Chapter 8: Sarbanes-Oxley, Internal Control, and Cash

116.

Which of the following would not be included with the cash and cash equivalents on the balance sheet?

a.

commercial paper

b.

short-term receivables

c.

certificates of deposit

d.

money market mutual funds

117.

Pilger Corporation has cash on hand at year-end of $201,000 and a negative cash flow from operations of $144,000.

What is the ratio of cash to monthly cash expenses?

a.

12.0 months

b.

7.2 months

c.

1.4 months

d.

16.8 months

118.

During the year, Tempo Inc. has monthly cash expenses of $115,000. On December 31, its cash balance is

$1,437,500. The ratio of cash to monthly cash expenses is

a. 8.0

b. 12.5

c. 87.5

d. 11.5

Chapter 8: Sarbanes-Oxley, Internal Control, and Cash

119.

Identify each of the following as relating to (a) the control environment, (b) risk assessment, or (c)

control

procedures.

1.

Mandatory vacations

2.

Personnel policies

3.

Report of outside consultants on future market changes

120.

List the objectives of internal control and give an example of how each is implemented.

Chapter 8: Sarbanes-Oxley, Internal Control, and Cash

121.

You began your new job as the accountant at Bolivar Industries during the month of December. During your

first

month, you found several interesting issues.

1)

While looking through the invoices, you found Invoices 213–242, 245–271, and 275–290. It appears that

invoices

243, 244, 272, 273, and 274 are missing.

2)

During the month, Clerk # 3 issued $250 in refunds as compared to Clerks #1, #2, and #4 who issued less than

$50 each.

3)

The daily cash receipts and bank deposits reconcile, except on Tuesdays during the month.

4)

Business is generally brisk during the holiday season, but two weeks before Christmas there was a

sudden

increase in slow payments.

REQUIRED:

Part A: What kind of warning signs could be associated with these issues?

Part B: What control could you put in place regarding cash refunds mentioned in Part A (2)?

Chapter 8: Sarbanes-Oxley, Internal Control, and Cash

122.

Two features of internal control are presented in the following sections. Each is followed by a list of four

irregularities that occurred in processing data. Identify the one irregularity from each list that would be

discovered

or prevented by the feature of internal control described.

(a)

The sum of the balances of the accounts in the customer’s ledger is compared at the end

of

each month with the balance of the accounts receivable account in the general ledger

by a

person who has no responsibility for maintaining either the general ledger or the

customer’s

ledger.

(1)

Five hours of services were rendered but the customer was only billed for four hours.

(2)

A cash receipt of $750 was recorded correctly in the accounts receivable controlling

account but was posted to the customer’s ledger as $75.

(3)

A bill for services rendered to Cole Co. was erroneously posted to the account of

Coleman Co. in the customer’s ledger.

(4)

No entry was made in the accounting records for services rendered to a customer.

(b)

Both cash and credit charges for services rendered are recorded on prenumbered invoices.

At the end of the day, all invoices are accounted for before the duplicate copies of the

invoices are routed to the accounting department for entry into the accounts and the cash is

sent to the cashier’s department for deposit.

(1)

Some charge customers complained that the monthly statements of account did

not

add all amounts correctly.

(2)

Some clerks used incorrect hourly rates in preparing invoices.

(3)

Some clerks destroyed duplicate copies of cash invoices and misappropriated the cash.

(4)

Some charge customers complained that the monthly statement of account did

not

indicate credits for payments made.

Chapter 8: Sarbanes-Oxley, Internal Control, and Cash

123.

List and define each of the five elements of internal control.

Chapter 8: Sarbanes-Oxley, Internal Control, and Cash

124.

The following procedures were recently implemented at the Health Station, Inc. For each procedure, indicate

whether the internal control over cash represents (1) a strength or (2) a weakness. If it is a weakness, please

explain why.

(a)

All mail is opened by the mail clerk, who forwards all cash remittances to the cashier. The cashier prepares

a

listing of the cash receipts and forwards a copy of the list to the accounts receivable clerk for recording in

the accounts.

(b)

The accounts payable clerk prepares a voucher for each disbursement. The voucher along with the supporting

documentation is forwarded to the treasurer’s office for approval.

(c) At the end of each day, all cash receipts are placed in the bank’s night depository.

(d) The bank reconciliation is prepared by the cashier, who works under the supervision of the treasurer.

Chapter 8: Sarbanes-Oxley, Internal Control, and Cash

125.

The following procedures were recently implemented at the Pampered Pets, Inc. For each procedure, indicate

whether the internal control over cash represents (1) a strength or (2) a weakness. If it is a weakness, please

explain why.

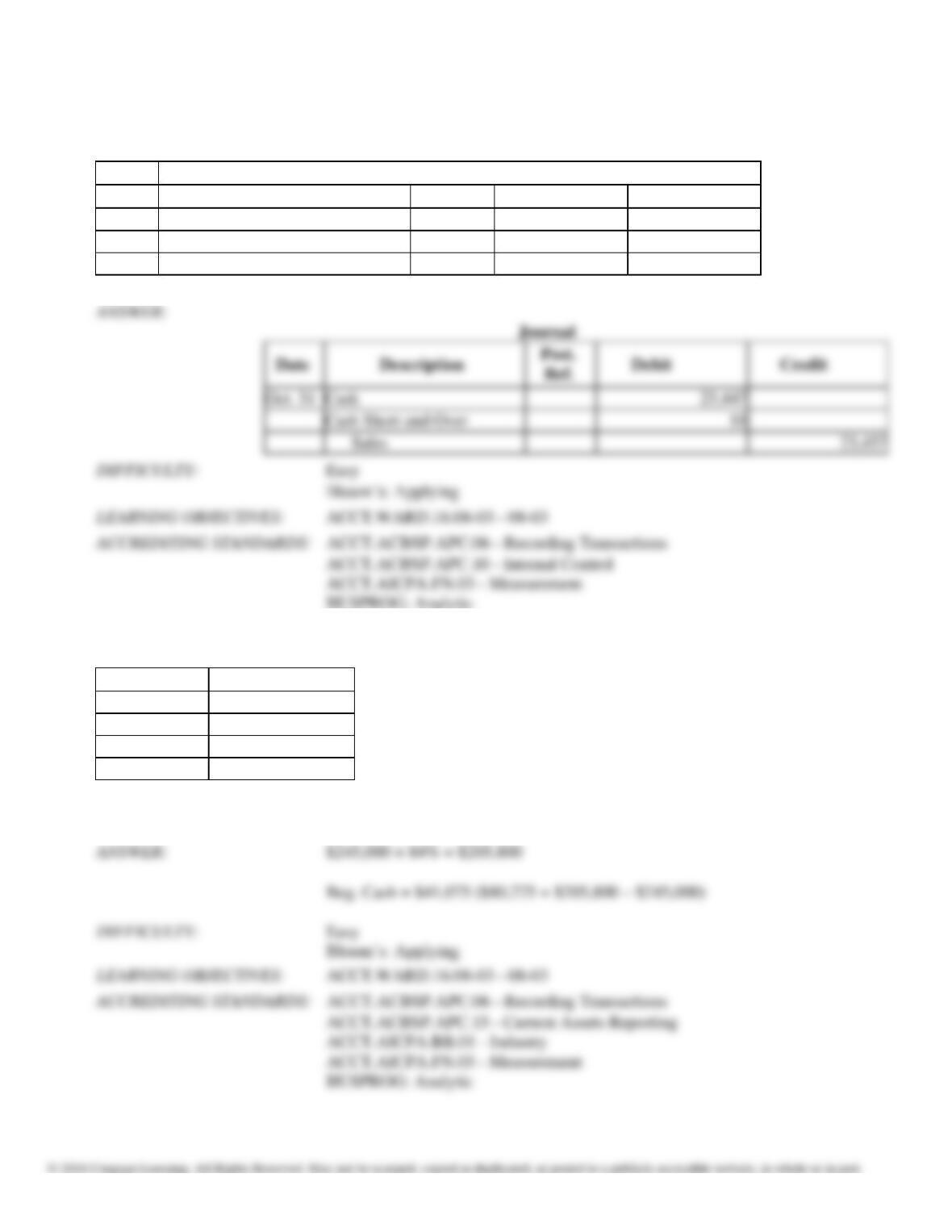

(a)

At the end of the day, cash register clerks are required to use their own funds to make up any cash shortages

in their registers.

(b)

At the end of the day, an accounting clerk compares the duplicate copy of the daily cash deposit slip with

the

deposit receipt obtained from the bank.

(c)

After necessary approvals have been obtained for the payment of a voucher, the treasurer signs and mails the

check. The treasurer then stamps the voucher and supporting documentation as paid and returns the voucher

and supporting documentation to the accounts payable clerk for filing.

(d)

Along with the petty cash receipts for postage, office supplies, etc., several postdated

employee

checks are in the petty cash fund.

Chapter 8: Sarbanes-Oxley, Internal Control, and Cash

126.

The following selected transactions relate to cash collections for a firm that maintains a $100 change fund at

all

times. Present entries to record the transactions for each of the two days of cash receipts from sales.

(a)

Actual cash in cash register, $5,412.36; cash receipts per cash register tally, $5,413.07.

(b)

Actual cash in cash register, $3,712.95; cash receipts per cash register tally, $3,712.16.

127.

The actual cash received during the week ended June 6 for cash sales was $8,276 and the amount indicated by the

cash register total was $8,262. Journalize the entry to record the cash receipts and cash sales.

Journal

Date

Description

Post. Ref.

Debit

Credit

Chapter 8: Sarbanes-Oxley, Internal Control, and Cash

128.

The actual cash received during the week ended October 31 for cash sales was $23,447 and the amount indicated

by the cash register total was $23,457. Journalize the entry to record the cash receipts and cash sales.

Journal

Date

Description

Post. Ref.

Debit

Credit

129.

Consider the following information from the cash account. Assume cash payments were 84% of collections.

Cash

??

Beg. balance

$245,000

Collections

??

Disbursements

$80,275

End balance

How much was the beginning balance of the cash account?

Chapter 8: Sarbanes-Oxley, Internal Control, and Cash

130.

Describe the features of a voucher system and list typical supporting documents for a voucher.

131.

The actual cash received during the week ended June 7 for cash sales was $18,632, and the amount indicated by

the cash register total was $18,628. Journalize the entry to record the cash receipts and cash sales.

Journal

Date

Description

Post.

Ref.

Debit

Credit

Post.

Ref.

Credit

Chapter 8: Sarbanes-Oxley, Internal Control, and Cash

132.

Consider the following journal entry made by Jones Company for one day‘s sales of a single cashier. Upon

investigation, what might you find happened to create this amount of Cash Over/Short account difference?

Give

three possible reasons for this difference.

Cash 2,235.00

Cash Short and Over 100.00

Sales 2,135.00

133.

List the principal advantages of electronic funds transfers.

Chapter 8: Sarbanes-Oxley, Internal Control, and Cash

134.

You are trying to explain debit and credit memos that appear on bank statements and whether these will increase or

decrease your company’s bank account balance. Complete the following table to help your new staff understand.

ITEM

Debit

or

Credit

Memo

Increases or

Decreases the

Company’s Bank

Account Balance

EFT payment

Bank correction of an error due to posting another

customer’s check to your account

Service charge

Note and interest collected for our company

NSF check

Bank correction of an error recording a $250

deposit

as $520

EFT deposit

Credit

Memo

EFT payment

Debit

Decrease

Service Charge

Debit

Decrease

Note and interest collected for our

NSF check

Debit

Decrease

Bank correction of an error recording a

EFT deposit

Credit

Increase

Chapter 8: Sarbanes-Oxley, Internal Control, and Cash

135.

The following items may appear on a bank statement:

1.

NSF check

2.

EFT deposit

3.

Service charge

4.

Bank correction of an error from recording a $300 check as $30.

Indicate whether the item would appear as debit or credit memo on the bank statement and whether the item would

increase or decrease the balance of your account. Use the following format:

Appears on the

Bank Statement as a Increases (Decreases) the

a Debit or Credit Balance of the Company’s

Item No.

Memo

Bank Account

Chapter 8: Sarbanes-Oxley, Internal Control, and Cash

136.

The following information is from Madison Corporation’s accounting records for May. Check #3269 was returned

as a double payment and voided. Checks that have not cleared the bank include #3252, #3260, and series #3275–

3278.

Check #

Amount

Check #

Amount

3247

$ 32.64

3263

$ 24.87

3248

400.00

3264

45.00

3249

309.22

3265

33.78

3250

256.00

3266

756.77

3251

3,212.17

3267

84.34

3252

56.89

3268

789.00

3253

98.02

3269

48.90

3254

47.55

3270

34.41

3255

1,124.77

3271

872.00

3256

250.00

3272

22.00

3257

68.00

3273

562.38

3258

215.56

3274

512.00

3259

38.55

3275

603.50

3260

92.65

3276

67.00

3261

44.61

3277

301.61

3262

72.96

3278

47.88

In addition to the above list of the checks, Madison had check #2264 for $32.98 and check #2655 for $45.99

outstanding previously that have not cleared.

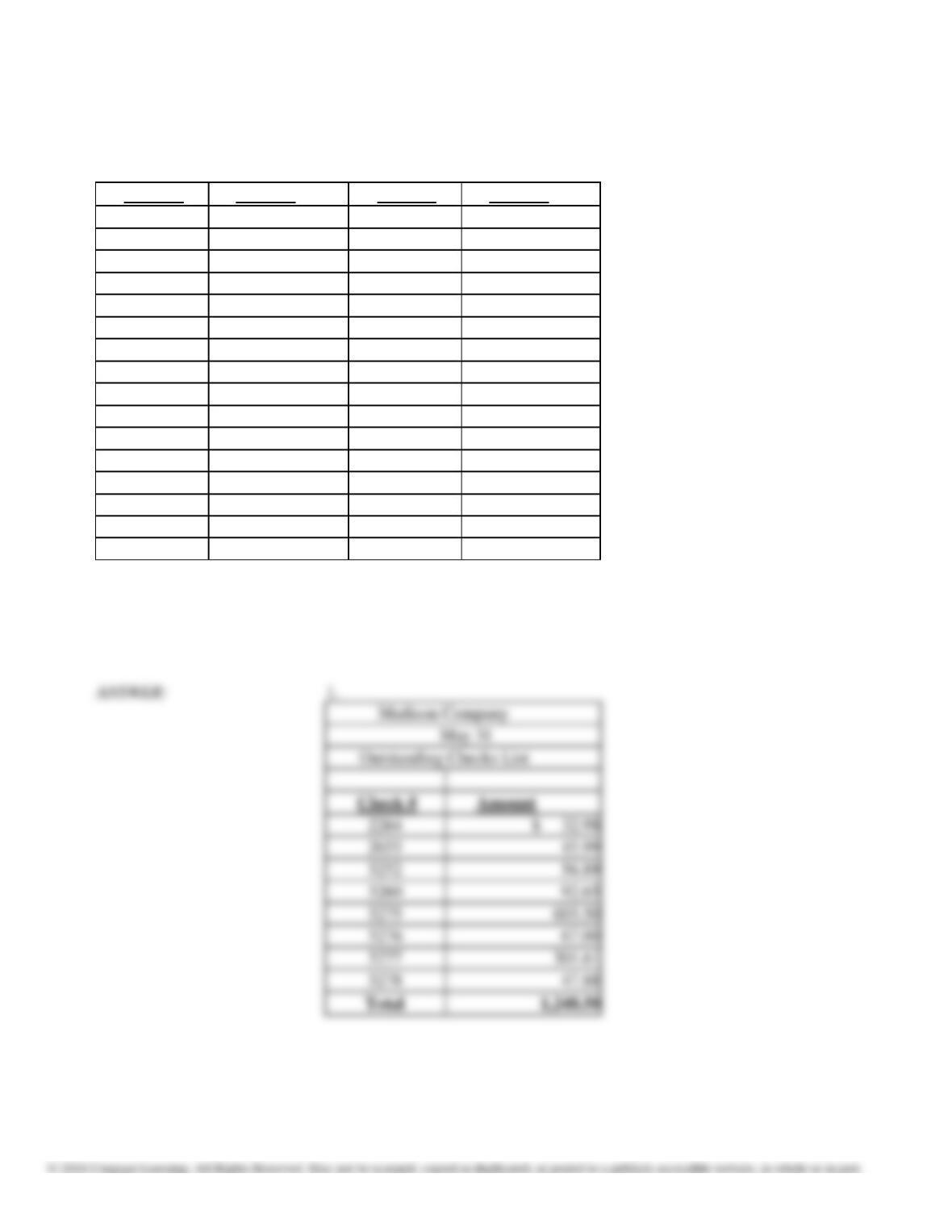

1.

Create an outstanding checks list for Madison at the end of May.

2.

What is the total amount of checks that cleared the bank (written in May)?

Chapter 8: Sarbanes-Oxley, Internal Control, and Cash

Chapter 8: Sarbanes-Oxley, Internal Control, and Cash

137.

The Scharf Company is a retailer located in a state without sales tax. The following data was given to you to

complete the transactions for the day’s sales to be recorded. All cash drawers start with $100 in change.

Reg. #1 Reg. #2 Reg. #3 Reg. #4

Cash in drawer 974.50 1,383.66 939.46 1,137.91

Sales reading 879.50 1,298.16 839.46 1,030.33

Difference

Record the journal entries for EACH cash register to determine the cashier’s accuracy.

Account

Debit

Credit

Chapter 8: Sarbanes-Oxley, Internal Control, and Cash

Chapter 8: Sarbanes-Oxley, Internal Control, and Cash

138.

Jackson Industries has collected the following information but needs assistance completing the table. The

cash

payments were 90% of collections.

Cash

??

Beg. balance

$511,770

Collections

??

Payments

$102,275

End balance

How much was the beginning balance of the cash account?

Cash

$511,770

Collections

$102,275

End balance

Chapter 8: Sarbanes-Oxley, Internal Control, and Cash

139.

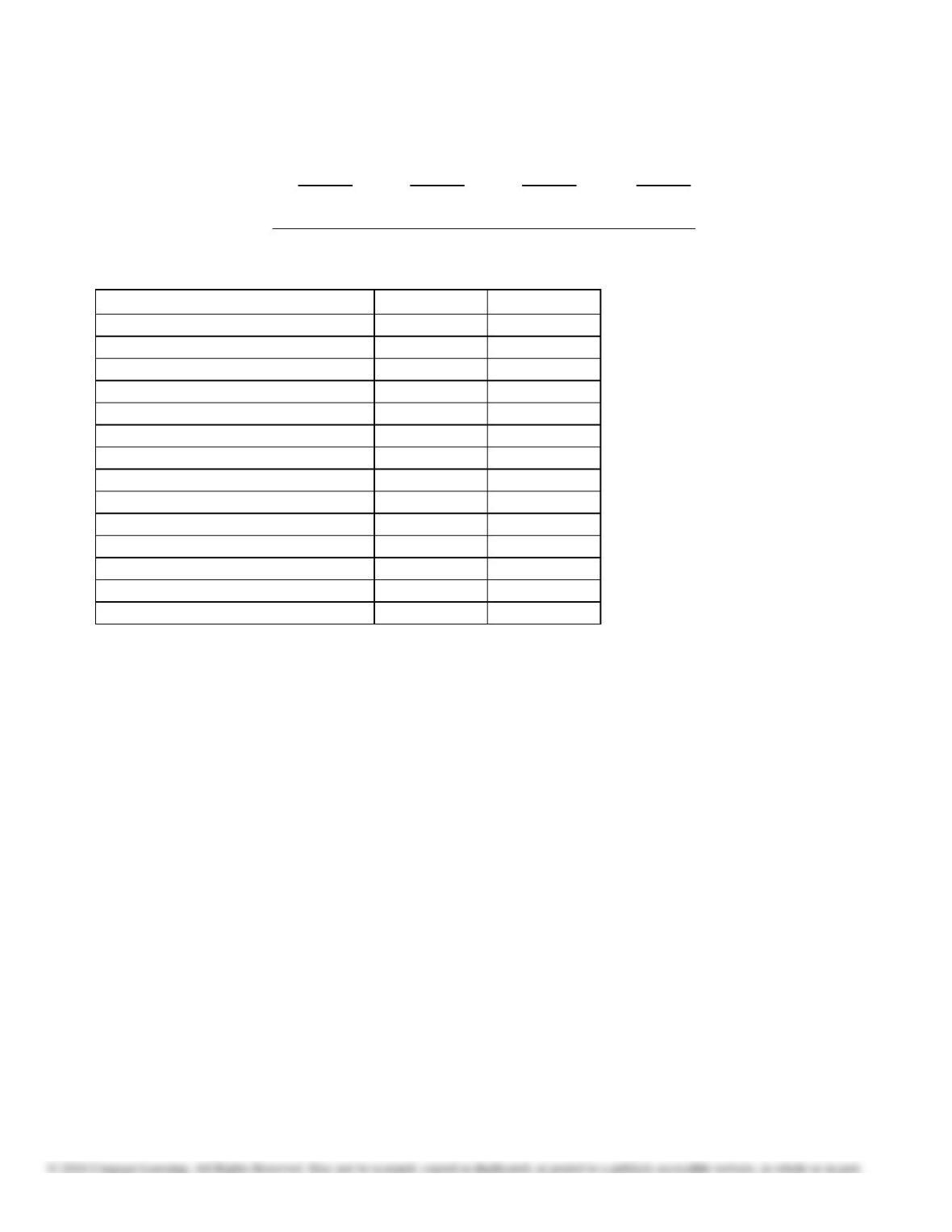

Identify each of the following reconciling items as (a) an addition to the cash balance according to the bank

statement, (b) deduction from the cash balance according to the bank statement, (c) an addition to the cash balance

according to the company’s records, or (d) a deduction from the cash balance according to the company’s records.

Assume that none of the transactions reported by bank debit and credit memos have been recorded by the

company. Also, indicate by writing “entry” by those items that will require a journal entry in the company’s

accounts.

1.

Deposits in transit.

2.

Bank service charges.

3.

NSF check.

4.

Outstanding checks.

5.

Check for $690 incorrectly recorded by the company as $960.

6.

Check for $420 incorrectly recorded by the company as $240.

ANSWER:

Chapter 8: Sarbanes-Oxley, Internal Control, and Cash

140.

Using the following information, prepare a bank reconciliation for Miller Co. for August 31:

(a)

The bank statement balance is $4,690

(b)

The cash account balance is $5,080.

(c)

Outstanding checks amounted to $715.

(d)

Deposits in transit are $1,020.

(e)

The bank service charge is $40.

(f)

A check for $72 for supplies was recorded as $27 in the ledger.