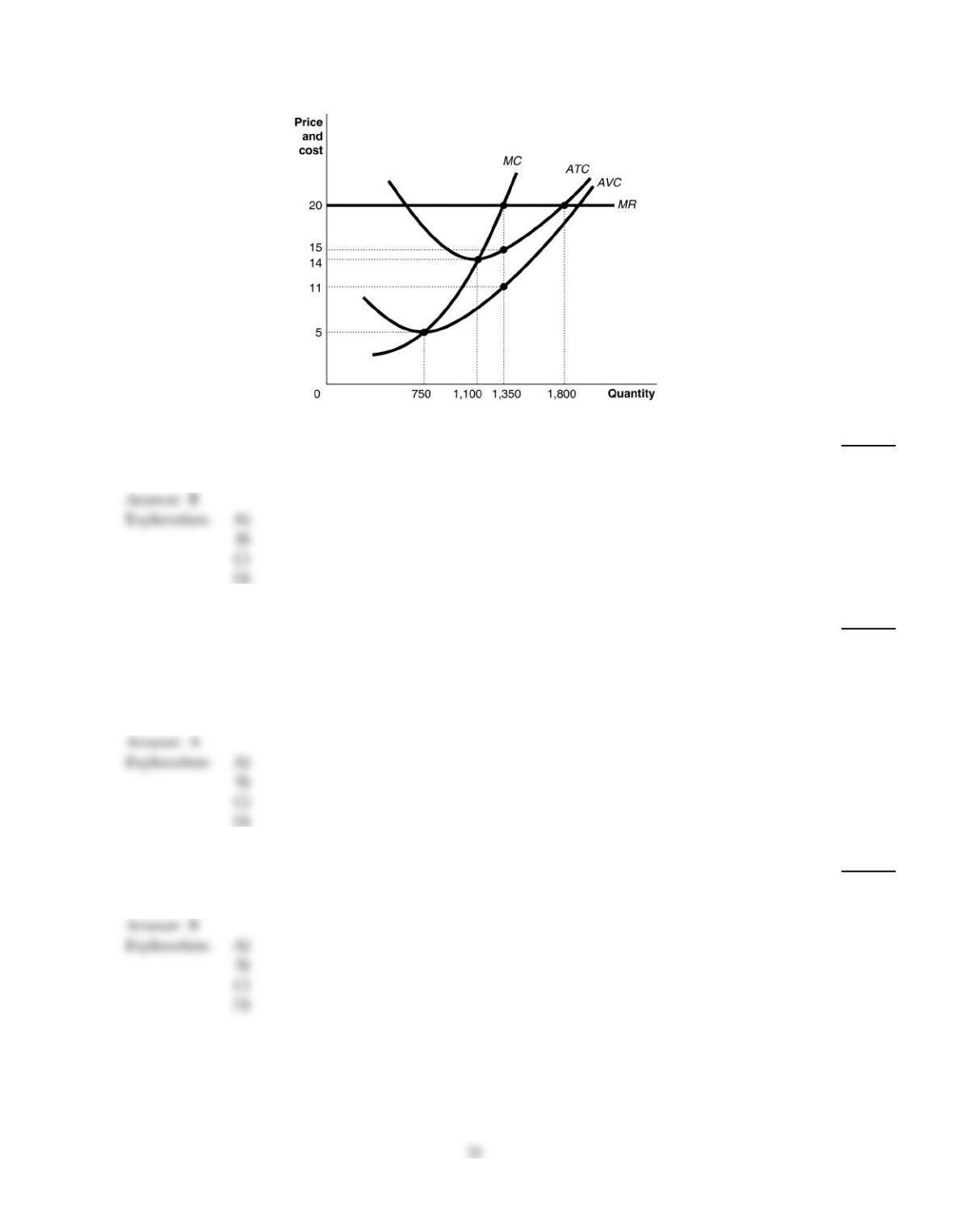

Figure 8–7

48)

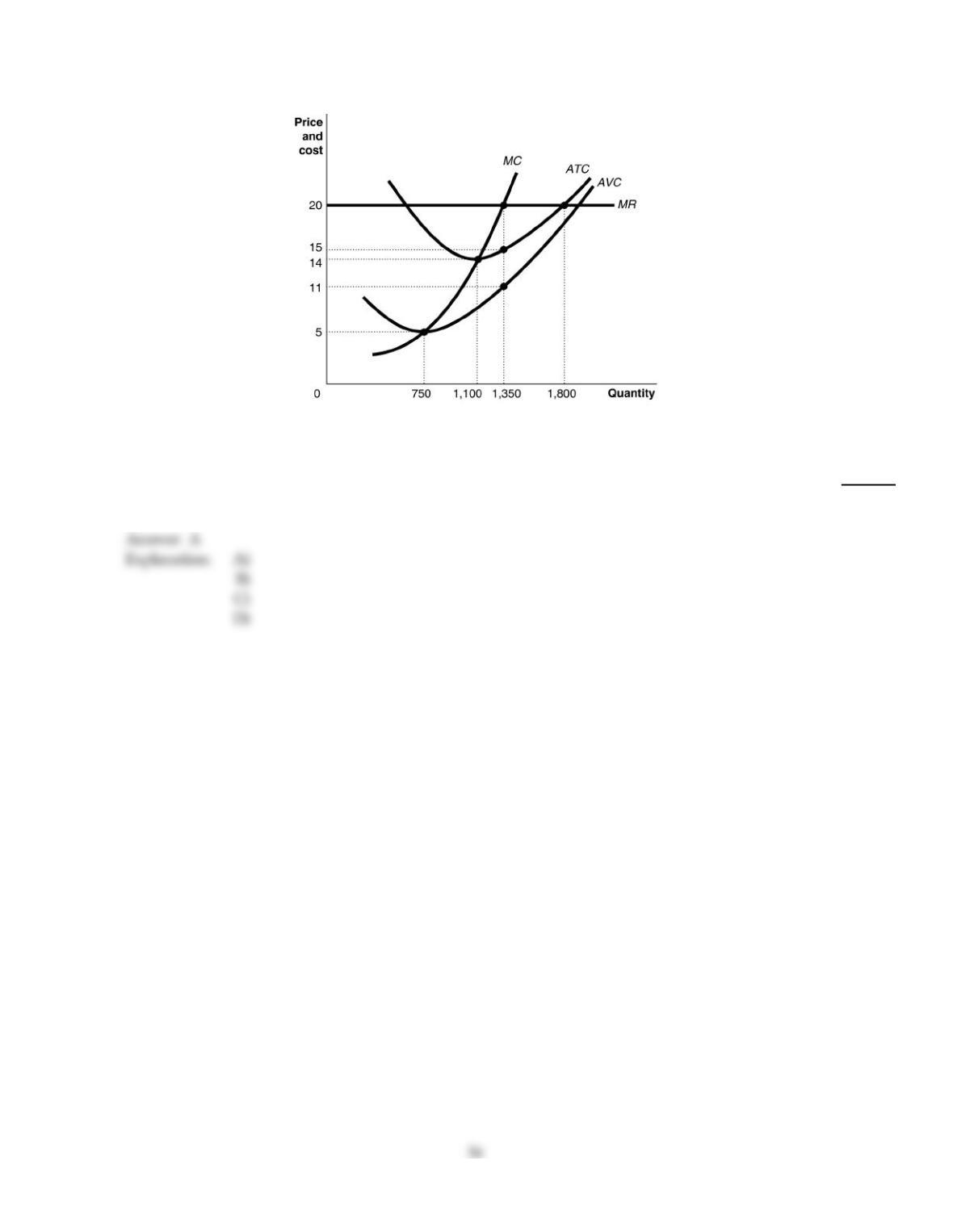

Refer to Figure 8–7. If this is a constant cost industry, what is the market price in the long run

equilibrium?

48)

A)

$20

B)

$14

C)

$5

D)

$15

49)

Refer to Figure 8–7. Suppose the prevailing price is $20 and the firm is currently producing 1,350

units. In the long run equilibrium, the firm represented in the diagram

49)

A)

will reduce its output to 1,100 units.

B)

will reduce its output to 750 units.

C)

will cease to exist.

D)

will continue to produce the same quantity.

50)

If the market price is $25 in a perfectly competitive market, the marginal revenue from selling the

fifth unit is

50)

A)

$12.50.

B)

$25.

C)

$5.

D)

$125.

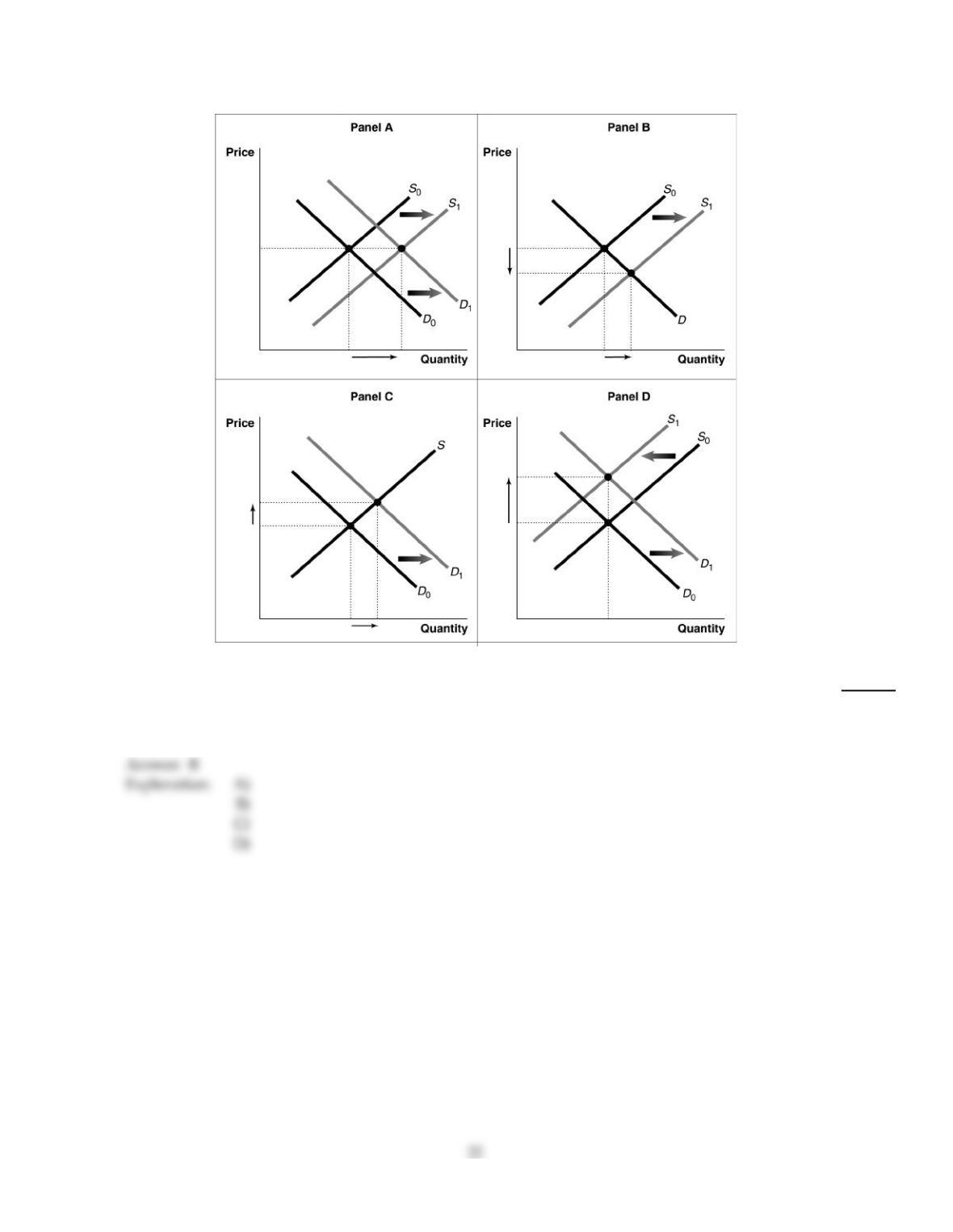

Figure 8–8

51)

Refer to Figure 8–8. Consider a typical firm in a perfectly competitive industry that makes

short–run profits. Which of the diagrams in the figure shows the effect on the industry as it

transitions to a long–run equilibrium?

51)

A)

Panel A

B)

Panel B

C)

Panel C

D)

Panel D

52)

“Between 1997 and 2001, many apple farmers switched from traditional to organic growing

methods, increasing production of organically grown apples from 1.2 million boxes per year to

more than 3 million boxes.” If the market for organic apples is perfectly competitive, which of the

following statements is inconsistent with the statement above?

52)

A)

The additional supply of organic apples resulted in a lower price for organic apples.

B)

It is relatively easy to enter the organic apples market.

C)

The price of organic apples is likely to rise over time as more and more farmers switch to

organic methods of farming.

D)

Organic apple farmers earned short–run economic profits between 1997 and 2001.

53)

A firm’s total profit can be calculated as all of the following except

53)

A)

(price minus average total cost) times quantity sold.

B)

total revenue minus total cost.

C)

average profit per unit times quantity sold.

D)

marginal profit times quantity sold.

54)

A perfectly competitive industry achieves allocative efficiency because

54)

A)

goods and services are produced at the lowest possible cost.

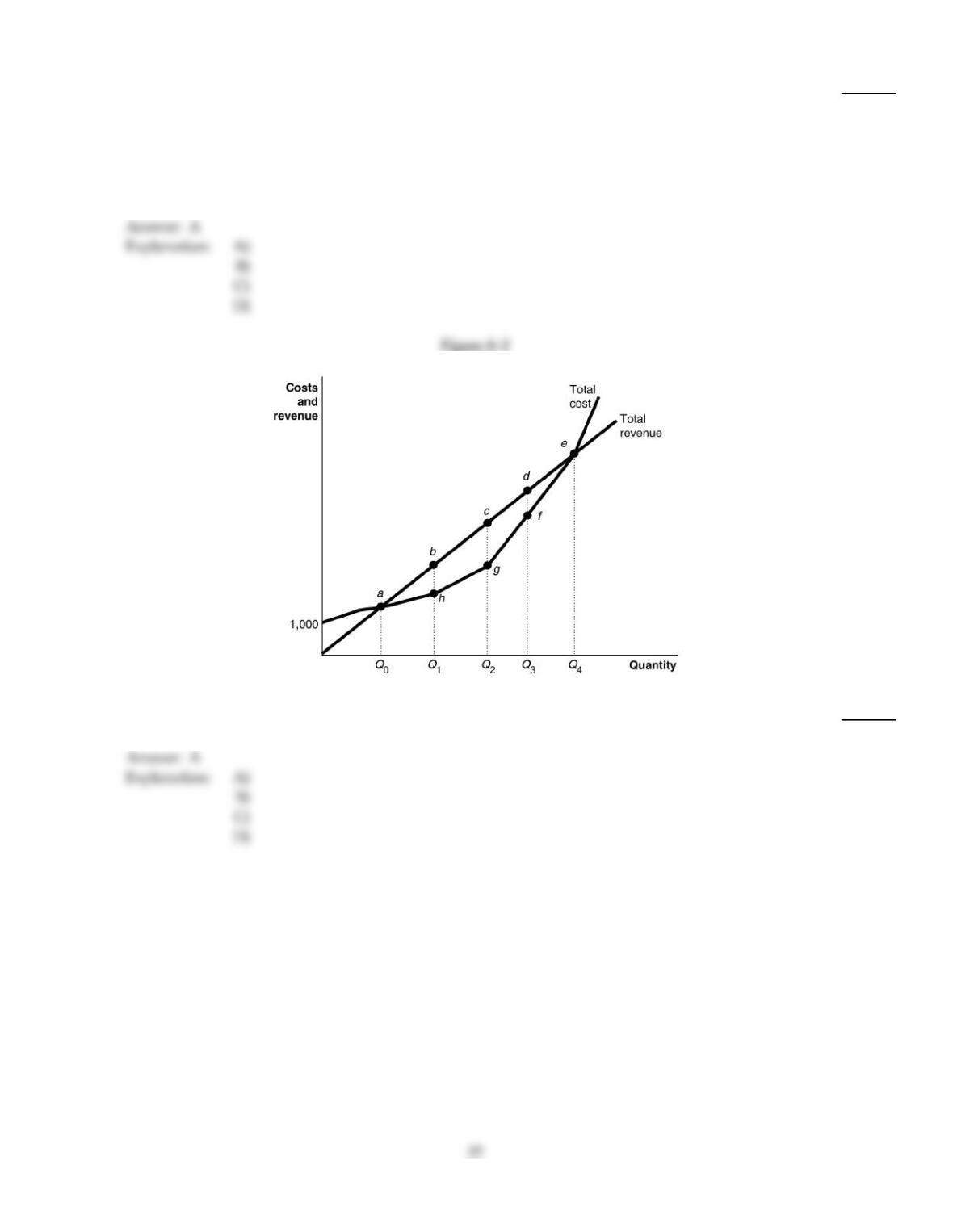

B)

it produces where market price equals marginal production cost.

C)

goods and services are produced up to the point where the last unit provides a marginal

benefit to consumers equal to the marginal cost of producing it.

D)

firms carry production surpluses.

55)

Which of the following is not true for a firm in perfect competition?

55)

A)

Price equals average revenue.

B)

Profit equals total revenue minus total cost.

C)

Average revenue is greater than marginal revenue.

D)

Marginal revenue equals the change in total revenue from selling one more unit.

56)

If a perfectly competitive firm’s price is less than its average total cost but greater than its average

variable cost, the firm

56)

A)

is incurring a loss.

B)

is breaking even.

C)

should shut down.

D)

is earning a profit.

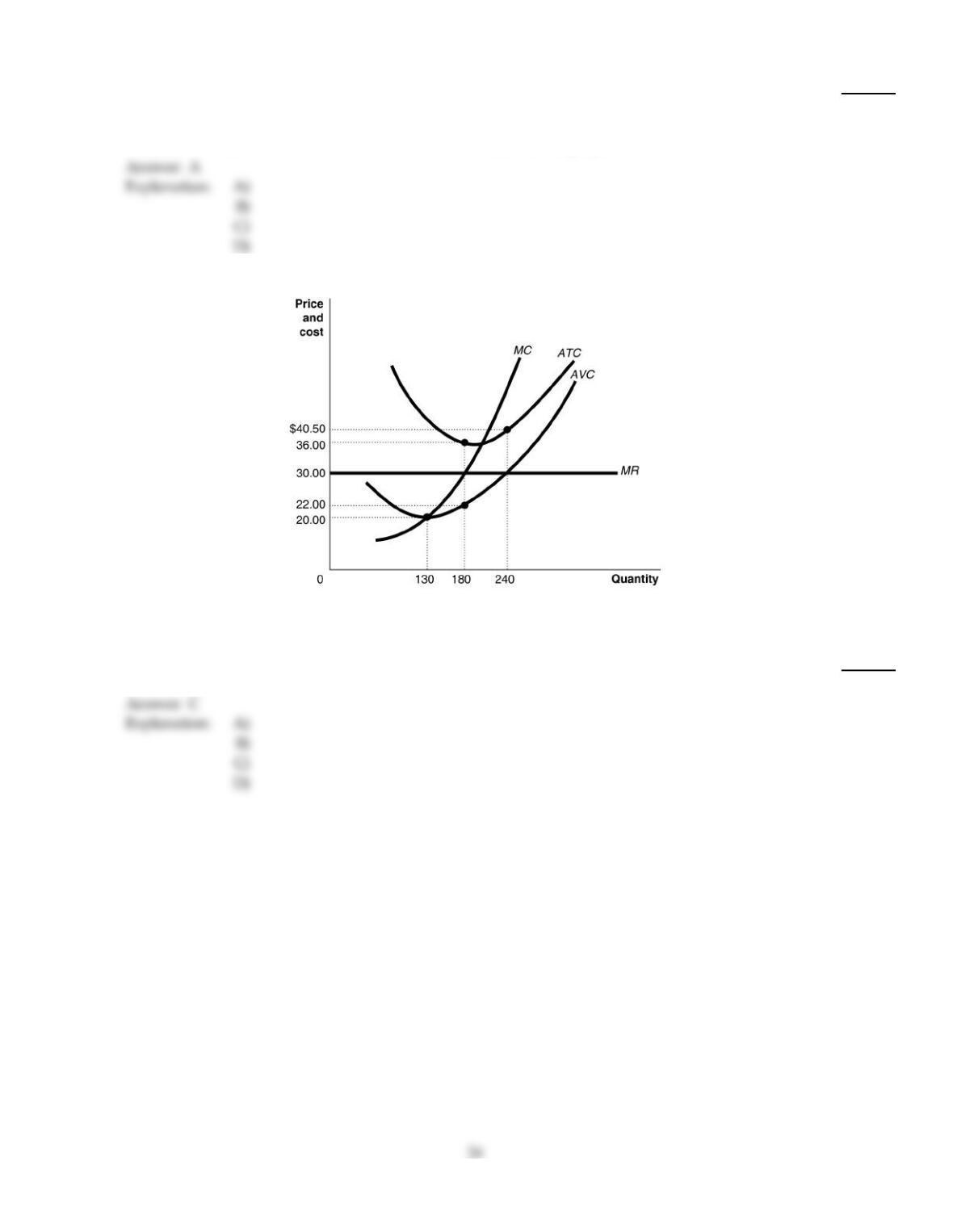

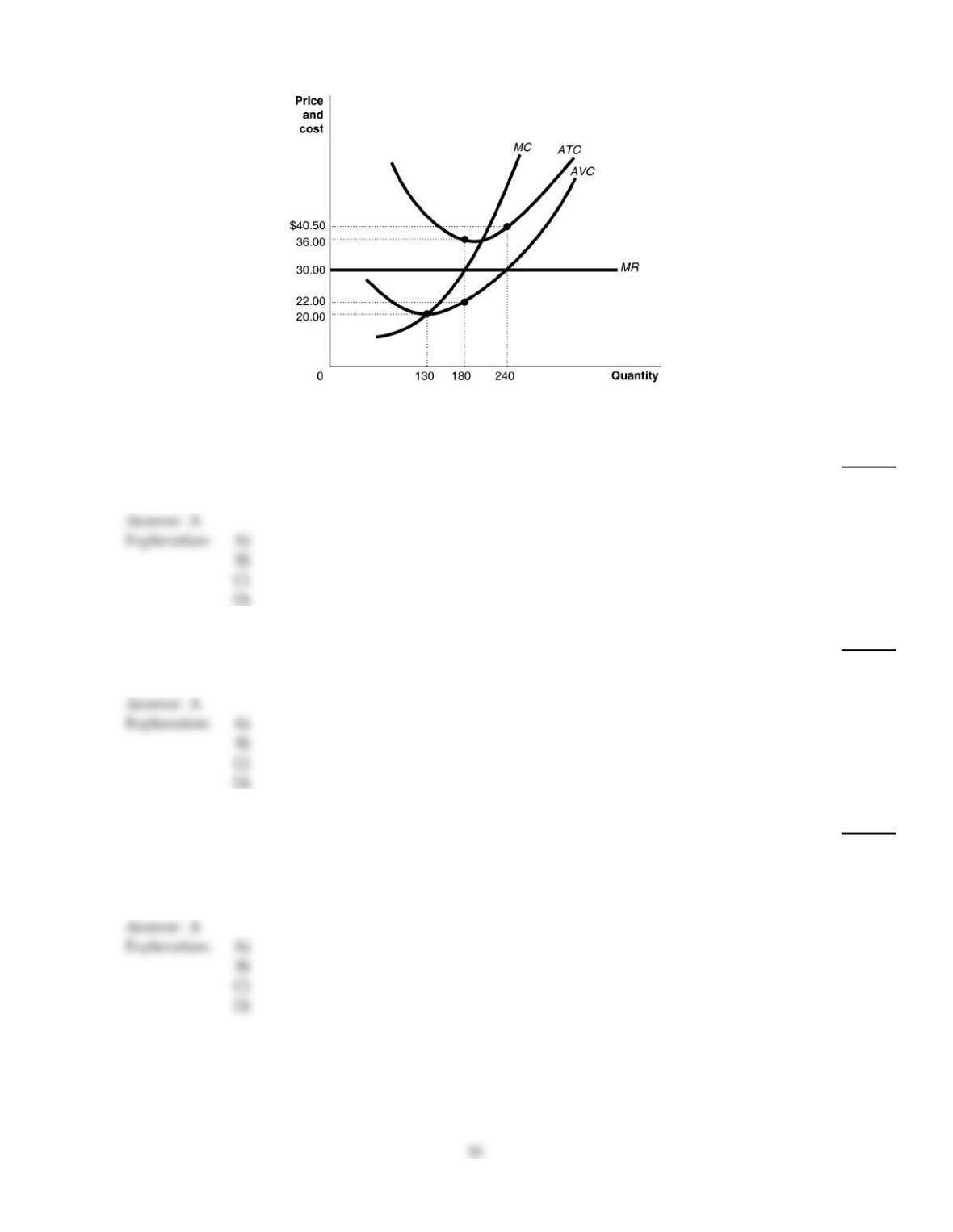

Figure 8–4

Figure 8–4 shows the cost and demand curves for a profit–maximizing firm in a perfectly competitive market.

57)

Refer to Figure 8–4. If the market price is $30, the firm’s profit maximizing output level is

57)

A)

0.

B)

130.

C)

180.

D)

240.

Figure 8–11

58)

Refer to Figure 8–11. Suppose a typical firm in a perfectly competitive market is earning economic

profits in the short run. Which of the diagrams in the Figure depicts what happens to in the

industry as it transitions to long–run equilibrium?

58)

A)

Panel A

B)

Panel B

C)

Panel C

D)

Panel D

59)

The demand for an individual seller’s product in perfect competition is

59)

A)

the same as market demand.

B)

horizontal.

C)

downward sloping.

D)

vertical.

60)

Which of the following is not a characteristic of monopoly?

60)

A)

The firms sells a unique product.

B)

There is only one seller in the market.

C)

The demand curve for a monopoly firm is the same as the demand curve for the industry. .

D)

It is easy for new firms to enter the market.

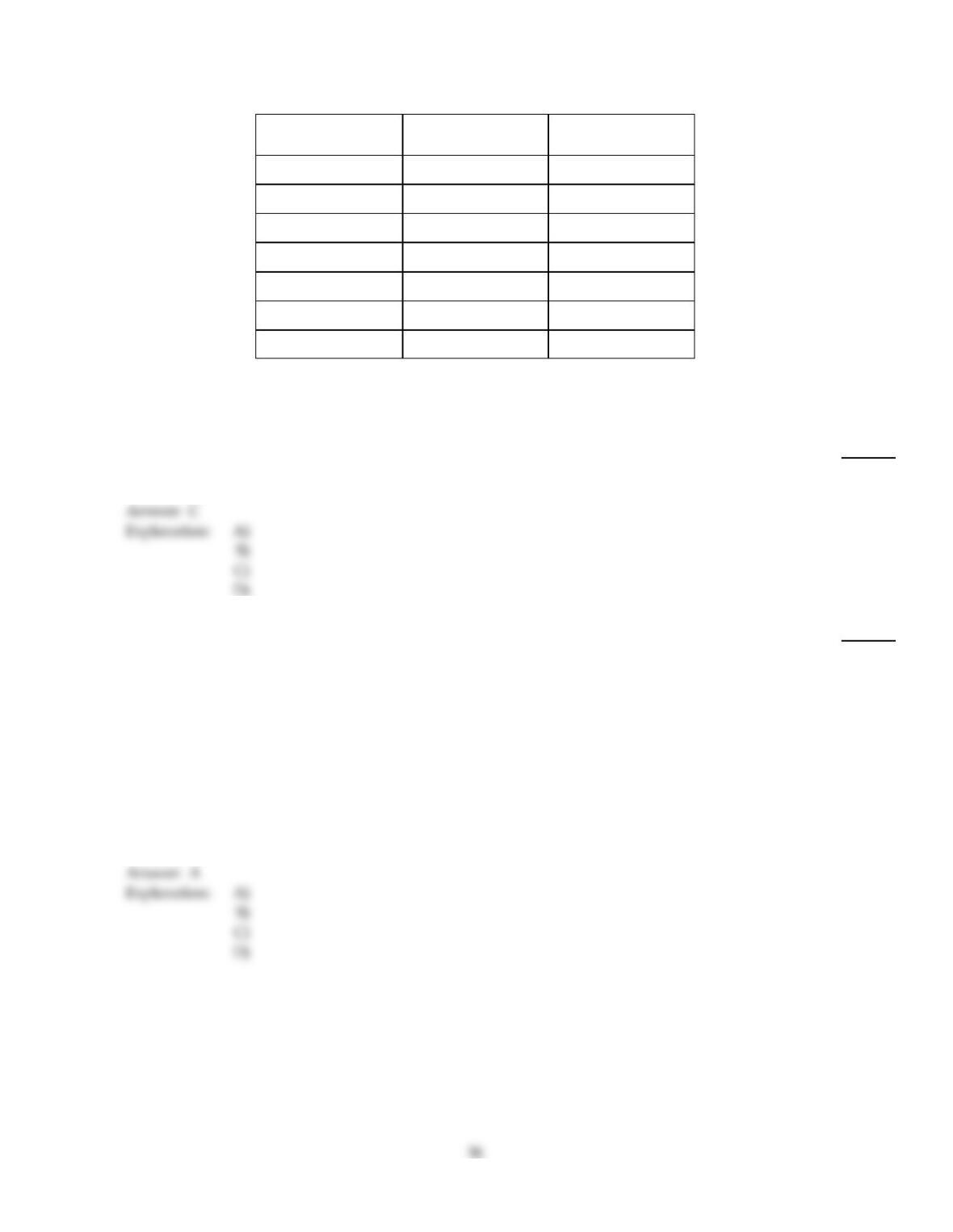

Table 8–1

Quantity Total Cost

(Dollars)

Variable Cost

(Dollars)

0$1,000 $0

100 1,360 360

200 1,560 560

300 1,960 960

400 2,760 1,760

500 4,000 3,000

600 5,800 4,800

Table 8–1 shows the short–run cost data of a perfectly competitive firm that produces plastic camera cases. Assume that

output can only be increased in batches of 100 units.

61)

Refer to Table 8–1. If the market price of each camera case is $8 what is the firm’s total revenue?

61)

A)

$2,400

B)

$3,200

C)

$4000

D)

$4,800

62)

In a perfectly competitive industry in long–run equilibrium

62)

A)

the typical firm is producing at the output where its long–run average total cost is not

minimized.

B)

the typical firm earns zero profit.

C)

is maximizing its revenue.

D)

the typical firm is earning an accounting profit greater than its implicit costs.

Table 8–1

Quantity Total Cost

(Dollars)

Variable Cost

(Dollars)

0$1,000 $0

100 1,360 360

200 1,560 560

300 1,960 960

400 2,760 1,760

500 4,000 3,000

600 5,800 4,800

Table 8–1 shows the short–run cost data of a perfectly competitive firm that produces plastic camera cases. Assume that

output can only be increased in batches of 100 units.

63)

Refer to Table 8–1. If the market price of each camera case is $8 what is the profit–maximizing

quantity?

63)

A)

300 units

B)

400 units

C)

500 units

D)

600 units

64)

Which of the following is the best example of a perfectly competitive industry?

64)

A)

wheat production

B)

airplane production

C)

electricity production

D)

steel production

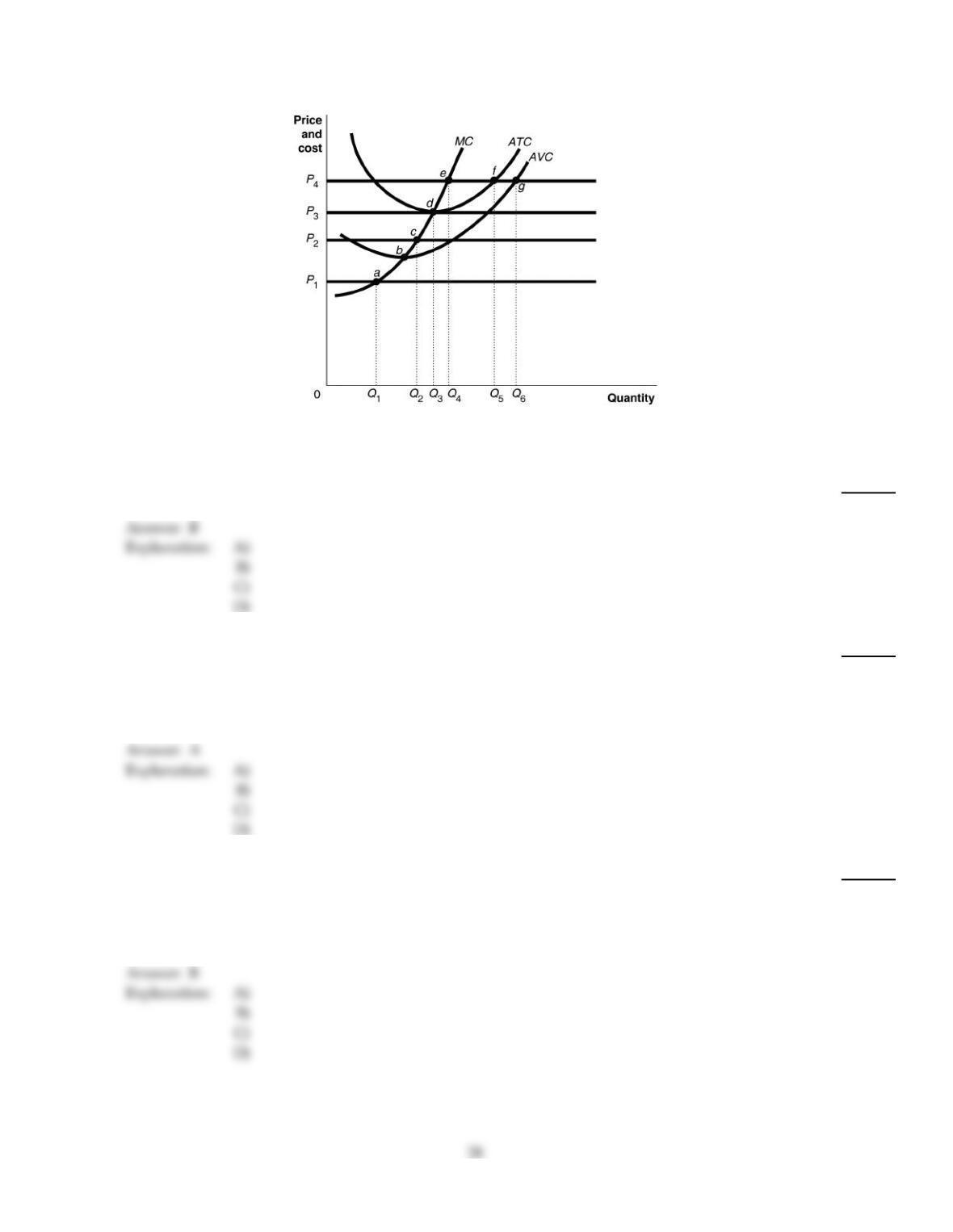

Figure 8–6

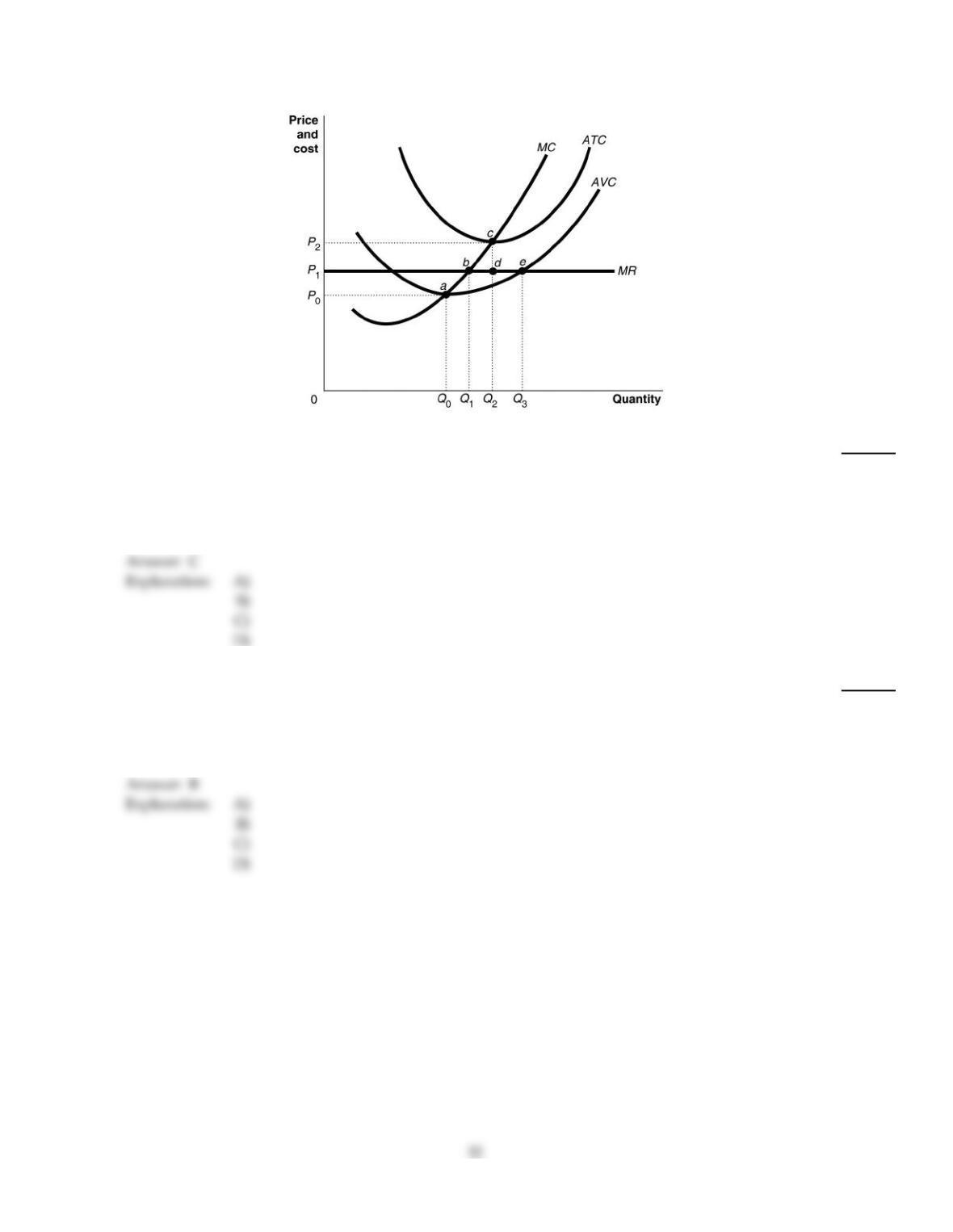

Figure 8–6 shows cost and demand curves facing a profit–maximizing perfectly competitive firm.

65)

Refer to Figure 8–6. Identify the shutdown point for the firm.

65)

A)

a

B)

b

C)

c

D)

d

66)

How are sunk costs and fixed costs related?

66)

A)

In the short run they are equal to each other.

B)

In the long run they are equal to each other.

C)

They are not related in any way.

D)

Sunk costs cannot be recovered and fixed costs can be avoided by shutting down.

Explanation:

67)

An industry’s long–run supply curve shows

67)

A)

how average productivity is changing.

B)

the relationship in the long run between market price and quantity supplied.

C)

how the government determines the price of the product.

D)

greater than normal profit.

Explanation:

Explanation:

68)

A constant–cost perfectly competitive market is in long–run equilibrium. At present, there are 1,000

firms each producing 400 units of output. The price of the good is $60. Now suppose there is a

sudden increase in demand for the industry’s product which causes the price of the good to rise to

$64. In the new long–run equilibrium, how will the average total cost of producing the good

compare to what it was before the price of the good rose?

68)

A)

The average total cost will be the same as it was before the price increase.

B)

The average total cost will be higher than it was before the price increase since the increase in

demand will drive up input prices.

C)

The average total cost will be lower than it was before the price increase because of economies

of scale.

D)

The average total cost will be higher than it was before the price increase because of

diseconomies of scale arising from the increased demand.

69)

Both individual buyers and sellers in perfect competition

69)

A)

can influence the market price by joining with a few of their competitors.

B)

have to take the market price as a given.

C)

can influence the market price by their own individual actions.

D)

have the market price dictated to them by government.

Table 8–1

Quantity Total Cost

(Dollars)

Variable Cost

(Dollars)

0$1,000 $0

100 1,360 360

200 1,560 560

300 1,960 960

400 2,760 1,760

500 4,000 3,000

600 5,800 4,800

Table 8–1 shows the short–run cost data of a perfectly competitive firm that produces plastic camera cases. Assume that

output can only be increased in batches of 100 units.

70)

Refer to Table 8–1. Assume that the price per unit is $8. If fixed cost then rises by $500 and the

price per unit is still $8, what happens to the firm’s profit maximizing output level?

70)

A)

This question cannot be answered without knowing the impact on marginal cost.

B)

It must rise to offset the increased cost.

C)

It will remain the same.

D)

It must fall.

Figure 8–5

Figure 8–5 shows cost and demand curves facing a typical firm in a perfectly competitive industry.

71)

Refer to Figure 8–5. The figure shows the cost structure of a firm in a perfectly competitive market.

If the firm’s fixed cost increases by $1,000 due to a new environmental regulation, what happens to

its profit maximizing output level?

71)

A)

It decreases.

B)

It remains the same.

C)

It increases.

D)

It could increase, decrease or remain constant, depending on whether the firm is able to cut

cost somewhere else.

Figure 8–12

72)

Refer to Figure 8–12. If the market price is P1, what is the allocatively efficient output level?

72)

A)

Q2

B)

Q0

C)

Q1

D)

There is no allocatively efficient output level because the firm is making a loss.

73)

Which of the following is not a characteristic of a monopolistically competitive market structure?

73)

A)

Firms sell differentiated products.

B)

Each firm must react to the actions of other firms.

C)

There are many firms.

D)

It is easy for new firms to entry the market.

Figure 8–6

Figure 8–6 shows cost and demand curves facing a profit–maximizing perfectly competitive firm.

74)

Refer to Figure 8–6. At price P3, the firm would produce

74)

A)

Q2 units

B)

Q5 units.

C)

Q3 units.

D)

Q4units.

Figure 8–5

Figure 8–5 shows cost and demand curves facing a typical firm in a perfectly competitive industry.

75)

Refer to Figure 8–5. What is the amount of the firm’s fixed cost?

75)

A)

$5,400

B)

$6,750

C)

$8,100

D)

It cannot be determined.

Figure 8–4

Figure 8–4 shows the cost and demand curves for a profit–maximizing firm in a perfectly competitive market.

76)

Refer to Figure 8–4. If the market price is $30 and the firm is producing output, what is the amount

of the firm’s profit or loss?

76)

A)

loss of $1,080

B)

profit of $1,300

C)

loss of $2,520

D)

profit of $1,440

77)

Perfect competition is characterized by all of the following except

77)

A)

heavy advertising by individual sellers.

B)

homogeneous products.

C)

firms have horizontal demand curves.

D)

sellers are price takers.

78)

Which of the following statements is correct?

78)

A)

Economic profit takes into account all costs involved in producing a product.

B)

Accounting profit is the same as economic profit.

C)

Economic profit always exceeds accounting profit.

D)

Accounting profit is not relevant in preparing a firm’s financial statement.

Table 8–1

Quantity Total Cost

(Dollars)

Variable Cost

(Dollars)

0$1,000 $0

100 1,360 360

200 1,560 560

300 1,960 960

400 2,760 1,760

500 4,000 3,000

600 5,800 4,800

Table 8–1 shows the short–run cost data of a perfectly competitive firm that produces plastic camera cases. Assume that

output can only be increased in batches of 100 units.

79)

Refer to Table 8–1. What is the fixed cost of production?

79)

A)

$500

B)

$0

C)

$1,000

D)

It cannot be determined.

80)

A perfectly competitive market is in long–run equilibrium. At present there are 100 identical firms

each producing 5,000 units of output. The prevailing market price is $20. Assume that each firm

faces increasing marginal cost. Now suppose there is a sudden increase in demand for the

industry’s product which causes the price of the good to rise to $24. Which of the following

describes the effect of this increase in demand on a typical firm in the industry?

80)

A)

In the short run the typical firm increases its output and makes an above normal profit.

B)

In the short run the typical firm increases its output but its total cost also rises. Hence, the

effect on the firm‘s profit cannot be determined without more information.

C)

In the short run the typical firm’s output remains the same but because of the higher price its

profit increases.

D)

In the short run the typical firm increases its output but its total cost also rises, resulting in no

change in profit.

81)

Val Alvarado, an accountant, quit his $80,000–a–year job and bought an existing laundry from its

previous owner. The lease on the laundry had five years remaining and required a monthly

payment of $4,000. The lease

81)

A)

is a fixed cost of operating the laundry.

B)

is part of the marginal cost of operating the laundry.

C)

is a variable cost of operating the laundry.

D)

is an implicit cost of operating the laundry.

82)

Refer to Figure 8–2. The firm breaks even at an output level of

82)

A)

Q4 units.

B)

Q2 units.

C)

Q3 units.

D)

Q1 units.