Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

7. Under U.S. GAAP, application of the LIFO and FIFO inventory methods result in differences in the

balance sheet, income statement and cash flow statement. Compare and contrast the effect of the two

methods on each financial statement and determine the advantages and disadvantages of each method.

9-20

8. Many firms use derivative instruments to hedge exposure to changes in the fair value an asset or

liability or to hedge exposure to variability in expected future cash flows. As an analyst examining the

financial reports of a company that uses derivative instruments to hedge, what questions should be

asked when thinking about derivatives and accounting quality?

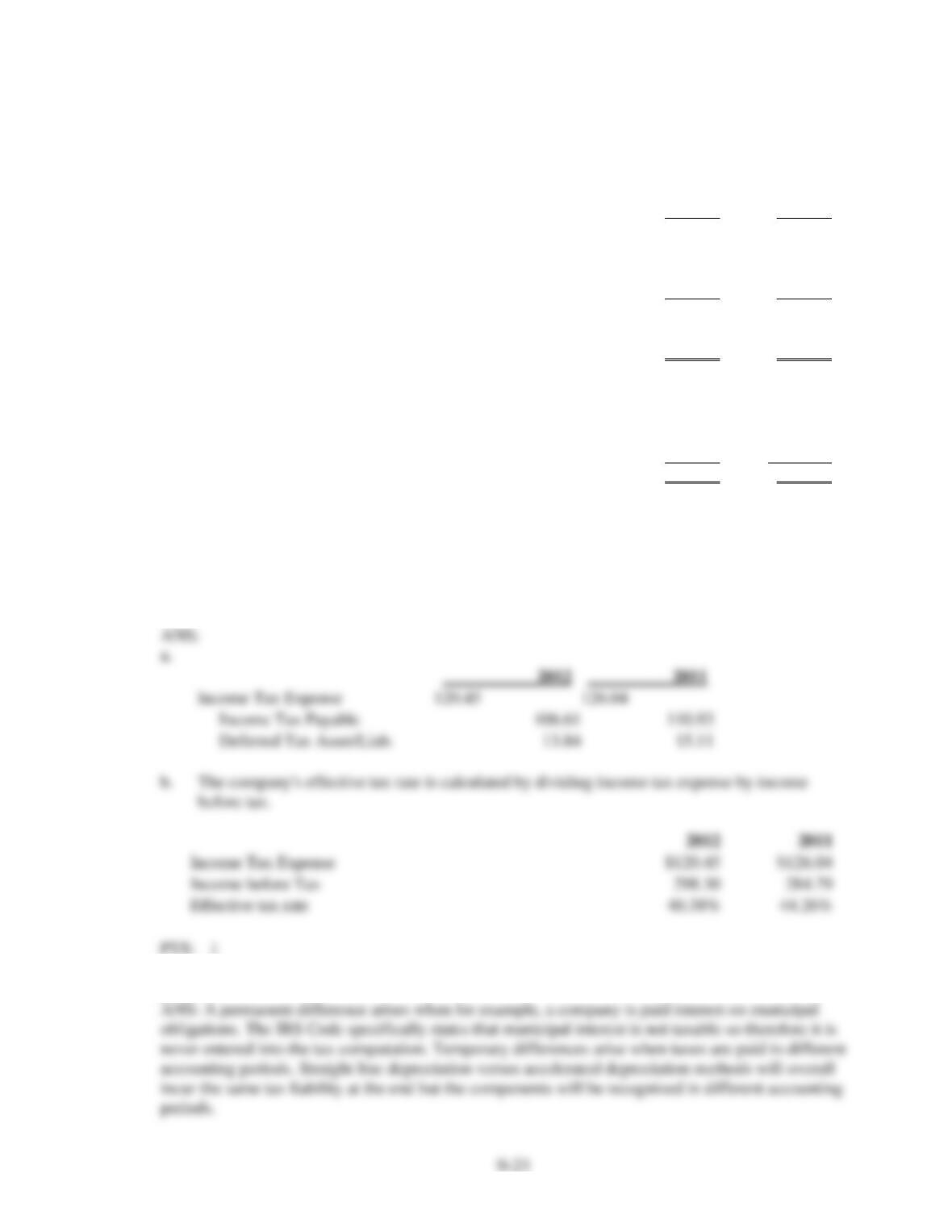

9. Global, Inc. provides consulting services throughout the world. The company pays taxes to the nation

where revenues are earned. Information about the company's taxes are presented below:

Global, Inc.

Components of Income Tax Expense

(in millions)

2012

2011

Current - Federal

$ 35.60

$ 29.80

- Foreign

53.86

65.85

- State and Local

17.15

15.28

Total Current

$106.61

$110.93

Deferred - Federal

$ 10.56

$ 8.54

- Foreign

3.28

6.57

Total Deferred

$ 13.84

$ 15.11

Total Income Tax Expense

$120.45

$126.04

Components of Income before Taxes

2012

2011

United States

$155.45

$150.29

Foreign

142.85

134.50

Total

$298.30

$284.79

Required:

a.

Using the information provided for Global, prepare the company's journal entry to record

income taxes for 2012 and 2011.

b.

Using the information provided for Global, determine the company's effective tax rate for

2012 and 2011.

10. Explain the difference between a temporary and a permanent timing difference for income tax

purposes”

9-22

11. What are the foiur disclosures required by US. GAAP relating to income taxes?

PROBLEM

1. The following information is related to the defined benefit pension plan of Xavier Company for 2012:

Service cost

$60,000

Contributions to pension plan

142,400

Benefits paid to retirees

150,000

Plan assets (fair value), January 1

740,000

Plan assets (fair value), December 31

850,000

Unamortized Prior Service Cost, January 1

160,000

Unamortized Prior Service Cost, December 31

110,000

Actual return on plan assets

150,000

PBO, January 1

900,000

PBO, December 31

960,000

ABO, December 31

890,000

Discount rate

10%

Long-term expected return on plan assets

9%

Required:

1.

Using the above information calculate pension expense for 2012?

2.

Will it be necessary for the company to report a minimum pension liability at Dec. 31,

2012? If so what is the amount.

2.

At Dec. 31, 2012, the company’s ABO exceeds its plan assets by $40,000, given that

the company does not have prepaid or accrued pension cost than its minimum pension

liability will also be $40,000.

2. Given the following information, compute December 31, 2012 projected benefit obligation (PBO) and

fair market value (FMV) of plan assets for Eagan Company.

Prior service cost granted in a 2012 plan amendment

$115,000

Interest on PBO

73,000

Actual return on plan assets

101,000

Service cost

84,000

Contribution sent to plan trustee

62,000

Benefit payments to retirees

24,000

Liability loss (gain)

(37,000)

FMV of plan assets, January 1, 2012

735,000

PBO, January 1, 2012

814,000

What amount of asset or liability will be reported on the balance sheet at December 31, 2012?

3. A large manufacturer recently changed its cost-flow assumption method for inventories at the

beginning of 2012. The manufacturer has been in operation for almost 40 years, and for the last

decade, it has reported moderate growth in revenues. The firm changed from the LIFO method to the

FIFO method and reported the following information:

December 31: (amounts in millions)

2011

2012

Inventories at FIFO cost

$ 388.1

$ 419.7

Excess of FIFO cost over LIFO cost

(229.0)

(210.4)

Cost of goods sold (FIFO)

$2,050.8

Cost of goods sold (LIFO)

$2,417.1

Calculate the inventory turnover ratio for 2012 using the LIFO and FIFO cost-flow assumption

methods. Explain why the costs assigned to inventory under LIFO at the end of 2011 and 2012 are so

much less than they are under FIFO.

4. Firm A places its order for the equipment on June 30, Year 1. It simultaneously signs a forward

foreign exchange contract for 20,000 GBP. The forward rate on June 30, Year 1, for settlement on

June 30, Year 2, is $1.64 per GBP. Firm A designates the forward foreign exchange contract as a fair

value hedge of the firm commitment.

Required

a. U.S. GAAP and IFRS do not require Firm A to record the purchase commitment or the

forward foreign exchange contract on the balance sheet as a liability and an asset on

June 30, Year 1. What is the logic for this accounting?

b. On December 31, Year 1, the forward foreign exchange rate for settlement on June

30, Year 2, is $1.73 per GBP. Using the financial statement effects template, show the

financial statement effects of recording the change in the value of the purchase commitment

and the change in the value of the forward contract for Year 1. Assume an 8 percent per year interest

rate for discounting cash flows to their present values on December 31, Year 1.

c. Show the financial statement effects on June 30, Year 2, of recording the change in the present value

of the purchase commitment and the forward foreign exchange contract for the passage of time.

d. On June 30, Year 2, the spot foreign exchange rate is $1.75 per GBP. Show the financial

statement effects of recording the change in the value of the purchase commitment and the change in

the value of the forward contract due to changes in the exchange rate during the first six months of

Year 2.

e. Show the financial statement effects of the June 30, Year 2, purchase of 20,000 GBP with U.S.

dollars and acquisition of the equipment.

f. Show the financial statement effects on June 30, Year 2, to settle the forward foreign

exchange contract.

g. How would the effects in Parts b–f differ if Firm A had chosen to designate the forward

foreign exchange contract as a cash flow hedge instead of a fair value hedge?

h. Suggest a scenario that would justify Firm A treating the forward foreign exchange contract as a fair

value hedge and a scenario that would justify the firm treating the

contract as a cash flow hedge.

5. Firm D holds 20,000 gallons of chemicals in inventory on October 31, Year 1, that cost $225

per gallon. Firm D contemplates selling the chemicals on March 31, Year 2, when it completes

the processing. Uncertainty about the selling price of the chemical on March 31, Year 2, leads

Firm D to acquire a forward contract on the chemical. The forward contract does not require an initial

investment of funds. Firm D designates the forward commodity contract as a cash flow hedge of an

anticipated transaction. The forward price on October 31, Year 1, for delivery on March 31, Year 2, is

$320 per gallon.

Required

a. Using the financial statement effects template, show the financial statement effects,

if any, that Firm D would have on October 31, Year 1, when it acquires the forward

commodity price contract.

b. On December 31, Year 1, the end of the accounting period for Firm D, the forward

price of the chemical for March 31, Year 2, delivery is $310 per gallon. Show the financial

statement effects of recording the change in the value of the forward commodity

price contract. Ignore the discounting of cash flows in this part and in the remainder

of the problem.

c. Show the financial statement effects of the December 31, Year 1, decline in value of

the chemical inventory.

d. On March 31, Year 2, the price of the chemical declines to $270 per gallon. Show the

financial statement effects of revaluing the forward contract.

e. Show the financial statement effects on March 31, Year 2, to reflect the decline in

value of the inventory.

f. Show the financial statement effects on March 31, Year 2, to settle the forward contract.

g. Assume that Firm D sells the chemical on March 31, Year 2, for $270 a gallon. Show

the financial statement effects of recording the sale and recognizing the cost of

goods sold.

9-29

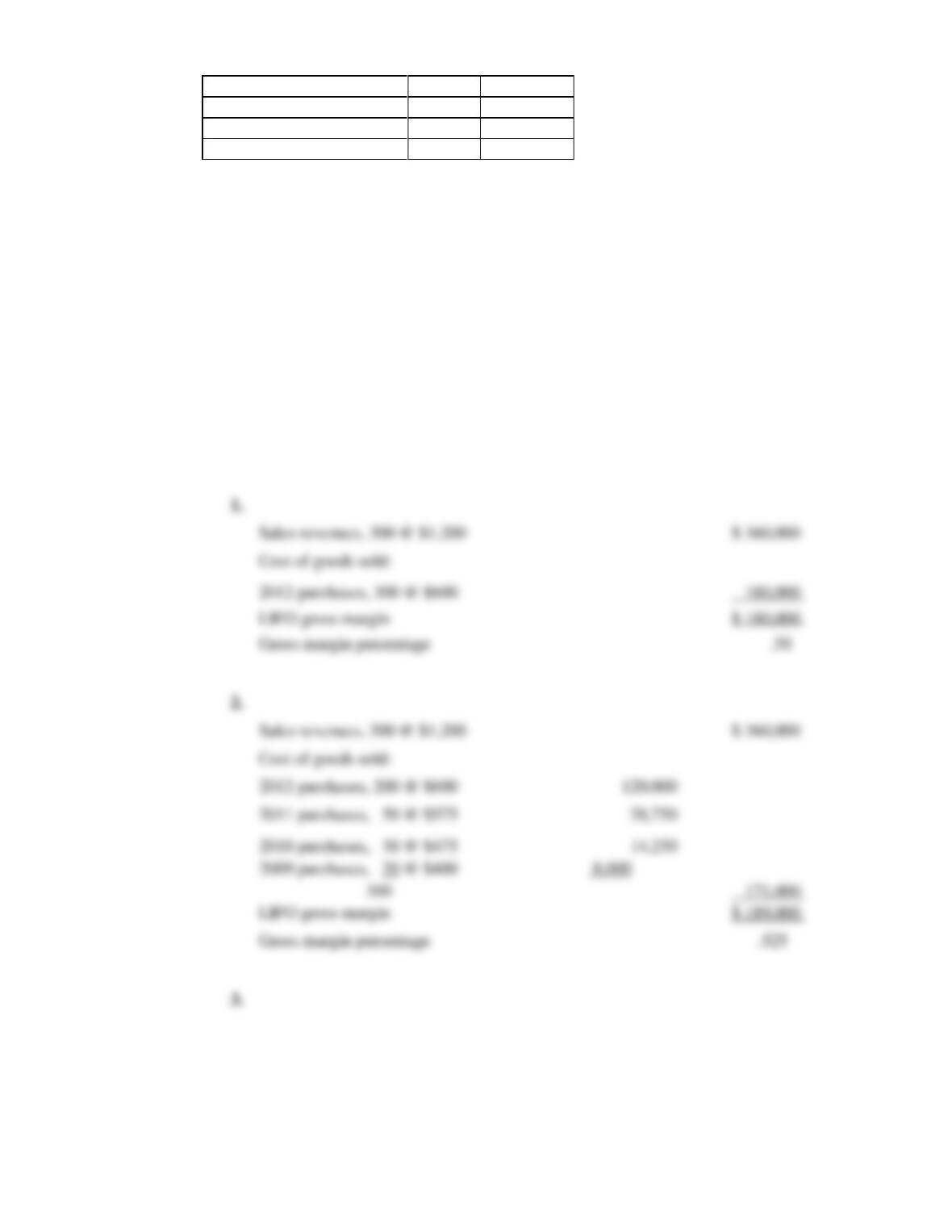

6. Cooke Industries imports and sells quality merchandise. The company had the following layers in its

LIFO inventory at January 1, 2012, at which time the replacement cost of the inventory was $600 per

unit.

9-30

Year LIFO Layer Added

Units

Unit Cost

2009

40

$400

2010

30

$475

2011

50

$575

The replacement cost of the merchandise remained constant throughout 2012. Cooke sold 300 units

during 2012. The company established the selling price of each unit by doubling its replacement cost

at the time of sale.

Required:

1. Determine the gross margin and the gross margin percentage for 2012 assuming that Cooke

purchased 310 units during the year.

2. Determine the gross margin and the gross margin percentage for 2012 assuming that Cooke

purchased 200 units during the year.

3. Explain why the assumed number of units purchased makes a difference in your answers.

ANS:

9-31

7. Magnum Construction contracted to construct a factory building for $545,000. The company started

during 2012 and was completed in 2013. Information relating to the contract is as follows:

2012

2013

Costs incurred during the year

$310,000

$170,000

Estimated additional cost to complete

165,000

--

Billings during the year

280,000

285,000

Cash collections during the year

260,000

305,000

Required:

Record the preceding transactions in Magnum’s books under completed-contract and the percentage of

completion methods. Determine amounts that will be reported on the balance sheet at the end of 2012.

9-32

9-33

8. The following information is taken from Satin financial statements (amounts in thousands):

12/31/2010

12/31/2009

Inventory at LIFO

$219,686

$241,154

Cost of goods sold

754,661

675,138

Stockholders’ Equity

242,503

242,712

Net Income

31,185

64,150

Tax rate

37%

37%

Inventory Footnote: If the first-in, first-out method of accounting for inventory had been used,

inventory would have been approximately $26.9 million and $25.1 million higher than reported at

12/31/2010 and 12/31/2009, respectively.

9-34

Required:

a.

Calculate what inventory would have been at 12/31/2010 and 12/31/2009 had the FIFO

inventory method been used.

b.

What would net income for the year ended 12/31/2010, have been if the FIFO inventory

method been used?

c.

Calculate what stockholders' equity would have been at 12/31/2010 and 12/31/2009 had

the FIFO inventory method been used.

9. Bower Construction Comp. has consistently used the percentage-of-completion method for

recognizing revenue on its long-term contracts. During 2010 Bower entered into a fixed-price contract

to construct an office building for $8,000,000. Information relating to the contract is as follows:

2010

2011

2012

Percent Complete

25%

70%

100%

Estimated Total Cost at Completion

$5,600,000

$6,400,000

$6,500,000

Gross Profit Recognized to date

600,000

1,120,000

?

Required (Show Calculations):

1.

Compute contract costs incurred during 2010, 2011 and 2012.

2.

Determine how much gross profit Bower should recognize in 2012.

3.

Under what conditions would it not be reasonable for a company to use the percentage of

completion method of recognizing revenue on long-term contracts?

4.

If Bower had used the completed contract method of accounting for this long-term contract

how much gross profit would it have earned in 2010, 2011 and 2012?

10. The following information is available from Sheldon Corp.:

Information from the Balance Sheet:

2012

2011

Depreciable Assets

$2,458,600

$1,985,400

Accumulated Depreciation

(1,350,700)

(1,046,000)

Depreciable Assets (Net)

$1,107,900

$939,400

From the Income Statement

2012

Depreciation Expense

$384,500

Use the information above to calculate the following:

a. Average age of the depreciable assets

b. Average remaining useful life of the depreciable assets