9-1: Job Order Sheet

The Talbott Company has received an order (#324) for 100 widgets. On January 20 the

shop supervisor requisitioned 100 units of part 503 at a cost of $5 per unit and 500 units part 456

at a cost of $3 per unit to begin work on the 100 widgets. On the same day 20 hours of direct labor

at $20 per hour are used to work on the widgets. On January 21, 200 units of part 543 at $6 per

unit are requisitioned and 10 hours of direct labor at $15 per hour are performed on the 100 units

of widgets to complete the job. Overhead is allocated to the job based on $5 per direct labor hour.

Required:

Make a job order cost sheet for the 100 widgets.

9-1: Solution to Job Order Sheet (15 minutes)

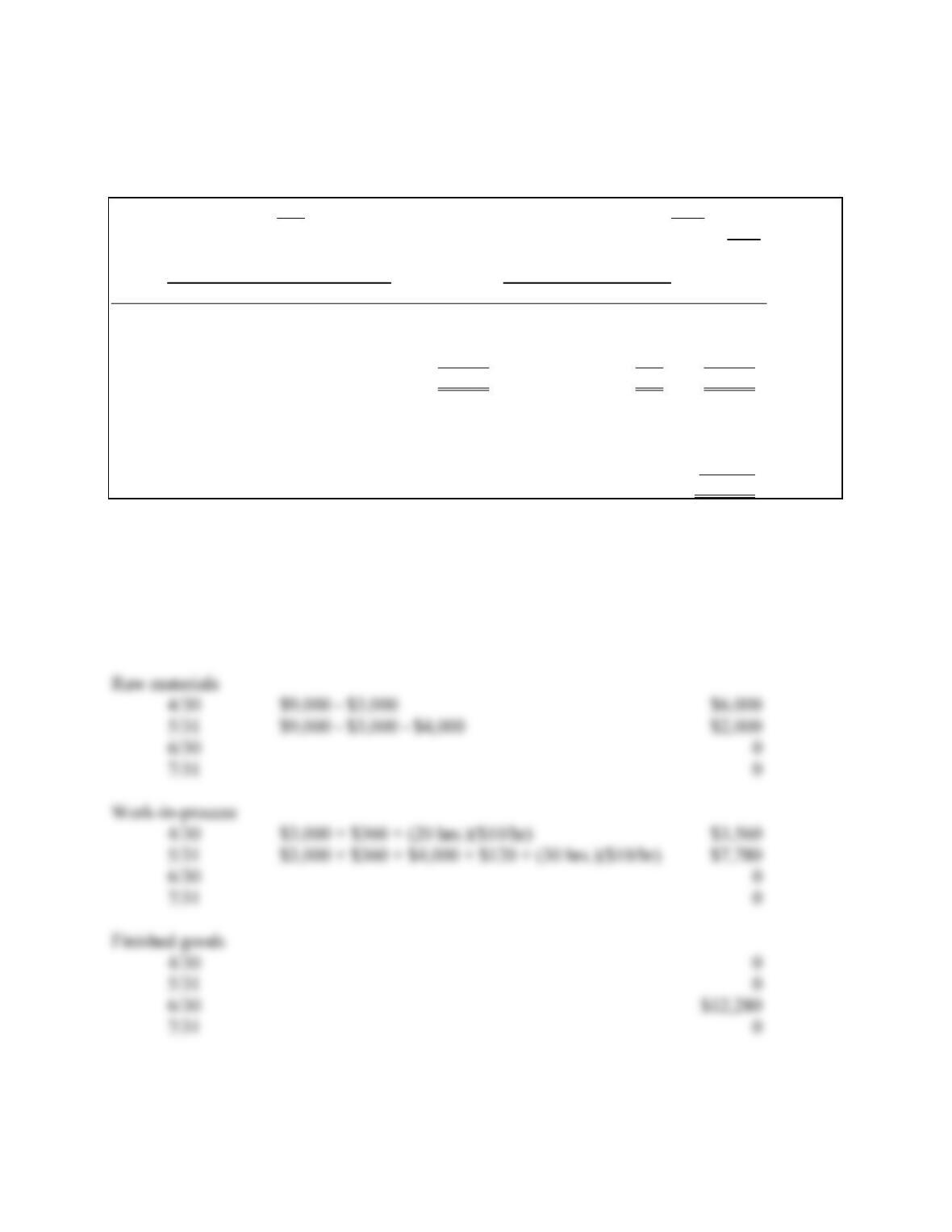

9-2: Job Cost Flows

The job cost sheet for 1,000 units of toy trucks is:

Job Number 555 Date Started 4/13

Date Completed 6/18

Raw Materials Direct Labor

Date Type Cost Qty. Amount Cost Hours Amount

4/13 565 $ 3 1,000 $3,000 $18 20 $ 360

5/24 889 1 4,000 4,000 12 10 120

6/18 248 2 1,000 2,000 15 100 1,500

$9,000 130 $1,980

Total direct materials $9,000

Total direct labor 1,980

Overhead (130 direct labor hours @ $10/hour) 1,300

Total Job Cost $12,280

All of the materials for the job were purchased on 4/10. The batch of 1,000 toy trucks is

sold on 7/10.

What are the costs of this job order in the raw materials account, the work–in-process

account, the finished goods account, and the cost of goods account on 4/30, 5/31, 6/30 and 7/31?

9-2: Solution to Job Cost Flows (15 minutes)

9-3: Over/Underabsorbed Overhead

The Alphonse Company allocates fixed overhead costs by machine hours and variable

overhead costs by direct labor hours. At the beginning of the year the company expects fixed

overhead costs to be $600,000 and variable costs to be $800,000. The expected machine hours are

6,000 and the expected direct labor hours are 80,000. The actual fixed overhead costs are $700,000

and the actual variable overhead costs are $750,000. The actual machine hours during the year are

5,500 and the actual direct labor hours are 90,000.

Required:

a. How much overhead is allocated?

b. What is the over/underabsorbed overhead?

9-3: Solution to Over/Underabsorbed Overhead (10 minutes)

9-4: Prorating Over/Underabsorbed Overhead

A computer manufacturer has the following account balances at the end of the year.

Work-in-process $ 100,000

Finished goods 800,000

Cost of goods sold 2,000,000

Total $2,900,000

These accounts contain $500,000 of allocated overhead. Actual overhead, however, is $600,000.

What are the account balances after prorating the underabsorbed overhead?

9-4: Solution to Prorating Over/Underabsorbed Overhead (10 minutes)

9-5: Incentives and Depreciation Methods

What conditions are likely to exist when operating managers are compensated based on

accounting earnings and accelerated depreciation methods are used to compute overhead charges

to operating departments?

9-5: Solution to Incentives and Depreciation Methods (10 minutes)

9-6: Plantwide vs. Department Overhead Rates

Rose Bach has recently been hired as controller of Empco Inc., a sheet-metal manufacturer.

Empco has been in the sheet-metal business for many years and is currently investigating ways to

modernize its manufacturing process. At the first staff meeting Bach attended, Bob Kelley, chief

engineer, presented a proposal for automating the drilling department. Kelley recommended that

Empco purchase two robots that could replace the eight direct labor workers in the department.

The cost savings outlined in Kelley’s proposal include two elements. First, direct labor cost in the

drilling department is eliminated. Second, manufacturing overhead cost in the department is

reduced to zero because Empco charges manufacturing overhead on the basis of direct labor dollars

using a plantwide rate.

The president of Empco felt that Kelley’s explanation of the cost savings made no sense.

Bach agreed and explained that as firms become more automated, they should rethink their

manufacturing overhead systems. The president asked Bach to look into the matter and prepare a

report for the next staff meeting.

To refresh her knowledge, Bach reviewed articles on manufacturing overhead allocation

for an automated factory and discussed the matter with some of her peers. She also gathered the

historical data presented below on the manufacturing overhead rates experienced by Empco over

the years. Bach also wanted to have some departmental data to present at the meeting. Using

Empco’s accounting records, she was able to estimate the annual averages presented below for

each manufacturing department in the 1990s.

Historical Data

Date

Average Annual

Direct Labor

Cost

Average Annual

Manufacturing

Overhead Cost

Average

Manufacturing

Overhead

Application

Rate

1950s

$1,000,000

$1,000,000

100%

1960s

1,200,000

3,000,000

250

1970s

2,000,000

7,000,000

350

1980s

3,000,000

12,000,000

400

1990s

4,000,000

20,000,000

500

Annual Averages

Cutting

Department

Grinding

Department

Drilling

Department

Direct labor

$ 2,000,000

$1,750,000

$ 250,000

Manufacturing overhead

11,000,000

7,000,000

2,000,000

Required:

a. Disregarding the proposed use of robots in the drilling department, describe the

shortcomings of Empco’s current system for applying overhead.

b. Do you agree with Bob Kelley’s statement that the manufacturing overhead cost in the

drilling department will be reduced to zero if the automation proposal is implemented?

Explain.

c. Recommend ways to improve Empco’s method for applying overhead by describing how

it should revise its overhead accounting system:

(i) in the cutting and grinding departments.

(ii) to accommodate the automation of the drilling department.

Source: CMA adapted.

9-6: Solution to Plantwide vs. Department Overhead Rates (CMA adapted) (20 minutes)

9-7: Absorption Costing in a Bank

First Eastern Bank is a large, multibranch bank offering a wide variety of commercial and

retail banking services. Eastern uses an absorption costing system to monitor the costs of various

services and provide information for a variety of decisions.

One set of services is a retail loan operation providing residential mortgages, car loans, and

student college loans. All loan applications are filed by the applicant at a branch bank, where the

branch manager fills out the loan application. From there, the loan application is sent to the loan

processing department, where the applicant’s credit history is checked and a recommendation is

made regarding loan approval based on the applicant’s credit history and current financial situation.

This recommendation is forwarded to the loan committee of senior lending officers, who review

the file and make a final decision.

Thus, there are three stages to making a loan: application in a branch, the loan processing

department, and the loan committee. Mr. and Mrs. Jones visit the West Street branch and file an

application for a residential mortgage. The Jones’s loan application is processed through the three

stages.

• West Street Branch Bank. The branch manager spends one hour taking the application.

The branch manager spends 1,000 hours per year of her total time taking loan applications

and the remainder of her time providing other direct services to customers. Total overhead

in the West Street Branch is budgeted to be $259,000, excluding the manager’s salary, and

is allocated to direct customer services using the branch manager’s time spent providing

direct customer services. The branch manager’s annual salary is $42,600.

• Processing department. The processing department budgets its total overhead for the year

to be $800,000, which is allocated to loans processed using direct labor hours. Budgeted

direct labor hours for the year are 40,000 hours. Direct labor hours in the processing

department cost $18 per hour. The Jones’s loan requires five direct labor hours in the loan

processing department.

• Loan committee. Ten senior bank executives are on the loan committee. The loan

committee meets 52 times per year, every Wednesday, all day, to approve all loans. The

average salary and benefits of each member of the loan committee are $104,000. The loan

committee spends 15 minutes reviewing the Jones’s loan application before approving it.

For costing purposes, all employees are assumed to work eight-hour days, five days per

week, 52 weeks per year.

Required:

Calculate the total cost of taking the application, processing, and approving the Joneses’

mortgage.

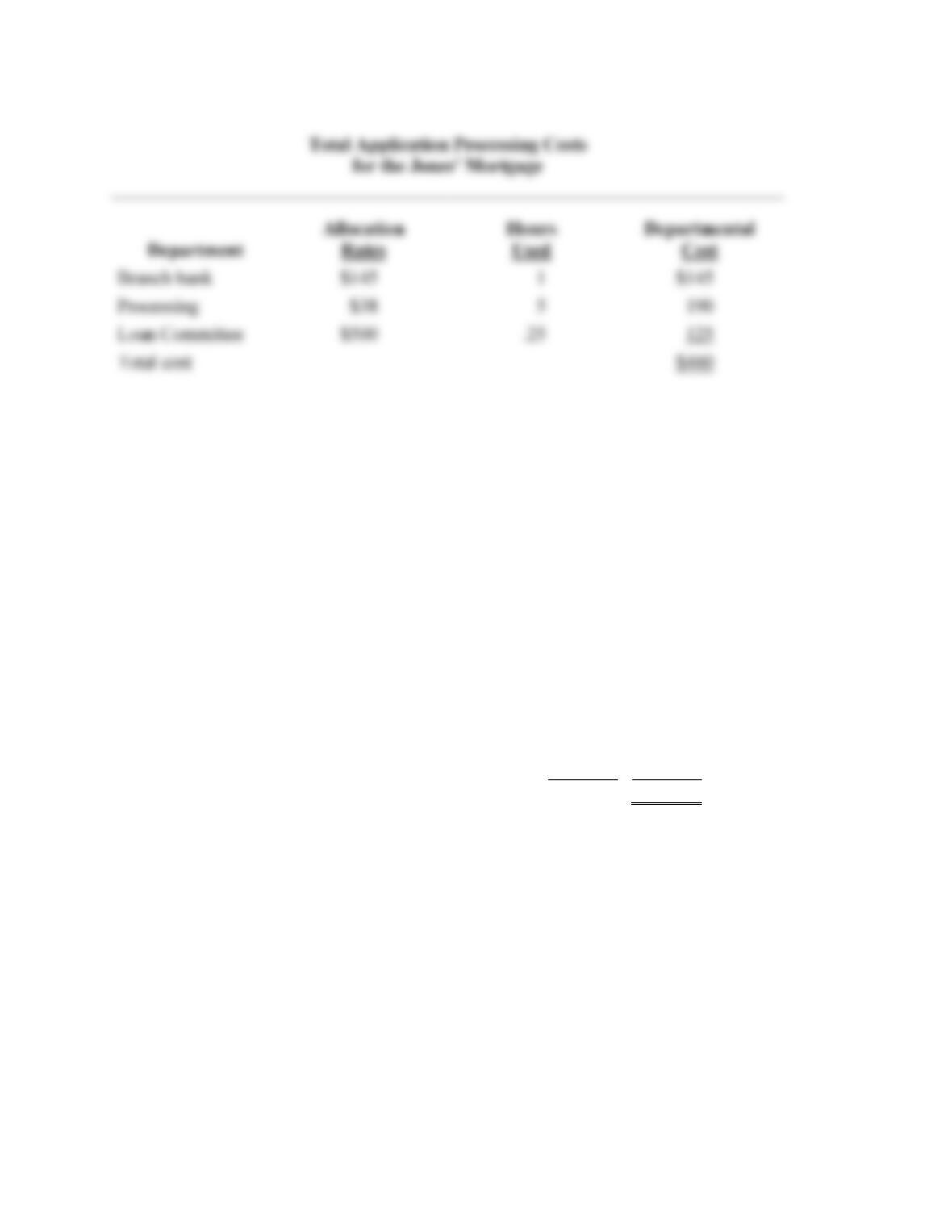

9-7: Solution to Absorption Costing in a Bank (25 minutes)

Branch bank

Processing

Loan Committee

Total cost

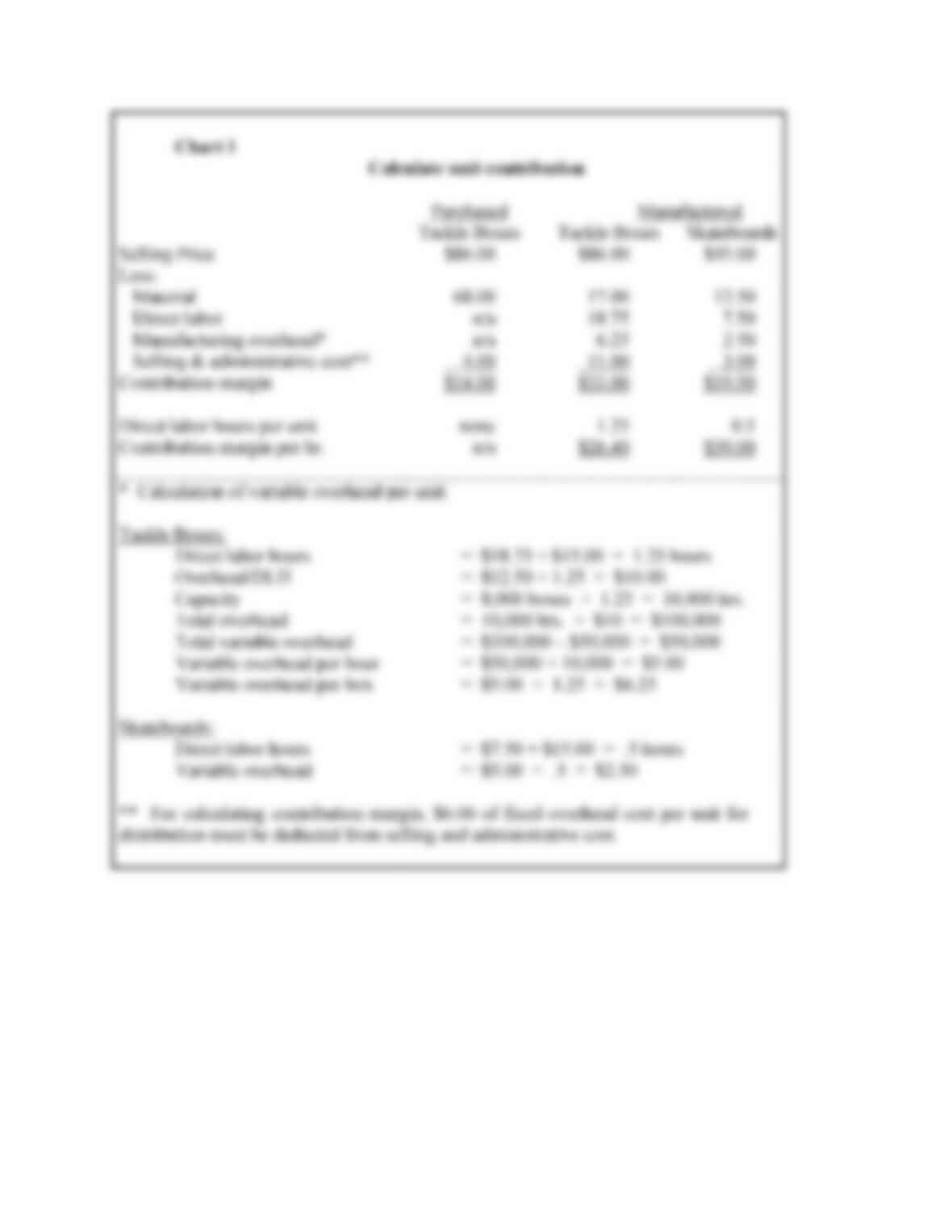

9-8: Product Profitability and Mix — Calculating Variable Overhead

Sportway Inc. is a wholesale distributor supplying a wide range of moderately priced

sporting equipment to large chain stores. About 60 percent of Sportway’s products are purchased

from other companies and the remainder are manufactured by Sportway. The company has a

plastics department that is currently manufacturing molded fishing tackle boxes. Sportway is able

to manufacture and sell 8,000 tackle boxes annually, making full use of its direct labor capacity at

available workstations. Presented below are the selling price and costs associated with Sportway’s

tackle boxes.

Selling price per box

$86.00

Costs per box

Molded plastic

$ 8.00

Hinges, latches, handle

9.00

Direct labor ($15.00/hr.)

18.75

Manufacturing overhead

12.50

Selling and administrative cost

17.00

65.25

Profit per box

$20.75

Because Sportway believes it could sell 12,000 tackle boxes if it had sufficient

manufacturing capacity, the company has looked into the possibility of purchasing the tackle boxes

for distribution. Maple Products, a steady supplier of quality products, would be able to provide

up to 9,000 tackle boxes per year at a price of $68 per box delivered to Sportway’s facility.

Bart Johnson, Sportway’s product manager, has suggested that the company could make

better use of its plastics department by manufacturing skateboards. To support his position,

Johnson has a market study that indicates an expanding market for skateboards and a need for

additional suppliers. Johnson believes that Sportway could expect to sell 17,500 skateboards

annually at $45 per skateboard. Johnson’s estimate of the costs to manufacture the skateboards

follows.

Selling price per skateboard

$45.00

Costs per skateboard

Molded plastic

5.50

Wheels, hardware

7.00

Direct labor ($15.00/hr.)

7.50

Manufacturing overhead

5.00

Selling and administrative cost

9.00

34.00

Profit per skateboard

$11.00

In the plastics department, Sportway uses direct labor hours as the application base for

manufacturing overhead. Included in manufacturing overhead for the current year is $50,000 of

factorywide, fixed manufacturing overhead that has been allocated to the plastics department. For

each product that Sportway sells, regardless of whether the product has been purchased or is

manufactured by Sportway, a portion of the selling and administrative cost is fixed at $6 per unit.

Total selling and administrative costs for the purchased tackle boxes would be $10 per unit.

Required:

Prepare an analysis based on the data presented that will show which product or products

Sportway Inc. should manufacture and/or purchase to maximize the company’s profitability. Show

the associated financial impact. Support your answer with appropriate calculations.

Source: CMA adapted.

9-8: Solution to Product Profitability and Mix – Calculating Variable Overhead (CMA

adapted) (50 minutes)