170. In Exhibit 7-13, AFC is shown by the graph labeled:

a.

I.

b.

II.

c.

III.

d.

IV.

e.

V.

171. In Exhibit 7-13, ATC is shown by the graph labeled:

a.

I.

b.

II.

c.

III.

d.

IV.

e.

V.

172. Which of the following must be true if average total cost is rising?

a.

Average fixed cost must be rising.

b.

Total fixed cost must be rising.

c.

Average variable cost must be falling.

d.

Marginal cost must be greater than average total cost.

173. Which of the following statements is true?

a.

The law of diminishing returns states that beyond some point the marginal product of a

variable resource continues to rise.

b.

The marginal product is the change in total output by adding one additional unit of a fixed

input.

c.

Fixed costs are costs which vary with the output level.

d.

When marginal productivity of a variable input is falling then marginal costs of production

must be rising.

e.

When marginal cost is below average cost, average cost rises; when marginal cost is above

average cost, average cost falls.

174. Which of the following is true at the point where diminishing returns set in?

a.

Both marginal product and marginal cost are at a maximum.

b.

Both marginal product and marginal cost are at a minimum.

c.

Marginal product is at a maximum and marginal cost at a minimum.

d.

Marginal product is at a minimum and marginal cost at a maximum.

175. If total cost is $1,000 when output is zero, and total cost is $1,200 when output is one, and total cost is

$1,500 when output is two, then which of the following is true?

a.

Total fixed cost is $1,500.

b.

The marginal cost of producing the first unit of output is $1,200.

c.

The marginal cost of producing the second unit of output is $300.

d.

The average fixed cost is $750 when two units of output are produced.

176. Which of the following best describes marginal cost?

a.

The change in total cost when one additional unit of output is produced.

b.

Total cost divided by the quantity of output produced.

c.

Total variable cost divided by the quantity of output produced.

d.

Total fixed cost divided by the quantity of output produced.

e.

Costs that do not vary as output varies, and that must be paid even if output is zero.

177. In the long run, total fixed cost will:

a.

remain constant.

c.

decrease.

b.

increase.

d.

not exist by definition.

178. For a typical firm, the long-run average total cost curve:

a.

is tangent to the minimum point of each possible short-run average total cost curves.

b.

is tangent to each possible short-run average total cost curve at one point.

c.

intersects each possible short-run average total cost curve at two points.

d.

passes through the minimum points of all possible short-run average total cost curves.

179. Each potential short-run average total cost curve is tangent to the long-run average cost curve at:

a.

the level of output that minimizes short-run average total cost.

b.

the minimum point of the average total cost curve.

c.

the minimum point of the long-run average cost curve.

d.

a single point on the short-run average total cost curve.

180. When the curve that envelops the series of possible short-run average total cost curves is horizontal,

this means that there are:

a.

economies of scale.

b.

diseconomies of scale.

c.

constant returns to scale.

d.

diminishing returns.

e.

some fixed factors of production.

181. If the minimum points of all the possible short-run average total cost curves become successively

lower as quantity of output increases, then:

a.

the firm should try to produce less output.

b.

total fixed costs are constant along the LRAC curve.

c.

there are economies of scale.

d.

the firm is probably having significant management problems.

e.

when output is doubled, total costs are doubled.

182. A downward-sloping portion of a long-run average total cost curve is the result of:

a.

economies of scale.

c.

diminishing returns.

b.

diseconomies of scale.

d.

the existence of fixed resources.

183. In the long run, firms in many industries often experience a falling average total cost curve as a result

of:

a.

gains through trade.

c.

economies of scale.

b.

increasing marginal returns.

d.

lower fixed costs.

184. A large aircraft manufacturer, like Boeing, may have a cost advantage over a new smaller

manufacturer because of:

a.

diseconomies of scale.

b.

economies of scale.

c.

diminishing returns to a fixed factor of production.

d.

the principal agent problem is generally less severe for larger firms.

185. Long-run economies of scale exist when the long-run average cost curve:

a.

rises.

c.

falls.

b.

remains constant.

d.

does not exist.

186. Long-run economies of scale exist over the range of output for which the long-run average cost curve:

a.

is constant.

c.

is rising.

b.

is falling.

d.

does not exist.

187. Economies of scale are created by greater efficiency of capital and by:

a.

longer chains of command in management.

b.

better wages for labor.

c.

smaller plant sizes.

d.

increased specialization of labor.

188. Economies of scale imply that within some range one can increase the size of operation and:

a.

total cost will decrease.

b.

fixed cost will decrease.

c.

average total cost will decrease.

d.

average total cost will increase.

e.

average variable cost will decrease.

189. The decreasing portion of a firm’s long run average cost curve is attributable to:

a.

diminishing returns to scale.

b.

increasing marginal cost.

c.

economies of scale.

d.

diseconomies of scale.

e.

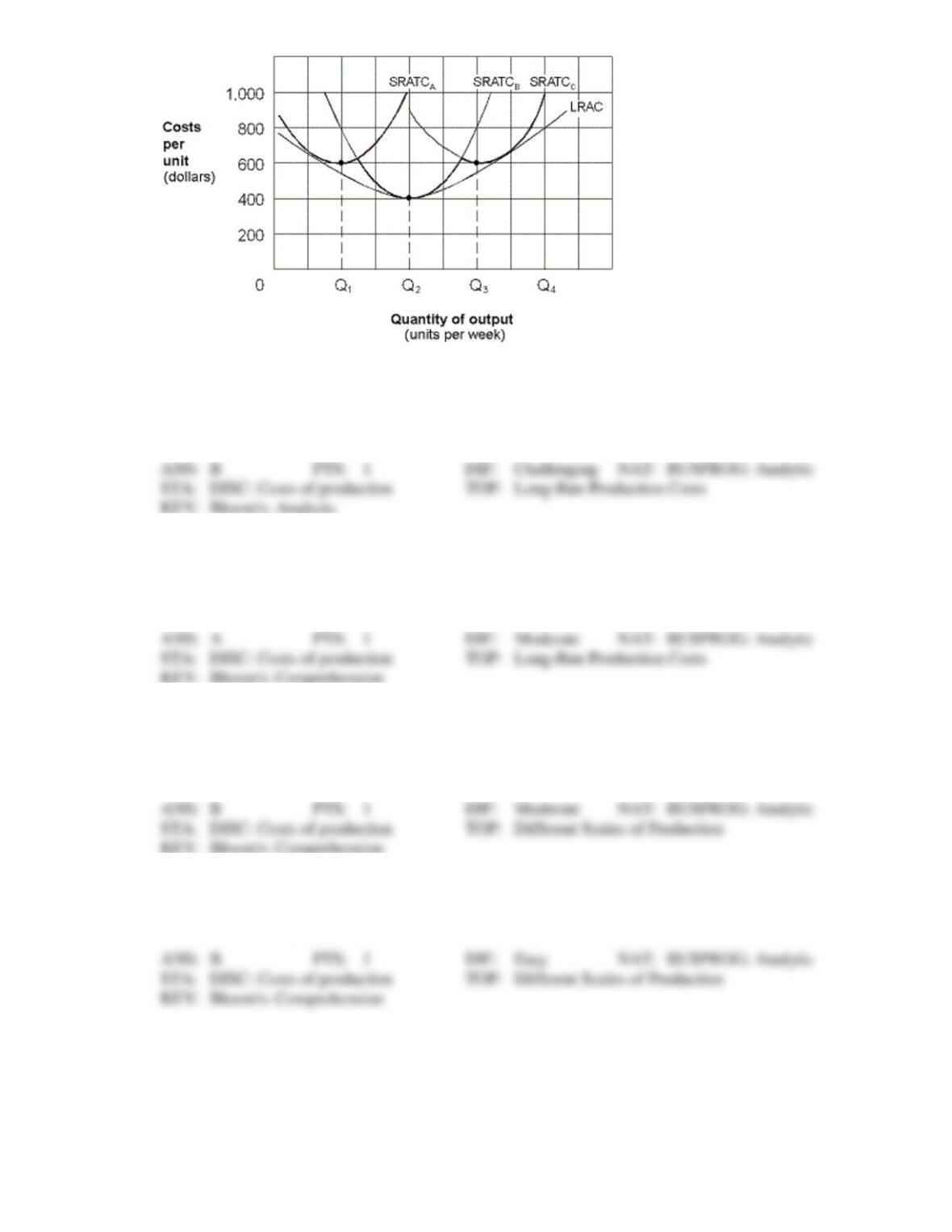

constant returns to scale.

190. Economies of scale can be caused by all of the following except:

a.

price discounts for large scale purchases.

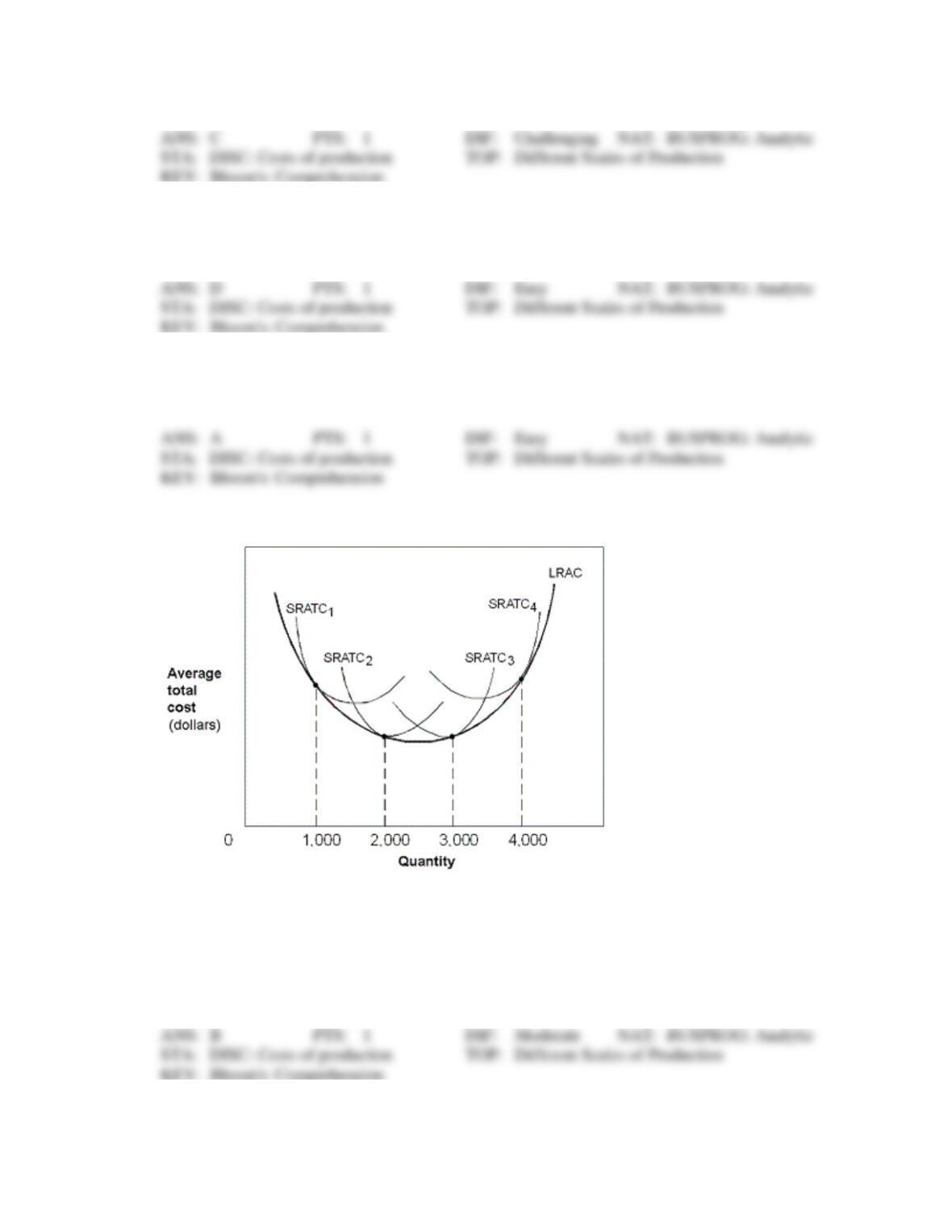

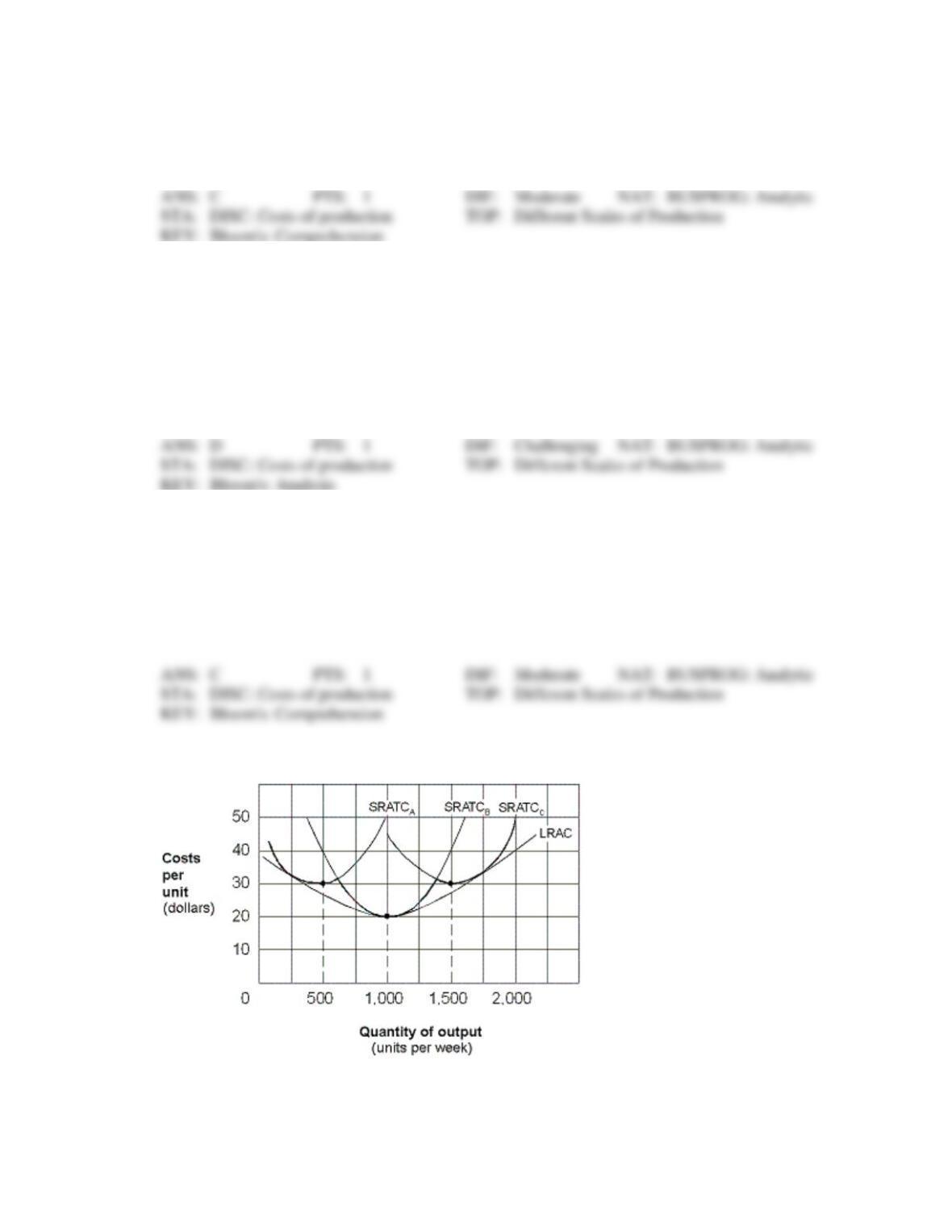

b.

labor specialization.

c.

use of more productive equipment.

d.

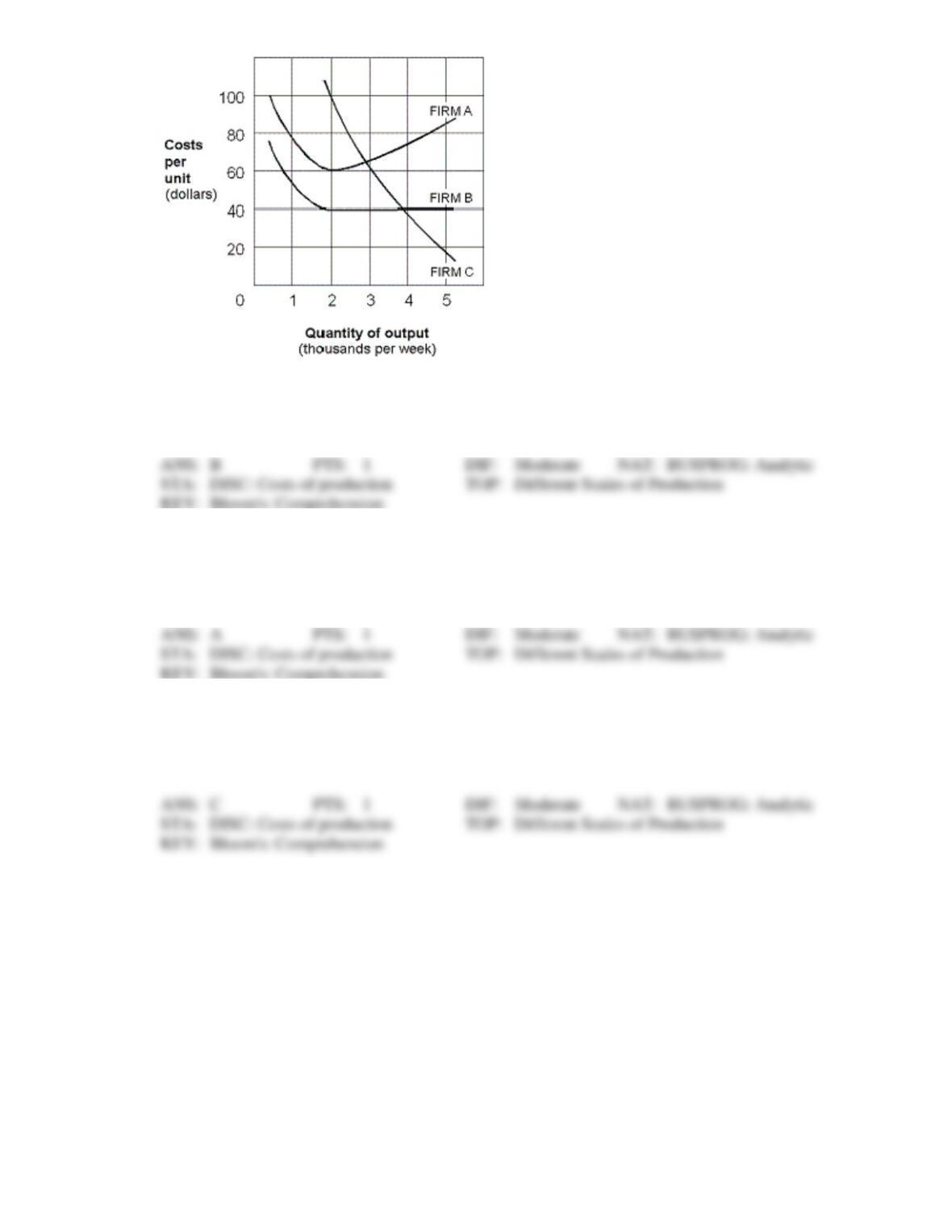

increases in the firm’s average total cost.

e.

more cost-efficient methods of marketing.

191. Since the 1980s, Wal-Mart stores have appeared in almost every community in America. Wal-Mart

buys their goods in large quantities and therefore at cheaper prices. Wal-Mart also locates its stores

where land prices are low, usually outside of the community business district. Many customers shop at

Wal-Mart because of low prices and free parking. Local retailers, like the neighborhood drug store,

often go out of business because they lose customers. This story demonstrates that:

a.

consumers are boycotting local retailers.

b.

Wal-Mart engages in illegal acts of monopolization.

c.

there are diseconomies of scale in retail sales.

d.

there are economies of scale in retail sales.

e.

Wal-Mart is managed by ruthless business people.

192. Which of the following is not a source of economies of scale?

a.

Division and specialization of labor.

b.

Increase in output.

c.

More efficient use of capital.

d.

All of the above.

e.

Centralized marketing.

193. A car leasing company that expands its size by buying its competitors may run the risk of increasing

production cost per unit due to:

a.

diseconomies of scale.

b.

economies of scale.

c.

diminishing returns.

d.

greater use of large-volume purchases.

194. In the long run, a firm might experience rising per-unit cost due to:

a.

economies of scale.

b.

diseconomies of scale.

c.

the law of supply.

d.

the law of diminishing marginal returns.

195. Diseconomies of scale exist over the range of output for which the long-run average cost curve is:

a.

constant.

c.

rising.

b.

falling.

d.

subject to diminishing returns.

196. Diseconomies of scale exist over the range of output for which the long-run average cost curve is:

a.

constant.

c.

rising.

b.

falling.

d.

none of these.

197. If a firm enlarges its factory size and realizes higher average (per unit) costs of production then:

a.

it has experienced economies of scale.

b.

it has experienced diseconomies of scale.

c.

it has experienced constant returns to scale.

d.

the long-run average cost curve slopes downward.

e.

the long-run average cost curve shifts upward.

198. The primary source of scale diseconomies appears to be:

a.

a firm’s inability to acquire quality resources.

b.

too little demand for the firm’s product.

c.

consumers who resist dealing with large firms.

d.

division of labor.

e.

the organizational difficulties of managing an ever larger enterprise.

199. Diseconomies of scale exist for all of the following reasons except:

a.

bureaucratic inefficiencies.

b.

management problems.

c.

failures in information flows.

d.

firm size is too small.

e.

organizational problems.

200. Suppose there is a technology to produce Grendels such that there are diseconomies of scale after the

first unit is produced. There are both fixed (a physical plant called a lair) and variable (food that grows

in lairs) costs of production. Which statement is true?

a.

b and d.

b.

Producing multiple units increases the average fixed cost.

c.

There will be no more than one firm in this industry.

d.

It is cheaper to make five Grendels by buying five lairs and producing one Grendel in each

lair than it is to produce five Grendels in one lair.

e.

This is an impossible situation.

201. If a firm’s long-run average cost curve is rising, it is experiencing:

a.

a constant return to scale.

c.

diseconomies of scale.

b.

economies of scale.

d.

none of these.

202. Constant returns to scale exist over the range of output for which the long-run average cost is:

a.

neither rising or falling.

c.

rising.

b.

falling.

d.

none of these.

203. Constant returns to scale cause the long-run average cost curve to be:

a.

horizontal.

c.

upward-sloping.

b.

vertical.

d.

downward-sloping.

Exhibit 7-14 Cost curves

204. In Exhibit 7-14, economies of scale only exist for output levels up to:

a.

1,000.

b.

2,000.

c.

3,000.

d.

4,000.

e.

greater than 4,000.

205. In Exhibit 7-14, constant returns to scale only exist for output levels between:

a.

0 and 1,000.

b.

1,000 and 2,000.

c.

2,000 and 3,000.

d.

3,000 and 4,000.

e.

4,000 and infinity.

206. In Exhibit 7-14, a firm finds that it is experiencing numerous managerial and information problems.

The position of its short- and long-run average total cost curves suggest that it is operating at a

production level:

a.

between 0 and 1,000.

b.

between 1,000 and 2,000.

c.

between 2,000 and 3,000.

d.

between 3,000 and 4,000.

e.

where it should shut down immediately.

207. In Exhibit 7-14, the U-shaped LRAC curve indicates which of the following as quantity increases from

0 to 4,000?

a.

Diseconomies of scale; constant returns to scale; economies of scale.

b.

Constant returns to scale; economies of scale; diseconomies of scale.

c.

Economies of scale; constant returns to scale; diseconomies of scale.

d.

Diseconomies of scale; economies of scale; constant returns to scale.

e.

Economies of scale; diseconomies of scale; constant returns to scale.

Exhibit 7-15 Long-run average cost

208. In Exhibit 7-15, short-run average total cost, short-run marginal cost, and long-run average cost are all

equal at which level of output per week?

a.

500 units.

c.

1,500 units.

b.

1,000 units.

d.

2,000 units.

209. If the firm represented in Exhibit 7-15 is operating with a plant whose size corresponds to short-run

average total cost curve A, the level of output that would minimize its short-run average total cost is:

a.

500 units per week.

c.

1,500 units per week.

b.

1,000 units per week.

d.

2,000 units per week.

210. Given the short-run average total cost curves in Exhibit 7-15, what level of output per week minimizes

average total cost?

a.

500 units.

c.

1,500 units.

b.

1,000 units.

d.

2,000 units.

211. In Exhibit 7-15, economies of scale exist up to:

a.

500 units of output per week.

c.

1,500 units of output.

b.

1,000 units of output per week.

d.

2,000 units of output.

212. In Exhibit 7-15, diseconomies of scale are shown in the range of:

a.

0 to 500 units per week.

c.

1,000 to 2,000 units per week.

b.

500 to 1,000 units per week.

d.

zero per week.

Exhibit 7-16 Long-run average cost curves

213. In Exhibit 7-16, which firm’s long-run average cost curve experiences constant returns to scale?

a.

Firm A.

c.

Firm C.

b.

Firm B.

d.

Firms A and C.

214. Which firm in Exhibit 7-16 displays a long-run average cost curve with diseconomies beginning at

2,000 units of output per week?

a.

Firm A.

c.

Firm C.

b.

Firm B.

d.

Firms A and C.

215. Which firm in Exhibit 7-16 displays a long-run average cost curve with economies of scale throughout

the range of output shown?

a.

Firm A.

c.

Firm C.

b.

Firm B.

d.

Firms A and B.

Exhibit 7-17 Long-run average cost curve

216. In Exhibit 7-17, short-run average total cost, short-run marginal cost, and long-run average cost are all

equal at which level of output per week?

a.

Q1 units.

c.

Q3 units.

b.

Q2 units.

d.

Q4 units.

217. If the firm represented in Exhibit 7-17 is operating with a plant whose size corresponds to short-run

average total cost curve A, the level of output that would minimize its short-run average total cost is:

a.

Q1 units per week.

c.

Q3 units per week.

b.

Q2 units per week.

d.

Q4 units per week.

218. Given the short-run average total cost curves in Exhibit 7-17, what level of output per week minimizes

average total cost?

a.

Q1 units.

c.

Q3 units.

b.

Q2 units.

d.

Q4 units.

219. In Exhibit 7-17, economies of scale exist up to:

a.

Q1 units of output per week.

c.

Q3 units of output.

b.

Q2 units of output per week.

d.

Q4 units of output.

TRUE/FALSE

1. Economic profit equals accounting profit minus implicit costs.

2. If economic profit is zero, then a normal profit is earned.

3. Suppose a firm earns an accounting profit. This means the firm also earns a positive economic profit.

4. Economic profit equals accounting profit minus implicit costs.

5. Suppose Joe Rich owns his own company and does not pay himself a salary. This means the salary he

could have earned in alternative employment is considered an implicit cost for the firm.

6. If marginal product is at a maximum, then marginal cost is at a minimum.

7. In the short-run, total fixed costs always exceed total variable costs.

8. In the long run, all costs are fixed costs.

9. All of a firm’s inputs are considered to be variable in the long run.

10. In the long run, all costs are considered variable.

11. A firm’s marginal product curve slopes downward throughout its length.

12. The marginal product curve rises when the marginal cost curve rises.

13. For most firms, the costs of energy and raw materials will be total fixed costs.

14. A firm’s average fixed cost curve can never be U-shaped, even if its other average cost curves are U-

shaped.

15. The vertical distance between the average total cost curve and the average variable cost curve at any

given output level equals average fixed cost at that particular output level.

16. If a firm’s average variable cost curve is rising, its marginal cost must exceed its average variable cost.

17. Marginal cost is calculated by dividing the change in total cost by the change in total output.

18. If the total variable cost of producing 5 units of output is $10 and the total variable cost of producing 6

units is $15, the marginal cost of producing a sixth unit is $5.

19. The marginal product curve rises when the marginal cost curve rises.

20. The law of diminishing returns causes a firm’s short-run marginal cost curve to be s-shaped.

21. If a firm’s marginal cost exceeds its average cost, then its average cost must be rising.

22. Each short-run average total cost curve is tangent at its lowest point to the long-run average cost curve.

23. Economies of scale exist over all ranges of output for which short-run average total cost exceeds long-

run average cost.

24. If a firm increases output and its average total cost rises, then the firm is experiencing economies of

scale.

25. The primary cause of diseconomies of scale is scarcity of machinery and capital.

26. Diseconomies of scale cause the short-run marginal cost curve to slope upwards.

27. Diseconomies of scale occur when high levels of output are produced in a short period of time.

ESSAY

1. What is the difference between economic and accounting profit? Why is a distinction between them

important?

2. Distinguish the short run from the long run. Generally, what causes costs of production to vary with

output in the short run? What generally causes costs of production to vary in the long run?

3. What are the seven short run cost calculations? How are they related?

4. Distinguish economies and diseconomies of scale. How can the extent to which economies and

diseconomies of scale explain the size and number of real world firms in an industry?