Chapter 7—Production Costs

MULTIPLE CHOICE

1. Which of the following is an explicit cost?

a.

The opportunity cost of an owner/entrepreneur’s time invested in the firm.

b.

The opportunity cost of the money the business owner/entrepreneur has invested in the

firm.

c.

The wages paid to workers.

d.

None of the above.

2. Explicit costs would include:

a.

rent.

b.

the interest loss of the business owner on money withdrawn from his/her saving account

and invested in the business.

c.

the loss of rent on a building the business owner owns and uses in his/her business.

d.

the opportunity costs of the business owner’s time.

e.

the use of tools owned by the business owner and dedicated to the business.

3. Unlike implicit costs, explicit costs:

a.

reflect opportunity costs.

b.

include the value of the owner’s time.

c.

are not included in the accounting statement of the firm.

d.

are actual cash payments.

e.

do not change with the output rate of the firm.

4. A young chef is considering opening his own sushi bar. To do so, he would have to quit his current

job, which pays $20,000 a year, and take over a store building that he owns and currently rents to his

brother for $6,000 a year. His expenses at the sushi bar would be $50,000 for food and $2,000 for gas

and electricity. What are his explicit costs?

a.

$26,000.

b.

$66,000.

c.

$78,000.

d.

$52,000.

e.

$72,000.

5. Which of the following is not an explicit cost?

a.

Salaries.

b.

Sales taxes.

c.

Utilities, such as gas and electricity.

d.

Insurance.

e.

The firm owner’s time.

6. Cash payments to a steel mill for steel used in production would be an example of:

a.

sunk costs.

b.

fixed costs.

c.

explicit costs.

d.

implicit costs.

e.

entrepreneurial costs.

7. Sam quits his job as an airline pilot and opens his own pilot training school. He was earning $40,000

as a pilot. He withdraws $10,000 from his savings where he was earning 6 percent interest and uses the

money in his new business. He uses a building he owns as a hanger and could rent it out for $5,000 per

year. He rents a computer for $1,200, buys office supplies for $500, rents an airplane for $6,000, pays

$1,300 for fuel and maintenance, and hires one worker for $30,000. Sam’s total revenue from pilot

training classes this year equaled $90,400. Sam’s explicit costs this year equals:

a.

$84,400.

b.

$39,000.

c.

$55,000.

d.

$45,600.

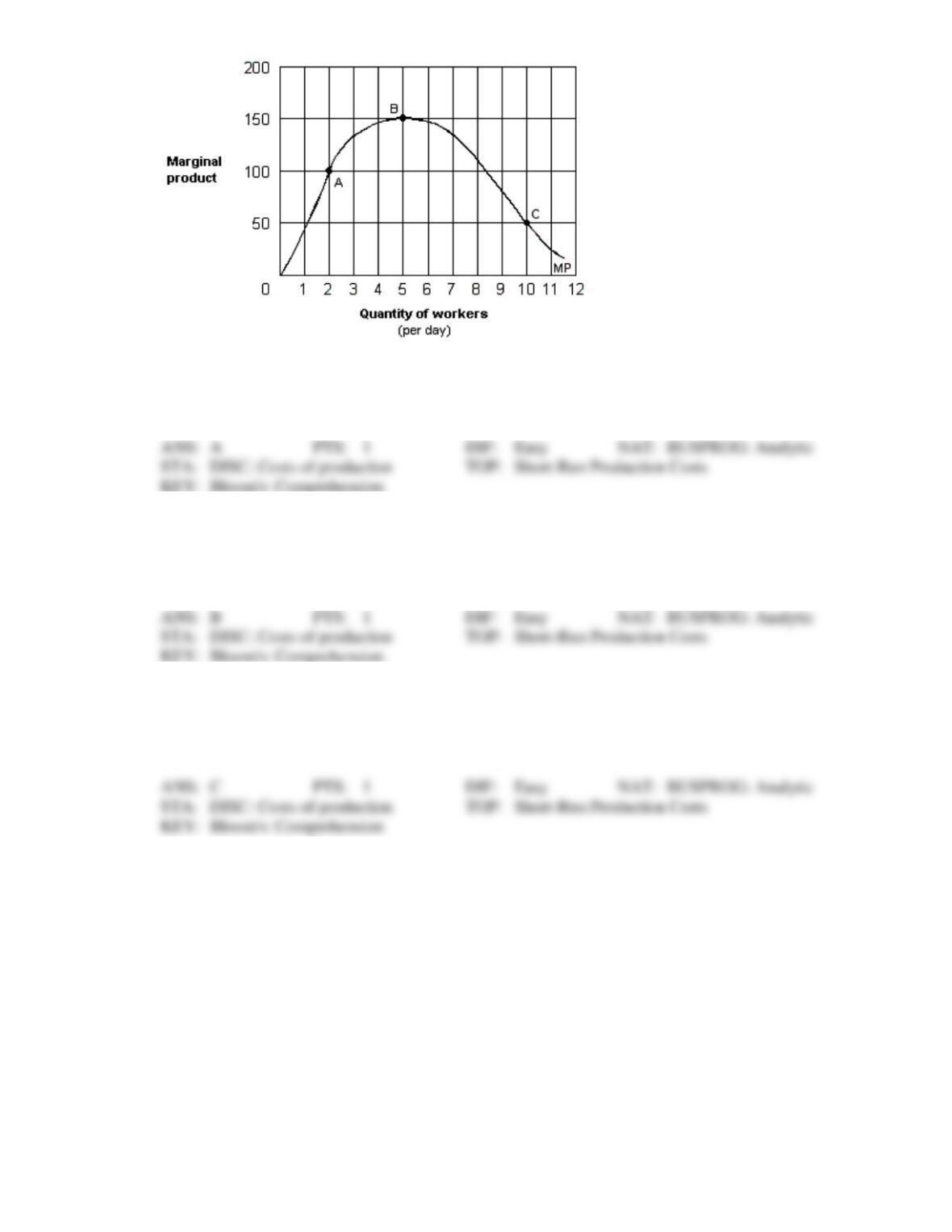

e.

$40,000.

8. Paul’s Plumbing is a small business that employs 12 people. Which of the following is the best

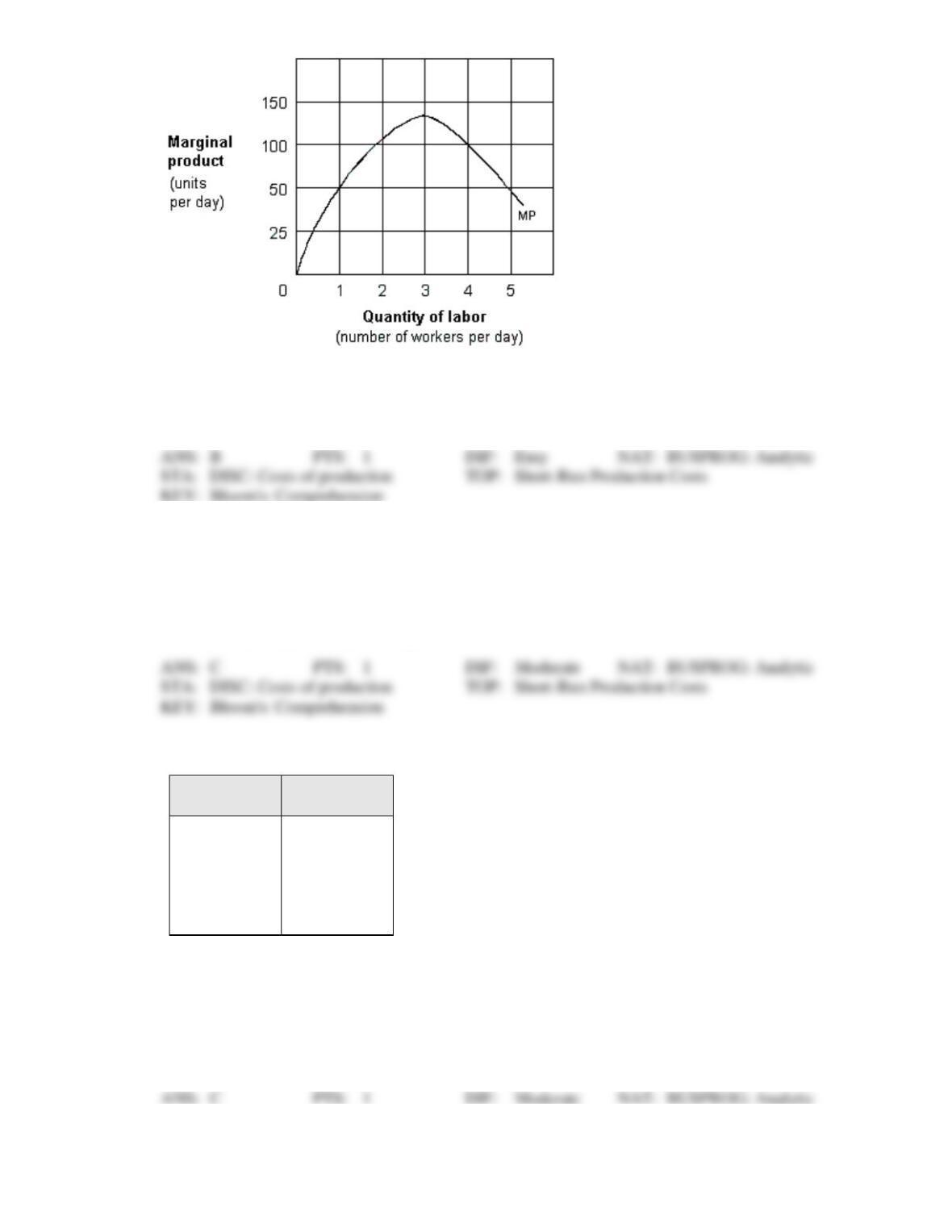

example of an implicit cost incurred by this firm?

a.

The tax payments on property owned by the firm.

b.

The wages paid to the 12 employees.

c.

The half of the payroll taxes on the wages of the 12 employees paid by the employers, but

not the half paid by the employees.

d.

The accounting services provided free of charge to the firm by Paul’s wife, who is an

accountant.

9. Which of the following would be considered an implicit cost?

a.

Health insurance of employees paid for by the firm

b.

The water bill of the firm

c.

The salaries paid to the managers of the firm

d.

Foregone rent on assets owned by the firm

10. The opportunity costs associated with the use of resources owned by a firm are:

a.

externalities.

c.

explicit costs.

b.

implicit costs.

d.

sunk costs.

11. Payments to nonowners of a firm are called:

a.

implicit costs.

c.

explicit costs.

b.

accounting costs.

d.

economic costs.

12. The amount of money that could have been made by renting a piece of land to be used for building an

office building instead of using the land for employee parking is a(n):

a.

implicit cost.

c.

explicit cost.

b.

accounting cost.

d.

pure economic cost.

13. Implicit costs are best thought of as:

a.

variable costs.

b.

marginal costs.

c.

accounting costs.

d.

opportunity costs.

e.

sunk costs.

14. Which of the following is an implicit cost of going to college?

a.

Tuition.

b.

Books.

c.

Lost income.

d.

Future income.

e.

Room and board.

15. Which of the following are implicit costs for a typical firm?

a.

Insurance costs.

b.

Electricity costs.

c.

Opportunity costs of capital owned and used by the firm.

d.

Cost of labor hired by the firm.

e.

The cost of raw materials.

16. A firm’s opportunity cost of using resources provided by the firm’s owners is called:

a.

sunk costs.

b.

fixed costs.

c.

explicit costs.

d.

implicit costs.

e.

entrepreneurial costs.

17. A young chef is considering opening his own sushi bar. To do so, he would have to quit his current

job, which pays $20,000 a year, and take over a store building that he owns and currently rents to his

brother for $6,000 a year. His expenses at the sushi bar would be $50,000, for food and $2,000 for gas

and electricity. What are his implicit costs?

a.

$26,000.

b.

$66,000.

c.

$78,000.

d.

$52,000.

e.

$72,000.

18. Two friends, Diane and Sam, own and run a bar. Diane tends bar on Monday, Wednesday, and Friday

and receives a wage in addition to tips. Sam tends bar on Tuesday, Thursday, and Saturday and

receives only tips. Which of the following represents an implicit cost of operating the bar?

a.

Diane’s wage.

b.

Sam’s time.

c.

Diane’s tips.

d.

Sam’s tips.

e.

Both Diane’s and Sam’s tips.

19. Implicit costs are:

a.

the opportunity costs of using resources owned by the entrepreneur in his/her own

business.

b.

payments the business owner must make on borrowed funds.

c.

costs which vary as the level of output varies.

d.

those payments the business owner makes in cash.

e.

the payments the business owner makes for public relations, such as donations to charity.

20. Sam quits his job as an airline pilot and opens his own pilot training school. He was earning $40,000

as a pilot. He withdraws $10,000 from his savings where he was earning 6 percent interest and uses the

money in his new business. He uses a building he owns as a hanger and could rent it out for $5,000 per

year. He rents a computer for $1,200, buys office supplies for $500, rents an airplane for $6,000, pays

$1,300 for fuel and maintenance, and hires one worker for $30,000. Sam’s total revenue from pilot

training classes equaled $90,400. Sam’s implicit costs for this year are equal to:

a.

$84,400.

b.

$39,000.

c.

$55,000.

d.

$45,600.

e.

$40,000.

21. The sum of the explicit and implicit costs incurred in the production process is called:

a.

fixed cost.

c.

marginal cost.

b.

sunk cost.

d.

total cost.

22. Which of the following is most likely to be true of economic and accounting profits?

a.

Economic profits are less than accounting profits.

b.

Accounting profits are less than economic profits.

c.

Economic profits plus accounting profits equal zero.

d.

Accounting profits minus economic profits equal zero.

23. Economic profit is:

a.

total revenues minus variable costs.

c.

total revenues minus explicit costs.

b.

total revenues minus private costs.

d.

total revenues minus total costs.

24. Suppose that a small business takes in monthly revenue of $100,000. Labor, rental, energy, and other

purchased input costs are $70,000. The owner/entrepreneur could earn $5,000 per month in another

job, and the owner/entrepreneur could get a return of $5,000 each month if she sold her business and

invested the net proceeds in a financial asset, such as a treasury bond. Which of the following correctly

describes her monthly economic profit?

a.

$100,000.

b.

$90,000.

c.

$70,000.

d.

$30,000.

e.

$20,000.

25. The difference between a firm’s total revenues and total costs when all explicit and implicit costs are

included is the firm’s:

a.

economic profit.

c.

opportunity cost of capital.

b.

accounting profit.

d.

long-run average total cost.

26. If a firm has total revenue of $200 million, explicit costs of $190 million, and implicit costs of $30

million, its economic profit is:

a.

$200 million.

b.

$70 million.

c.

$10 million.

d.

−$10 million.

e.

−$20 million.

27. A firm has $200 million in total revenue and explicit costs of $190 million. Suppose its owners have

invested $100 million in the company at an opportunity cost of 10 percent interest rate per year. The

firm’s economic profit is:

a.

$400 million.

c.

$80 million.

b.

$100 million.

d.

zero.

28. Economic profit is:

a.

always less than zero.

b.

never less than accounting profit.

c.

less than accounting profit if implicit costs are zero.

d.

less than accounting profit if implicit costs are greater than zero.

29. An economist left her $100,000-a-year teaching position to work full-time in her own consulting

business. In the first year, she had total revenue of $200,000 and business expenses of $100,000. She

made a(n):

a.

economic profit.

b.

economic loss.

c.

implicit profit.

d.

accounting loss but not an economic loss.

e.

zero economic profit.

30. Economic profit equals accounting profit minus:

a.

explicit costs.

c.

fixed costs.

b.

implicit costs.

d.

variable costs.

31. An economist left his $100,000-a-year teaching position to work full-time in his own consulting

business. In the first year, he had total revenue of $200,000 and business expenses of $150,000. He

made a(n):

a.

implicit profit.

b.

economic loss.

c.

economic profit.

d.

accounting loss but not an economic loss.

e.

zero economic profit.

32. A firm has $200 million in total revenue and explicit costs of $190 million. If its owners have invested

$100 million in the company at an opportunity cost of 10 percent interest per year, the firm’s

accounting profit is:

a.

$400 million.

b.

$100 million.

c.

$80 million.

d.

$10 million.

e.

zero.

33. Suppose a firm has total revenue of $200 million, explicit costs of $190 million, and implicit costs of

$20 million. This firm’s accounting profit is:

a.

$80 million.

c.

$10 million.

b.

$70 million.

d.

−$10 million.

34. When total revenue minus total cost is equal to zero, the firm is:

a.

earning above-average economic profit.

b.

earning a normal profit.

c.

losing too much money to stay in business.

d.

earning abnormally low profits.

35. Normal profit is a term for:

a.

explicit profit.

b.

the minimum profit to keep a firm in operation.

c.

the accounting profit forgone.

d.

pure economic profit.

36. Normal profit is defined as a(n):

a.

foregone percent rate of return.

b.

opportunity profit.

c.

implicit profit.

d.

minimum necessary to keep a firm in operation.

37. Economists say that a firm has a normal profit when:

a.

it earns a return of at least 10 percent.

c.

it can pay all its variable costs.

b.

its accounting profit is positive.

d.

its economic profit is zero.

38. Which of the following is an example of a fixed input?

a.

The acreage of a farmer’s land.

c.

The size of a firm’s plant.

b.

Machinery.

d.

All of these.

39. Variable inputs are defined as any resource that:

a.

varies with the size of the firm’s plant.

c.

can be changed as output changes.

b.

cannot be changed as output changes.

d.

can be increased or decreased hourly.

40. Which of the following represents the key difference between the short run and the long run?

a.

In the long run, the firm makes commitments to a certain type of production technology

which are represented as fixed costs in the long run. For example, they have signed a lease

on a particular production facility. These fixed costs do not exist in the short run.

b.

In the short run, the firm makes commitments to a certain type of production technology,

which are represented as fixed costs in the short run. For example, they have signed a lease

on a particular production facility. These fixed costs do not exist in the long run.

c.

The short run refers to less than two years and the long run in over two years.

d.

None of the above are correct.

41. During the short-run period of the production process, a firm will be:

a.

unable to vary any of its factors of production.

b.

able to vary some of its factors of production.

c.

able to vary all of its factors of production.

d.

able to vary the size of its plant.

42. The short run is a time period such that:

a.

the existing firms in the market do not have sufficient time to change the amounts of any

of the inputs that they employ.

b.

the existing firms in the market do not have sufficient time to either increase or decrease

their current rate of output.

c.

the existing firms in the market do not have sufficient time to increase the size of their

existing plant or build a new factory.

d.

new firms may build plants and enter the industry.

43. The short run is a period of time:

a.

in which a firm uses at least one fixed input.

b.

that is long enough to permit changes in the firm’s plant size.

c.

in which production occurs within one year.

d.

in which production occurs within six months.

44. During the course of a week, McDonald’s has enough time to hire or layoff workers, but it does not

have enough time to expand its kitchen or add an additional seating area. In this situation, McDonald’s:

a.

has no fixed costs.

c.

suffers an economic loss.

b.

is in the short run.

d.

earns a large profit.

45. During the short run, a firm has enough time to adjust:

a.

its technology.

b.

its fixed inputs.

c.

its variable inputs.

d.

all of its inputs⎯both fixed and variable.

46. Which of the following factors of production is not variable in the long run?

a.

the size of the firm’s plant.

b.

property taxes on the assets of the firm.

c.

highly trained labor.

d.

All factors of production are variable in the long run.

47. The long run is a period of:

a.

at least one year.

b.

sufficient length to allow a firm to expand output by hiring additional workers.

c.

sufficient length to allow a firm to alter its plant size and capacity and all other factors of

production.

d.

sufficient length to allow a firm to transform economic losses into economic profits by

hiring better workers.

48. The long run is a period of time:

a.

that is too short to change the size of a firm’s plant.

b.

that is long enough to permit changes in all the firm’s inputs, both fixed and variable.

c.

in which production occurs beyond one year.

d.

in which production occurs beyond five years.

49. The long run is a planning period:

a.

during which the firm can vary all inputs including its plant size.

b.

less than six months.

c.

less than one year.

d.

less than five years.

50. In the long run, total fixed cost:

a.

falls.

c.

is constant.

b.

rises.

d.

does not exist.

51. Which of the following statements is true?

a.

Economic profit equals accounting profit minus implicit costs.

b.

The short run is any period of time in which there is at least one fixed input.

c.

A fixed input is any resource for which the quantity cannot change during the period under

consideration.

d.

In the long run there are no fixed costs.

e.

All of these.

52. The increase in total output that results from a unit increase in one unit of a variable input is equal to

the input’s:

a.

total product.

c.

average product.

b.

marginal product.

d.

marginal cost.

53. Which of the following best describes a production function?

a.

The relationship between consumer preferences and market demand.

b.

The relationship between the quantity of labor employed and total cost.

c.

The relationship between the maximum amounts of output a firm can produce and various

quantities of inputs.

d.

The relationship between price and quantity supplied by sellers in a market.

54. If two workers can produce 22 units of output, and the addition of a third worker increases output to 30

units, the marginal product of the third worker is:

a.

8 units.

c.

22 units.

b.

10 units.

d.

30 units.

55. A firm can produce 450 gallons of milk per day with 4 workers and 500 gallons per day with 5

workers. The marginal product of the fifth worker expressed in gallons per worker per day, is:

a.

35.

c.

70.

b.

50.

d.

350.

56. A farm is able to produce 9,000 pints of strawberries per season on 10 acres. It adds one more acre and

is able to produce 12,000 pints per season. The marginal product of land for this farm is:

a.

900 pints per acre per year.

c.

3,000 pints per acre per year.

b.

1,000 pints per acre per year.

d.

12,000 pints per acre per year.

57. If the units of variable input in a production process are 1, 2, 3, 4, and 5, and the corresponding total

outputs are 30, 34, 37, 39, and 40, respectively. The marginal product of the fourth unit is:

a.

2.

c.

37.

b.

1.

d.

39.

58. A farm is able to produce 5,000 bushels of peaches per season on 100 acres. Assume it adds one more

acre and is able to produce 6,000 bushels per season. The marginal product of the additional acre of

land for this farm is:

a.

6,000 bushels per acre per year.

c.

1,000 bushels per acre per year.

b.

5,000 bushels per acre per year.

d.

11,000 bushels per acre per year.

59. A farm is able to produce 10,000 bushels of peanuts per season on 10 acres. Assume it adds one more

acre and is able to produce 12,000 bushels per season. The marginal product of the additional acre of

land for this farm is:

a.

10,000 bushels per acre per year.

c.

2,000 bushels per acre per year.

b.

1,200 bushels per acre per year.

d.

12,000 bushels per acre per year.

60. A farm can produce 10,000 bushels of wheat per year with 5 workers and 13,000 bushels with 6

workers. The marginal product of the sixth worker for this farm is:

a.

10,000 bushels.

c.

500 bushels.

b.

3,000 bushels.

d.

23,000 bushels.

61. Suppose when a car wash has 2 washing stations and 5 workers and is able to wash 100 cars per day.

When it adds a third station, but no more workers, it is able to wash 150 cars per day. The marginal

product of the third washing station is:

a.

100 cars per day.

c.

5 cars per day.

b.

150 cars per day.

d.

50 cars per day.

62. Marginal product measures the change in:

a.

total cost brought about by changing production by one unit.

b.

product price brought about by changing production by one unit.

c.

a firm’s revenue brought about by changing production by one unit.

d.

the firm’s output brought about by employing one additional unit of input.

e.

the firm’s profit brought about by employing one more input.

63. When a total output curve is falling, its corresponding marginal product curve is:

a.

vertical.

c.

rising.

b.

horizontal.

d.

falling.

Exhibit 7-1 Production of pizza data

Workers

Pizzas

0

0

1

4

2

10

3

15

4

18

5

19

64. Exhibit 7-1 shows the change in the production of pizzas as more workers are hired. The marginal

product of the second employee equals:

a.

4.

b.

10.

c.

14.

d.

6.

e.

15.

65. Exhibit 7-1 shows the change in the production of pizzas as more workers are hired. The marginal

product of the fifth employee equals:

a.

4.

b.

18.

c.

19.

d.

3.

e.

1.

66. Exhibit 7-1 shows the change in the production of pizzas as more workers are hired. The total output

of pizzas after hiring 4 workers is:

a.

4.

b.

15.

c.

18.

d.

3.

e.

1.

67. Exhibit 7-1 shows the change in the production of pizzas as more workers are hired. The marginal

product of the labor input begins to fall with the employment of the ____ worker.

a.

first

b.

second

c.

third

d.

fourth

e.

fifth

68. Exhibit 7-1 shows the change in the short run production of pizzas as more workers are hired. The

table shows marginal product increasing between the 0 to 2 hired workers. A possible reason for this

increased marginal product is:

a.

increased wages.

b.

increases in plant size.

c.

decreases in fixed cost.

d.

increased division of labor as additional workers are hired.

e.

increased product price.

69. Exhibit 7-1 shows the change in the short-run production of pizzas as more workers are hired. The

table shows the marginal product of the labor input is decreasing with the hiring of the third worker. A

possible reason for this diminishing marginal product is:

a.

decreased wages.

b.

increases in plant size.

c.

decreases in fixed cost.

d.

increased division of labor as additional workers are hired.

e.

decreases in labor productivity.

Exhibit 7-2 Cost schedule for pizza production

Pizzas

Labor

Cost

Energy

Cost

Materials

Cost

0

$10

$ 0

$ 0

1

10

12

4

2

24

22

8

3

40

30

12

4

60

36

16

5

90

40

20

70. Exhibit 7-2 shows the labor, energy, and materials cost of making various quantities of pizzas. The

table shows that the labor cost of making pizzas will:

a.

increase at a decreasing rate.

b.

decrease at a decreasing rate.

c.

decrease at an increasing rate.

d.

increase at an increasing rate.

e.

increase at a constant rate.

71. Exhibit 7-2 shows the labor, energy, and materials cost of making various quantities of pizzas. The

table shows that the energy cost of making pizzas will:

a.

increase at a decreasing rate.

b.

decrease at a decreasing rate.

c.

decrease at an increasing rate.

d.

increase at an increasing rate.

e.

increase at a constant rate.

72. Exhibit 7-2 shows the labor, energy, and materials cost of making various quantities of pizzas. The

table shows that the materials cost of making pizzas will:

a.

increase at a decreasing rate.

b.

decrease at a decreasing rate.

c.

decrease at an increasing rate.

d.

increase at an increasing rate.

e.

increase at a constant rate.

73. In the short run, a firm will eventually experience rising per-unit costs because of:

a.

economies of scale.

c.

the law of supply.

b.

diseconomies of scale.

d.

the law of diminishing returns.

74. Which of the following best describes the law of diminishing returns?

a.

The principle that beyond some point the marginal product decreases as additional units of

a variable factor (ex: labor) are added to a fixed factor (ex: a restaurant kitchen).

b.

The concept that as a person consumes more and more of a good, such as pizza slices, that

the marginal utility from each additional slice will decline.

c.

The empirical fact that the profitability of firms declines in the long run due to increasing

competition.

d.

None of the above.

75. Which of the following is an implication of the law of diminishing returns?

a.

Total output will decline as more workers are hired.

b.

In the long run, average total cost will eventually decline as output is expanded.

c.

In the short run, expansion of output will eventually lead to increases in marginal cost and

average total cost.

d.

A doubling of all inputs will lead to more than a doubling of output.

76. Bill lives in Montana and likes to grow zucchini. He applies fertilizer to his crops twice during the

growing season and notices that the second layer of fertilizer increases his crop, but not as much as the

first layer. What economic concept best explains this observation?

a.

The law of diminishing marginal utility.

b.

The law of diminishing returns.

c.

Return equalization principle.

d.

The principal-agent problem.

77. The law of diminishing marginal returns implies that, in the short run:

a.

output must fall beyond a certain point.

b.

price must fall beyond a certain point.

c.

the marginal product of the variable input must eventually decrease.

d.

wages of workers must eventually increase.

e.

total cost must fall beyond a certain point.

78. In order for the law of diminishing returns to be present, we must have:

a.

at least one factor of production to be fixed.

b.

output decreasing as more laborers are hired.

c.

the price of labor increasing as more workers are hired.

d.

simultaneous changes in labor and capital.

e.

double the output when labor input is doubled.

79. Applying a price of labor to the law of diminishing returns generates:

a.

the law of increasing costs.

b.

less output as more labor is hired.

c.

differences in the quality of labor.

d.

a negatively-sloped labor supply curve.

e.

specialization and the division of labor.

80. As a fishing firm hires its first, second, and third workers, it could find that marginal product actually

rises. The reason for this is:

a.

diminishing returns have set in.

b.

the division of labor creates greater productivity.

c.

the firm has hired another boat.

d.

all tasks are shared by all workers.

e.

less qualified workers are becoming available.

81. The law of diminishing returns applies to which of the following segments of the marginal product of

labor curve?

a.

The entire curve.

c.

The upward sloping segment only.

b.

The downward-sloping segment only.

d.

The point where labor input is zero.

82. The situation in which the marginal product of labor is greater than zero and declining as more labor is

hired is called the law of:

a.

negative response.

c.

diminishing returns.

b.

inverse return to labor.

d.

demand.

83. If a firm’s use of labor obeys the law of diminishing returns, then:

a.

it does not have enough time to hire or fire workers.

b.

doubling the number of workers causes the firm’s output to also double.

c.

its marginal costs must be falling.

d.

hiring additional workers adds less and less additional output.

84. The ____ is the situation in which the marginal product of labor is greater than zero and declining as

more labor is hired.

a.

law of demand

c.

law of diminishing returns

b.

law of diminishing supply

d.

law of returns to scale

Exhibit 7-3 A marginal product curve

85. As shown in Exhibit 7-3, the law of diminishing returns applies where there are:

a.

more than 5 workers per day.

c.

more than 3 workers per day.

b.

more than 4 workers per day.

d.

between 0 and 5 workers per day.

86. As shown in Exhibit 7-3, the marginal product of labor for the last worker hired when 2 workers are

employed per day is:

a.

50.

c.

150.

b.

100.

d.

175.

87. As shown in Exhibit 7-3, the marginal product of labor for the last worker hired when 5 workers are

employed per day is:

a.

50.

c.

150.

b.

100.

d.

175.

Exhibit 7-4 A marginal product curve

88. As shown in Exhibit 7-4, the law of diminishing returns applies in the range of:

a.

over 10 workers per day.

c.

over 2 workers per day.

b.

over 5 workers per day.

d.

between 0 and 5 workers per day.

89. As shown in Exhibit 7-4, which of the following conclusions can you draw about the firm’s total

output curve?

a.

It slopes downward throughout the range of 0−10 units of input.

b.

It reaches a maximum at 5 units of output.

c.

It has an inflection point at 5 units of input.

d.

It has zero slope at 5 units of input.

Exhibit 7-5 Workers and output data

Laborers

Total

Product

0

0

1

8

2

20

3

25

4

28

5

29

90. In Exhibit 7-5, diminishing returns set in when the ____ worker is hired.

a.

first

b.

second

c.

third

d.

fourth

e.

fifth

91. In Exhibit 7-5, the marginal product of the second worker is:

a.

0.

b.

8.

c.

10.

d.

12.

e.

20.

92. Paul’s Plumbing is a small business that employs 12 people. Which of the following is most likely to

be a fixed cost for Paul’s Plumbing?

a.

The tax and insurance payments on the property owned by the firm.

b.

The wages paid to the 12 employees.

c.

The payroll taxes on the wages of the 12 employees.

d.

The salary paid to Paul, who is the manager of the firm.

93. Which of the following is true about average fixed cost?

a.

Average fixed cost has a U-shape, and marginal cost crosses average fixed cost at its

minimum point.

b.

Average fixed cost does not vary as output increases.

c.

Average fixed cost is the difference between marginal cost and average total cost.

d.

Average fixed cost is total fixed cost divided by the quantity of output produced, and it

declines steadily as output increases.

94. Fixed costs are best defined as:

a.

costs that do not vary with output.

b.

costs that are at a minimum when output approaches the firm’s capacity.

c.

the amount that one more unit of output adds to total costs.

d.

costs that decline as output increases.

95. Which of the following is most likely to be a fixed cost for a business?

a.

expenditures on low-skill labor.

b.

shipping charges for the delivery of products.

c.

managerial salaries.

d.

property taxes on the firm’s buildings.