Reporting and Analyzing Receivables

8-41

189. All of the following statements are true regarding the average collection period except:

a. it is a popular variant of the accounts receivable turnover .

b. it is used to assess the effectiveness of a company’s credit and collection policies.

c. it should generally exceed the credit term period.

d. its increase may suggest a decline in the financial health of customers.

190. In the table below the information for four companies is provided.

Company

Accounts Receivable

turnover

Average collection period

Martin

13.9

26.3

Lewis

13.3

27.4

Danforth

10.4

35.1

Garner

14.5

25.2

Industry Average

13.0

28.1

If Garner’s net credit sales are $435,000, what are its average net accounts receivable?

a. $17,262

b. $30,000

c. $63,075

d. $109,620

191. In the table below the information for four companies is provided.

Company

Accounts Receivable

turnover

Average collection period

Martin

13.9

26.3

Lewis

13.3

27.4

Danforth

10.4

35.1

Garner

14.5

25.2

Industry Average

13.0

28.1

Assuming all four companies are in the same industry, which company appears to have

the greatest likelihood of paying its current obligations?

a. Martin

b. Lewis

c. Danforth

d. Garner

Test Bank for Financial Accounting: Tools for Business Decision Making, Eighth Edition

8-42

192. Simonic Retailers accepted $80,000 of Citibank Visa credit card charges for merchandise

sold on July 1. Citibank charges 4% for its credit card use. The entry to record this

transaction by Simonic Retailers will include a credit to Sales Revenue of $80,000 and a

debit(s) to

a. Cash $76,800 and Service Charge Expense $3,200.

b. Accounts Receivable $76,800 and Service Charge Expense $3,200.

c. Cash $76,800 and Interest Expense $3,200.

d. Accounts Receivable $80,000.

193. Selling accounts receivables to factors and allowing credit terms such as 2/10, n/30

a. represent common business practices.

b. represent ways to accelerate receivables collections.

c. result in collections that are less than the gross accounts receivable.

d. All of these answer choices are correct.

194. Factoring arrangements

a. are ways to accelerate receivable collections.

b. involve no commissions or service charges because the factor is guaranteed

collections on the due date.

c. are generally used by businesses that are insolvent.

d. are mainly used in the textile and furniture industries.

195. ABC Company accepted a national credit card for a $9,000 purchase. The cost of the

goods sold is $7,200. The credit card company charges a 3% fee. What is the impact of

this transaction on net operating income?

a. Increase by $1,746.

b. Increase by $1,800.

c. Increase by $1,530.

d. Increase by $8,730.

196. XYZ Company accepted a national credit card for a $10,000 purchase. The cost of the

goods sold is $8,000. The credit card company charges a 3% fee. What is the impact of

this transaction on net operating income?

a. Increase by $1,940.

b. Increase by $2,000.

c. Increase by $1,700.

d. Increase by $9,700.

Reporting and Analyzing Receivables

8-43

197. A company sells $800,000 of accounts receivable to a factor for cash less a 2% service

charge. The entry to record the sale should not include a

a. debit to Interest Expense for $16,000.

b. debit to Cash for $784,000.

c. debit to Service Charge Expense for $16,000.

d. credit to Accounts Receivable for $800,000.

198. The sale of receivables by a business

a. indicates that the business is in financial difficulty.

b. is generally the major revenue item on its income statement.

c. is an indication that the business is owned by a captive finance company.

d. can be a quick way to generate cash for operating needs.

199. If a retailer regularly sells its receivables to a factor, the service charge of the factor

should be classified as a(n)

a. selling expense.

b. interest expense.

c. other expense.

d. contra asset.

200. The sale or transfer of accounts receivable in order to raise funds is called

a. pledging.

b. factoring.

c. leasing.

d. collateralizing.

201. If a company sells its accounts receivables to a factor

a. the seller pays a commission to the factor.

b. the factor pays a commission to the seller.

c. there is a gain on the sale of the receivables.

d. the seller defers recognition of sales revenue until the account is collected.

202. A captive finance company refers to

a. a finance company that is owned by individuals who borrow money from the company.

b. finance companies that won’t allow early repayment of loans.

c. a company that is wholly owned by another company and provides financing to

purchasers of its owner company’s goods.

d. any company that issues a major credit card.

Test Bank for Financial Accounting: Tools for Business Decision Making, Eighth Edition

8-44

203. Receivables might be sold to

a. lengthen the cash-to-cash operating cycle.

b. take advantage of deep discounts on the cash realizable value of receivables.

c. generate cash quickly.

d. finance companies at an amount greater than cash realizable value.

204. A company regularly sells its receivables to a factor who assesses a 2% service charge

on the amount of receivables purchased. Which of the following statements is true for the

seller of the receivables?

a. The loss section of the income statement will increase each time receivables are sold.

b. The credit to Accounts Receivable is less than the debit to Cash when the accounts

are sold.

c. Selling expenses will increase each time accounts are sold.

d. The other expenses section of the income statement will increase each time accounts

are sold.

205. Gipson Furniture factors $700,000 of receivables to Kwik Factors, Inc. Kwik Factors

assesses a 3% service charge on the amount of receivables sold. Gipson Furniture

factors its receivables regularly with Kwik Factors. What journal entry does Gipson make

when factoring these receivables?

a. Cash 679,000

Loss on Sale of Receivables 21,000

Accounts Receivable 700,000

b. Cash 679,000

Accounts Receivable 679,000

c. Cash 500,000

Accounts Receivable 679,000

Gain on Sale of Receivables 21,000

d. Cash 679,000

Service Charge Expense 21,000

Accounts Receivable 700,000

206. When customers make purchases with a national credit card, the retailer

a. is responsible for maintaining customer accounts.

b. is not involved in the collection process.

c. absorbs any losses from uncollectible accounts.

d. receives cash equal to the full price of the merchandise sold from the credit card

company.

Reporting and Analyzing Receivables

8-45

207. On April 5 Donna’s Boutique accepted a Visa card for a $750 purchase. Visa charges a

2% service fee. The entry to record this transaction would include a

a. credit to Cash of $735.

b. debit to Cash of $750.

c. debit to Service Charge Expense of $15.

d. credit to Service Charge Expense of $15.

208. Schofield Retailers accepted $40,000 of Silver Bank MasterCard credit card charges for

merchandise sold on August 1. Silver Bank charges 4% for its credit card use. The entry

to record this transaction by Schofield Retailers will include a credit to Sales Revenue of

$40,000 and a debit(s) to

a. Cash for $38,400 and Service Charge Expense for $1,600.

b. Accounts receivable for $38,400 and Service Charge Expense for $2,400.

c. Cash for $40,000.

d. Accounts Receivable for $40,000.

209. The retailer considers Visa and MasterCard sales as

a. cash sales.

b. promissory sales.

c. credit sales.

d. contingent sales.

Test Bank for Financial Accounting: Tools for Business Decision Making, Eighth Edition

FOR INSTRUCTOR USE ONLY

8-46

Reporting and Analyzing Receivables

FOR INSTRUCTOR USE ONLY

8-47

BRIEF EXERCISES

Be. 210

Presented below are various receivable transactions entered into by Renner Tool Company.

Indicate whether the receivables are reported as accounts receivable, notes receivable, or other

receivables on the balance sheet.

a. Advanced $1,000 to a trusted employee.

b. Accepted a $2,000 promissory note from a customer as payment on account.

c. Determined that a $10,000 income tax refund is due from the IRS.

d. Sold goods to a customer on account for $5,000.

e. Recorded $500 accrued interest on a note receivable due next year.

f. Loaned a company officer $4,000.

Be. 211

Finney had the following transactions during March 2017.

1. Finney sold and delivered $14,000 of merchandise to LJ Enterprises, terms 2/10, n30.

2. LJ Enterprises also ordered an additional $5,000 worth of goods on the last day of the month.

3. Finney lent $1,000 to its company president who promised to repay the loan on the 15th day of

the next month.

4. Finney sold old storage sheds to Alt Traders on 3/31. Alt Traders gave a $2,500 promissory

note to Finney agreeing to pay for the sheds in 3 months.

5. Other current assets totaled $50,000.

Finney received no cash arising from the above transactions during March. Based only on the

above transactions, and ingnoring beginning balances, compute the percentage accounts

receivable is of the total current assets as of month end.

Test Bank for Financial Accounting: Tools for Business Decision Making, Eighth Edition

FOR INSTRUCTOR USE ONLY

8-48

Be. 212

The following are sales of The Holiday Store during February. The Store sells seasonal holiday

items.

2/3 Sold 50 heart balloons for $5 cash each.

2/8 Sold 100 boxes of chocolates at $10 each, terms 2/10, n/30. Collected within the discount

period.

2/10 Sold 50 heart necklaces for $25 each with no discount. Have not collected as of month end.

2/14 Sold 100 bouquets of roses at $30 per bouquet. Half the sales were on account. By month

end, 75% of the credit sales were collected.

2/27 Sold 20 leftover heart necklaces to a discount store for $15 each on credit.

2/28 Sold a display cabinet at a swap meet for $100 on account.

Determine the balance in Accounts Receivable at 2/28.

Be. 213

Prepare journal entries to record the following transactions entered into by the Castagno

Company:

2017

Nov. 1 Sold merchandise on account to Mercer, Inc., for $18,000, terms 2/10, n/30.

Nov. 5 Mercer, Inc., returned merchandise worth $1,000.

Nov. 9 Received payment in full from Mercer, Inc.

Reporting and Analyzing Receivables

FOR INSTRUCTOR USE ONLY

8-49

Be. 214

Assuming that the allowance method is being used, prepare general journal entries without

explanations to record the following transactions.

January 1 Sold merchandise to Mary Baden for $500 on account.

February 1 Received $300 from Baden.

July 1 Wrote off Baden’s account as uncollectible.

September 1 Unexpectedly received payment in full from Baden.

(To record collection on account)

Be. 215

The ledger of the Ramirez Company at the end of the current year shows Accounts Receivable of

$200,000.

Instructions

(a) If Allowance for Doubtful Accounts has a credit balance of $3,000 in the trial balance and

bad debts are expected to be 8% of accounts receivable, journalize the adjusting entry for

end of the period. (Show all calculations.)

(b) If Allowance for Doubtful Accounts has a debit balance of $3,000 in the trial balance and bad

debts are expected to be 8% of accounts receivable, journalize the adjusting entry for end of

the period. (Show all calculations.)

Test Bank for Financial Accounting: Tools for Business Decision Making, Eighth Edition

FOR INSTRUCTOR USE ONLY

8-50

Be. 216

Benson Products uses the allowance method in estimating uncollectible accounts. On December

31, 2017, the balance in Accounts Receivable was $650,000. An aging analysis of the accounts

receivable indicated that $29,500 in accounts are expected to be uncollectible.

Prepare the adjusting entry to record estimated bad debts expense using the percentage of

receivables basis under each of the following independent assumptions:

(a) Allowance for Doubtful Accounts has a credit balance of $3,000 before adjustment.

(b) Allowance for Doubtful Accounts has a debit balance of $830 before adjustment.

Be. 217

Strickman Company uses the allowance method for estimating uncollectible accounts. Prepare

journal entries to record the following transactions:

January 5 Sold merchandise to Sue Land for $1,800, terms n/15.

April 15 Received $400 from Sue Land on account.

August 21 Wrote off as uncollectible the balance of the Sue Land account when she

declared bankruptcy.

October 5 Unexpectedly received a check for $650 from Sue Land.

Reporting and Analyzing Receivables

FOR INSTRUCTOR USE ONLY

8-51

Be. 218

Compute the maturity value as indicated for each of the following notes receivable.

1. A $9,000, 6%, 3-month note dated July 20.

Maturity value $____________.

2. A $16,000, 9%, 150-day note dated August 5.

Maturity value $____________.

Be. 219

Determine the interest on the following notes:

(a) $5,000 at 6% for 90 days.

(b) $800 at 9% for 5 months.

(c) $6,000 at 8% for 60 days

(d) $1,600 at 7% for 6 months

Be. 220

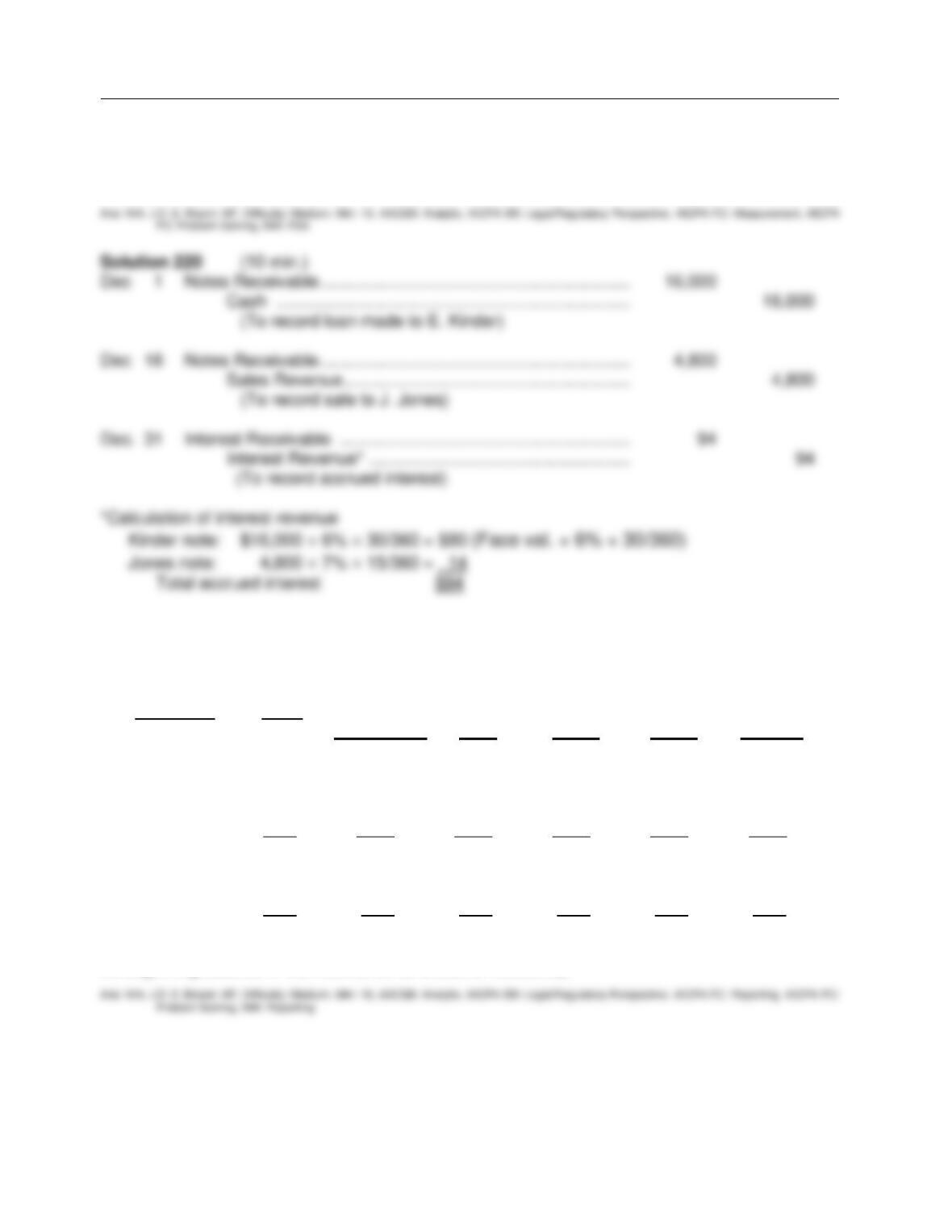

Trent Distributors has the following transactions related to notes receivable during the last two

months of the year.

Dec. 1 Loaned $16,000 cash to E. Kinder on a 1-year, 6% note.

16 Sold goods to J. Jones, receiving a $4,800, 60-day, 7% note.

31 Accrued interest revenue on all notes receivable.

Test Bank for Financial Accounting: Tools for Business Decision Making, Eighth Edition

FOR INSTRUCTOR USE ONLY

8-52

Be. 220 (cont.)

Instructions

Journalize the transactions for Trent Distributors.

Be. 221

Merry Co. sells Christmas angels. Merry determines that at the end of December, they have the

following aging schedule of Accounts Receivable:

Customer Total Number of Days Past Due

Not yet due 1–30 31–60 61–90 Over 90

K. Brant $500 $300 $200

D. Eaton 300 100 200

S Klein 150 50 100

C. Sheen 200 200

? 300 300 250 200 100

% uncollectible 1% 5% 10% 25% 50%

Total Estimated Uncollectible

Amounts ? ? ? ? ? ?

Compute the net receivables based on the above information at the end of December (There was

no beginning balance in the Allowance for Doubtful Accounts).

Reporting and Analyzing Receivables

FOR INSTRUCTOR USE ONLY

8-53

Be. 222

The following data exists for Mather Company.

2017 2016

Accounts Receivable $ 80,000 $ 70,000

Net Sales 560,000 410,000

Calculate the accounts receivable turnover and the average collection period for accounts

receivable in days for 2017.

Be. 223

Donaldson Company has the following accounts in its general ledger at July 31: Accounts

Receivable $40,000 and Allowance for Doubtful Accounts $2,500. During August, the following

transactions occurred.

Oct. 15 Sold $30,000 of accounts receivable to Fast Factors, Inc. who assesses a 3% finance

charge.

25 Made sales of $900 on Visa credit cards. The credit card service charge is 2%.

Instructions

Journalize the transactions.

Test Bank for Financial Accounting: Tools for Business Decision Making, Eighth Edition

FOR INSTRUCTOR USE ONLY

8-54

EXERCISES

Ex. 224

On January 10 Donna Stark uses her Baver Co. credit card to purchase merchandise from Baver

Co. for $2,600. On February 10, she is billed for the amount due of $2,600. On February 12 Stark

pays $1,600 on the balance due. On March 10 Stark is billed for the amount due, including

interest at 1% per month on the unpaid balance as of February 12.

Instructions

Prepare the entries on Baver Co.’s books related to the transactions that occurred on January 10,

February 12, and March 10.

Ex. 225

At the beginning of the current period, Emler Corp. had balances in Accounts Receivable of

$200,000 and in Allowance for Doubtful Accounts of $9,000 (credit). During the period, it had net

credit sales of $650,000 and collections of $590,000. It wrote off as uncollectible accounts

receivable of $5,000. However, a $3,000 account previously written off as uncollectible was

recovered before the end of the current period. Uncollectible accounts are estimated to total

$20,000 at the end of the period.

Instructions

(a) Prepare the entries to record sales and collections during the period.

(b) Prepare the entry to record the write-off of uncollectible accounts during the period.

(c) Prepare the entries to record the recovery of the uncollectible account during the period.

(d) Prepare the entry to record bad debts expense for the period.

(e) Determine the ending balances in Accounts Receivable and Allowance for Doubtful

Accounts.

(f) Calculate the net realizable value of the receivables at the end of the period.

Reporting and Analyzing Receivables

FOR INSTRUCTOR USE ONLY

8-55

Ex. 226

The December 31, 2016 balance sheet of the Kramer Company had Accounts Receivable of

$650,000 and a credit balance in Allowance for Doubtful Accounts of $33,000. During 2017, the

following transactions occurred: sales on account $1,550,000; sales returns and allowances,

$100,000; collections from customers, $1,250,000; accounts written off, $35,000; previously

written off accounts of $8,000 were collected.

Instructions

(a) Journalize the 2017 transactions.

(b) If the company uses the percentage of receivables basis to estimate bad debt expense and

determines that uncollectible accounts are expected to be 6% of accounts receivable, what is

the adjusting entry at December 31, 2017?

Test Bank for Financial Accounting: Tools for Business Decision Making, Eighth Edition

FOR INSTRUCTOR USE ONLY

8-56

Reporting and Analyzing Receivables

FOR INSTRUCTOR USE ONLY

8-57

Ex. 227

An inexperienced accountant made the following entries. In each case, the explanation to the

entry is correct.

Dec. 17 Cash ……………………………………………………………………….. 2,940

Sales Discounts ………………………………………………………….. 60

Accounts Receivable ……………………………………………. 3,000

(To record collection of 12/4 sales, terms 2/10, n/30)

27 Cash ……………………………………………………………………….. 1,200

Bad Debt Expense ………………………………………………. 1,200

(Collection of account previously written off as

uncollectible under allowance method)

31 Bad Debt Expense ………………………………………………………. 1,800

Allowance for Doubtful Accounts ……………………………. 1,800

(To recognize estimated bad debts based on 3% of

accounts receivable of $600,000)

Instructions

Prepare the correcting entries.

Test Bank for Financial Accounting: Tools for Business Decision Making, Eighth Edition

FOR INSTRUCTOR USE ONLY

8-58

Ex. 228

Prepare journal entries to record the following transactions entered into by the Merando

Company:

2016

June 1 Received a $10,000, 6%, 1-year note from Dan Gore as full payment on his account.

Nov. 1 Sold merchandise on account to Barlow, Inc., for $14,000, terms 2/10, n/30.

Nov. 5 Barlow, Inc., returned merchandise worth $1,000.

Nov. 9 Received payment in full from Barlow, Inc.

Dec. 31 Accrued interest on Gore‘s note.

2017

June 1 Dan Gore honored his promissory note by sending the face amount plus interest.

Reporting and Analyzing Receivables

FOR INSTRUCTOR USE ONLY

8-59

Ex. 229

The Garvey Sign Company uses the allowance method in accounting for uncollectible accounts.

Past experience indicates that 6% of accounts receivable will eventually be uncollectible.

Selected account balances at December 31, 2016, and December 31, 2017, appear below:

12/31/2016 12/31/2017

Net Credit Sales $400,000 $500,000

Accounts Receivable 80,000 100,000

Allowance for Doubtful Accounts 4,000 ?

Instructions

(a) Record the following events in 2017.

Aug. 10 Determined that the account of Kurt West for $900 is uncollectible.

Sept. 12 Determined that the account of Jill Lynch for $3,000 is uncollectible.

Oct. 10 Received a check for $300 as payment on account from Kurt West, whose

account had previously been written off as uncollectible.

(b) Prepare the adjusting journal entry to record the bad debt provision for the year ended

December 31, 2017.

(c) What is the balance of Allowance for Doubtful Accounts at December 31, 2017?

Test Bank for Financial Accounting: Tools for Business Decision Making, Eighth Edition

FOR INSTRUCTOR USE ONLY

8-60

Ex. 230

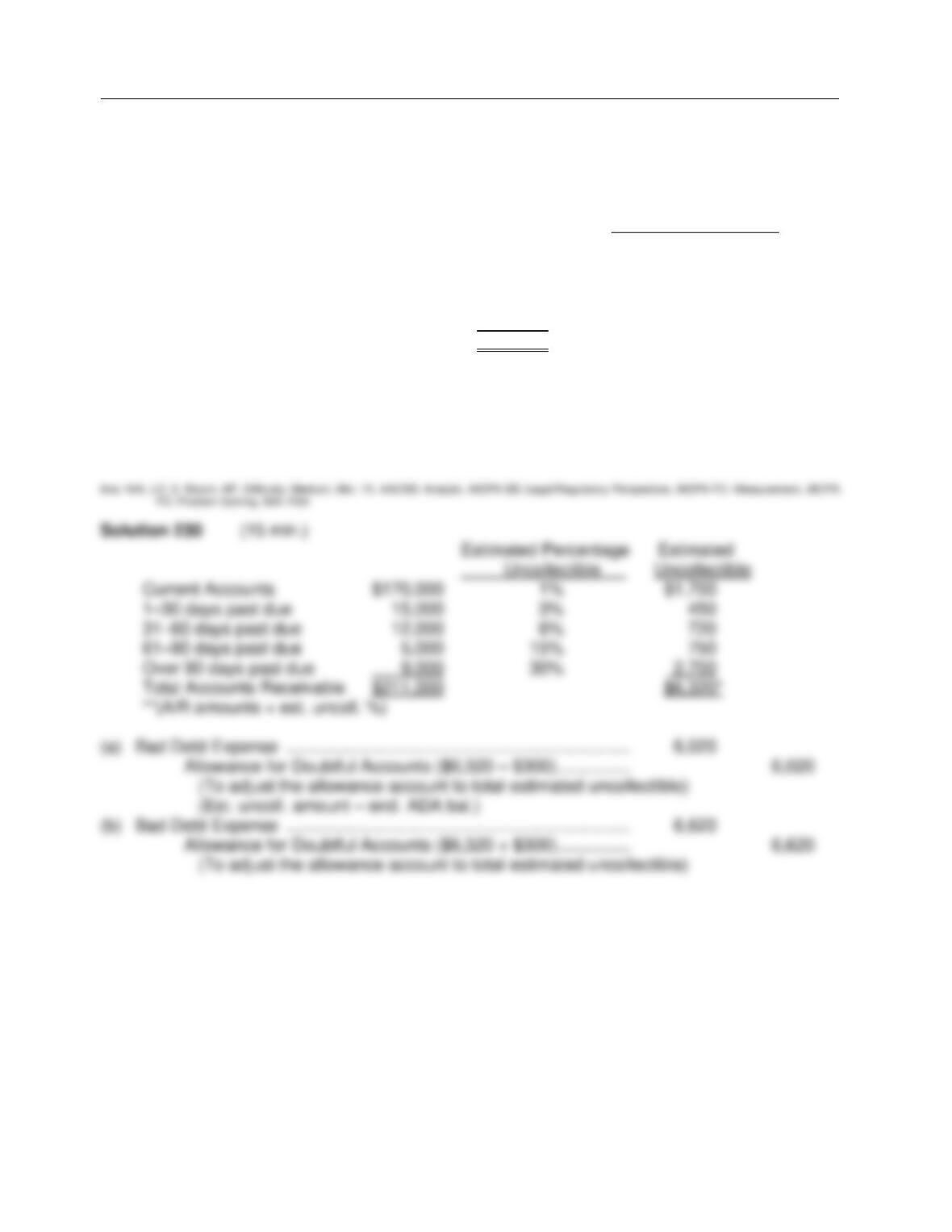

Erickson Company had a $300 credit balance in Allowance for Doubtful Accounts at December

31, 2017, before the current year’s provision for uncollectible accounts. An aging of the accounts

receivable revealed the following:

Estimated Percentage

Uncollectible

Current Accounts $170,000 1%

1–30 days past due 15,000 3%

31–60 days past due 12,000 6%

61–90 days past due 5,000 15%

Over 90 days past due 9,000 30%

Total Accounts Receivable $211,000

Instructions

(a) Prepare the adjusting entry on December 31, 2017, to recognize bad debts expense.

(b) Assume the same facts as above except that the Allowance for Doubtful Accounts account

had a $300 debit balance before the current year’s provision for uncollectible accounts.

Prepare the adjusting entry for the current year‘s provision for uncollectible accounts.