199. High Life Corporation has the following sales budget for the last four months of 2014:

Month Sales

September $400,000

October 320,000

November 440,000

December 360,000

Historically, the following trend has been established regarding cash collection of sales:

65 percent in month of sale

25 percent in month following sale

8 percent in second month following sale

2 percent uncollectible

The company allows a 2 percent cash discount for payments made by customers during the month of the sale.

July and August sales were $400,000 and $240,000, respectively.

Required:

Prepare a schedule of budgeted cash collections from sales for September, October, and November.

200. Sales for October, November, and December are expected to be $200,000, $180,000, and $220,000,

respectively, for the Gurumai Company. All sales are on account (terms 2/15, net 30 days) and are collected 50

percent in the month of sale and 50 percent in the following month. One-half of all sales discounts are taken on

the average. Materials are purchased one month before being needed, and all purchases and expenses are paid

for as incurred. Activities for the quarter are expected to be:

October

November

December

Materials used

$40,000

$36,000

$44,000

Salaries

70,000

68,000

72,000

Maintenance and repairs

18,000

18,000

18,000

Depreciation

36,000

36,000

36,000

Utilities and other

14,000

14,000

14,000

Dividends paid

-0-

10,000

-0-

Payment on bonds

8,000

8,000

8,000

Required:

Using the given information, prepare a cash budget for November.

Cash receipts:

Sales:

October ($200,000 ´ 0.50 ´ 0.99*)

$99,000

November ($180,000 ´ 0.50 ´ 0.99*)

89,100

Total

$188,100

Cash disbursements:

Materials

$44,000

Salaries and wages

68,000

Maintenance and repairs

18,000

Utilities and other

14,000

Dividends

10,000

Payment on bonds

8,000

162,000

Net cash inflow (outflow)

$ 26,100

201. Thunderbolt Corporation is in the process of preparing its budget for next year. Cost of goods sold has

been estimated at 60 percent of sales. Merchandise purchases are to be made during the month preceding the

month of the sales. Thunderbolt pays 60 percent in the month of purchase, and 40 percent in the month

following. Wages are estimated at 20 percent of sales and are paid during the month of sale. Other operating

costs amounting to 10 percent of sales are to be paid in the month following the sale. The accounts payable

balance on June 30 was $48,000.

Month Sales

June $170,000

July 200,000

August 120,000

September 150,000

October 160,000

November 100,000

Required:

Prepare a schedule of cash disbursements for July, August, and September.

202. Edison, Inc., a retailer of specialty art supplies, prepares a monthly master budget. Data for the September

master budget are given below:

a.

The August 31st balance sheet:

Cash

$ 25,500

Accounts payable

$ 53,760

Accounts receivable

90,000

Capital stock

265,000

Inventory

28,800

Retained earnings

25,540

Building and equipment (net)

200,000

b.

Actual sales for August and budgeted sales for September, October, and November are given below:

August

$120,000

September

360,000

October

200,000

November

180,000

c.

Sales are 25 percent for cash and 75 percent on credit. All credit sales are collected in the month following the sale. There are no bad

debts.

d.

The gross margin percentage is 60 percent of sales. The desired ending inventory is equal to 20 percent of the following month’s cost of

goods sold. One fifth of the purchases are paid for in the month of purchase and the others are purchased on account and paid in full the

following month.

e.

The monthly cash operating expenses are $80,000, including the monthly depreciation expense of $7,000.

f.

During September, Edison, Inc., will purchase new office equipment for $17,000 cash.

g.

Dividends of $13,500 were declared and paid in September.

h.

The company must maintain a minimum cash balance of $25,000. A line of credit is used to maintain this balance. Borrowing will be made

in increments of $1,000. All borrowing is done at the beginning of the month and repayments are made at the end of the month. The annual

interest rate is 12 percent, paid when the loan is repaid (ignore accrual of interest).

Required:

Prepare a balance sheet, income statement, and cash budget for the month of September.

Balance Sheet:

Cash

$ 25,000

Accounts payable

$104,960

Accounts receivable

270,000

Loans payable

3,000

Inventory

16,000

Capital stock

265,000

Building and equipment (net)

210,000

Retained earnings

148,040

$521,000

$521,000

203. The city of Charleston had the following sales of water for the selected months of 2014:

Month

Sales

February

$50,000

March

45,000

April

60,000

May

42,500

June

70,000

July

120,000

All sales are on credit. Historically, 50 percent is collected in the month of sale, 35 percent during the first month following the sale, and 15 percent

in the second month following the sale.

Cost of water averages 75 percent of sales. Water is purchased in the month of sale. All purchases are paid during the month following the purchase.

Operating costs of $10,000 are paid each month.

The April 1 cash balance is expected to be the minimum balance of $5,000.

Money can be borrowed from a local bank in increments of $1,000. (Do not include interest charges in your budget.)

Required:

Prepare a cash budget for April, May, and June.

April

May

June

Total

Beginning cash balance

$ 5,000

$14,500

$ 8,500

$ 5,000

Plus: Cash collections:

Month of sale (0.50)

30,000

21,250

35,000

86,250

Month following (0.35)

15,750

21,000

14,875

51,625

Second mo. following (0.15)

7,500

6,750

9,000

23,250

Total cash available

$58,250

$63,500

$67,375

$166,125

Less disbursements:

Water

$33,750

$45,000

$31,875

$110,625

Operating costs

10,000

10,000

10,000

30,000

Total disbursements

$43,750

$55,000

$41,875

$140,625

Ending cash balance

$14,500

$ 8,500

$25,500

$ 25,500

204. Ruger, Inc., is looking for feedback on performance. The company compares the budget for the year with

the actual costs.

Ruger had the following budgeted data:

Budgeted variable costs per unit:

Direct materials

$11.00

Direct labor

15.00

Supplies

0.80

Indirect labor

1.00

Power

0.10

Budgeted fixed overhead for 2014:

Supervision

$ 9,000

Depreciation

13,000

Rent

12,000

Required:

Prepare a flexible budget for production costs for the following range of activity: 2,500 units; 4,000 units; 6,000 units.

2,500 Units

4,000 Units

6,000 Units

Direct materials

$11.00

$ 27,500

$ 44,000

$ 66,000

Direct labor

15.00

37,500

60,000

90,000

Supplies

0.80

2,000

3,200

4,800

Indirect labor

1.00

2,500

4,000

6,000

Power

0.10

Budgeted fixed overhead for 2014:

Supervision

9,000

9,000

9,000

Depreciation

13,000

13,000

13,000

Total costs

$103,750

$145,600

$201,400

205. Missoula, Inc., is looking for feedback on performance. The company compares the budget for the year

with the actual costs.

Missoula, Inc., had the following budgeted data:

Unit sales for 2014

10,000

Unit production for 2014

10,000

Budgeted fixed overhead for 2014:

Supervision

$18,000

Depreciation

20,000

Rent

10,000

Budgeted variable costs per unit:

Direct materials

$18.00

Direct labor

25.00

Supplies

0.20

Indirect labor

1.00

Power

0.10

The following actually occurred:

Actual unit sales for 2014

11,000

Actual unit production for 2014

12,000

Actual fixed overhead for 2014:

Supervision

$17,850

Depreciation

20,000

Rent

10,000

Actual variable costs for 2014:

Direct materials

$214,000

Direct labor

320,000

Supplies

2,500

Indirect labor

10,000

Power

1,500

Required:

a.

Prepare a performance report for all costs showing static budget variances.

b.

Prepare a performance report for all costs showing flexible budget variances.

206. Compare and contrast static budgets, flexible budgets, and activity-based budgets.

A static budget is a budget developed for one level of activity. Once a sales number is calculated, the

production, marketing, and administrative budgets are based on that sales number. A static budget does not take

into consideration fluctuations in actual demand and sales for an organization. Since actual activity rarely equals

a budgeted level, static budgets are not usually relevant when performance reports are needed. They are useful

for planning purposes.

207. Collibri, Inc., has done a cost analysis for its production of banners. The following activities and cost

drivers have been developed:

Activity

Cost Formula

Maintenance

$13,000 + $2 per machine hour

Machining

$45,000 + $6 per machine hour

Inspection

$70,000 + $500 per batch

Setups

$2,000 per batch

Purchasing

$80,000 + $150 per purchase order

Following are the actual costs of producing 75,000 banners:

1,000 machine hours; 15 batches; 10 purchase orders

Maintenance

$14,000

Machining

50,000

Inspection

70,000

Setups

32,000

Purchasing

82,000

Required:

Prepare an activity-based performance report.

Actual

Budget 75,000

Variance

Maintenance

$ 14,000

$ 15,000

$1,000 F

Machining

50,000

51,000

1,000 F

Inspection

70,000

77,500

7,500 F

Setups

32,000

30,000

2,000 U

Purchasing

82,000

81,500

500 U

Total

$248,000

$255,000

$7,000 F

208. Ringwold, Inc., has done a cost analysis for its production of baseball cards. The following activities and

cost drivers have been developed:

Activity

Cost Formula

Photography

$50 + $35 per labor hour

Printing

$25,000 + $0.01 per machine hour

Setups

$25 per batch

Purchasing

$25 + $25 per purchase order

Following are the actual costs of producing 35,000 cards:

60 labor hours; 500 machine hours; 5 batches; 30 purchase orders

Photography

?

Printing

$25,000

Setups

?

Purchasing

$770

The following variances were given in the activity performance report:

Photography

$10 F

Printing

?

Setups

$20 U

Purchasing

?

Required:

Find the missing values.

Actual

Budget

Variance

Photography

$ 2,140

$ 2,150

$10 F

Printing

25,000

25,005

5 F

Setups

20 U

Purchasing

770

775

5 F

Total costs

$28,055

$28,055

$-0-

209. Splendor, Inc., has done a cost analysis for its production of motorcycle lights.

The following activities and cost drivers have been developed:

Activity

Cost Formula

Maintenance

$5,000 + $8 per machine hour

Machining

$25,000 + $4 per machine hour

Inspection

$90,000 + $1,000 per batch

Setups

$5,000 per batch

Purchasing

$100,000 + $100 per purchase order

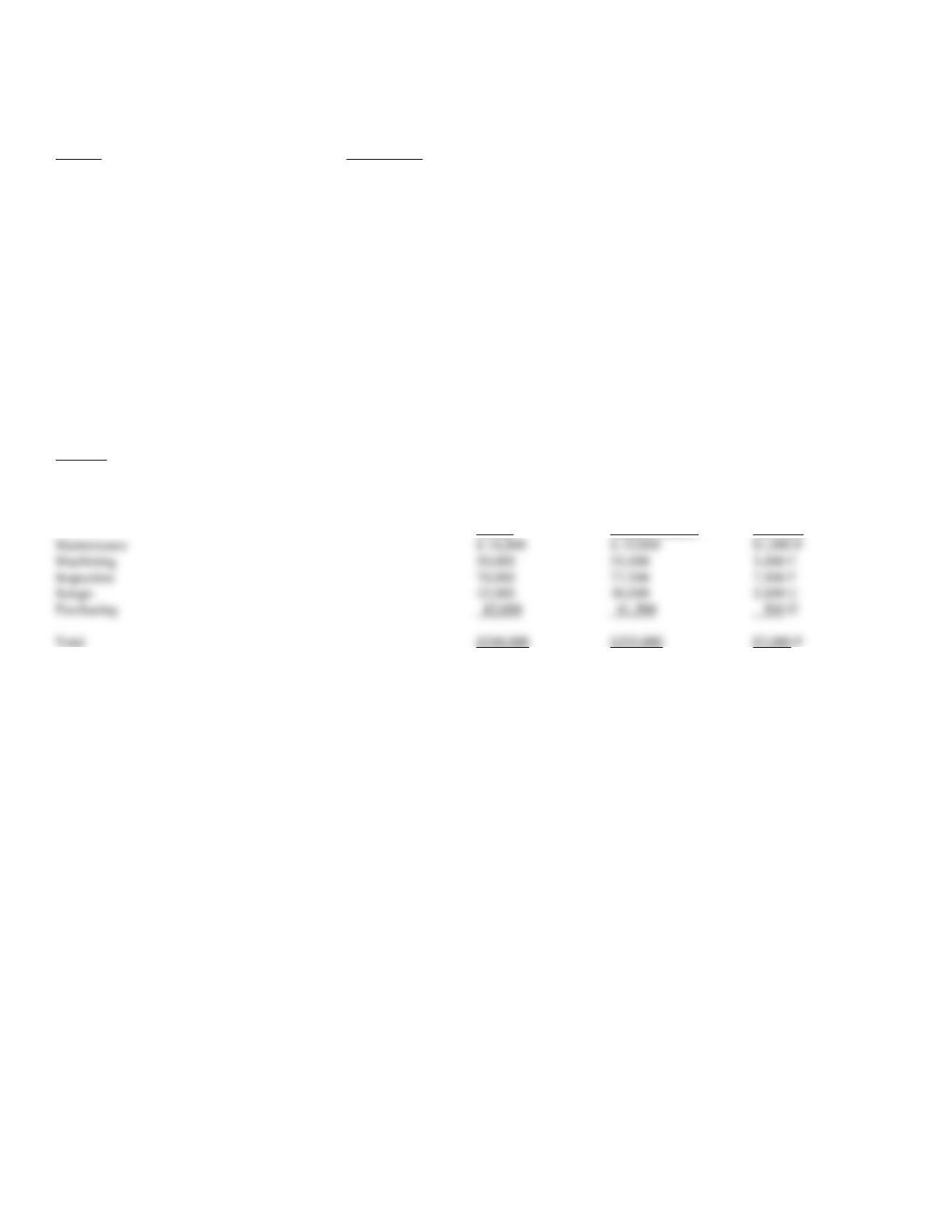

Required:

Prepare an activity-based budget for the following:

210. Discuss the features of an ideal budgetary process.

60,000 Units

100,000 Units

Maintenance

$ 85,000

$ 149,000

Machining

65,000

97,000

Inspection

120,000

130,000

Setups

150,000

200,000

Purchasing

2,100,000

3,100,000