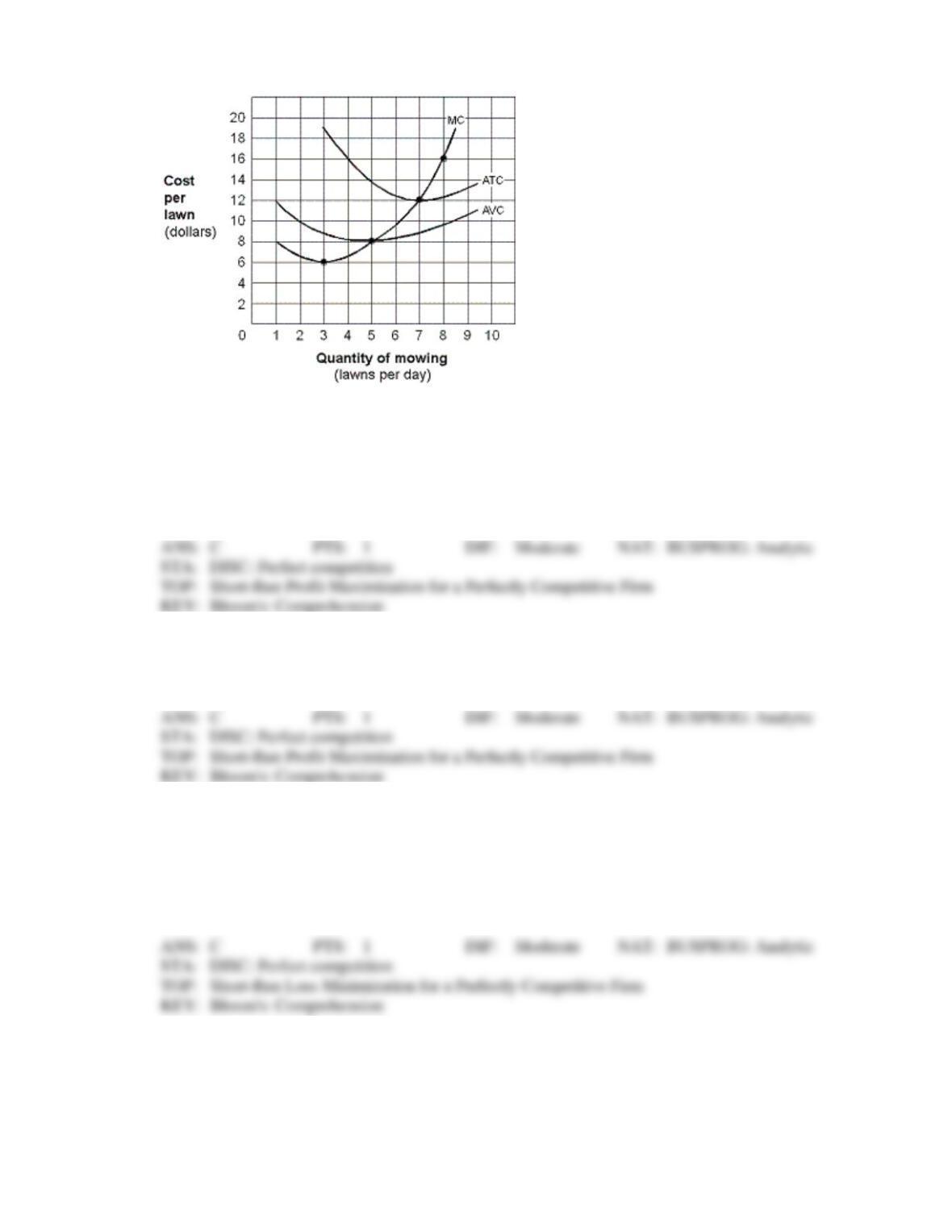

Exhibit 8-15 Short-run cost curves for E-Z Care lawn mowing company

158. In Exhibit 8-15, if the market price of mowing lawns is $16 per lawn, then E-Z-Care will earn the

biggest profit by mowing:

a.

5 lawns per day.

b.

7 lawns per day.

c.

8 lawns per day.

d.

as many lawns per day as is physically possible.

159. In Exhibit 8-15, what market price would cause E-Z-Care to just beak even?

a.

$6 per lawn.

c.

$12 per lawn.

b.

$8 per lawn.

d.

$16 per lawn.

160. In Exhibit 8-15, suppose the market price of mowing lawns falls to $10 per lawn. In this situation, E-

Z-Care will:

a.

permanently exit the industry.

b.

shut down its operations, at least in the short run.

c.

continue to mow lawns despite its economic losses.

d.

earn a normal profit.

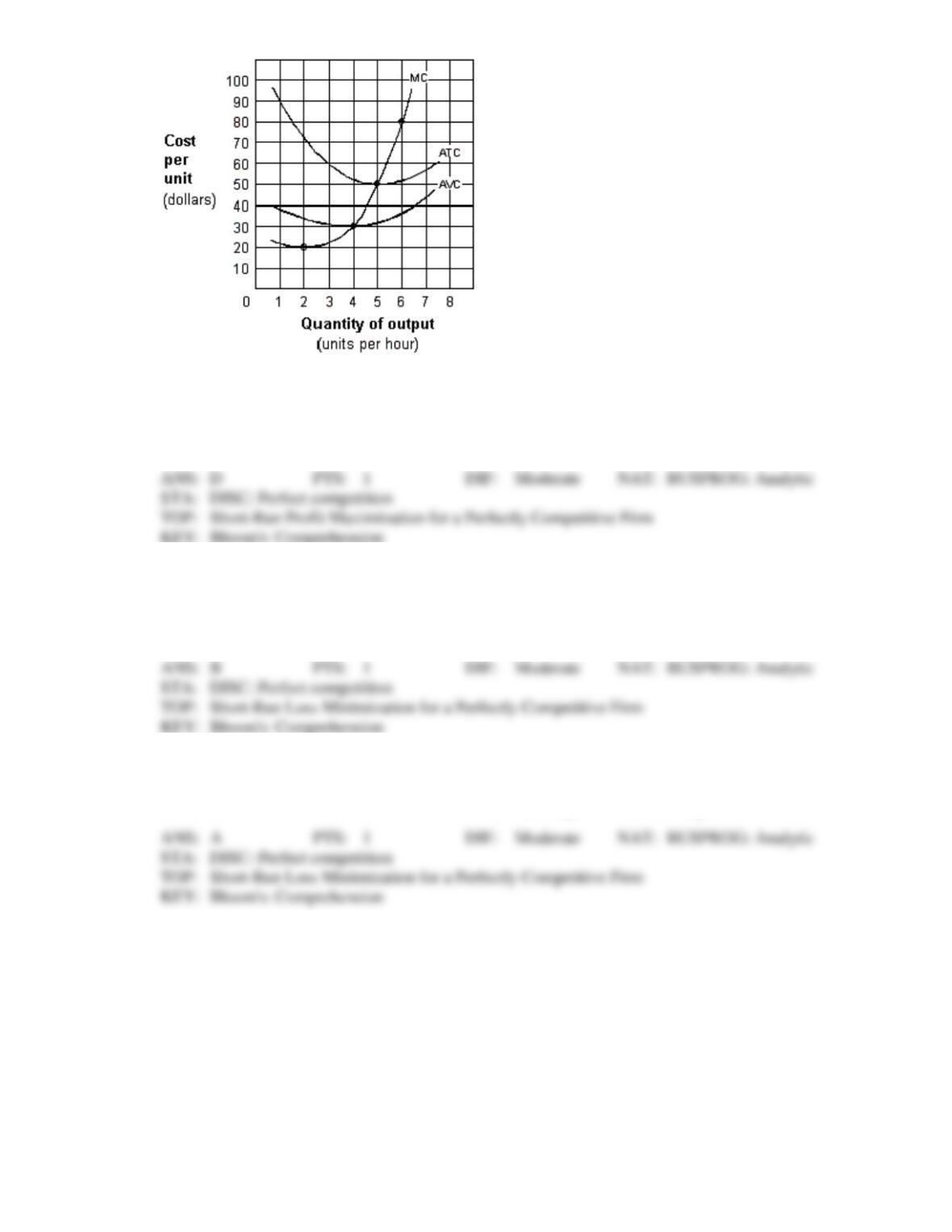

Exhibit 8-16 Short-run cost curves for a competitive firm

161. In Exhibit 8-16, suppose the firm faces a price of $80 per unit. How much should the firm produce to

earn the largest possible profit?

a.

2 units per hour.

c.

5 units per hour.

b.

4 units per hour.

d.

6 units per hour.

162. In Exhibit 8-16, the firm should shut down in the short run if the market price of its product falls

below:

a.

$20 per unit.

c.

$50 per unit.

b.

$30 per unit.

d.

$80 per unit.

163. In Exhibit 8-16, if the market price of its product is $50 per unit, then the firm will:

a.

break even.

c.

exit the industry.

b.

shut down.

d.

earn a positive economic profit.

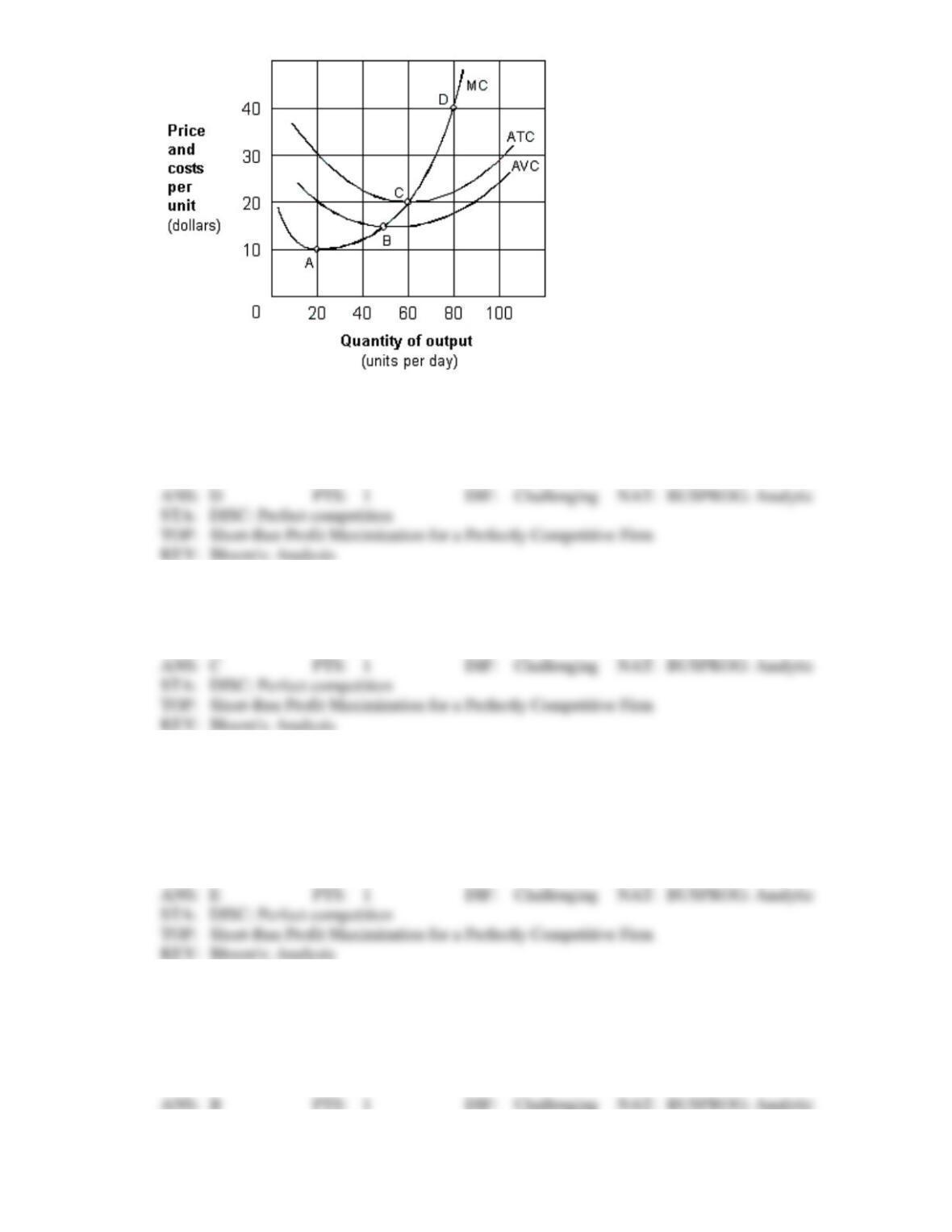

Exhibit 8-17 Marginal revenue and cost per unit curves

164. As shown in Exhibit 8-17, if the product price is either $10, $15, $20, or $40, the firm’s economic

profit is maximum at an output of:

a.

20 units per day.

c.

60 units per day.

b.

40 units per day.

d.

80 units per day.

165. In Exhibit 8-17, if the price of the firm’s product is $20 per unit, the firm will produce:

a.

20 units per day.

c.

60 units per day.

b.

40 units per day.

d.

80 units per day.

166. As shown in Exhibit 8-17, the price at which the firm earns zero economic profit in the short-run is:

a.

$10 per unit.

b.

$15 per unit.

c.

$40 per unit.

d.

more than $20 per unit.

e.

$20 per unit.

167. If the price of the firm’s product in Exhibit 8-17 is $15 per unit, the firm should:

a.

shut down permanently.

b.

stay in operation for the time being even though it is making a pure economic loss.

c.

shut down temporarily.

d.

continue to operate because it is earning a positive economic profit.

168. As shown in Exhibit 8-17, the firm will produce in the short run if the price is at least equal to:

a.

$10 per unit.

b.

$15 per unit.

c.

$20 per unit.

d.

$30 per unit.

e.

$40 per unit.

169. As shown in Exhibit 8-17, the short-run supply curve for the firm corresponds to which segment of its

marginal cost curve?

a.

C and all points above.

b.

B and all points above.

c.

A and all points above.

d.

A to C only.

e.

B to D only.

170. Which of the following is a key characteristic of the long-run competitive equilibrium that

distinguishes it from the short-run competitive equilibrium?

a.

Free entry to reduce short-run profits, or free exit to reduce short-run losses.

b.

Economic profits are positive, but cannot be negative.

c.

Marginal revenue is greater than marginal cost.

d.

Average revenue is less than average cost.

171. In long-run equilibrium, the typical perfectly competitive firm has no incentive to:

a.

change output.

c.

enter or leave the industry.

b.

change plant size.

d.

do any of these.

172. What is the largest possible loss that is consistent with a firm producing in a perfectly competitive

market in long-run competitive equilibrium?

a.

An amount equal to (price less average variable cost).

b.

An amount equal to total variable.

c.

Zero.

d.

An amount equal to total fixed cost.

173. The long run is a planning period:

a.

during which the firm can vary its plant size.

b.

less than six months.

c.

less than one year.

d.

less than five years.

174. In long-run equilibrium, the perfectly competitive firm sets its price equal to which of the following?

a.

Short-run average total cost.

c.

Long-run average cost.

b.

Short-run marginal cost.

d.

All of these.

175. In long-run equilibrium, which of the following is not equal to price for a perfectly competitive firm?

a.

Short-run average variable cost.

c.

Short-run marginal cost.

b.

Long-run average total cost.

d.

Short-run average total cost.

176. In long-run equilibrium, a competitive firm produces the level of output at which:

a.

marginal cost is at a minimum.

b.

short-run average total cost and long-run average cost are at a minimum.

c.

total revenue is at a maximum.

d.

diseconomies of scale end.

177. Which of the following statements is true?

a.

To maximize profits, a firm must maximize total revenue.

b.

In long-run equilibrium, a competitive firm produces at the point of minimum average

total cost.

c.

In the short-run, a perfectly competitive firm produces where total cost is minimum.

d.

In the short-run, a perfectly competitive firm will close down whenever price is less than

average total cost.

178. In long-run equilibrium for a perfectly competitive firm, price equals which of the following?

a.

Economies of scale.

b.

Minimum short-run average total cost.

c.

The sum of each short-run marginal cost curve.

d.

All of these.

179. In the long-run equilibrium for a perfectly competitive firm, price equals which of the following?

a.

price.

c.

short-run marginal cost.

b.

minimum short-run average total cost.

d.

All of these.

180. If there is a permanent increase in demand for the product of a perfectly competitive industry, the

process of transition to a new long-run equilibrium will include:

a.

the entry of new firms.

c.

both a and b.

b.

temporarily higher profits.

d.

neither a nor b.

181. In long-run equilibrium, the typical perfectly competitive firm will:

a.

earn zero economic profit.

c.

change output in the short run.

b.

change plant size in the long run.

d.

do any of these.

182. In long-run equilibrium for a perfectly competitive firm, price equals which of the following?

a.

Economies of real cost.

b.

Maximum total revenue.

c.

Diseconomies of scale cost.

d.

Minimum point on the long-run average cost curve.

183. In a perfectly competitive industry, assume there is a permanent increase in demand for a product. The

process of transition to a new long-run equilibrium will include:

a.

the exit of firms.

c.

both a and b.

b.

temporarily lower production costs.

d.

neither a nor b.

184. In a perfectly competitive industry, assume the short-run average total cost increases as the output of

the industry expands. In the long run, the industry supply curve will:

a.

first have a positive slope and then a negative slope.

b.

have a negative slope.

c.

be perfectly horizontal.

d.

be perfectly vertical.

e.

have a positive slope.

185. Under long-run perfect competition, which of the following are the same (equal) at all levels of

output?

a.

Price and marginal cost.

c.

Marginal cost and marginal revenue.

b.

Price and marginal revenue.

d.

All of these.

186. Suppose that in a perfectly competitive market, firms are making economic profits. In the long run, we

can expect to see:

a.

some firms leave.

b.

the market price rise.

c.

market supply shift to the left.

d.

economic profits become zero.

e.

production levels remaining the same as in the short-run.

187. The long-run equilibrium condition for perfect competition is:

a.

P = AVC = MR = MC.

b.

P = ATC = MR = MC.

c.

Q = AVC = MR = MC.

d.

Q = ATC = MR = MC.

e.

TR = ATC = MR = MC.

188. Consider a firm operating with the following: price = 10; MR = 10; MC = 10; ATC = 10. This firm is:

a.

making an economic profit of 10.

b.

an example of monopolistic competition.

c.

going to go out of business in the long run.

d.

a monopolist for a product with a relatively inelastic demand.

e.

perfectly competitive in long-run equilibrium.

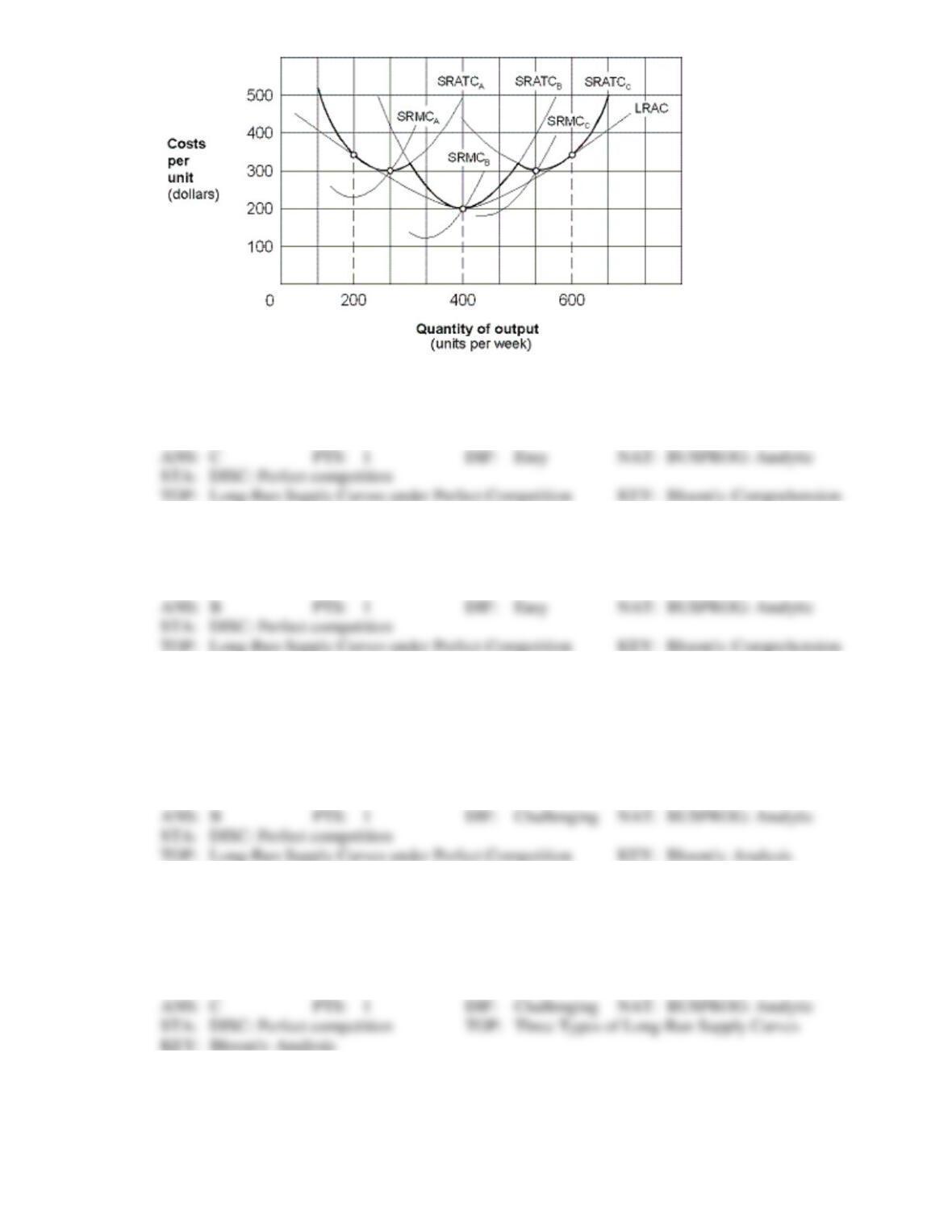

Exhibit 8-18 A typical firm in a perfectly competitive market

189. As shown in Exhibit 8-18, the perfectly competitive firm is in long-run equilibrium at an output of:

a.

zero units per week.

c.

400 units per week.

b.

200 units per week.

d.

600 units per week.

190. As shown in Exhibit 8-18, the perfectly competitive firm is in long-run equilibrium at a price of:

a.

$100.

c.

$300.

b.

$200.

d.

$400.

191. In Exhibit 8-18, assume the perfectly competitive firm is in long-run equilibrium and there is an

increase in demand. As a result, the firm in the short run will increase output along its:

a.

short-run average total cost curve B.

b.

short-run marginal cost curve B.

c.

long-run average cost curve.

d.

none of these because the firm shuts down.

192. In a constant cost industry:

a.

a natural monopoly is likely to occur.

b.

total cost is the same, no matter how much a firm produces.

c.

the long-run supply curve will be perfectly elastic.

d.

entry of new firms in the industry will lead to a reduction in the cost of inputs.

193. If the expansion of output in an industry leads to unchanged resource prices, the industry is most likely

to be a(n):

a.

decreasing cost industry.

b.

increasing cost industry.

c.

constant cost industry.

d.

industry characterized by economies of scale.

194. If resource prices rise and the per-unit cost of producing a product increases as the firms in an industry

expand output in response to an increase in demand, the long-run market supply curve for the product

will:

a.

be perfectly elastic (a horizontal line).

b.

be perfectly inelastic (a vertical line).

c.

slope upward to the right.

d.

be more inelastic than the short-run supply curve for the product.

195. If the demand for a product increases in an increasing cost industry, as the market adjusts in the long

run:

a.

price will rise.

b.

the firm’s per-unit cost will increase.

c.

the firm’s per-unit cost will fall.

d.

the market price will return to its initial position.

196. Assume the short-run average total cost for a perfectly competitive industry remains constant as the

output of the industry expands. In the long run, the industry supply curve will:

a.

have a positive slope.

c.

be perfectly horizontal.

b.

have a negative slope.

d.

be perfectly vertical.

197. Assume the short-run average total cost for a perfectly competitive industry decreases as the output of

the industry expands. In the long run, the industry supply curve will:

a.

have a positive slope.

c.

be perfectly horizontal.

b.

have a negative slope.

d.

be perfectly vertical.

198. Assume the short-run average total cost for a perfectly competitive industry increases as the output of

the industry expands. In the long run, the industry supply curve will:

a.

have a positive slope.

c.

be perfectly horizontal.

b.

have a negative slope.

d.

be perfectly vertical.

199. If input prices for a perfectly competitive industry remain constant as the output of the industry

expands in the long run, the industry supply curve will:

a.

have a positive slope.

c.

be perfectly horizontal.

b.

have a negative slope.

d.

be perfectly vertical.

200. If a perfectly competitive industry’s long-run supply curve is downward sloping, we can conclude that

input prices will:

a.

increase as industry output increases.

b.

decrease as industry output increases.

c.

remain constant as industry output increases.

d.

none of these conclusions can be drawn.

201. If input prices for a perfectly competitive firm increase as the output of the industry expand in the long

run, the long-run industry supply curve will:

a.

have a positive slope.

c.

be perfectly horizontal.

b.

have a negative slope.

d.

be perfectly vertical.

202. In a constant-cost industry, input prices remain constant as:

a.

the supply of inputs fluctuates.

c.

workers become more experienced.

b.

firms encounter diseconomies of scale.

d.

firms enter and exit the industry.

203. Suppose that, in the long run, the price of feature films rises as the movie production industry expands.

We can conclude that movie production is a(n):

a.

increasing-cost industry.

c.

decreasing-cost industry.

b.

constant-cost industry.

d.

marginal-cost industry.

204. As the electronic components industry expands, the salaries paid to electrical engineers rise in

response to higher demand. We can conclude that the electronic components industry is:

a.

a constant-cost industry.

c.

a decreasing-cost industry.

b.

an increasing-cost industry.

d.

a marginal-cost industry.

205. The long-run supply curve for a competitive constant-cost industry is:

a.

horizontal.

c.

upward-sloping.

b.

vertical.

d.

downward-sloping.

206. Which of the following is true of a perfectly competitive market?

a.

If economic profits are earned then the price will fall over time.

b.

In long-run equilibrium P = MR = SRMC = SRATC = LRAC.

c.

A constant-cost industry exists when the entry of new firms has no effect on their cost

curves.

d.

All of these.

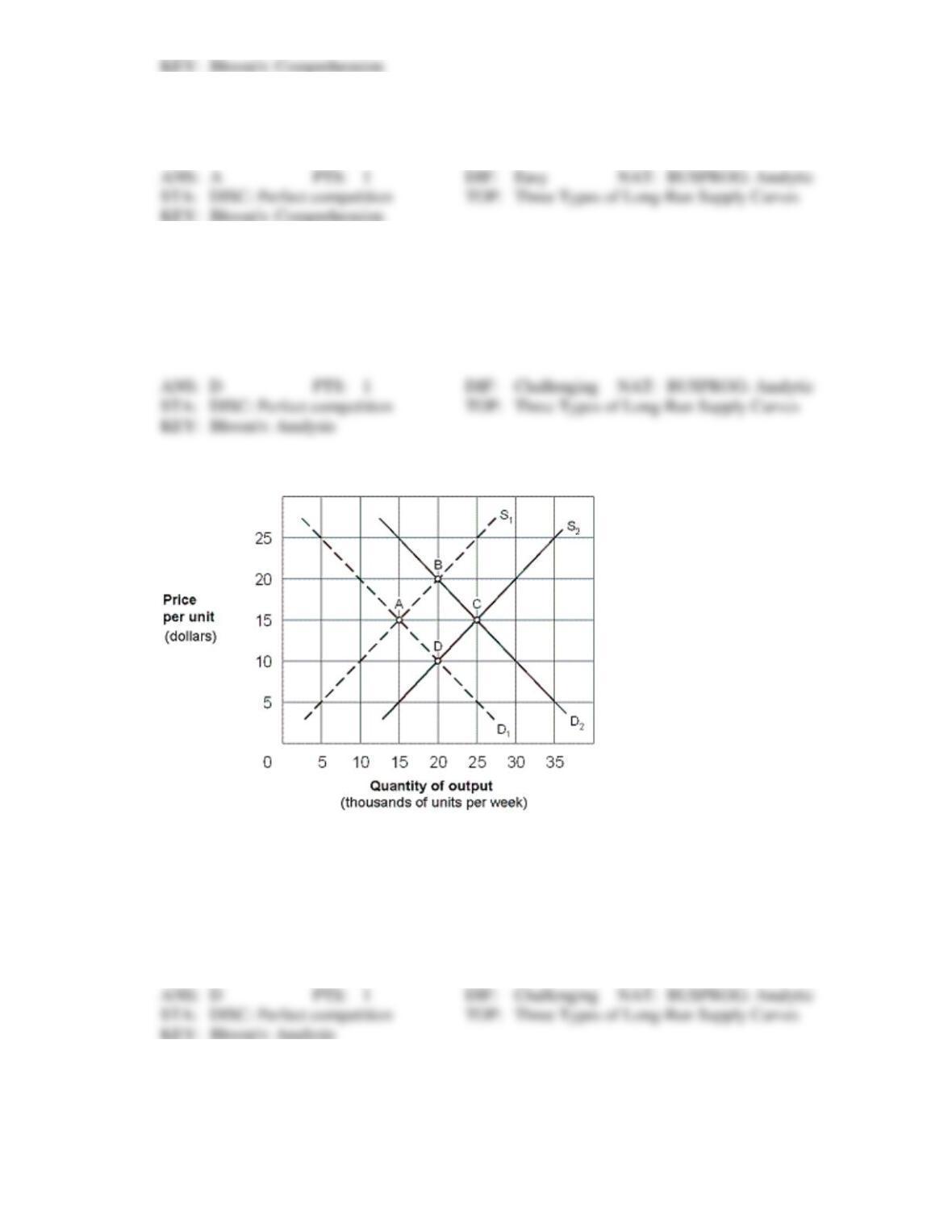

Exhibit 8-19 Long-run perfectly competitive industry

207. As shown in Exhibit 8-19, assume that a perfectly competitive industry is in long-run equilibrium at

point A and the demand curve shifts from D1 to D2. Which of the following is a part of the industry

adjustment process?

a.

The price will temporarily rise at point B.

b.

New firms will enter the industry.

c.

Firms will temporarily make positive economic profits.

d.

All of these.

208. As shown in Exhibit 8-19, assume that a perfectly competitive industry is in long-run equilibrium at

point A. If the demand curve shifts from D1 to D2, the adjustment sequence between points will be:

a.

A to B, then back to A.

c.

A to D, then to C.

b.

A to D, then back to A.

d.

A to B, then to C.

209. As shown in Exhibit 8-19, assume that a perfectly competitive industry is in long-run equilibrium at

point A and the demand curve shifts from D1 to D2. The result is a long-run supply curve drawn from

point:

a.

A to point B.

c.

A to point D.

b.

B to point A.

d.

A to point C.

TRUE/FALSE

1. Competitive firms frequently use advertising to differentiate their product from their competitors’

products.

2. A perfectly competitive market is characterized by the free entry and exit of firms.

3. A perfectly competitive market is characterized by highly advertised goods.

4. If a perfectly competitive firm charges more than the market price, then it loses all of its customers.

5. In the short run, the profit maximizing (or minimizing) quantity of output for any firm to produce

exists at that output level at which marginal revenue equals marginal cost.

6. If a firm is producing an output level at which marginal revenue exceeds marginal cost, the firm will

increase profits by reducing its output level.

7. In the short run, a firm should shut down if its economic loss from operating exceeds its total fixed

cost.

8. If at some output level for a firm price exceeds average total cost, then the firm is earning an economic

profit.

9. If marginal revenue exceeds marginal cost in the short run, the perfectly competitive firm earns an

economic profit in the short-run.

10. If marginal revenue equals marginal cost in the short run, the perfectly competitive firm earns zero

profits.

11. If marginal revenue exceeds marginal cost in the short run, total revenue for the perfectly competitive

firm is greater than total cost.

12. A perfectly competitive firm will shut down in the short run when marginal revenue equals marginal

cost at a price less than minimum average variable cost.

13. The short-run supply curve and short-run marginal cost curve for a perfectly competitive firm coincide

when the market price is greater than average variable cost.

14. In the short run, the profit maximizing (or minimizing) quantity of output for any firm to produce

exists at that output level at which marginal revenue equals marginal cost.

15. If a firm is producing an output level at which marginal revenue exceeds marginal cost in the short run,

the firm will increase profits by reducing its output level.

16. If a perfectly competitive firm cannot cover all of its costs, then it should shut down in the short run.

17. When faced with an economic loss, a competitive firm will shut down its operations in the short run.

18. A perfectly competitive firm shuts down in the short-run when the market price is less than the average

variable cost.

19. In the short run, the supply curve for a perfectly competitive firm is its marginal cost curve for all

levels of output.

20. A perfectly competitive firm’s short-run supply curve is its marginal cost curve below its average

variable cost curve.

21. In long-run equilibrium, a perfectly competitive firm’s short-run marginal cost curve crosses the long-

run average cost curve at the lowest point on the long-run average cost curve.

22. A perfectly competitive industry must have a perfectly elastic long-run supply curve.

23. In long-run equilibrium, a perfectly competitive firm will produce an output level at which its long-run

average cost curve is upward sloping.

24. In the long run, a competitive firm will earn zero economic profit.

25. When faced with an economic loss, a competitive firm will exit the industry in the long run.

26. In long-run equilibrium, a perfectly competitive firm’s short-run marginal cost curve crosses the long-

run average cost curve at the lowest point on the long-run average cost curve.

27. The long-run supply curve for a competitive industry always has a positive slope.

28. A perfectly competitive industry always has a perfectly elastic (flat) long-run supply curve.

ESSAY

1. What are the characteristics of the perfectly competitive market?

2. What is the profit maximizing (loss minimizing) quantity for the perfectly competitive firm to

produce?

3. What is a firm’s short run supply curve?

4. Assume a competitive market has firms earning large economic profits. What is expected to happen

over time in this competitive market and to firm’s profits?

5. What are the pros and cons of a competitive market in the long run?