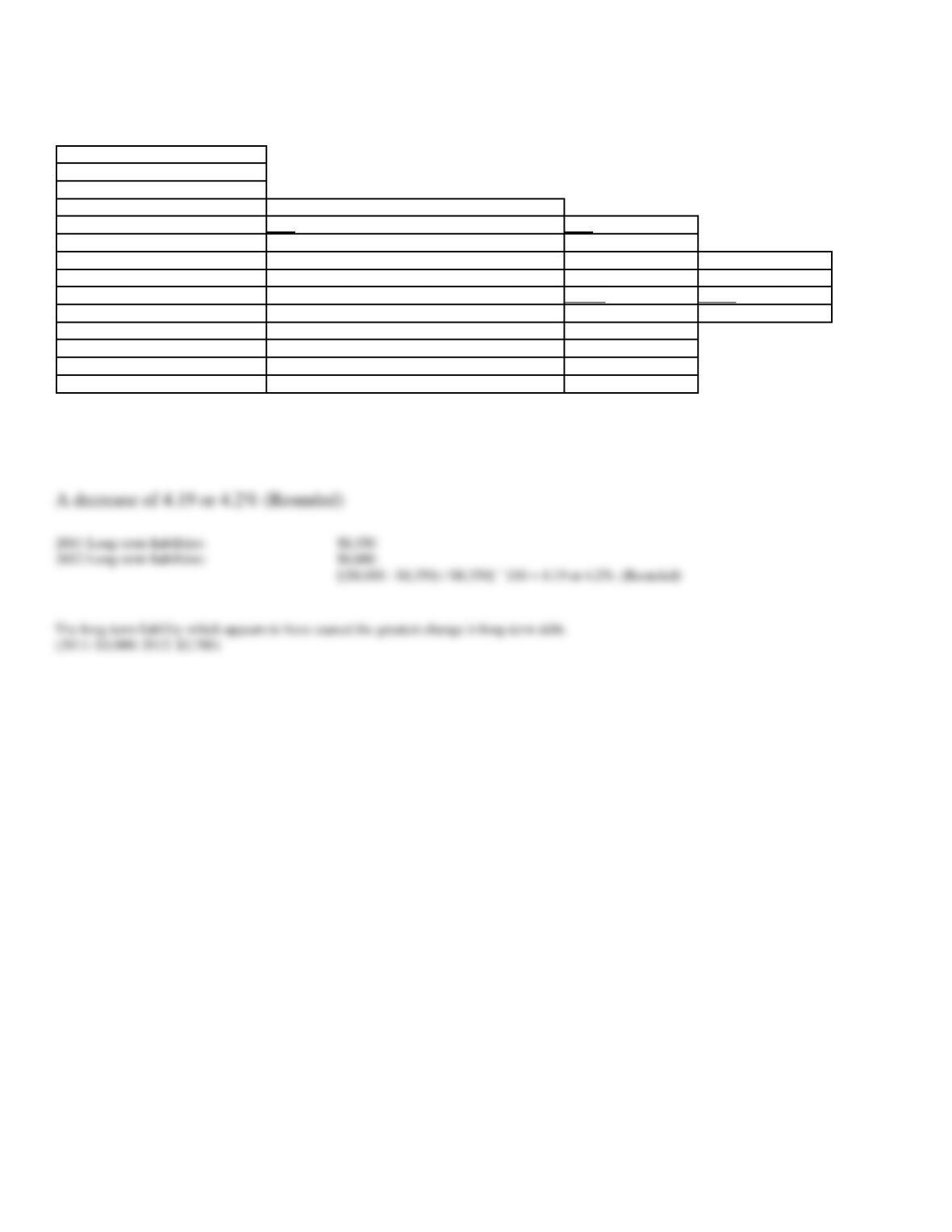

C)

Give the journal entry to record the repayment of the loan principal on December 31, 2016.

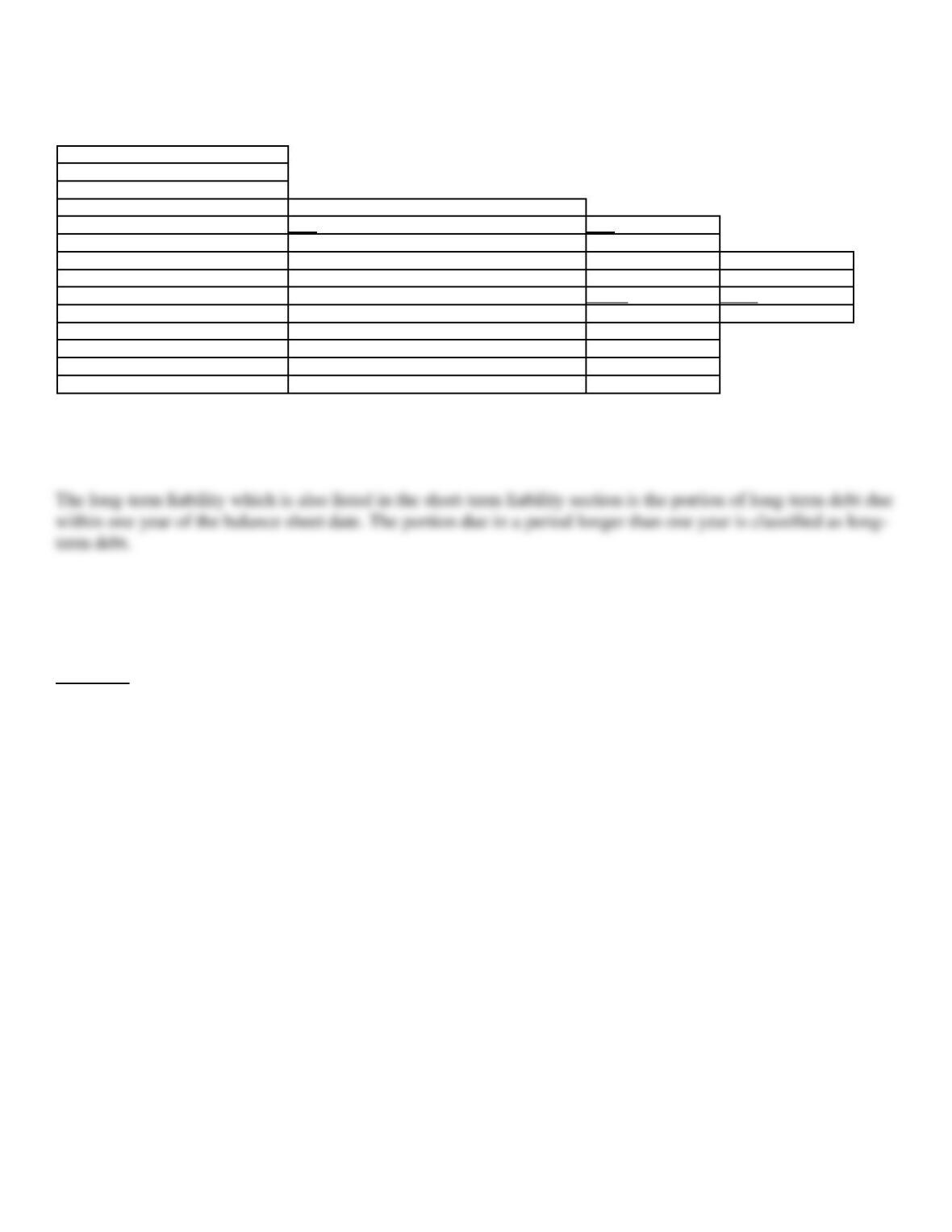

76. State Corporation

Below is a note on Disclosure of Leases for the State Corporation.

The State Corporation leases office, warehouse and showroom space, retail stores and office equipment under

operating leases, which expire no later than 2027. The Corporation normalizes fixed escalations in rental

expense under its operating leases. Minimum annual rentals under non-cancelable operating leases, excluding

operating cost escalations and contingent rental amounts based upon retail sales, are payable as follows:

Fiscal year ending March 31,

2013

$10,051,000

2014

11,121,000

2015

10,161,000

2016

9,063,000

2017

8,814,000

Thereafter

46,681,000

A)

January 1, 2012

Cash

9,800,000

Discount on Bonds Payable

200,000

Bonds Payable

10,000,000

B)

June 30/Dec. 31

Interest Expense

470,000

2012 – 2016

Cash

450,000

Discount on Bonds Payable

20,000

(Discount = $200,000 / 10 periods)

C)

December 31, 2016

Bonds Payable

10,000,000

Cash

10,000,000

Rent expense was $12,551,000; $8,911,000; and $5,768,000 for the years ended March 31, 2012, 2011, and 2010, respectively.

Refer to the information provided for State Corporation. What are the two types of leases that a company can have? Describe each briefly.

77. State Corporation

Below is a note on Disclosure of Leases for the State Corporation.

The State Corporation leases office, warehouse and showroom space, retail stores and office equipment under

operating leases, which expire no later than 2027. The Corporation normalizes fixed escalations in rental

expense under its operating leases. Minimum annual rentals under non-cancelable operating leases, excluding

operating cost escalations and contingent rental amounts based upon retail sales, are payable as follows:

Fiscal year ending March 31,

2013

$10,051,000

2014

11,121,000

2015

10,161,000

2016

9,063,000

2017

8,814,000

Thereafter

46,681,000

Rent expense was $12,551,000; $8,911,000; and $5,768,000 for the years ended March 31, 2012, 2011, and 2010, respectively.

Refer to the information provided for State Corporation. Does the note disclosure show evidence of the two types of leases?

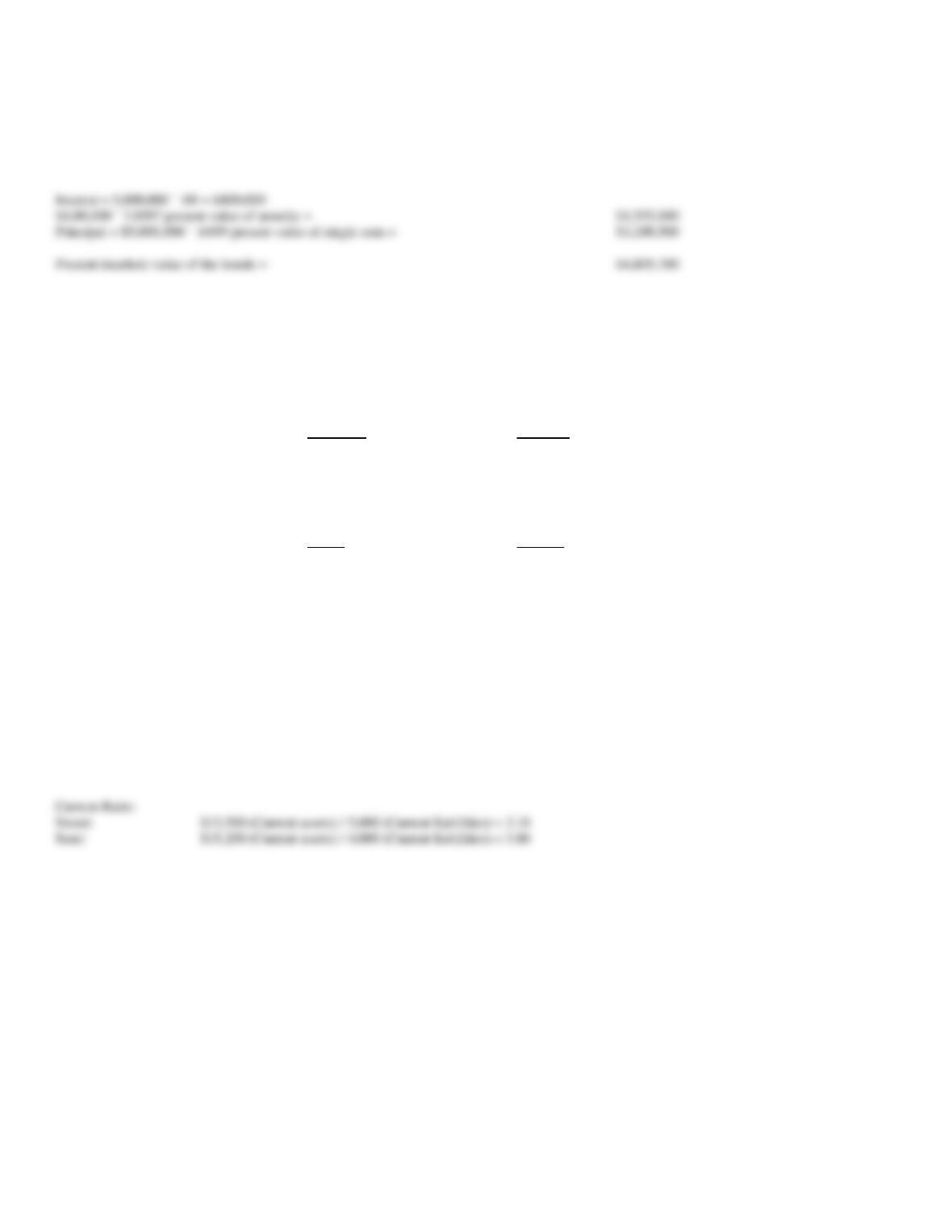

78. On January 1, 2012, Hawkeye Corporation issued $5,000,000 of 8% bonds, due in five years with interest

payable annually on December 31. The market rate is 9 percent. Calculate the present value (market value) of

the bonds.

79. Use the following selected financial information to compare these two companies at December 31, 2012,

and to answer the questions that follow.

Sweet Co.

Sour Co.

Cash

$ 1,100

$ 300

Short-term investments

100

900

Accounts and notes receivable

11,700

12,400

Inventories

1,200

1,000

Prepaid expenses

1,400

600

Total current assets

15,500

15,200

Total current liabilities

5,000

4,000

Long-term liabilities

12,300

12,000

Stockholders’ equity

5,300

7,300

Compute the current ratios for the two companies.

Current Ratio:

Sweet:

$15,500 (Current assets) / 5,000 (Current liabilities) = 3.10

Sour:

$15,200 (Current assets) / 4,000 (Current liabilities) = 3.80

Principal = $5,000,000 ´ .6499 present value of single sum =

$3,249,500

Present (market) value of the bonds =

$4,805,380

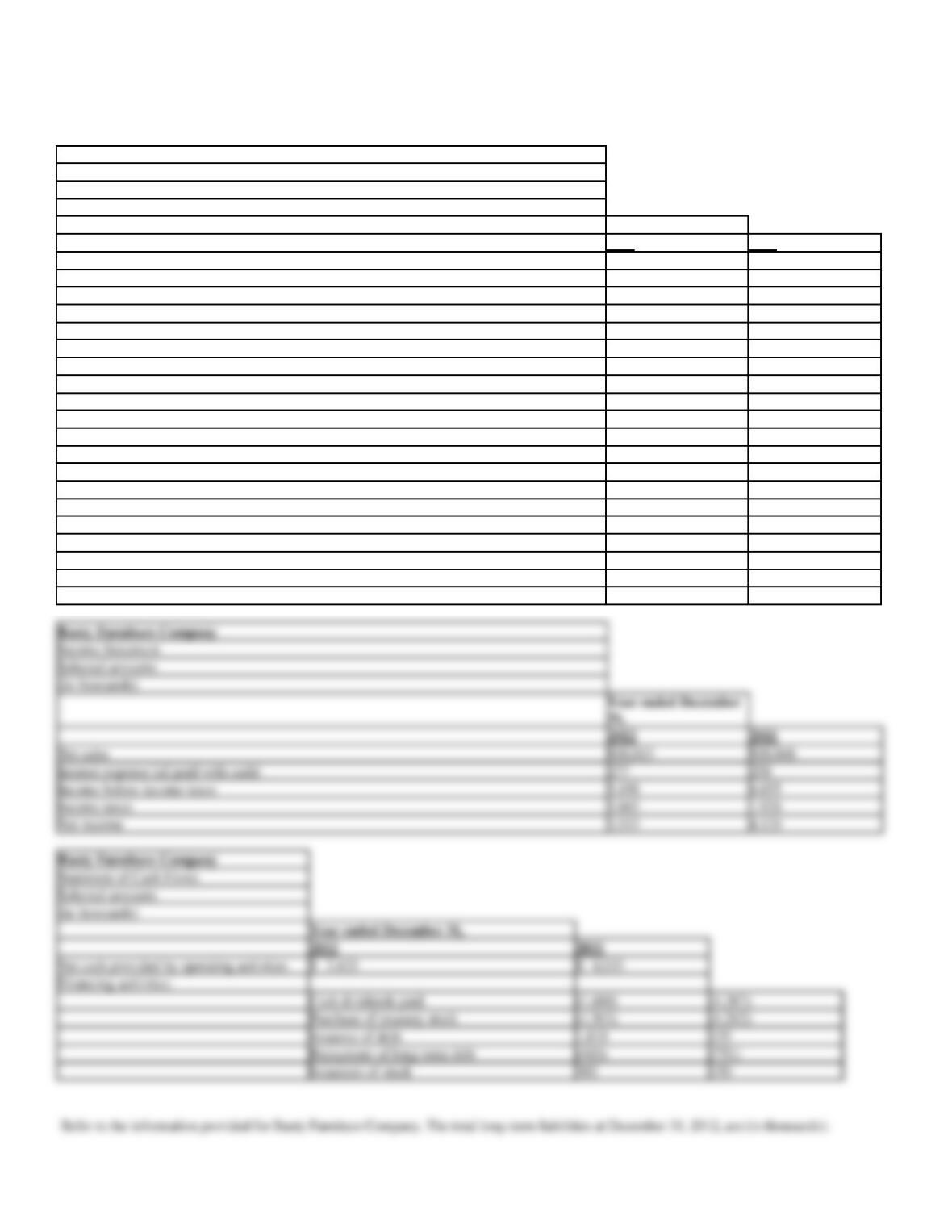

80. Rusty Furniture Company

Selected data from the comparative financial statements for Rusty Furniture Company are provided below.

Rusty Furniture Company

Balance Sheet Accounts

(all accounts have normal balances)

(in thousands)

December 31,

2012

2011

Accounts payable and accrued expenses

$ 3,141

$ 3,249

Accrued income taxes

1,037

1,056

Accumulated depreciation

2,016

2,028

Buildings

1,507

1,535

Cash and cash equivalents

1,648

1,737

Common stock

865

861

Containers

124

157

Current maturities of long-term debt

3

397

Deferred income taxes (long-term liability)

424

426

Goodwill and other intangible assets

547

668

Inventories

890

959

Land

19

183

Loans payable (short-term)

4,459

2,677

Long-term investments

8,549

6,501

Machinery & equipment

3,855

3,896

Marketable securities

159

106

Other long-term liabilities

991

1,001

Other fixed assets

1,580

1,087

Retained earnings

7,608

6,773

Trade accounts receivable

1,666

1,639

Rusty Furniture Company

Income Statement

Selected amounts

(in thousands)

2012

2011

Net sales

$18,813

$18,868

Interest expense (all paid with cash)

277

258

Income before income taxes

5,198

6,055

Income taxes

1,665

1,926

Net income

3,533

4,129

Rusty Furniture Company

Statement of Cash Flows

Selected amounts

(in thousands)

Year ended December 31,

2012

2011

Net cash provided by operating activities

$ 3,433

$ 4,033

Financing activities:

Cash dividends paid

(1,480)

(1,387)

Purchase of treasury stock

(1,563)

(1,262)

Issuance of debt

1,818

155

Repayment of long-term debt

(410)

(751)

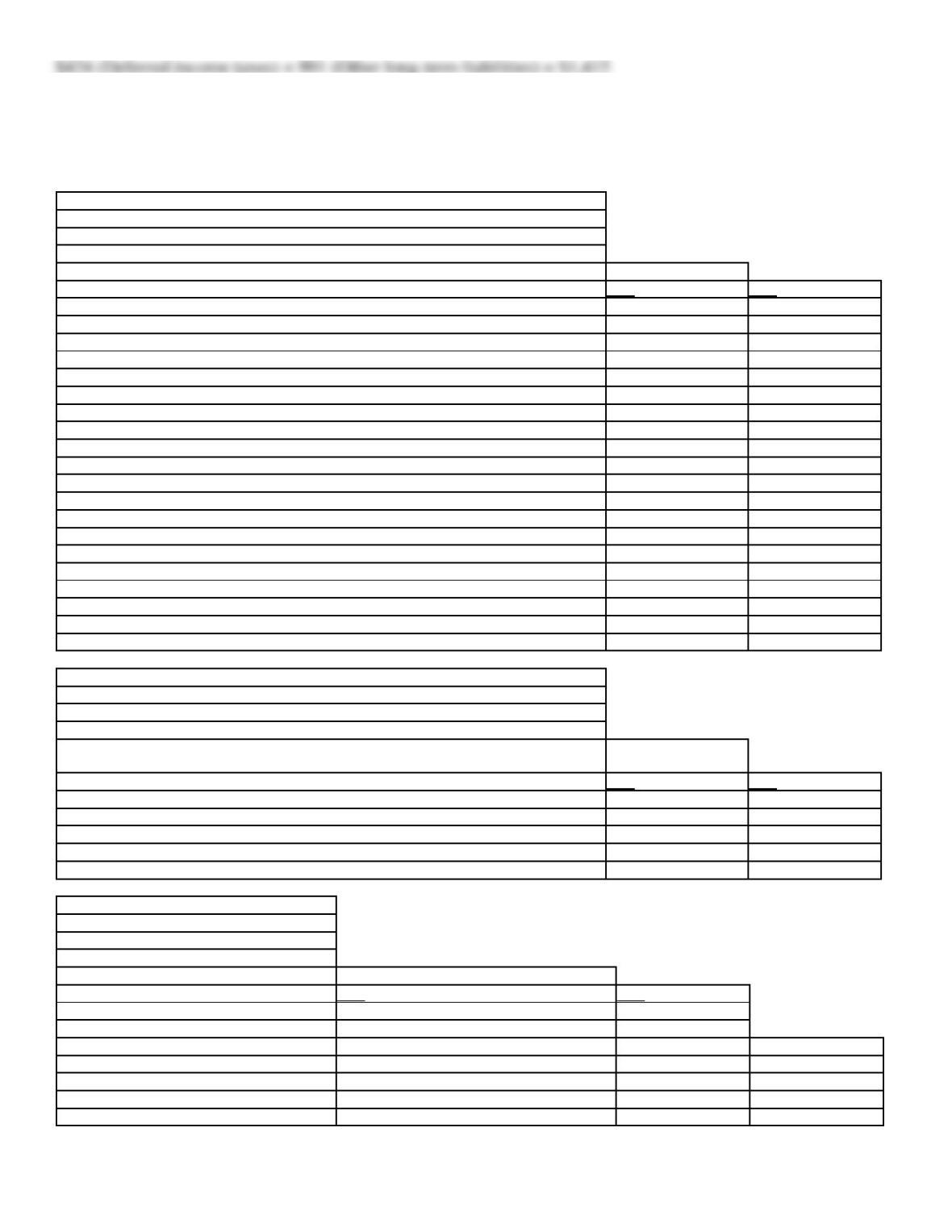

81. Rusty Furniture Company

Selected data from the comparative financial statements for Rusty Furniture Company are provided below.

Rusty Furniture Company

Balance Sheet Accounts

(all accounts have normal balances)

(in thousands)

December 31,

2012

2011

Accounts payable and accrued expenses

$ 3,141

$ 3,249

Accrued income taxes

1,037

1,056

Accumulated depreciation

2,016

2,028

Buildings

1,507

1,535

Cash and cash equivalents

1,648

1,737

Common stock

865

861

Containers

124

157

Current maturities of long-term debt

3

397

Deferred income taxes (long-term liability)

424

426

Goodwill and other intangible assets

547

668

Inventories

890

959

Land

19

183

Loans payable (short-term)

4,459

2,677

Long-term investments

8,549

6,501

Machinery & equipment

3,855

3,896

Marketable securities

159

106

Other long-term liabilities

991

1,001

Other fixed assets

1,580

1,087

Retained earnings

7,608

6,773

Trade accounts receivable

1,666

1,639

Rusty Furniture Company

Income Statement

Selected amounts

(in thousands)

Year ended December

31,

2012

2011

Net sales

$18,813

$18,868

Interest expense (all paid with cash)

277

258

Income before income taxes

5,198

6,055

Income taxes

1,665

1,926

Net income

3,533

4,129

Rusty Furniture Company

Statement of Cash Flows

Selected amounts

(in thousands)

Year ended December 31,

2012

2011

Net cash provided by operating activities

$ 3,433

$ 4,033

Financing activities:

Cash dividends paid

(1,480)

(1,387)

Purchase of treasury stock

(1,563)

(1,262)

Issuance of debt

1,818

155

Repayment of long-term debt

(410)

(751)

Issuances of stock

302

150

Refer to the information provided for Rusty Furniture Company.

A)

The total liabilities at December 31, 2012, are (in thousands):

B)

The debt to assets ratio at December 31, 2012, is:

82. South Shore Company

The liabilities section of South Shore’s consolidated balance sheets is provided below.

South Shore Company

Consolidated Balance Sheets

(in millions)

December 31,

2012

2011

Current liabilities

Short-term borrowings

$ 250

$ 200

Accounts payable and other current liabilities

4,500

4,450

Income taxes payable

200

50

Total current liabilities

$4,950

$4,700

Long-term debt

$2,700

$3,000

Other long-term liabilities

3,800

3,950

Deferred income taxes

1,500

1,400

Refer to the information provided for South Shore Company. What are the total long-term liabilities for each of the two years presented?

2012:

$8,000 (in millions)

$2,700 (Long-term debt) + 3,800 (Other long-term debt) + 1,500 (Deferred income taxes) = $8,000

$3,000 (Long-term debt) + 3,950 (Other long-term debt) + 1,400 (Deferred income taxes) = $8,350

B)

Total liabilities = $10,055 (from Part A)

Total assets = $18,528

$10,055 (Total liabilities) / $18,528 (Total assets) = .5427

83. South Shore Company

The liabilities section of South Shore’s consolidated balance sheets is provided below.

South Shore Company

Consolidated Balance Sheets

(in millions)

December 31,

2012

2011

Current liabilities

Short-term borrowings

$ 250

$ 200

Accounts payable and other current liabilities

4,500

4,450

Income taxes payable

200

50

Total current liabilities

$4,950

$4,700

Long-term debt

$2,700

$3,000

Other long-term liabilities

3,800

3,950

Deferred income taxes

1,500

1,400

Refer to the information provided for South Shore Company. What would the horizontal analysis of long-term liabilities for 2012 show? Which

liability appears to have caused the greatest change?

2011 Long-term liabilities:

$8,350

2012 Long-term liabilities:

$8,000

[($8,000 – $8,350) / $8,350] ´ 100 = 4.19 or 4.2%. (Rounded)

84. South Shore Company

The liabilities section of South Shore’s consolidated balance sheets is provided below.

South Shore Company

Consolidated Balance Sheets

(in millions)

December 31,

2012

2011

Current liabilities

Short-term borrowings

$ 250

$ 200

Accounts payable and other current liabilities

4,500

4,450

Income taxes payable

200

50

Total current liabilities

$4,950

$4,700

Long-term debt

$2,700

$3,000

Other long-term liabilities

3,800

3,950

Deferred income taxes

1,500

1,400

Refer to the information provided for South Shore Company. Which long-term liability would also be listed in the short-term liability section?

Why?

85. A company issued 5-year bonds with a face value of $35,000,000 and a 7% annual stated rate of interest on

January 2, 2012. The issue price of the bond issue was $36,474,327 which reflected a 6% effective interest rate.

Interest payments are made annually.

Required:

A)

Give the journal entry to record the issuance of the bonds.

B)

Give the journal entry to record the recognition of interest expense at December 31, 2012. Any premium or discount should be

amortized using the effective interest rate method.

C)

Give the journal entry to record the interest paid to the bondholders on January 2, 2012.

D)

Give the journal entry to record the recognition of interest expense at December 31, 2013. Any premium or discount should be

amortized using the effective interest rate method.

86. Obligations that extend beyond one year are referred to as ____________________.

87. The amount of money the borrower agrees to repay at maturity of a bond is usually referred to as the

____________________.

88. If the market rate of interest is greater than the stated rate, then the bonds are issued at a(n)

____________________.

89. The ____________________ is the rate of return that investors in the bond markets demand for bonds of

similar risk.

Cash

36,474,327

Bonds Payable

35,000,000

Interest Expense

2,188,460

Premium on Bonds Payable

216,540

Interest Payable

2,450,000

Interest Expense

2,172,767

Premium on Bonds Payable

277,233

90. Discount on Bonds Payable is shown on the balance sheet as a(n) ____________________.

91. Under the ____________________ method of amortization, an equal amount of discount or premium is

amortized each time interest is paid.

92. ____________________ bonds may be retired by the issuing company before their specified due date.

93. A(n) ____________________ lease is recorded on the lessee’s balance sheet as an asset and related

liability.

94. Although operating leases are not recorded on the balance sheet by the lessee, they are disclosed in the

____________________.

95. An obligation that arises from an existing condition whose outcome is uncertain and whose resolution

depends on a future event is called a ____________________.

96. The current ratio is computed by dividing current assets by ____________________.