Reporting and Analyzing Receivables

FOR INSTRUCTOR USE ONLY

8-61

Ex. 231

On December 31, 2016, when its Allowance for Doubtful Accounts had a credit balance of

$1,500, Leeds Company estimates that 6% of its accounts receivable balance of $95,000 will

become uncollectible. On March 3, 2017, Leeds Company determined that Megan Jost’s account

of $950 was uncollectible. On May 15, 2017, Jost paid the amount previously written off.

Instructions

Prepare the journal entries for December 31, 2016, March 3, 2017 and May 15, 2017.

Ex. 232

The percentage of receivables approach to estimating bad debts expense is used by Hayes

Company. On February 28, the firm had accounts receivable in the amount of $585,000 and

Allowance for Doubtful Accounts had a credit balance of $370 before adjustment. Net credit sales

for February amounted to $3,000,000. The credit manager estimated that uncollectible accounts

would amount to 5% of accounts receivable. On March 10, an accounts receivable from Mark

Dole for $2,100 was determined to be uncollectible and written off. However, on March 31, Dole

received an inheritance and immediately paid his past due account in full.

(a) Prepare the journal entries made by Hayes Company on the following dates:

1. February 28

2. March 10

3. March 31

(b) Assume no other transactions occurred that affected the allowance account during March.

Determine the balance of Allowance for Doubtful Accounts at March 31.

Test Bank for Financial Accounting: Tools for Business Decision Making, Eighth Edition

FOR INSTRUCTOR USE ONLY

8-62

Ex. 233

Hess Computer Store has credit sales of $450,000 in 2016 and a debit balance of $600 in the

Allowance for Doubtful Accounts at year end. As of December 31, 2016, $130,000 of accounts

receivable remain uncollected. The credit manager of Hess prepared an aging schedule of

accounts receivable and estimates that $7,800 will prove to be uncollectible.

On March 4, 2017 the credit manager authorizes a write-off of the $1,000 balance owed by A.

Myers.

Instructions

(a) Prepare the adjusting entry to record the estimated uncollectible accounts expense in 2016.

(b) Show the balance sheet presentation of accounts receivable on December 31, 2016.

(c) On March 4, before the write-off, assume the balance of Accounts Receivable account is

$145,000 and the balance of Allowance for Doubtful Accounts is a credit of $5,000. Make the

appropriate entry to record the write off of the Myers account. Also show the balance sheet

presentation of accounts receivable before and after the write-off.

Reporting and Analyzing Receivables

FOR INSTRUCTOR USE ONLY

8-63

Cash Realizable Value $140,000 $140,000

Ex. 234

Hachey Company has accounts receivable of $95,100 at March 31, 2017. An analysis of the

accounts shows these amounts.

Balance, March 31

Month of Sale 2017 2016

March $65,000 $75,000

February 12,600 8,000

December and January 10,100 2,400

November and October 7,400 1,100

$95,100 $86,500

Credit terms are 2/10, n/30. At March 31, 2017, there is a $2,500 credit balance in Allowance for

Doubtful Accounts prior to adjustment. The company uses the percentage of receivables basis for

estimating uncollectible accounts. The company’s estimates of bad debts are as shown below

Estimated Percentage

Age of Accounts Uncollectible

Current 2%

1–30 days past due 7

31–90 days past due 25

Over 90 days past due 50

Instructions

(a) Determine the total estimated uncollectibles.

(b) Prepare the adjusting entry at March 31, 2017, to record bad debts expense.

Test Bank for Financial Accounting: Tools for Business Decision Making, Eighth Edition

FOR INSTRUCTOR USE ONLY

8-64

Ex. 235

Compute the missing amount for each of the following notes:

Principal Annual Interest Rate Time Total Interest

______________________________________________________________________

(a) $50,000 5% 2.5 years ?

______________________________________________________________________

(b) $120,000 ? 9 months $7,200

______________________________________________________________________

(c) ? 9% 90 days $1,350

______________________________________________________________________

(d) $60,000 6% ? $1,200

______________________________________________________________________

Ex. 236

Record the following transactions in general journal form for the Newell Company.

July 1 Received a $9,000, 8%, 3–month note, dated July 1, from Lois Patton in payment of

her open account.

Oct. 1 Received notification from Lois Patton that she was unable to honor her note at this

time. It is expected that Patton will pay at a later date.

Nov. 15 Received full payment from Lois Patton for note receivable previously dishonored.

Reporting and Analyzing Receivables

FOR INSTRUCTOR USE ONLY

8-65

Ex. 237

Grey Boat Company often requires customers to sign promissory notes for major credit

purchases. Journalize the following transactions for Grey Boat Company.

Feb. 12 Accepted a $35,000, 6%, 60-day note from Bill Bazil for a 19-foot motorboat built to

his specifications.

April 14 Received notification from Bill Bazil that he was unable to honor his promissory note

but that he expects to pay the amount owed in May.

May 26 Received a check from Bill Bazil for the total amount owed.

June 10 Received notification by the bank that Bill Bazil’s check was being returned “NSF” and

that Mr. Bazil had declared personal bankruptcy.

Test Bank for Financial Accounting: Tools for Business Decision Making, Eighth Edition

8-66

Ex. 238

Compute the maturity value as indicated for each of the following notes receivable.

1. An $8,000, 6%, 3-month note dated April 20.

Maturity value $____________.

2. A $20,000, 9%, 72-day note dated March 5.

Maturity value $____________.

3. A $12,000, 5%, 30-day note dated September 10.

Maturity value $____________.

4. A $9,000, 7%, 6-month note dated November 15.

Maturity value $____________.

Ex. 239

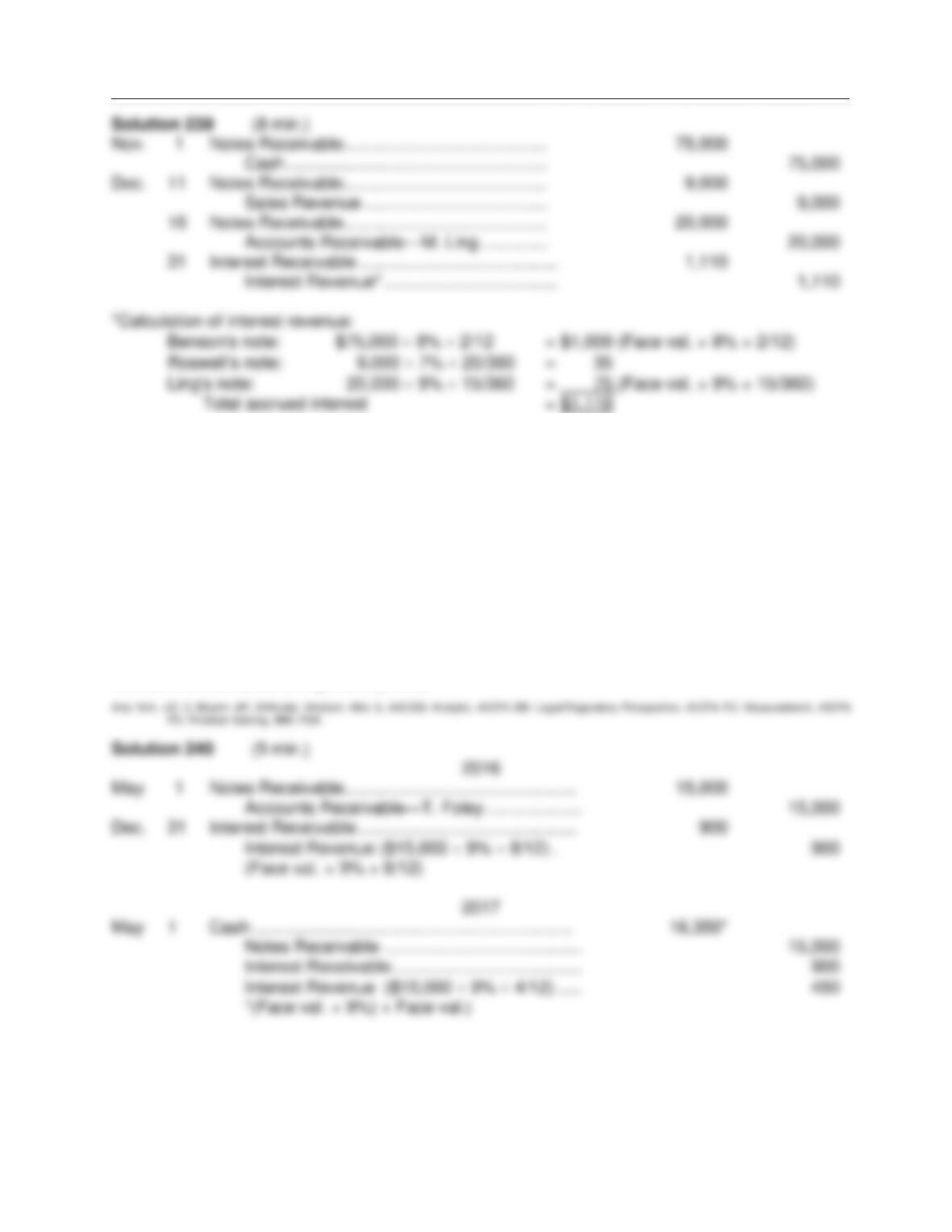

Great Plains Supply Co. has the following transactions related to notes receivable during the last

2 months of the year.

Nov. 1 Loaned $75,000 cash to B. Benson on a 1-year, 8% note.

Dec. 11 Sold goods to Roswell, Inc., receiving a $9,000, 90-day, 7% note.

16 Received a $20,000, 6-month, 9% note to settle an open account from M. Ling.

31 Accrued interest revenue on all notes receivable.

Instructions

Journalize the transactions for Great Plains Supply Co.

Reporting and Analyzing Receivables

FOR INSTRUCTOR USE ONLY

8-67

Ex. 240

These transaction took place for Sanders Co.

2016

May 1 Received a $15,000, 1-year, 9% note in exchange for an outstanding account

receivable from T. Foley.

Dec. 31 Accrued interest revenue on the T. Foley note.

2017

May 1 Received principal plus interest on the T. Foley note. (No interest has been accrued

since December 31, 2016.)

Instructions

Record the transactions in general journal.

Test Bank for Financial Accounting: Tools for Business Decision Making, Eighth Edition

8-68

Ex. 241

Presented here is basic financial information (in millions) from the annual reports of Nike and

Adidas.

Nike Adidas

Sales revenue $18,627 $10,299

Allowance for doubtful accounts, Jan. 1 71.5 112

Allowance for doubtful accounts, Dec. 31 78.4 111

Accounts receivable balance (gross), Jan 1 2,566.2 1,527

Accounts receivable balance (gross), Dec. 31 2,873.7 1,570

Instructions

Calculate the accounts receivable turnover and average collection period for both companies.

Comment on the difference in their collection experiences.

Ex. 242

The following information is available from the annual reports of Nite and Day Companies.

(In millions)

Nite Day

Sales revenue $112,500 $32,000

Beginning accounts receivable, net 19,000 3,500

Ending accounts receivable, net 18,500 4,400

Instructions

(a) Based on the preceding information, compute the following for each company:

1. Accounts receivable turnover. (Assume all sales were credit sales.)

2. Average collection period.

(b) What conclusion concerning the management of accounts receivable can be drawn from

these data?

Reporting and Analyzing Receivables

FOR INSTRUCTOR USE ONLY

8-69

Ex. 243

Shafer Company has the following accounts in its general ledger at July 31: Accounts Receivable

$49,000 and Allowance for Doubtful Accounts $3,400. During August, the following transactions

occurred.

Aug. 15 Sold $30,000 of accounts receivable to More Factors, Inc. who assesses a 2%

finance charge.

25 Made sales of $2,500 on Visa credit cards. The credit card service charge is 3%.

28 Made sales of $4,000 on Shafer credit cards.

Instructions

(a) Journalize the transactions.

(b) Indicate the statement presentation of service charges.

Test Bank for Financial Accounting: Tools for Business Decision Making, Eighth Edition

8-70

COMPLETION STATEMENTS

244. Notes and accounts receivable that result from sales transactions are often called

______________ receivables.

245. Two accounting problems associated with accounts receivable are (1) ______________

and (2) ______________ accounts receivable.

246. The net amount expected to be collected in cash from receivables is the _____________.

247. When credit sales are made, _________________ Expense is considered a normal and

necessary risk of doing business on a credit basis.

248. The two methods used in accounting for uncollectible accounts are the ____________

method and the ______________ method.

249. Allowance for Doubtful Accounts is a _____________ account which is ______________

from Accounts Receivable on the balance sheet.

250. When the allowance method is used to account for uncollectible accounts, ____________

is debited when an account is determined to be uncollectible.

251. The _________________ basis of estimating uncollectibles normally results in the best

approximation of _______________ value.

252. A 75-day note receivable dated July 5 would mature on ______________.

253. Collection of a note receivable will result in a credit to ______________ for the face value

of the note and a credit to ______________.

254. A note that is not paid on the maturity date is said to be ______________.

Reporting and Analyzing Receivables

8-71

255. A concentration of ______________ is a threat of nonpayment from a single customer or

class of customers.

256. The ratio used to assess the liquidity of accounts receivable is the ______________.

257. A finance company or bank that purchases receivables from businesses is known as a

______________.

Answers to Completion Statements

MATCHING

258. Match the items below by entering the appropriate code letter in the space provided.

A. Aging the accounts receivable F. Percentage of receivables basis

B. Direct write-off method G. Promissory note

C. Obligation due H. Dishonored note

D. Trade receivables I. Cash net realizable value

E. Accounts receivable turnover J. Credit card sales

____ 1. A written promise to pay a specified amount on demand or at a definite time.

____ 2. Sales that involve the customer, the retailer, and the credit card issuer.

____ 3. A measure of the liquidity of receivables.

____ 4. Notes and accounts receivable that result from sales transactions.

____ 5. A note which is not paid in full at maturity.

____ 6. Analysis of customer account balances by length of time they have been unpaid.

____ 7. Emphasizes expected cash realizable value of accounts receivable.

____ 8. Bad debt losses are not estimated and no allowance account is used.

____ 9. The net amount expected to be received in cash.

Test Bank for Financial Accounting: Tools for Business Decision Making, Eighth Edition

8-72

Answers to Matching

5. H

SHORT-ANSWER ESSAY QUESTIONS

S-A E 259

a. List the characteristics of promissory notes.

b. List the reasons for obtaining promissory notes from customers.

c. What action relating to promissory notes must be taken at the end of the accounting period?

S-A E 260

Two methods can be used in accounting for uncollectible accounts. Identify and contrast the two

methods. How do the methods differ regarding the time periods in which Bad Debt Expense is

recognized?

Reporting and Analyzing Receivables

FOR INSTRUCTOR USE ONLY

8-73

S-A E 261

Your roommate is uncertain about the advantages of a promissory note. Compare the

advantages of a note receivable with those of an account receivable.

S-A E 262

Jenkins Company dishonors a note at maturity. What are the options available to the lender?

S-A E 263

An article in the Wall Street Journal indicated that companies are selling receivables at a record

rate. Why do companies sell their receivables?

S-A E 264

Your friend Mark has opened an office supply store. He will extend open credit to local

businesses and is concerned about potential bad debts. What can Mark do to reduce potential

bad debts?

Test Bank for Financial Accounting: Tools for Business Decision Making, Eighth Edition

FOR INSTRUCTOR USE ONLY

8-74

S-A E 265

Company

Name

Net Credit

Sales

Beginning

Net Receivables

Ending

Net Receivables

Brown

$180,000

$ 5,000

$30,000

Pink

$400,000

$52,000

$42,000

Yellow

$ 75,000

$ 5,400

$ 5,800

(a) Which company is doing the best job of managing its accounts receivable? Why? Be sure to

support your answer with computations.

(b) What are your concerns about these companies?

$180,000

Reporting and Analyzing Receivables

FOR INSTRUCTOR USE ONLY

8-75

S-A E 266

Banks that issue credit cards generally charge retailers a fee of 2 to 4% of the amount of sale.

List reasons why companies are willing to pay these fees.

S-A E 267

Customer purchases using credit cards are a significant source of revenue for many retailers.

From the standpoint of a retailer, briefly discuss some advantages and disadvantages of a retail

store having its own credit card as opposed to accepting one of the national credit cards (e.g.,

Visa or MasterCard).

Test Bank for Financial Accounting: Tools for Business Decision Making, Eighth Edition

FOR INSTRUCTOR USE ONLY

8-76

S-A E 268 (Ethics)

Two Brothers, a small book publishing company, wrote off the debt of The Learning Place, and

the Academy of Basic Education, both small private schools, after it determined that the schools

were facing serious financial difficulty. No notice of the action was sent to the schools; Two

Brothers simply stopped sending bills. Nearly a year later, The Learning Place was given a large

endowment and a government grant. The resulting publicity brought the school to the attention of

Two Brothers, which immediately reinstated the account, and sent a new bill to the school,

including interest for the entire time the debt was outstanding. No further action was taken

regarding the Academy of Basic Education, which was still operational.

Required:

Did Two Brothers act ethically in reinstating the debt of one client, and not the other? Explain.

S-A E 269 (Communication)

Schmidt Company received a letter from Deborah Stine, a customer. Deborah had purchased

$325 worth of clothing from Schmidt on credit. She has made two payments of $50 each. She

has missed the last two payments, and has received a collection letter from Schmidt. Her total

debt presently, with interest and late fees, is $251.13.

Deborah sent a letter to Schmidt in which she asked for her debt to be forgiven. She said she had

heard that companies make allowances for accounts they are doubtful about collecting, and that

Schmidt certainly should have been doubtful about her—that as a college student she had

changed her major three times. She also said that she could not enjoy a high quality of life when

making such high payments, but that she didn’t want to be embarrassed by bill collectors, either.

She especially didn’t want her parents to find out that she had not paid her debts. Having Schmidt

write off her account seemed to her the best solution in the circumstances. She added that the

clothes she bought at Schmidt were among the best she had ever owned, and that she “told

everybody” that Schmidt was definitely the best place to get clothes.

Reporting and Analyzing Receivables

FOR INSTRUCTOR USE ONLY

8-77

S-A E 269 (Cont.)

Required:

You are the accounting manager for Schmidt. Write a short letter to Deborah explaining why her

debt cannot be written off.

Test Bank for Financial Accounting: Tools for Business Decision Making, Eighth Edition

8-78

IFRS QUESTIONS

1. Which receivables accounting and reporting issue is not essentially the same for IFRS

and GAAP?

a. The use of allowance accounts and the allowance method.

b. How to record discounts.

c. How to record factoring.

d. All of these answer choices are essentially the same for IFRS and GAAP.

2. Which receivables accounting and reporting issue is essentially the same for IFRS and

GAAP?

a. The use of allowance accounts and the allowance method.

b. How to record discounts.

c. How to record factoring.

d. All of these answer choices are essentially the same for IFRS and GAAP.

3. IFRS requires loans and receivables to be recorded at

a. amortized cost.

b. amortized cost, adjusted for allowances for doubtful accounts.

c. unamortized cost.

d. unamortized cost, adjusted for allowances for doubtful accounts.

4. IFRS sometimes refers to allowances as

a. revenues.

b. discounts.

c. provisions.

d. reserves.

5. IFRS

a. implies that receivables with different characteristics should be reported separately.

b. requires that receivables with different characteristics should be reported separately.

c. implies that receivables with different characteristics should be reported as one unseg-

regated amount.

d. requires that receivables with different characteristics should be reported as one un-

segregated amount.

Reporting and Analyzing Receivables

8-79

6. Which board(s) has(have) worked to implement fair value measurement for financial in-

struments?

a. FASB, but not IASB.

b. IASB, but not FASB.

c. both FASB and IASB.

d. neither FASB nor IASB.

7. Which board(s) has(have) faced bitter opposition when working to implement fair value

measurement for financial instruments?

a. FASB, but not IASB.

b. IASB, but not FASB.

c. Both FASB and IASB.

d. Neither FASB nor IASB.

8. Which is part of IFRS accounting for financial instruments?

Disclosure of fair value information Optional recording of some financial

for receivables in the notes instruments at fair value

a. Yes Yes

b. Yes No

c. No Yes

d. No No

9. Which requires a two-tiered approach to test whether the value of loans and receivables

are impaired?

GAAP IFRS

a. yes no

b. yes yes

c. no no

d. no yes

10. What criteria are used to determine how to record a factoring transaction?

GAAP IFRS

a. risks and rewards, and loss of control risks and rewards, and loss of control

b. risks and rewards, and loss of control loss of control

c. loss of control loss of control

d. loss of control risks and rewards, and loss of control

Test Bank for Financial Accounting: Tools for Business Decision Making, Eighth Edition

8-80

11. Which permits partial derecognition of receivables?

GAAP IFRS

a. yes no

b. yes yes

c. no no

d. no yes