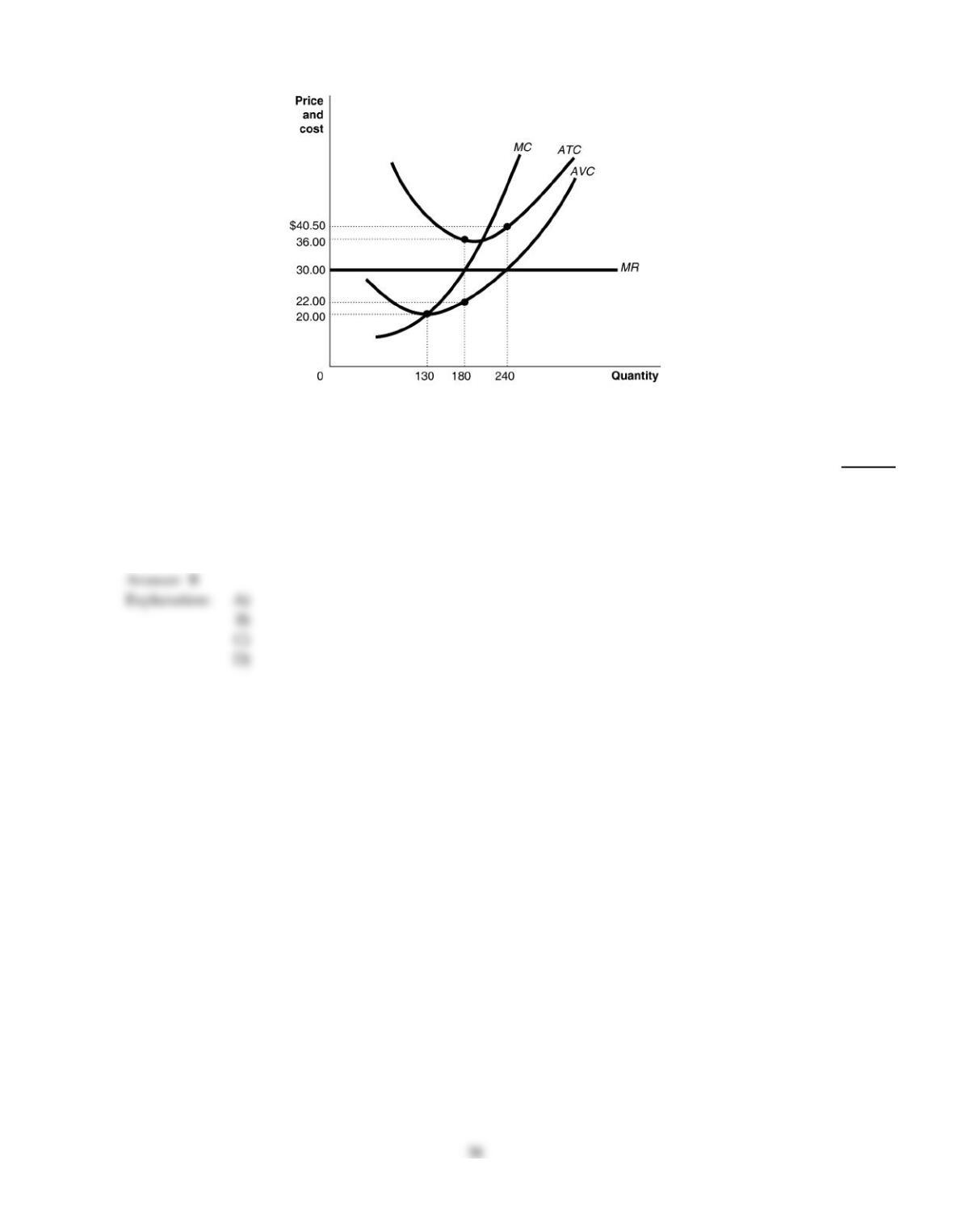

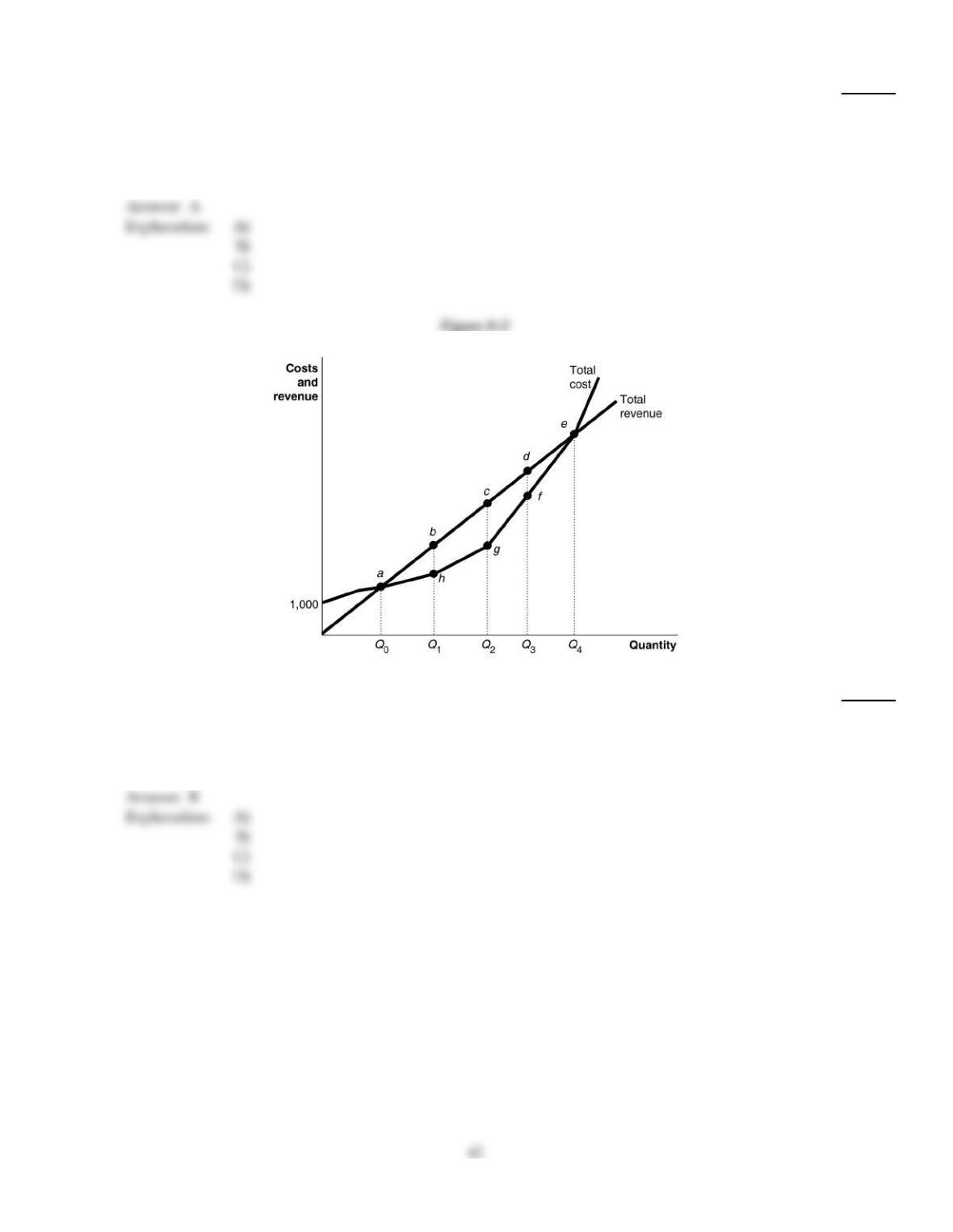

Figure 8–4

Figure 8–4 shows the cost and demand curves for a profit–maximizing firm in a perfectly competitive market.

83)

Refer to Figure 8–4. If the market price is $30, should the firm represented in the diagram continue

to stay in business?

83)

A)

No, it should shut down because it is making a loss.

B)

Yes, because it is covering part of its fixed cost.

C)

No, it should shut down because it cannot cover its variable cost.

D)

Yes, because it is making a profit.

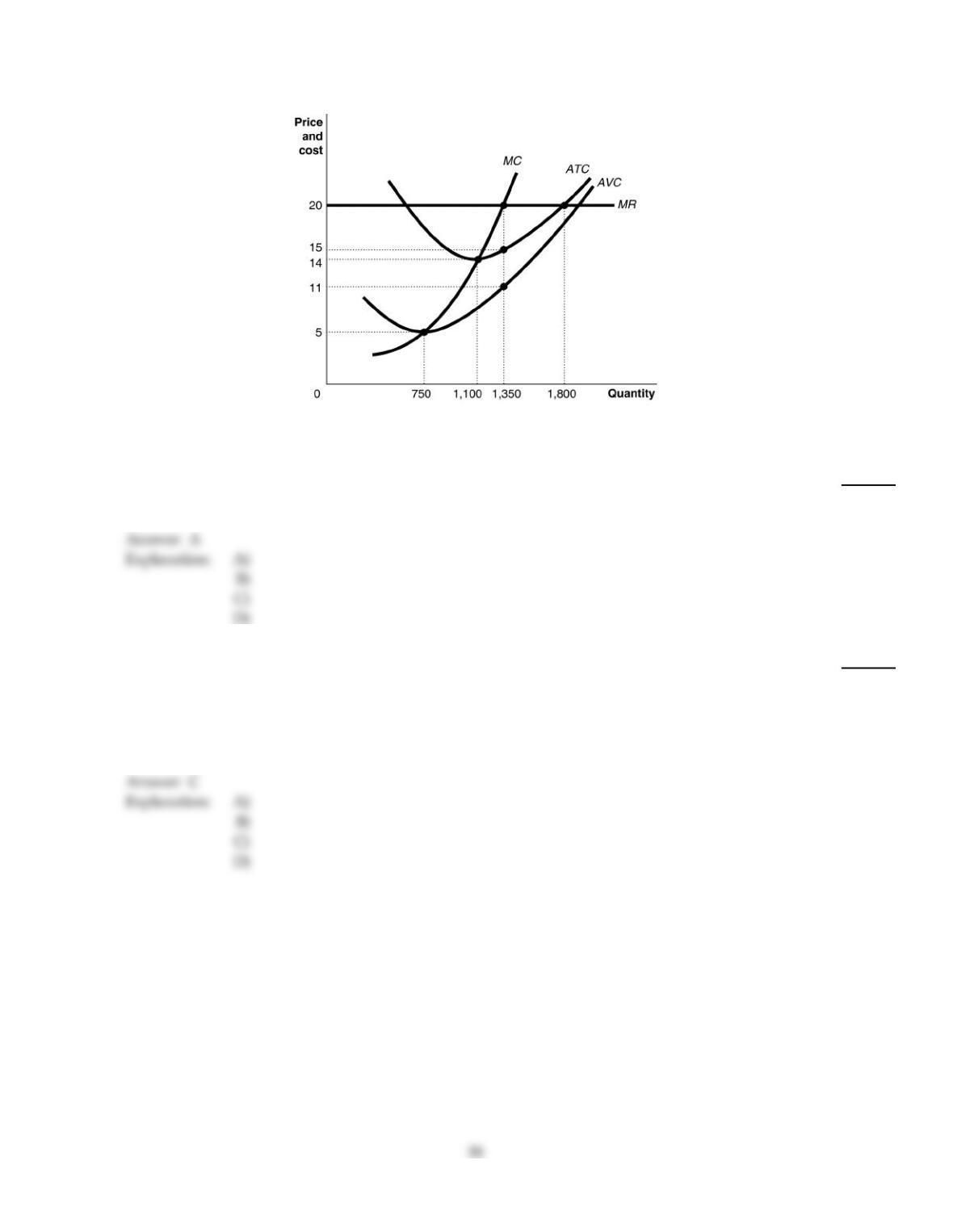

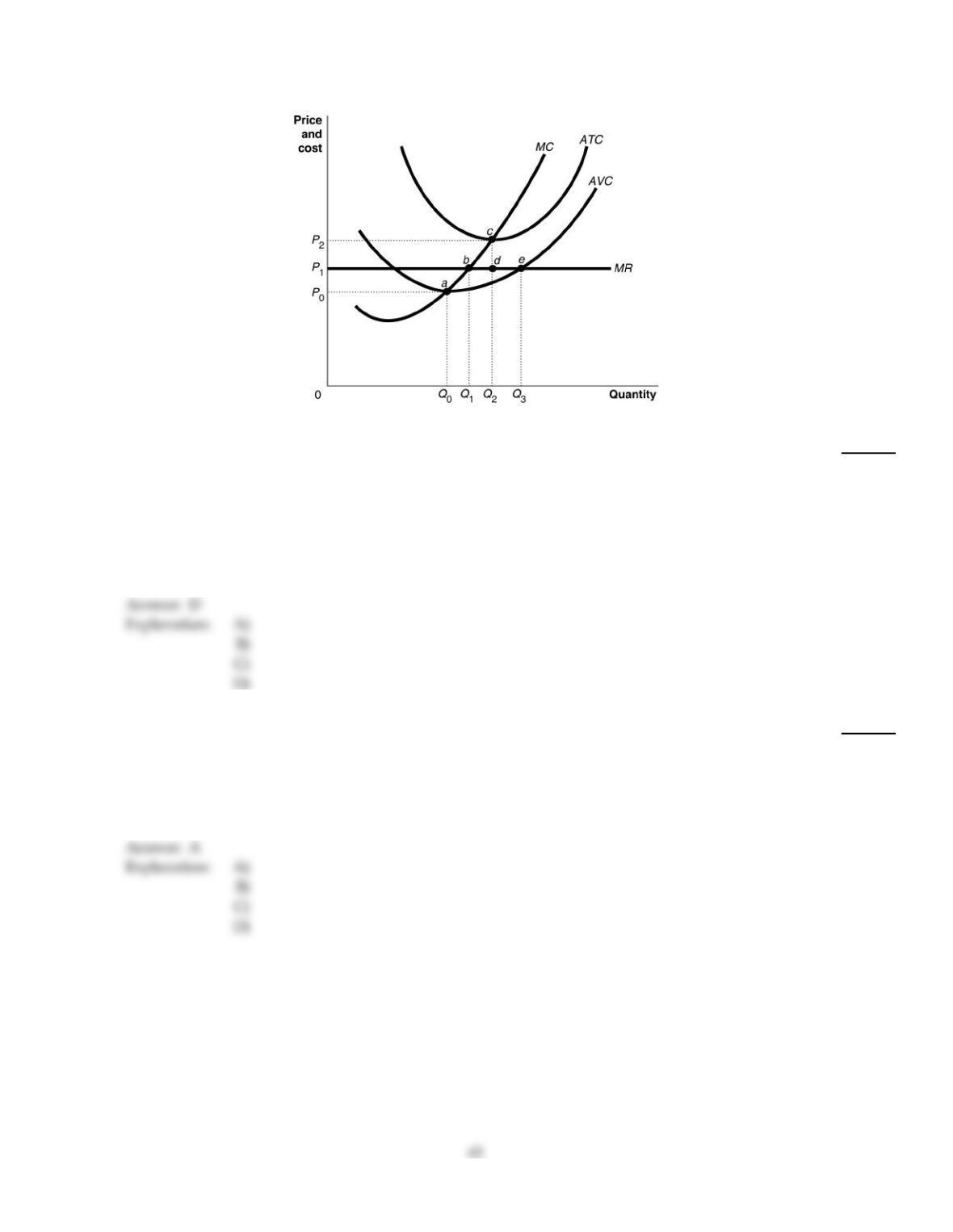

Figure 8–5

Figure 8–5 shows cost and demand curves facing a typical firm in a perfectly competitive industry.

84)

Refer to Figure 8–5. If the market price is $20, what is the average profit at the profit maximizing

quantity?

84)

A)

$5

B)

$6

C)

$9

D)

$20

85)

Both buyers and sellers are price takers in a perfectly competitive market because

85)

A)

each buyer and seller knows it is illegal to conspire to affect price.

B)

both buyers and sellers in a perfectly competitive market are concerned for the welfare of

others.

C)

each buyer and seller is too small relative to others to independently affect the market price.

D)

the price is determined by government intervention and dictated to buyers and sellers.

C

A

Figure 8–5

Figure 8–5 shows cost and demand curves facing a typical firm in a perfectly competitive industry.

86)

Refer to Figure 8–5. If the market price is $20, what is the amount of the firm’s profit?

86)

A)

$5,400

B)

$6,750

C)

$8,100

D)

$16,200

87)

An individual seller in perfect competition will not sell at a price lower than the market price

because

87)

A)

demand for the product will exceed supply.

B)

the seller can sell any quantity she wants at the prevailing market price.

C)

demand is perfectly inelastic.

D)

the seller would start a price war.

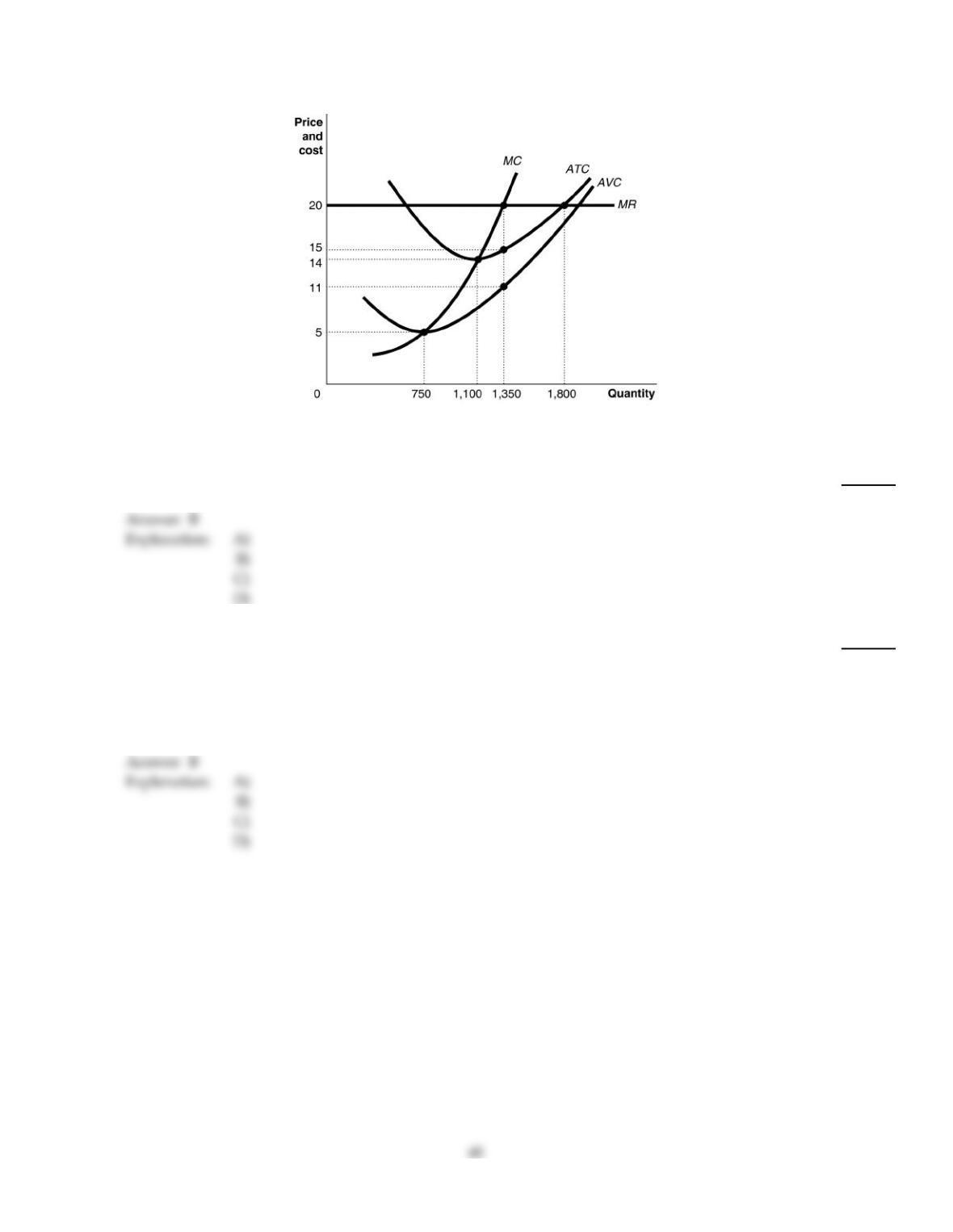

Figure 8–7

88)

Refer to Figure 8–7. Suppose the prevailing price is $20 and the firm is currently producing 1,350

units. In the long run equilibrium,

88)

A)

there will be more firms in the industry and total industry output remains constant.

B)

there will be more firms in the industry and total industry output increases.

C)

there will be fewer firms in the industry and total industry output decreases.

D)

there will be fewer firms in the industry but total industry output increases.

89)

If in a perfectly competitive industry the market price facing a firm is below its average total cost,

but above average variable cost at the output where marginal cost equals marginal revenue,

89)

A)

new firms are attracted to the industry.

B)

firms are breaking even.

C)

the industry supply will not change.

D)

some existing firms will exit the industry.

90)

All of the following can be used to compute profit per unit except

90)

A)

marginal profit minus marginal cost.

B)

price minus average total cost.

C)

average revenue minus average total cost

D)

total profit divided by quantity.

91)

The perfectly competitive market structure benefits consumers because

91)

A)

firms are forced by competitive pressure to be as efficient as possible.

B)

firms do not produce goods at the lowest possible price in the long run.

C)

firms add a much smaller markup over average cost than firms in any other type of market

structure.

D)

firms produce high quality goods at low prices.

92)

Refer to Figure 8–2. What happens if the firm produces more than Q4units?

92)

A)

It could make a profit or a loss depending on what happens to demand.

B)

It makes a loss.

C)

Its profit increases.

D)

Its total revenue is increasing faster than its total cost.

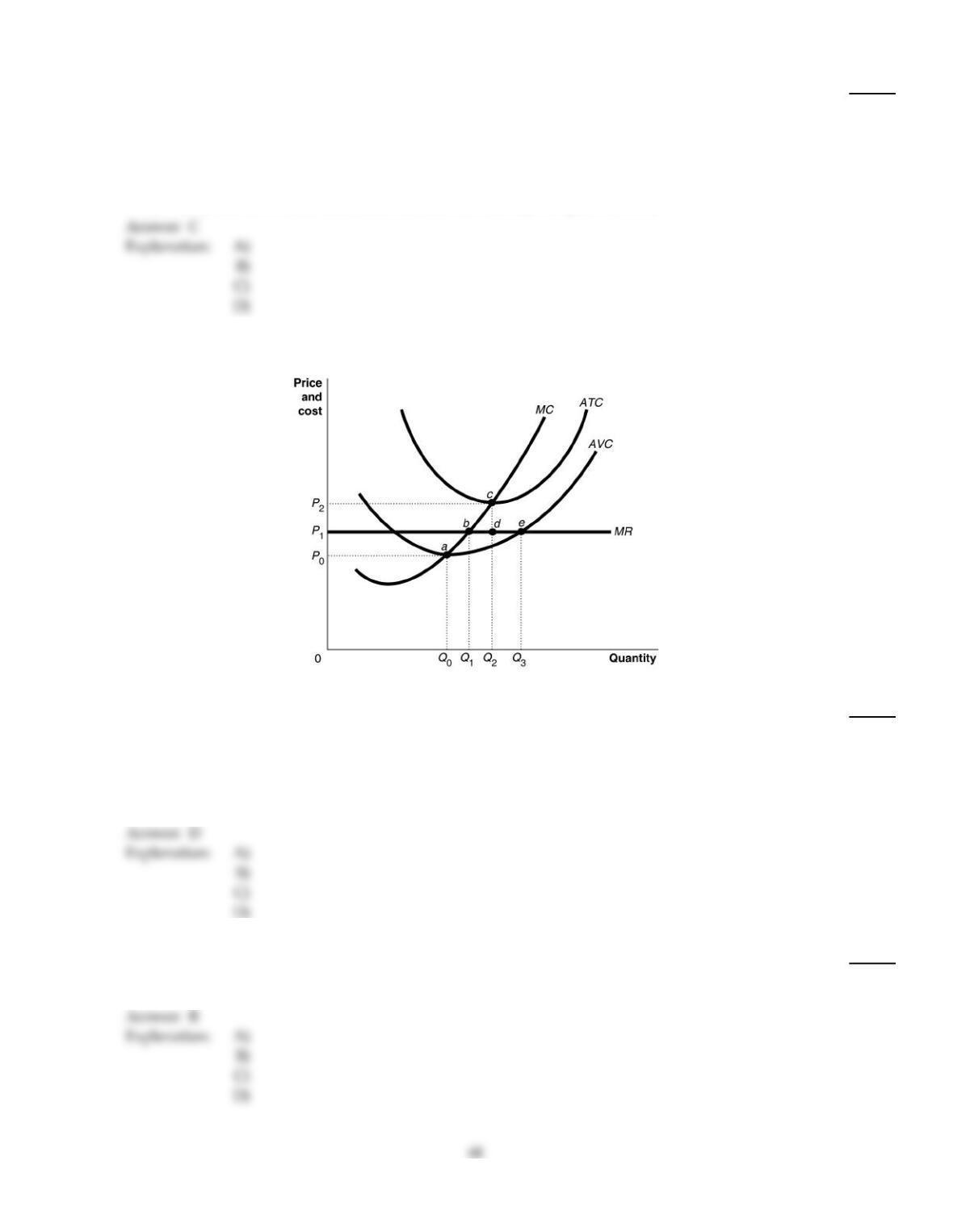

Figure 8–9

93)

Refer to Figure 8–9. Suppose the prevailing price is P1 and the firm is currently producing its

loss–minimizing quantity. If the firm represented in the diagram continues to stay in business, in

long–run equilibrium

93)

A)

it will reduce its output to Q0 and face a price of P0.

B)

it will expand its output to Q3 and face a price of P1.

C)

it will continue to produce Q1 but faces a higher price P2.

D)

it will expand its output to Q2 and face a price of P2.

94)

A perfectly competitive firm produces 1,000 units of a good at a total cost of $36,000. The

price of each good is $50. What is the firm‘s short run profit or loss?

94)

A)

profit of $14,000

B)

profit of $50,000

C)

a loss of $14,000

D)

There is insufficient information to answer the question.

95)

A perfectly competitive firm produces 3,000 units of a good at a total cost of $36,000. The

price of each good is $10. What is the firm’s short run profit or loss?

95)

A)

a loss of $6,000

B)

profit of $30,000

C)

profit of $6,000

D)

There is insufficient information to answer the question.

96)

In perfect competition

96)

A)

the market demand curve is perfectly elastic while the demand curve for an individual seller’s

product is perfectly inelastic.

B)

the market demand curve is downward–sloping while the demand curve for an individual

seller’s product is perfectly elastic.

C)

the market demand curve is perfectly inelastic while the demand curve for an individual

seller’s product is perfectly elastic.

D)

the market demand curve and the individual firm’s demand curve are identical.

97)

If a perfectly competitive firm maximizes its profit

97)

A)

total revenue is maximized.

B)

marginal revenue equals marginal cost.

C)

production must occur where average cost is minimized.

D)

market price exceeds marginal cost.

Figure 8–6

Figure 8–6 shows cost and demand curves facing a profit–maximizing perfectly competitive firm.

98)

Refer to Figure 8–6. At price P4, the firm would

98)

A)

lose an amount less than fixed costs.

B)

make a profit.

C)

make a normal profit.

D)

lose an amount equal to its fixed costs.

99)

Val Alvarado, an accountant, quit his $80,000–a–year job and bought an existing laundry from its

previous owner. The lease had five years remaining and required a monthly payment of $4,000.

Val’s explicit costs are $3,000 per month more than his revenue. Should Val continue operating his

business?

99)

A)

Val should continue to run the laundry until his lease runs out.

B)

If Val’s marginal revenue is greater than or equal to his marginal cost, then he should stay in

business.

C)

Val’s explicit cost exceeds his total revenue. He should shut down his laundry.

D)

cannot be determined without knowing his revenue

100)

If, as a perfectly competitive industry expands, it can supply larger quantities at the same long–run

market price, it is

100)

A)

an increasing–cost industry.

B)

a decreasing–cost industry.

C)

a fixed–cost industry.

D)

a constant–cost industry.

101)

Assume that the industry that produces television sets is perfectly competitive. Suppose a firm

develops a successful innovation that enables it to lower its cost of production. What happens in the

short run and in the long run?

101)

A)

Initially, the firm will be able to increase its profit significantly but in the long run its profits

will still be greater than zero but lower than its short–run profits because other firms would

also innovate.

B)

This firm will be able to earn above normal profits indefinitely if it obtains a patent for its

innovation.

C)

The firm will probably incur temporary losses because of the high cost of the innovation but

in the long run it will earn economic profits.

D)

The firm will be able to increase its profits temporarily but in the long run profits will be

eliminated as other firms copy the innovation.

102)

If, for a perfectly competitive firm, price exceeds the marginal cost of production the firm should

102)

A)

keep output constant and enjoy the above normal profit.

B)

reduce its output.

C)

increase its output.

D)

lower the price.

103)

For a perfectly competitive firm, which of the following is not true at profit maximization?

103)

A)

Marginal revenue equals marginal cost.

B)

Total revenue minus total cost is maximized.

C)

Market price is greater than marginal cost.

D)

Price equals marginal cost.

104)

In long–run perfectly competitive equilibrium, which of the following is false?

104)

A)

There is efficient, low–cost production at the minimum efficient scale.

B)

Economic surplus is maximized.

C)

Economies of scale are exhausted.

D)

Firms earn economic profit.

Figure 8–6

Figure 8–6 shows cost and demand curves facing a profit–maximizing perfectly competitive firm.

105)

Refer to Figure 8–6. At price P1, the firm would

105)

A)

lose an amount equal to its fixed costs.

B)

lose an amount less than fixed costs.

C)

lose an amount more than fixed costs.

D)

break even.

106)

A perfectly competitive firm earns an profit when price is

106)

A)

equal to minimum average variable cost.

B)

above minimum average total cost.

C)

equal to minimum average total cost.

D)

equal to minimum average fixed costs.

107)

A perfectly competitive firm in a constant–cost industry produces 3,000 units of a good at a total

cost of $36,000. The prevailing market price is $15. What will happen to the number of firms in the

industry and to the industry’s output in the long run?

107)

A)

The number of firms remains constant and the industry’s output decreases.

B)

The number of firms and the industry‘s output decrease.

C)

The number of firms and the industry’s output increase.

D)

The number of firms remains constant and the industry‘s output increases.

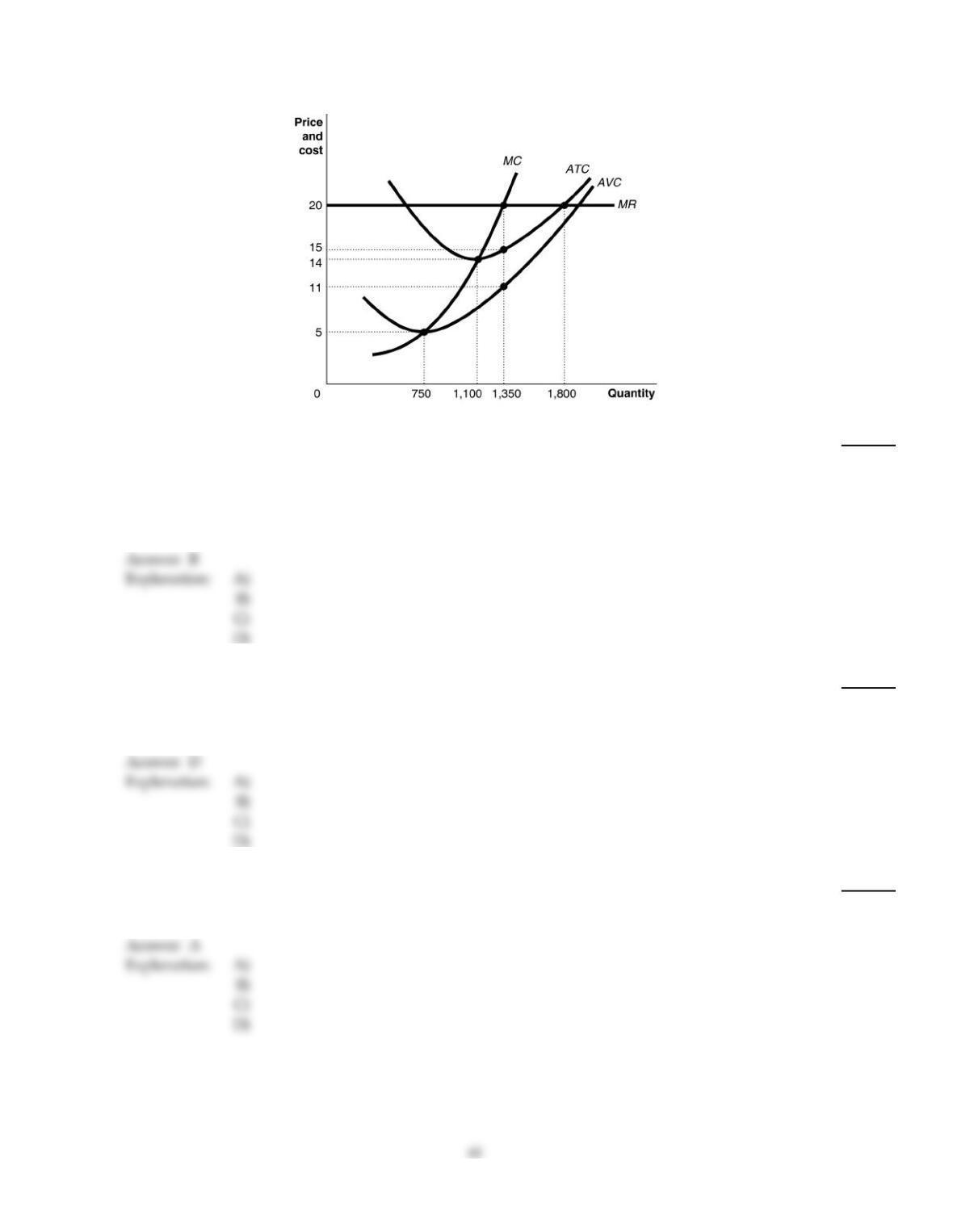

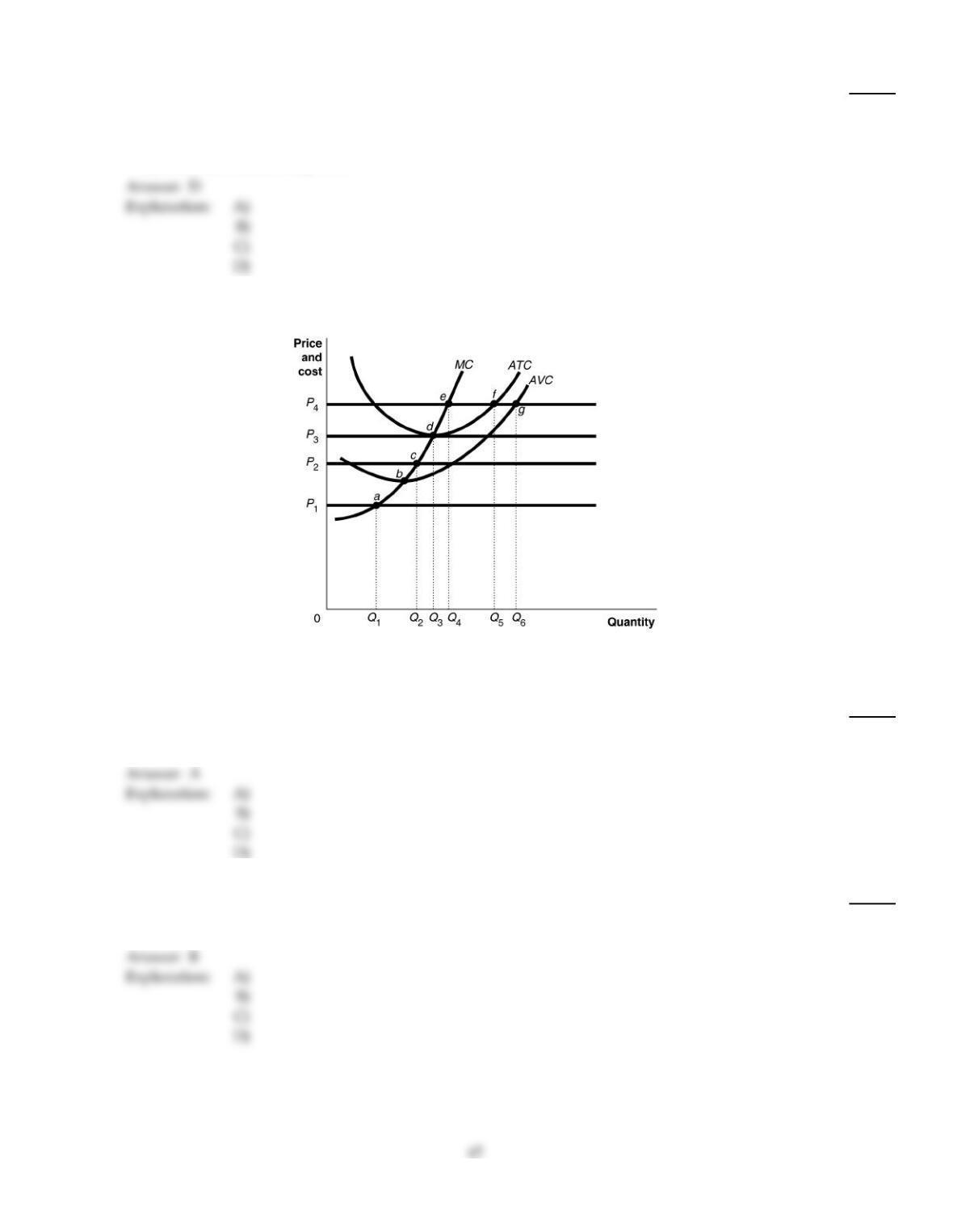

Figure 8–9

108)

Refer to Figure 8–9. Suppose the prevailing price is P1 and the firm is currently producing its

loss–minimizing quantity. In long–run equilibrium

108)

A)

there will be more firms in the industry and total industry output increases.

B)

there will be fewer firms in the industry but total industry output increases.

C)

there will be more firms in the industry and total industry output remains constant.

D)

there will be fewer firms in the industry and total industry output decreases.

D

109)

The price of a seller‘s product in perfect competition is determined by

109)

A)

a few of the sellers.

B)

market demand and market supply.

C)

the individual seller.

D)

the average consumer.

B

C

110)

If a perfectly competitive firm’s price is above its average total cost, the firm

110)

A)

should shut down.

B)

is incurring a loss.

C)

is breaking even.

D)

is earning a profit.

111)

If total variable cost exceeds total revenue at all output levels, a perfectly competitive firm

111)

A)

has covered its fixed costs.

B)

should shut down in the short run.

C)

should produce in the short run.

D)

is making short–run profits.

B

112)

In the long run a perfectly competitive market will

112)

A)

supply whatever amount consumers will buy at a price that will earn the firm an economic

profit.

B)

generate a long run equilibrium where the typical firm operates at a loss.

C)

supply whatever amount consumers demand at a price determined by the minimum point on

the typical firm’s average total cost curve.

D)

produce only the quantity of output that yields a long–run profit for the typical firm.

C

SHORT ANSWER. Write the word or phrase that best completes each statement or answers the question.

113)

Why are individual buyers and sellers in perfect competition called price takers?

113)

114)

How are market price, average revenue, and marginal revenue related for a perfectly

competitive firm and why?

114)

D

115)

Consider the market for wheat which is a perfectly competitive market. Is the market

demand curve the same as the demand curve facing an individual producer? If not,

explain how and why they are different. Illustrate your answer with graphs.

115)

116)

Under what conditions should a competitive firm shut down in the short run?

116)

TRUE/FALSE. Write ‘T’ if the statement is true and ‘F’ if the statement is false.

117)

Maximizing average profit is equivalent to maximizing total profit.

117)

118)

In the short run, if price falls below a firm’s minimum average total cost, the firm should shut

down.

118)

119)

Firms in perfect competition produce the allocatively efficient output in the short run and in the

long run.

119)

120)

In the short run, a firm might choose to produce rather than shut down even if its market price is

less than its average total cost of production.

120)

121)

A perfectly competitive firm breaks even at a price equals to its minimum average total cost.

121)

122)

In the short run, if a firm shuts down it avoids its variable cost but not its fixed cost.

122)

123)

For a perfectly competitive firm at the profit–maximizing output, average revenue equals marginal

cost.

123)

124)

The assumption that there are no barriers to new firms entering the market or exiting a market

guarantees that any excess profits will be eliminated.

124)

125)

A perfectly competitive firm in long–run equilibrium produces output at the lowest possible

average total cost.

125)

126)

If a perfectly competitive industry has a perfectly elastic long–run supply curve, then input prices

remain constant as the industry expands.

126)

127)

The market demand curve for a perfectly competitive industry is the horizontal summation of each

individual firm’s demand curve.

127)

128)

In the short run, a firm that incurs losses might choose to produce rather than shut down if the

amount of its revenue is less than its fixed cost.

128)

129)

A perfectly competitive firm‘s horizontal demand curve implies that the firm does not have to

lower its price to sell more output.

129)

130)

Farmers in California are taking resources out of non–organic produce farming and putting them

into organic produce farming. This suggests that at present organic produce farmers earn economic

profits.

130)

131)

Firms in perfect competition produce the productively efficient output level in the short run and in

the long run.

131)

132)

If a firm in a perfectly competitive industry introduces a lower–cost way of producing an existing

product the firm will be able to earn economic profits in the long run.

132)

133)

If a perfectly competitive industry has a downward sloping long–run supply curve, it suggests that

the demand for the industry‘s product is decreasing over time.

133)

134)

The minimum point on the average variable cost curve is called the loss–minimizing point.

134)

135)

In an increasing–cost industry the long–run supply curve is upward–sloping.

135)

136)

If in the long run a firm makes zero profit, it should exit the industry.

136)

137)

In the short run, if a firm shuts down its maximum loss equals the amount of its fixed cost.

137)

138)

If a firm’s total variable cost exceeds its total revenue, the firm should stop production by shutting

down temporarily.

138)

139)

Perfectly competitive industries tend to produce low–priced, low–technology products.

139)

140)

A perfectly competitive firm’s marginal revenue curve is downward–sloping.

140)

141)

Assume that the personal computer industry is perfectly competitive. The fact that the price of

personal computers over the last decade has fallen, despite increases in demand, signifies that the

industry is a decreasing–cost industry.

141)

142)

A perfectly competitive firm in a constant–cost industry produces 1,000 units of a good at a total

cost of $50,000. If the prevailing market price is $48, the number of firms and the industry’s output

will decrease in the long run.

142)

143)

A perfectly competitive firm in an increasing–cost industry faces an upward sloping long–run

demand curve.

143)