Exam

Name___________________________________

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

1)

What is productive efficiency?

1)

A)

A situation in which resources are allocated to their highest profit use.

B)

A situation in which firms produce as much as possible.

C)

A situation in which a good or service is produced at the lowest possible cost.

D)

A situation in which resources are allocated so that the last unit of output produced provides

a marginal benefit to consumers equal to the marginal cost of producing it.

2)

A perfectly competitive firm’s supply curve is its

2)

A)

marginal cost curve above its minimum average variable cost curve.

B)

marginal cost curve.

C)

marginal cost curve above its minimum average total cost curve.

D)

marginal cost curve above the minimum of its average fixed cost curve.

3)

A perfectly competitive firm in a constant–cost industry produces 1,000 units of a good at a total

cost of $50,000. The prevailing market price is $48. Assuming that this firm continues to produce

in the long run, what happens to output level in the long run?

3)

A)

The firm produces the same output level.

B)

The firm’s output increases.

C)

The firm’s output falls.

D)

There is insufficient information to answer the question.

4)

If, for the last unit of a good produced by a perfectly competitive firm, MR > MC then in producing

the last unit the firm

4)

A)

added more to total revenue than it added to total costs.

B)

added more to total costs than it added to total revenue.

C)

is maximizing marginal profit.

D)

has minimized its losses.

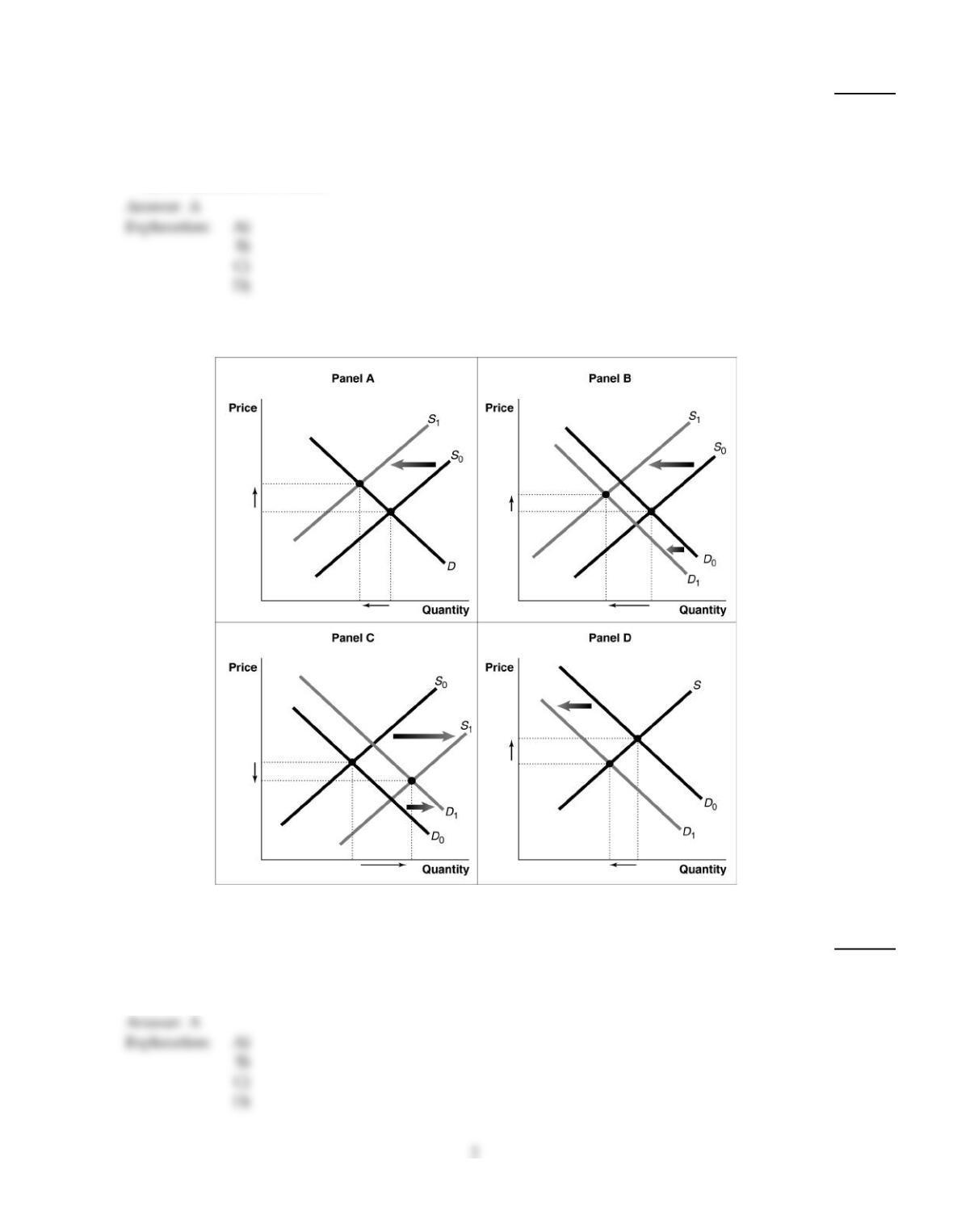

Figure 8–10

5)

Refer to Figure 8–10. Consider a typical firm in a perfectly competitive industry that is incurring

short run losses. Which of the diagrams in the Figure shows the effect on the industry as it

transitions to a long–run equilibrium?

5)

A)

Panel A

B)

Panel B

C)

Panel C

D)

Panel D

6)

Which of the following describes a situation in which a good or service is produced at the lowest

possible cost?

6)

A)

allocative efficiency

B)

profit maximization

C)

productive efficiency

D)

marginal efficiency

7)

A perfectly competitive firm produces 3,000 units of a good at a total cost of $36,000. The fixed cost

of production is $20,000. The price of each good is $10. Should the firm continue to produce in the

short run?

7)

A)

Yes, it should continue to produce because its price exceeds its average fixed cost.

B)

Yes, it should continue to produce because it is minimizing its loss.

C)

No, it should shut down because it is making a loss.

D)

There is insufficient information to answer the question.

Figure 8–6

Figure 8–6 shows cost and demand curves facing a profit–maximizing perfectly competitive firm.

8)

Refer to Figure 8–6. At price P2, the firm would

8)

A)

break even.

B)

lose an amount more than fixed costs.

C)

lose an amount less than its fixed costs.

D)

lose an amount equal to its fixed costs.

Table 8–1

Quantity Total Cost

(Dollars)

Variable Cost

(Dollars)

0$1,000 $0

100 1,360 360

200 1,560 560

300 1,960 960

400 2,760 1,760

500 4,000 3,000

600 5,800 4,800

Table 8–1 shows the short–run cost data of a perfectly competitive firm that produces plastic camera cases. Assume that

output can only be increased in batches of 100 units.

9)

Refer to Table 8–1. The firm will not produce in the short run if the output price falls below

9)

A)

$8.

B)

$4.

C)

$3.20.

D)

$2.80.

10)

According to Craig Johnson, president of retail consulting group Customer Growth Partners,

“Wal–Mart’s foray into organics should help to bring down prices for consumers.” Which of the

following statements supports Mr. Johnson’s argument?

Source: Parija Bhatnagar,”Wal–Mart’s Next Conquest: Organics” CNNMoney.com, May 1, 2006

10)

A)

Wal–Mart has a reputation for deliberately lowering prices to force its competitors out of the

market.

B)

Wal–Mart’s core customer base is the low–income consumer. Therefore, to compete for this

customer group organic food farmers will be compelled to lower prices.

C)

By expanding the organic market, Wal–Mart would bring in economies of scale that would,

when added to a competitive market, drive down prices.

D)

Wal–Mart is large enough that it can successfully pressure the U.S. Department of Agriculture

to force organic food farmers to lower their prices.

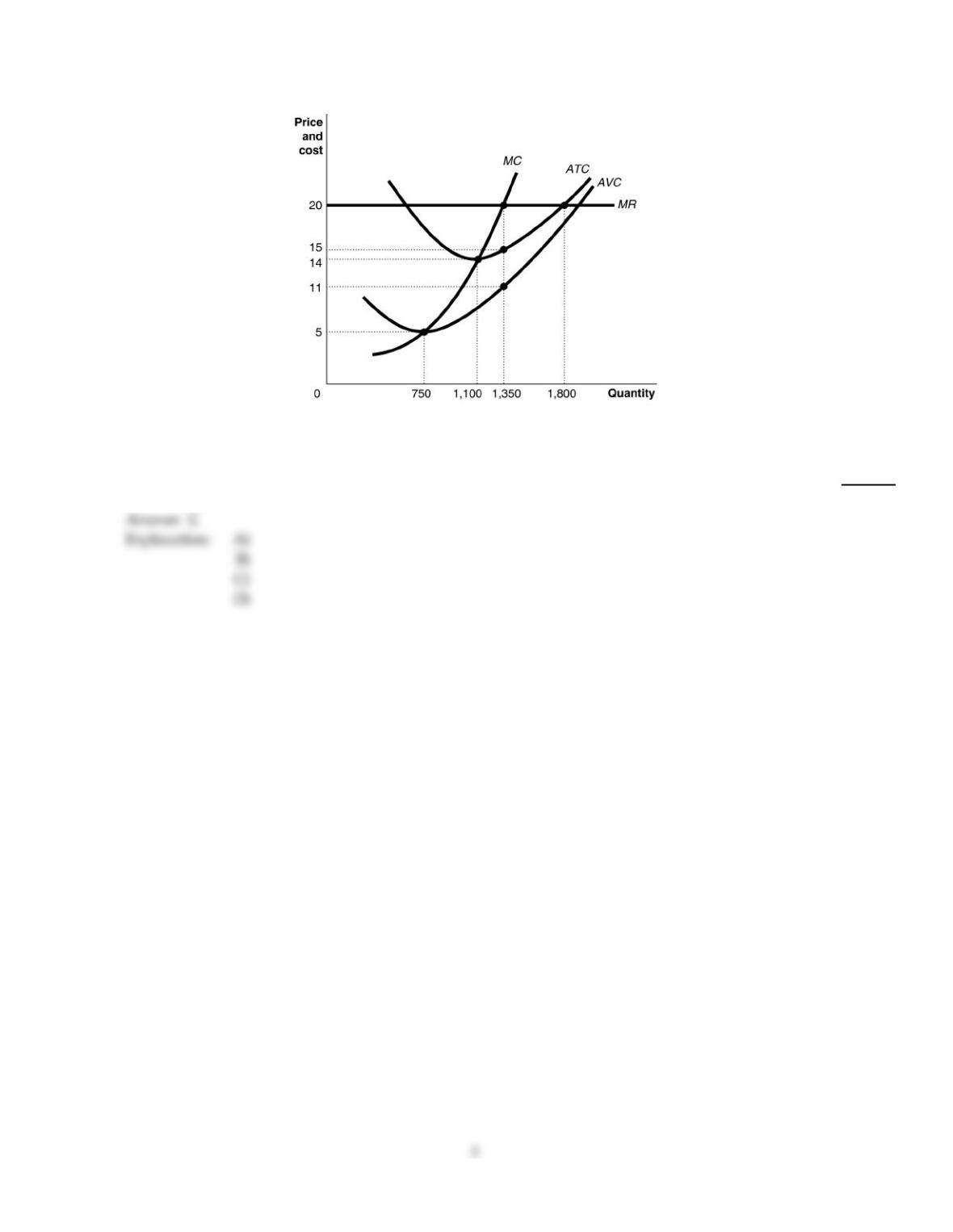

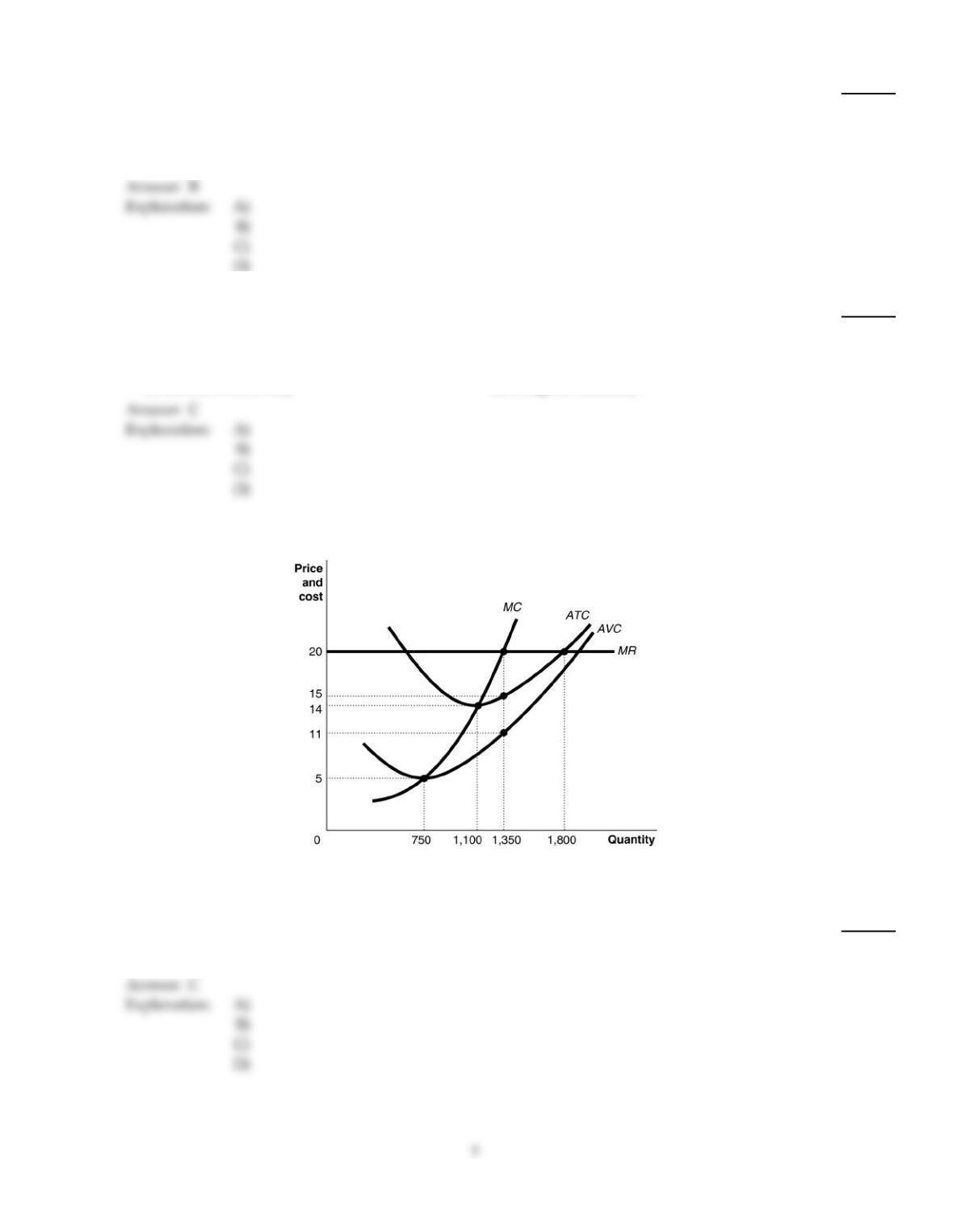

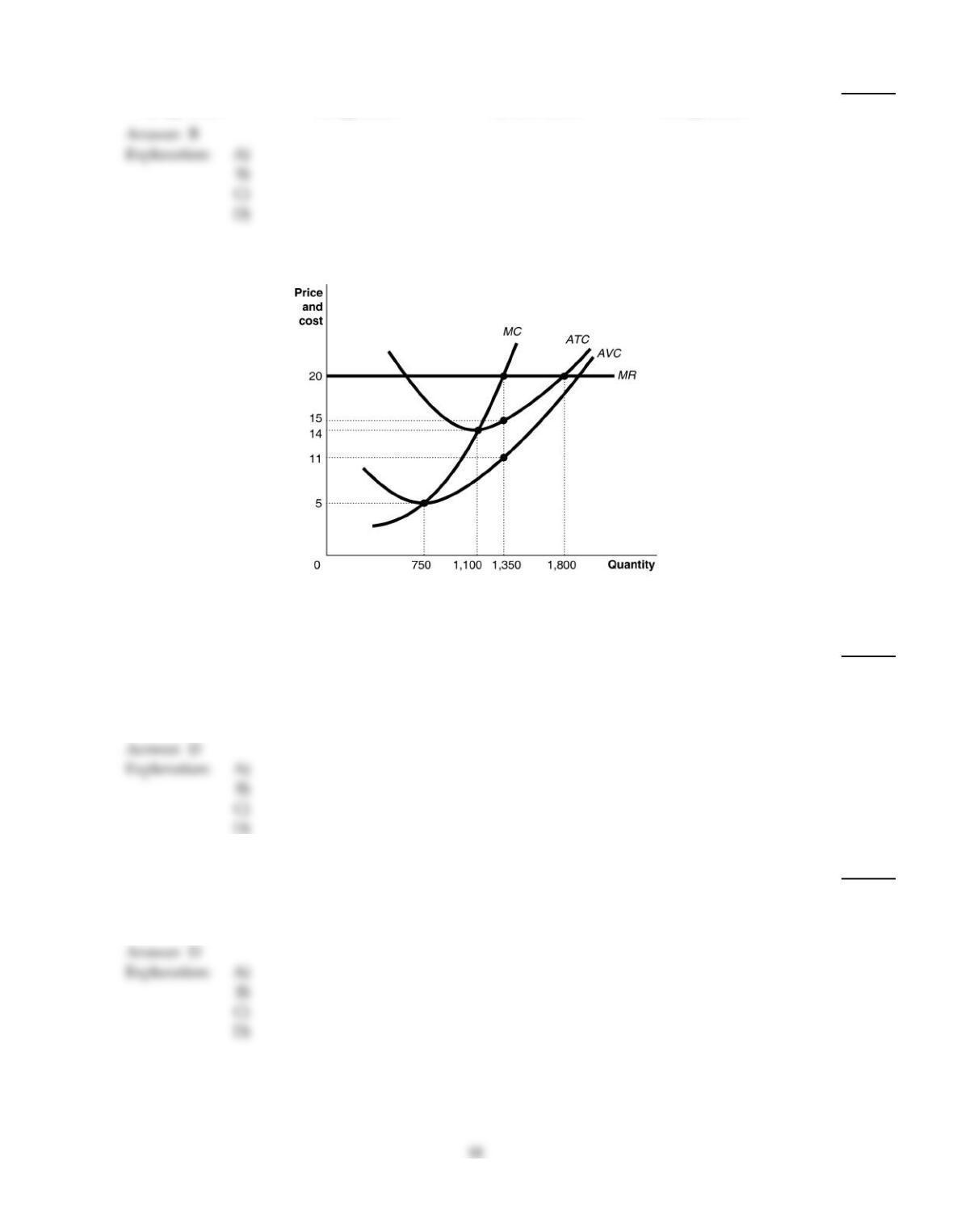

Figure 8–5

Figure 8–5 shows cost and demand curves facing a typical firm in a perfectly competitive industry.

11)

Refer to Figure 8–5. If the market price is $20, what is the firm’s profit maximizing output?

11)

A)

750 units

B)

1,100 units

C)

1,350 units

D)

1,800

Figure 8–1

12)

Refer to Figure 8–1. If the firm is producing 200 units,

12)

A)

it should cut back its output to maximize profit.

B)

it is making a loss.

C)

it should increase its output to maximize profit.

D)

it breaks even.

13)

How will an increase in the price of land for housing development affect apple growers who must

use land to produce apples?

13)

A)

It will raise the price of apples.

B)

It raises the opportunity cost of apple production.

C)

Apple growers will experience persistent losses if they do not sell their land to housing

developers.

D)

Apple growers will earn higher profit because their land is now more valuable.

14)

A very large number of small sellers who sell identical products implies

14)

A)

a multitude of vastly different selling prices.

B)

the inability of one seller to influence price.

C)

a downward–sloping demand for each seller’s product.

D)

chaos in the market.

15)

Which of the following describes a situation in which every good or service is produced up to the

point where the last unit provides a marginal benefit to consumers equal to the marginal cost of

producing it?

15)

A)

profit maximization

B)

productive efficiency

C)

allocative efficiency

D)

marginal efficiency

Figure 8–5

Figure 8–5 shows cost and demand curves facing a typical firm in a perfectly competitive industry.

16)

Refer to Figure 8–5. The firm’s manager suggests that the firm’s goal should be to maximize

average profit. If the firm does this, what is the amount of profit that it will earn?

16)

A)

$6,750

B)

$12,150

C)

$6,600

D)

$36,000

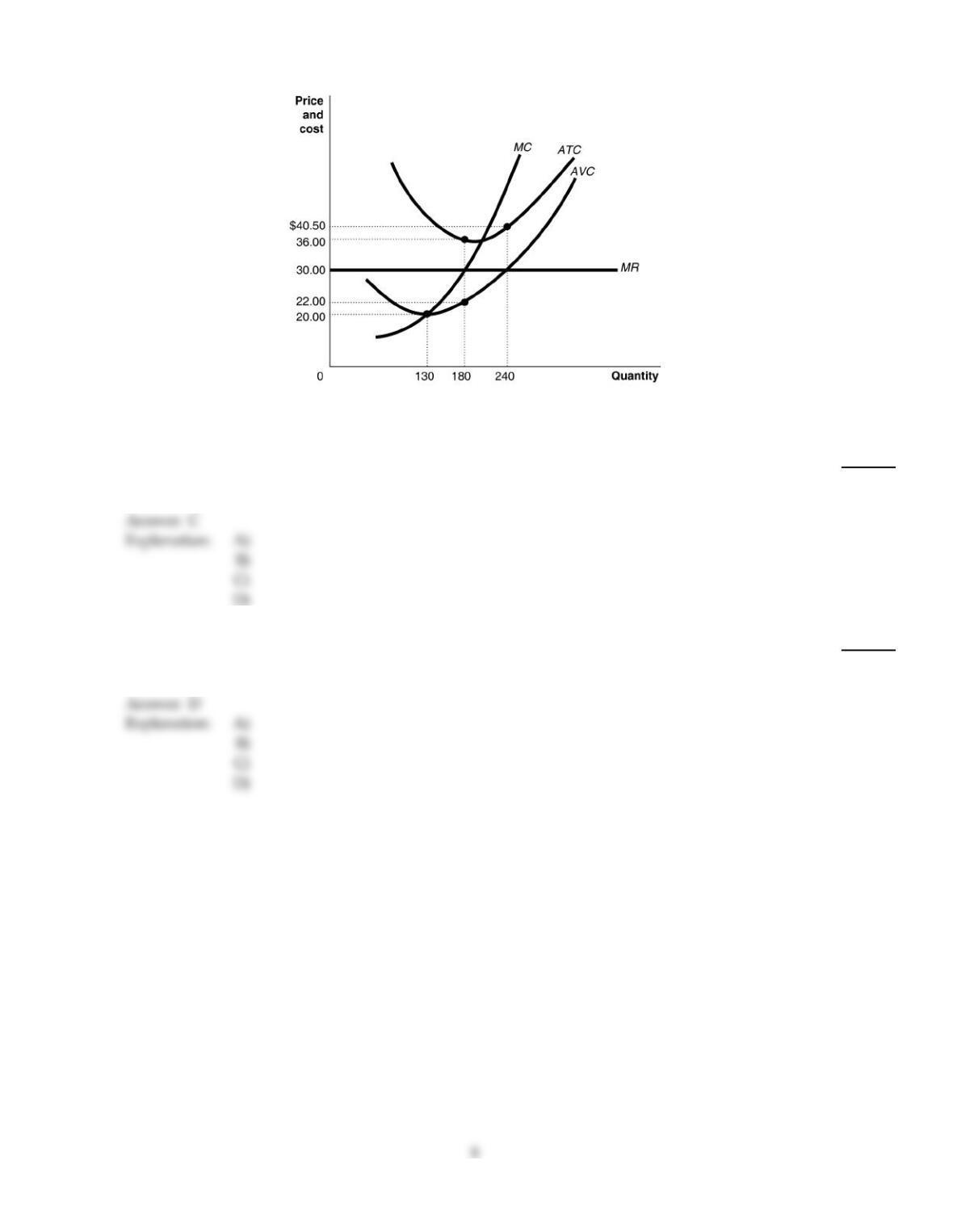

Figure 8–4

Figure 8–4 shows the cost and demand curves for a profit–maximizing firm in a perfectly competitive market.

17)

Refer to Figure 8–4. What is the amount of its total fixed cost?

17)

A)

$1,080

B)

$1,440

C)

$2,520

D)

It cannot be determined.

18)

Refer to Figure 8–4. If the market price is $30 and if the firm is producing output, what is the

amount of its total variable cost?

18)

A)

$7,200

B)

$6,480

C)

$5,400

D)

$3,960

Figure 8–6

Figure 8–6 shows cost and demand curves facing a profit–maximizing perfectly competitive firm.

19)

Refer to Figure 8–6. At price P4, the firm would produce

19)

A)

Q4 units.

B)

Q3 units.

C)

Q6 units.

D)

Q5units.

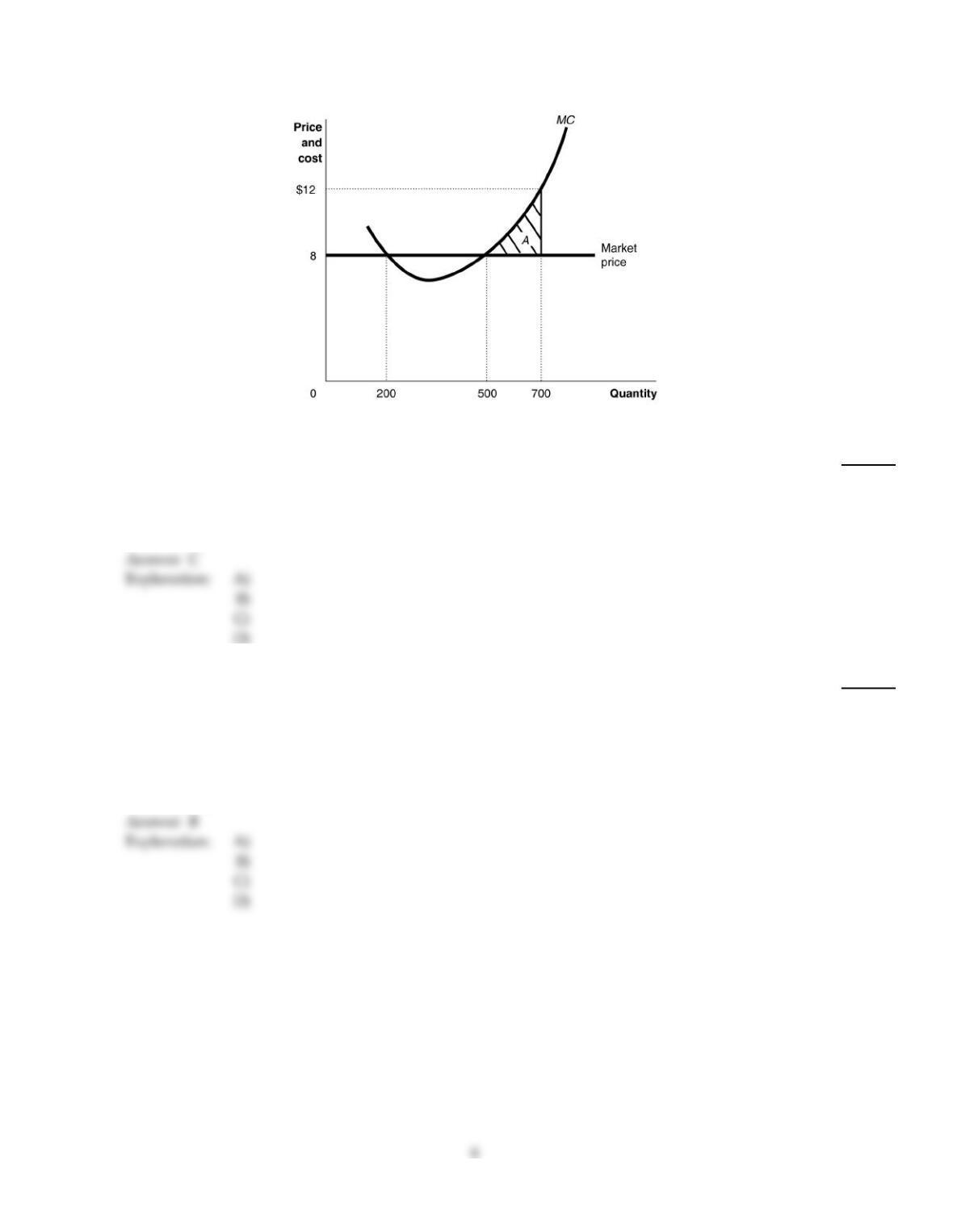

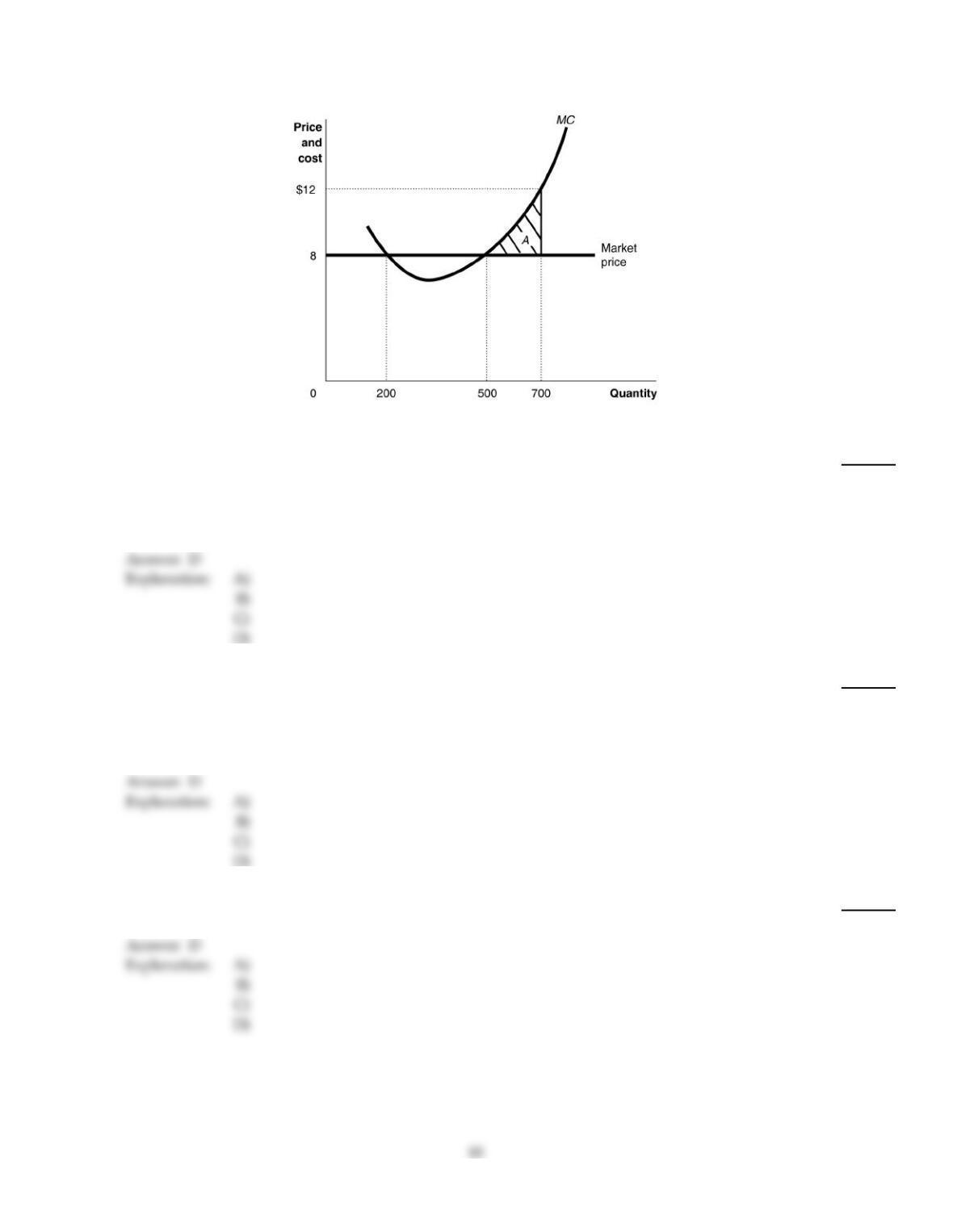

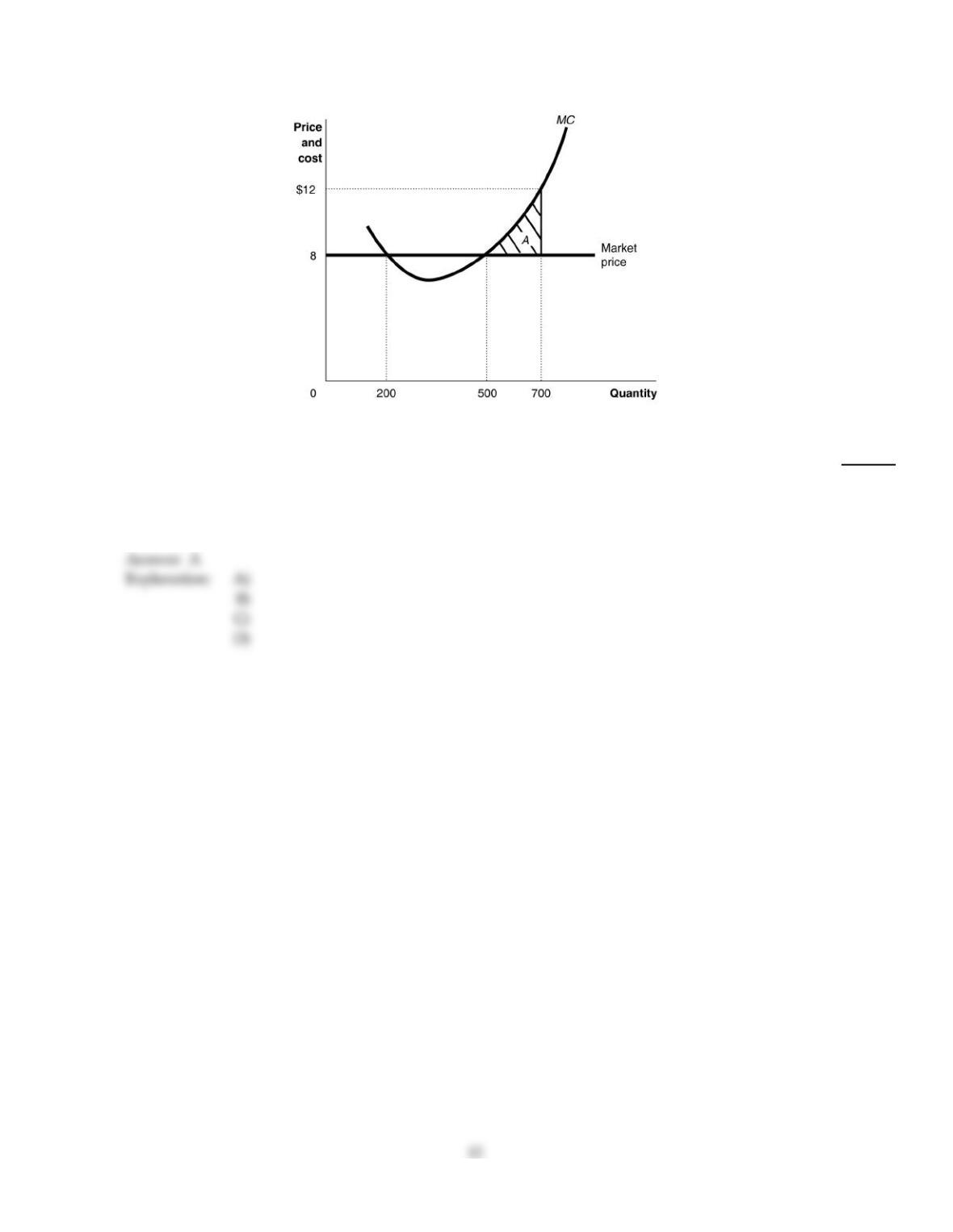

Figure 8–1

20)

Refer to Figure 8–1. If the firm is producing 700 units what is the amount of its profit or loss?

20)

A)

loss equivalent to the area A

B)

profit equivalent to the area A

C)

loss of $280

D)

There is insufficient information to answer the question.

21)

Which of the following is not a characteristic of a perfectly competitive market structure?

21)

A)

All firms sell identical products.

B)

There are a very large number of firms that are small compared to the market.

C)

There are no restrictions to entry by new firms.

D)

There are restrictions on the exit of firms.

Explanation:

22)

If the market price is $25 the average revenue if five units are sold is

22)

A)

$12.50.

B)

$5.

C)

$125.

D)

$25.

Explanation:

Explanation:

23)

Jason, a high–school student, mows lawns for families in his neighborhood. The going rate is $12

for each lawn–mowing service. Jason would like to charge $20 because he believes he has more

experience mowing lawns than the many other teenagers who also offer the same service. If the

market for lawn mowing services is perfectly competitive, what would happen if Jason raised his

price?

23)

A)

If Jason raises his price, then all others supplying the same service will also raise their prices.

B)

If Jason raises his price he will lose all of his customers.

C)

Initially, his customers might complain but over time they will come to accept the new rate.

D)

He would lose some but not all of his customers.

24)

If a typical firm in a perfectly competitive industry is earning profits, then

24)

A)

new firms will enter in the long run causing market supply to increase, market price to fall

and profits to decrease.

B)

all firms will continue to earn profits.

C)

new firms will enter in the long run causing market supply to decrease, market price to rise

and profits to increase.

D)

the number of firms in the industry will remain constant in the long run.

A

25)

Market supply is found by

25)

A)

horizontally summing each individual producer’s average total cost curve.

B)

vertically summing each individual producer’s average total cost curve.

C)

horizontally summing the relevant part of each individual producer’s marginal cost curve.

D)

vertically summing the relevant part of each individual producer’s marginal cost curve.

C

B

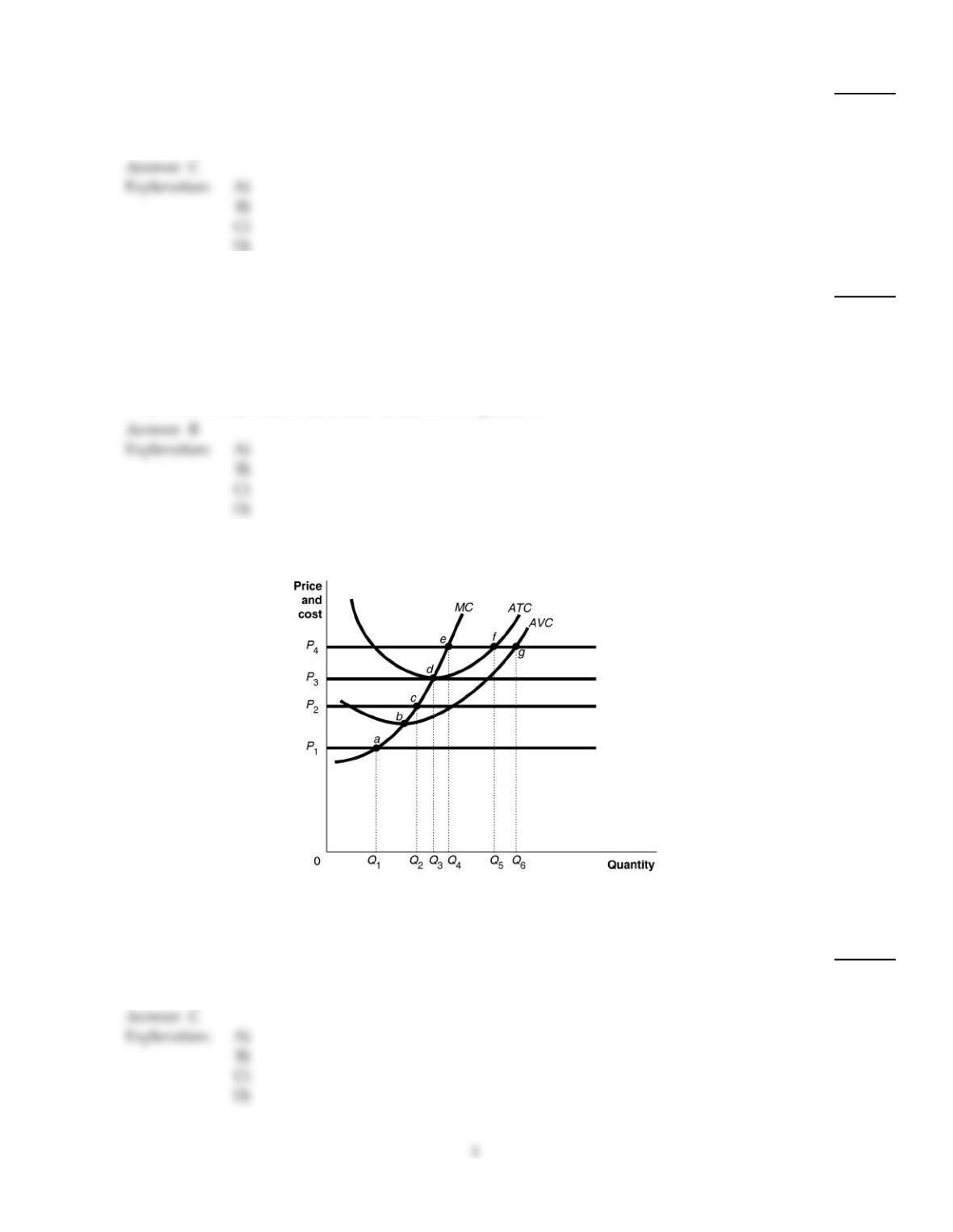

Figure 8–1

26)

Refer to Figure 8–1. If the firm is producing 700 units

26)

A)

it should cut back its output to maximize profit.

B)

it should increase its output to maximize profit.

C)

it is making a loss.

D)

it is making a profit.

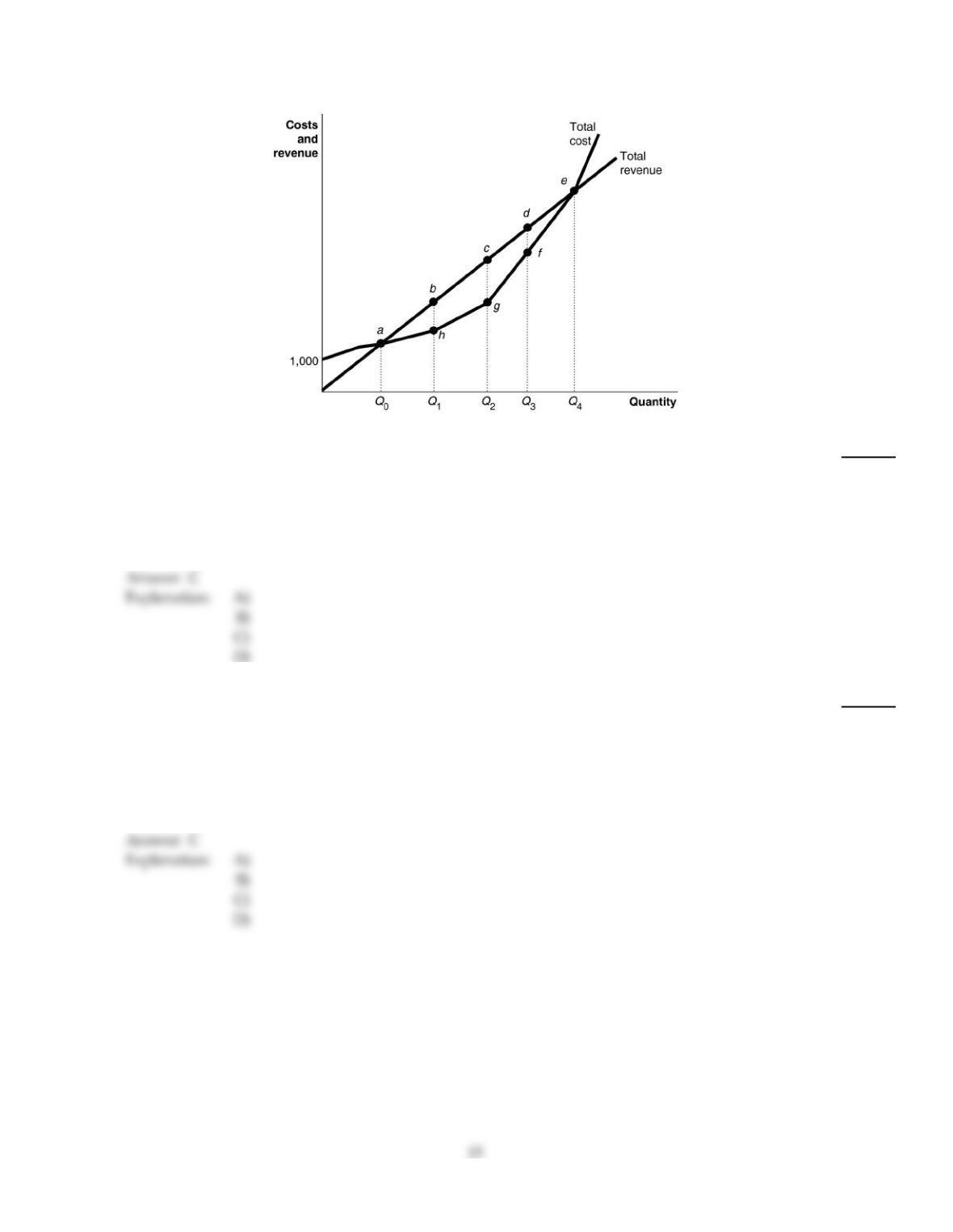

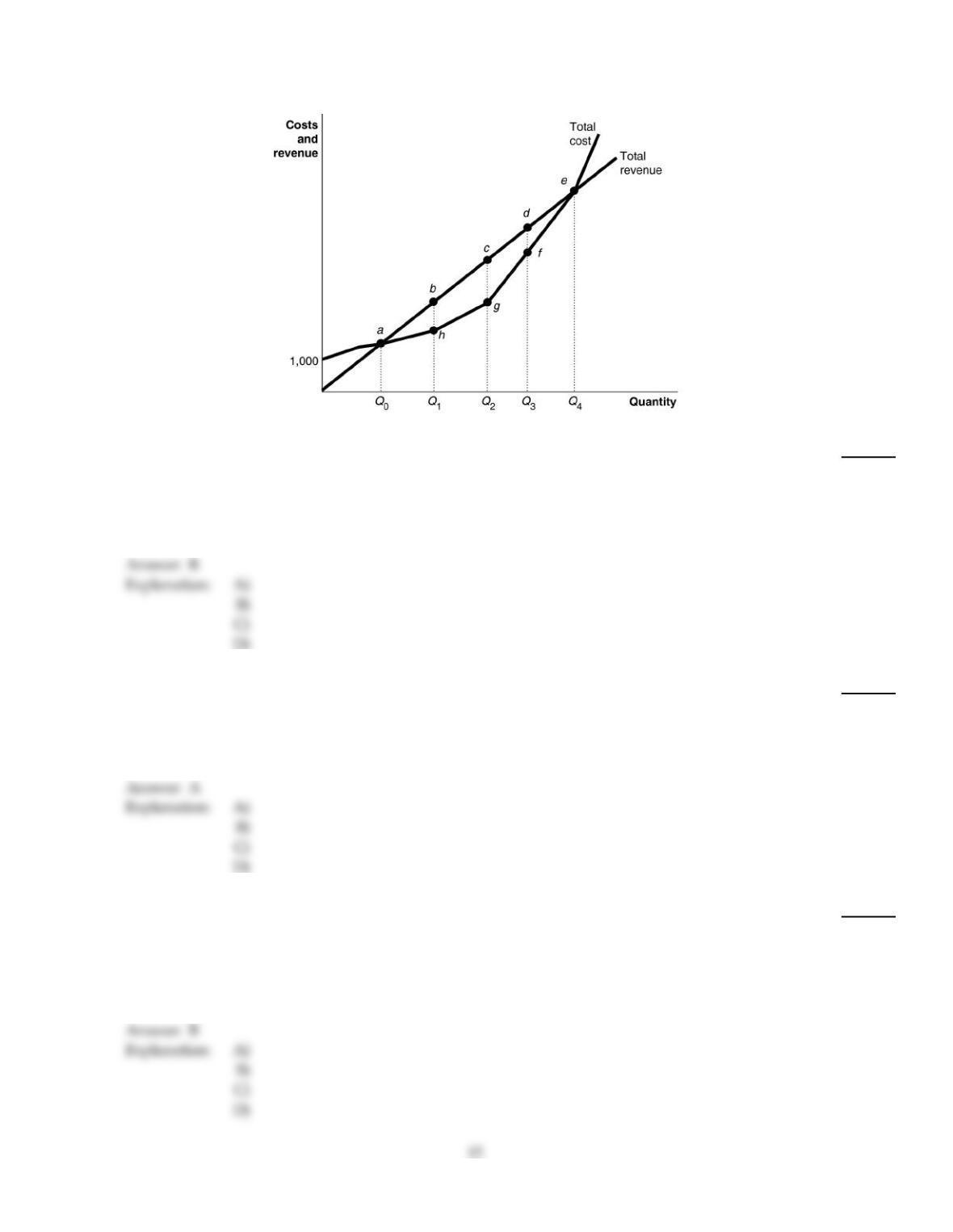

Figure 8–2

27)

Refer to Figure 8–2. Suppose the firm is currently producing Q2 units. What happens if it expands

output to Q3 units?

27)

A)

It incurs a loss.

B)

Its profit increases by the size of the vertical distance df.

C)

It makes less profit.

D)

It will be moving toward its profit–maximizing output.

28)

What is allocative efficiency?

28)

A)

It refers to a situation in which resources are allocated fairly to all consumers in a society.

B)

It refers to a situation in which resources are allocated such that goods can be produced at

their lowest possible cost.

C)

It refers to a situation in which resources are allocated so that the last unit of output produced

provides a marginal benefit to consumers equal to the marginal cost of producing it.

D)

It refers to a situation in which resources are allocated to their highest profit use.

29)

Which of the following is a characteristic of an oligopoly market structure?

29)

A)

It is easy for new firms to enter the industry.

B)

Each firm sells a unique product.

C)

Each firm need not react to the actions of rivals.

D)

There are a few firms.

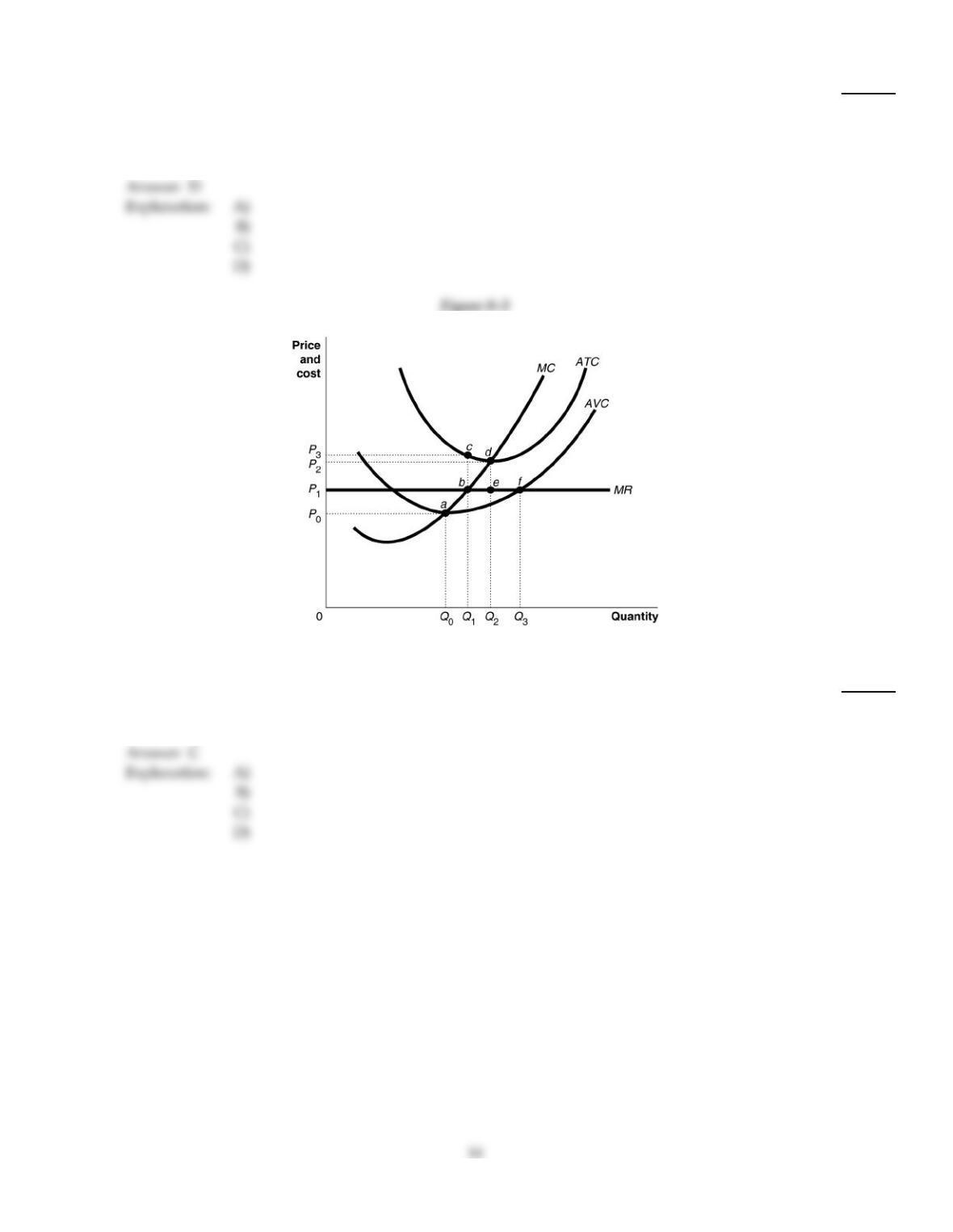

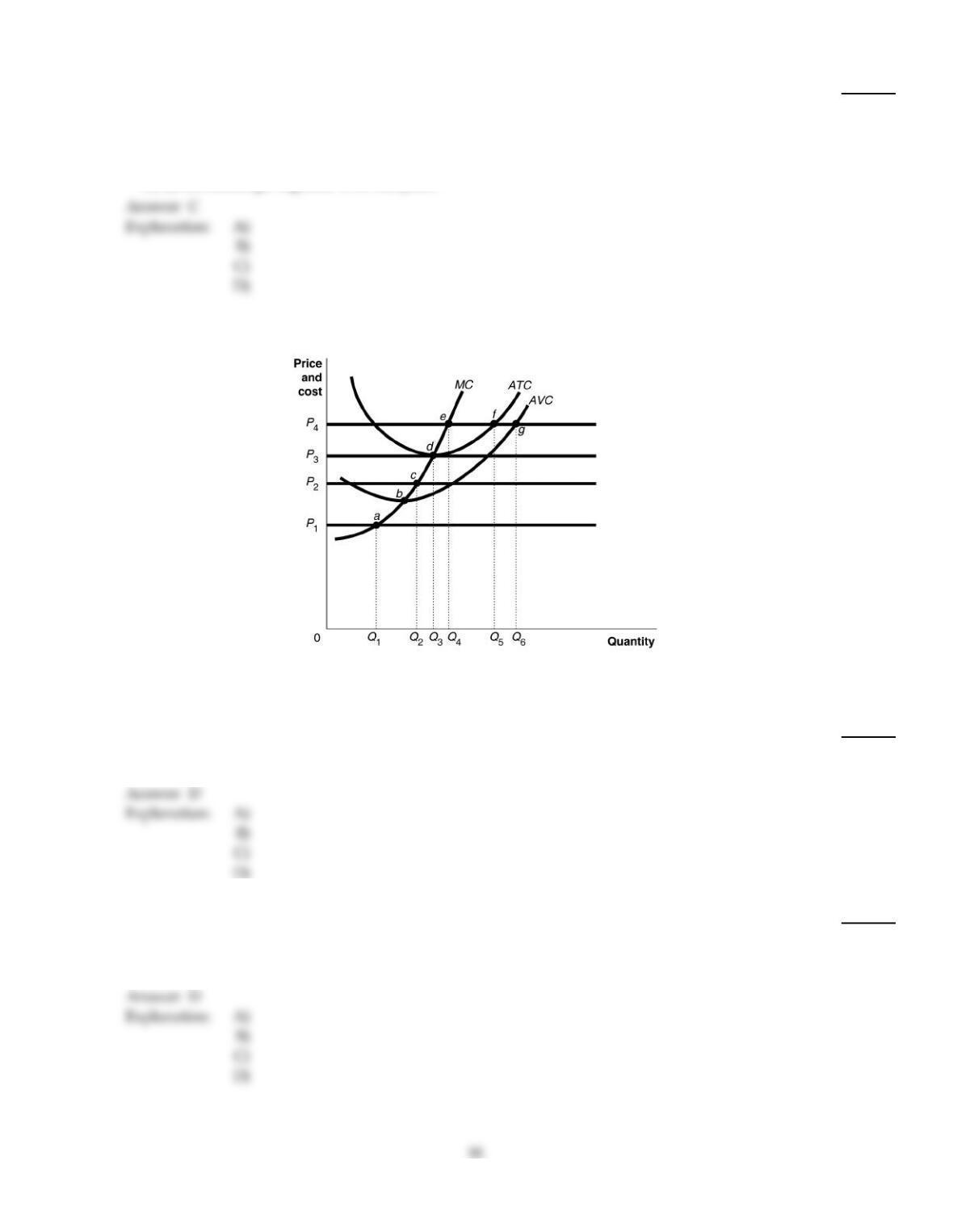

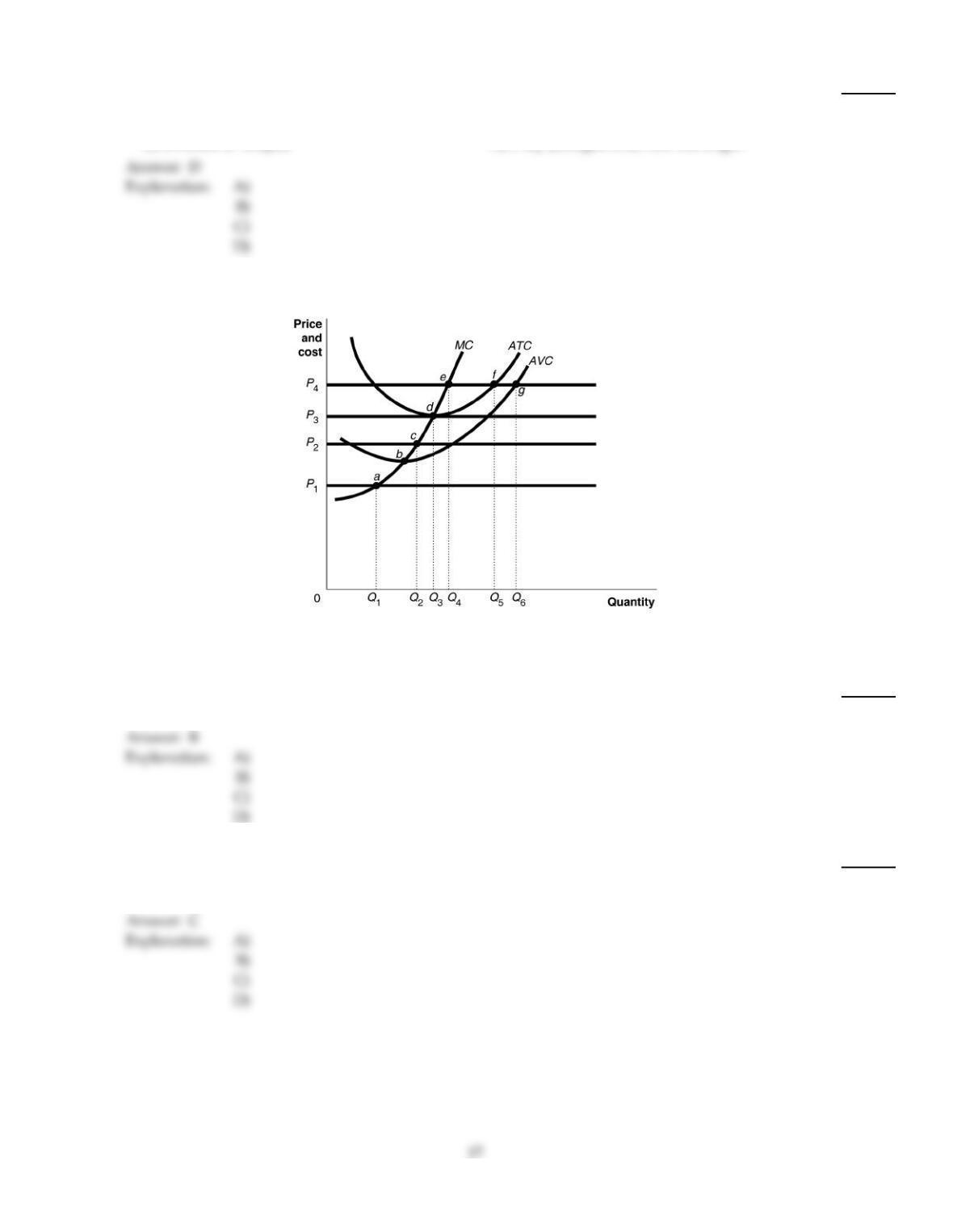

30)

Refer to Figure 8–3. Suppose the prevailing price is P1 and the firm is currently producing its

loss–minimizing quantity. Identify the area that represents the loss.

30)

A)

0P1 bQ1

B)

P2 deP1

C)

P3cbP1

D)

P3caP0

Figure 8–2

31)

Refer to Figure 8–2. What is the amount of profit if the firm produces Q2 units?

31)

A)

It is equal to the vertical distance g to Q2.

B)

It is equal to the vertical distance c to g.

C)

It is equal to the vertical distance c to Q2.

D)

It is equal to the vertical distance c to g multiplied by Q2units.

32)

Assume that the tuna fishing industry is perfectly competitive. Which of the following best

characterizes the industry if, as demand for tuna increases, fishing boats have to go farther into the

ocean to harvest tuna?

32)

A)

an increasing–cost industry

B)

a decreasing–cost industry

C)

a fixed–cost industry

D)

a constant–cost industry

33)

When a perfectly competitive firm finds that its market price is below its minimum average

variable cost, it will sell

33)

A)

any positive output the firm decides upon because all of it can be sold.

B)

nothing at all; the firm shuts down.

C)

the output level where marginal revenue equals marginal cost.

D)

the output where average total costs equal price.

34)

The demand for each seller’s product in perfect competition is horizontal at the market price

because

34)

A)

the price is set by the government.

B)

all consumers get together to set the price.

C)

each seller is too small to affect market price.

D)

all the sellers get together to set the price.

Figure 8–6

Figure 8–6 shows cost and demand curves facing a profit–maximizing perfectly competitive firm.

35)

Refer to Figure 8–6. At price P3, the firm would

35)

A)

lose an amount more than fixed costs.

B)

lose an amount less than fixed costs.

C)

lose an amount equal to its fixed costs.

D)

break even.

36)

If, as a perfectly competitive industry expands, it can supply larger quantities only at a higher

long–run equilibrium price, it is

36)

A)

a decreasing–cost industry.

B)

a constant–cost industry.

C)

a fixed–cost industry.

D)

an increasing–cost industry.

37)

In a graph with output on the horizontal axis and total revenue on the vertical axis, what is the

shape of the total revenue curve for a perfectly competitive firm?

37)

A)

a horizontal line

B)

U–shaped

C)

inverted U–shaped

D)

a ray (straight line) from the origin

Figure 8–6

Figure 8–6 shows cost and demand curves facing a profit–maximizing perfectly competitive firm.

38)

Refer to Figure 8–6. At price P1, the firm would produce

38)

A)

Q5units.

B)

zero units.

C)

Q1 units

D)

Q3 units.

B

39)

Refer to Figure 8–6. Identify the firm‘s short–run supply curve.

39)

A)

The marginal cost (MC) curve

B)

the marginal cost curve from a and above

C)

the marginal cost curve from b and above

D)

the marginal cost curve from d and above

C

D

40)

Refer to Figure 8–6. At price P2, the firm would produce

40)

A)

Q3 units.

B)

Q2 units.

C)

zero units.

D)

Q4units.

Figure 8–5

Figure 8–5 shows cost and demand curves facing a typical firm in a perfectly competitive industry.

41)

Refer to Figure 8–5. The firm’s manager suggests that the firm’s goal should be to maximize

average profit. In that case, what is the output level and what is the average profit that will achieve

the manger’s goal?

41)

A)

Q = 1,350 units, average profit =$9

B)

Q = 1,800 units, average profit =$20

C)

Q = 1,350 units, average profit =$5

D)

Q = 1,100 units, average profit =$6

42)

If, for a given output level, a perfectly competitive firm’s price is less than its average variable cost,

the firm

42)

A)

should increase output.

B)

is earning a profit.

C)

should increase price.

D)

should shut down.

43)

If a firm shuts down in the short run,

43)

A)

its loss equals zero.

B)

its total revenue is not large enough to cover its fixed costs.

C)

is makes zero economic profit.

D)

its loss equals its fixed cost.

44)

Between 1997 and 2001, the movement from traditional methods to organic growing methods in the

apple market was prompted mainly by

44)

A)

environmental groups who aggressively disseminated information on organic farming.

B)

the U.S. Department of Agriculture.

C)

the rising number of consumers who demanded organic products.

D)

the U.S. Organic Producers Association.

45)

If a typical firm in a perfectly competitive industry is incurring losses then

45)

A)

some firms will enter in the long run causing market supply to increase and market price to

rise increasing profit for all firms.

B)

some firms will exit in the long run causing market supply to decrease and market price to

fall increasing losses for the remaining firms.

C)

some firms will exit in the long run causing market supply to decrease and market price to

rise increasing profits for the remaining firms.

D)

all firms will continue to lose money.

Table 8–1

Quantity Total Cost

(Dollars)

Variable Cost

(Dollars)

0$1,000 $0

100 1,360 360

200 1,560 560

300 1,960 960

400 2,760 1,760

500 4,000 3,000

600 5,800 4,800

Table 8–1 shows the short–run cost data of a perfectly competitive firm that produces plastic camera cases. Assume that

output can only be increased in batches of 100 units.

46)

Refer to Table 8–1. If the market price of each camera case is $8 and the firm maximizes profit,

what is the amount of the firm’s profit or loss?

46)

A)

$0 (it breaks even)

B)

loss of $1,000

C)

profit of $440

D)

loss of $440

47)

If, in a perfectly competitive industry, the market price facing a firm is above its average total cost

at the output where marginal revenue equals marginal cost, then

47)

A)

market supply will remain constant.

B)

new firms are attracted to the industry.

C)

firms are breaking even.

D)

existing firms will exit the industry.