57. The general ledger account for Accounts Receivable shows a debit balance of $25,000. Allowance for

Uncollectible Accounts has a credit balance of $1,500. Net sales for the year were $250,000. In the

past, 3 percent of sales have proved uncollectible, and an aging of accounts receivable resulted in an

estimate of $10,000 of uncollectible accounts receivable.

Using the percentage of net sales method, the Allowance for Uncollectible Accounts balance (after

adjustment) would be

a.

$7,500.

b.

$10,000.

c.

$9,000.

d.

$6,000.

58. The general ledger account for Accounts Receivable shows a debit balance of $25,000. Allowance for

Uncollectible Accounts has a credit balance of $1,500. Net sales for the year were $250,000. In the

past, 3 percent of sales have proved uncollectible, and an aging of accounts receivable resulted in an

estimate of $10,000 of uncollectible accounts receivable.

Using the accounts receivable aging method, the entry to record the Uncollectible Accounts Expense

is:

a.

Uncollectible Accounts Expense 10,750

Allowance for Uncollectible Accounts 10,750

b.

Uncollectible Accounts Expense 8,500

Allowance for Uncollectible Accounts 8,500

c.

Uncollectible Accounts Expense 10,000

Allowance for Uncollectible Accounts 10,000

d.

Uncollectible Accounts Expense 11,500

Allowance for Uncollectible Accounts 11,500

59. The general ledger account for Accounts Receivable shows a debit balance of $25,000. Allowance for

Uncollectible Accounts has a credit balance of $1,500. Net sales for the year were $250,000. In the

past, 3 percent of sales have proved uncollectible, and an aging of accounts receivable resulted in an

estimate of $10,000 of uncollectible accounts receivable.

Using the accounts receivable aging method, the Allowance for Uncollectible Accounts balance (after

adjustment) would be

a.

$11,500.

b.

$10,000.

c.

$8,500.

d.

$10,750.

60. You have just received notice that Agnes Fisher, a customer of yours with an Accounts Receivable

balance of $200, has gone bankrupt and will not be making any future payments. Assuming you use

the allowance method, the journal entry you make is to

a.

debit Uncollectible Accounts Expense and credit Accounts Receivable.

b.

debit Allowance for Uncollectible Accounts and credit Uncollectible Accounts Expense.

c.

debit Uncollectible Accounts Expense and credit Allowance for Uncollectible Accounts.

d.

debit Allowance for Uncollectible Accounts and credit Accounts Receivable.

61. Under the direct charge-off method of dealing with uncollectible accounts,

a.

revenues and expenses are properly matched.

b.

Accounts Receivable is shown on the balance sheet at net realizable value.

c.

Uncollectible Accounts Expense is recorded in the period of the sale.

d.

no Allowance for Uncollectible Accounts exists.

62. If the amount of uncollectible accounts expense is understated at year end,

a.

net Accounts Receivable will be understated.

b.

total liabilities will be overstated.

c.

net income will be understated.

d.

Allowance for Uncollectible Accounts will be understated.

63. Each of the following is a characteristic of a promissory note except a(n)

a.

maturity date that can be determined on the date the note is signed.

b.

payee who has an unconditional right to receive a definite amount on a definite date.

c.

maker who agrees to pay a definite sum subject to certain conditions.

d.

amount to be paid that can be determined on the date the note is signed.

64. Which of the following statements is false regarding promissory notes?

a.

They are sometimes used to extend past-due accounts.

b.

They can be resold to banks.

c.

They must be held by the maker until maturity.

d.

They are often received upon the sale of machinery and automobiles.

65. A note receivable dated May 23 and due in 90 days would be due on

a.

August 20.

b.

August 21.

c.

August 23.

d.

August 22.

66. The interest on a three-month, 12 percent, $8,300 note receivable is

a.

$249.

b.

$83.

c.

$166.

d.

$996.

67. The maturity value of a 60-day, 9 percent, $2,000 note receivable is

a.

$1,970.33.

b.

$1,820.89.

c.

$2,029.59.

d.

$2,180.12.

68. Interest on a 90-day, 10 percent, $10,000 note receivable is

a.

$2,500.77.

b.

$288.38.

c.

$246.58.

d.

$1,000.63.

69. Interest on a note receivable may be calculated without knowledge of the

a.

principal amount.

b.

rate of interest.

c.

note’s maturity date.

d.

note’s duration.

70. A promissory note is executed in June. When the note is paid the following January, the payee’s entry

includes (assuming a calendar-year accounting period and no reversing entries) a

a.

debit to Interest Income.

b.

credit to Cash.

c.

credit to Interest Receivable.

d.

debit to Notes Receivable.

71. A dishonored note means the payee’s entry includes a

a.

credit to Accounts Receivable.

b.

debit to Interest Expense.

c.

debit to Notes Receivable.

d.

credit to Interest Income.

72. Cottage Sales Company made most of its sales on credit during its first year of operation, 2010. At the

end of the year, accounts receivable amounted to $100,000. On December 31, 2010, management

reviewed the collectible status of the accounts receivable. Approximately $6,000 of the $100,000 of

accounts receivable were estimated to be uncollectible. As per the accounts receivable aging method

the adjusting entry that would be made on December 31 of that year is:

a.

Uncollectible Accounts Expense 6,000

Accounts receivable 6,000

b.

Allowance for Uncollectible Accounts 10,000

Uncollectible Accounts Expense 10,000

c.

Uncollectible Accounts Expense 6,000

Allowance for Uncollectible Accounts 6,000

d.

Allowance for Uncollectible Accounts 10,000

Accounts receivable 10,000

73. Assume that the $1,000, 90-day, 8 percent note was received on August 31 and that the fiscal year

ended on September 30. The adjusting entry that would be made to record the interest receivable is

(amounts rounded to nearest dollar):

a.

Interest receivable 7

Interest Income 7

b.

Notes receivable 7

Interest Income 7

c.

Accounts receivable 20

Cash 20

d.

Interest income 20

Accounts receivable 20

74. Assume that on December 1, a $3,000, 90-day, 10 percent note receivable was received from a

customer as an extension of his of past – due account. The entry that would be made to record the note

is:

a.

Notes receivable 3,000

Cash 3,000

b.

Notes receivable 3,000

Interest Income account 3,000

c.

Notes receivable 3,000

Accounts receivable 3,000

d.

Cash 3,000

Accounts receivable 3,000

75. Assume that on December 1, a note which has a face value of $9,000, bears interest at 9 percent for

120 days, received from a customer as an extension of his of past – due account is dishonored. The

entry that would be made to record the dishonor (ignoring interest) is:

a.

Notes receivable 9,000

Cash 9,000

b.

Accounts receivable 9,000

Cash 9,000

c.

Accounts receivable 9,000

Notes receivable 9,000

d.

Cash 9,000

Accounts Receivable 9,000

76. Assume that on January 15, a customer who owes Shawni sales company $1,000 is declared bankrupt

by a federal court. The entry that would be made to write off this account is:

a.

Allowance for uncollectible 1,000

Accounts receivable, customer account 1,000

b.

Accounts receivable 1,000

Cash 1,000

c.

Accounts receivable 1,000

Notes receivable 1,000

d.

Cash 1,000

Accounts Receivable 1,000

77. Assume that on December 1, a note which has a face value of $1,000, bears interest at 6 percent for 90

days, received from a customer as an extension of his of past – due account is honored on due date.

The entry that would be made to record the receipt on due date (ignoring interest) is:

a.

Notes receivable 1,000

Cash 1,000

b.

Accounts receivable 1,000

Cash 1,000

c.

Accounts receivable 1,000

Notes receivable 1,000

d.

Cash 1,000

Notes receivable 1,000

SHORT ANSWER

1. What is a contingent liability, and how does it relate to the discounting of a note receivable at the

bank?

2. What purpose is served by a factoring arrangement? What does it mean to factor accounts receivable

with recourse?

3. The following data exist for Conner Company:

2010

2009

Accounts Receivable

$ 80,000

$ 90,000

Sales

510,000

410,500

Calculate the receivable turnover and the average days’ sales uncollected for 2010. Round answers to

one decimal place.

4. Jayne Luke started a computer business in her basement less than a year ago. Her personal attention to

clients and persistence in obtaining new customers has caused the business to grow at a tremendous

pace. Jayne has become so busy she has neglected to keep after clients who have failed to pay her. As

a result, Jayne has a large amount of accounts receivable and notes receivable on her balance sheet but

not much cash. She continues to service clients, but she now realizes that her cash will soon be

exhausted. Suggest some options Jayne has to achieve a strong cash balance.

5. On a balance sheet, what items normally are included in Cash?

6. Why do businesses need to keep some currency on hand?

7. What is a compensating balance? By whom is it required?

8. Compute the correct amount for each letter in the following table:

Case 1

Case 2

Case 3

Case 4

Balance per bank statement

$ a

$17,800

$630

$3,980

Deposits in transit

1,200

b

100

250

Outstanding checks

3,000

2,000

c

150

Balance per books

6,900

18,800

450

d

9. For each of the items below, use the following letters to identify the correct treatment in a bank

reconciliation.

A = Add to balance per bank

C = Add to balance per books

B = Deduct from balance per bank

D = Deduct from balance per books

____ 1. Interest income

____ 2. Outstanding checks

____ 3. Check written for $89, but $98 recorded in books

____ 4. Customer’s NSF check

____ 5. Note receivable collected by bank

____ 6. Deposit made for $70, but $700 recorded in books

____ 7. Bank check-printing charge

____ 8. Check written for $52, but $25 recorded in books

____ 9. Deposits in transit

____ 10. Bank fee for collection on note receivable

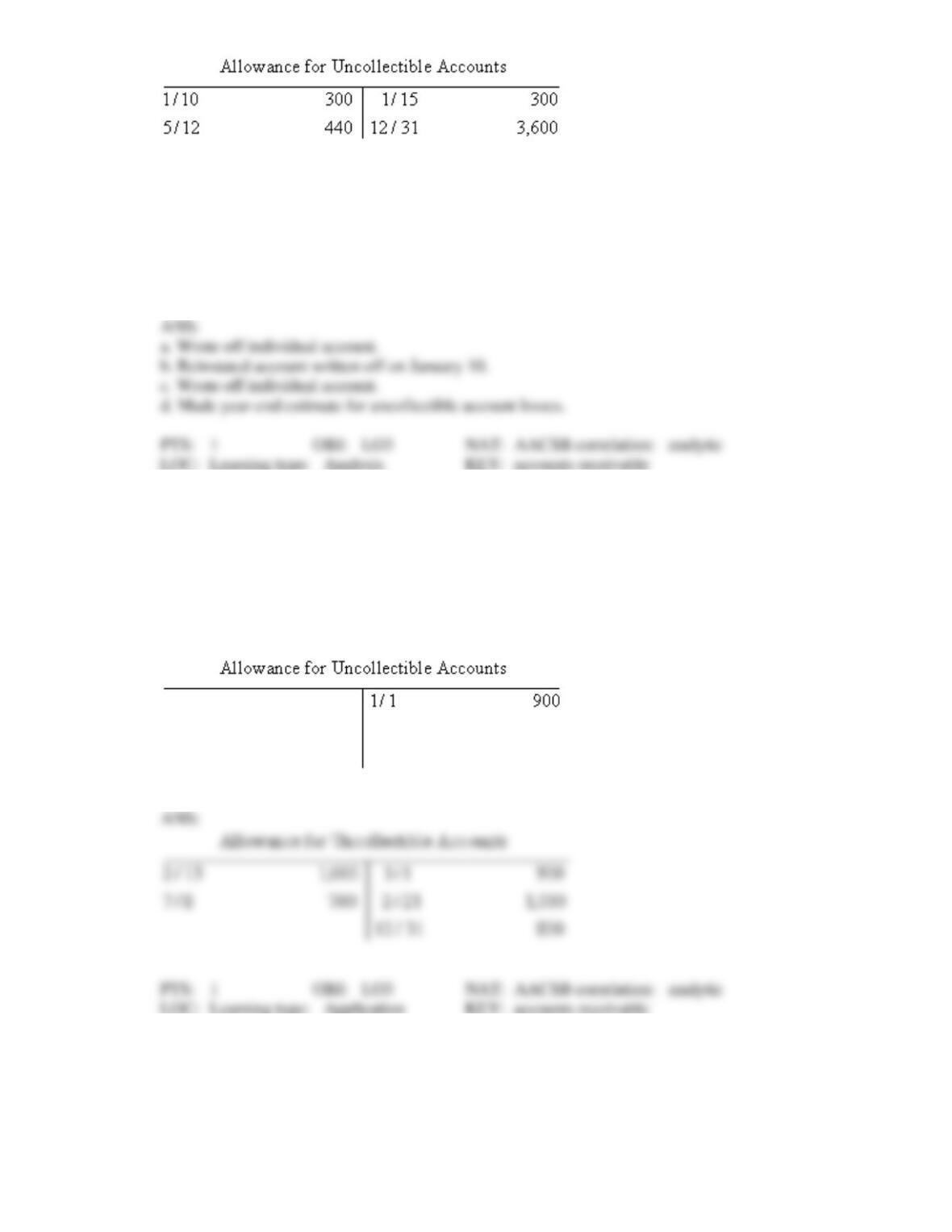

10. Use the following T account to answer the questions below (assume a calendar-year accounting

period).

What apparently occurred on:

a. January 10?

b. January 15?

c. May 12?

d. December 31?

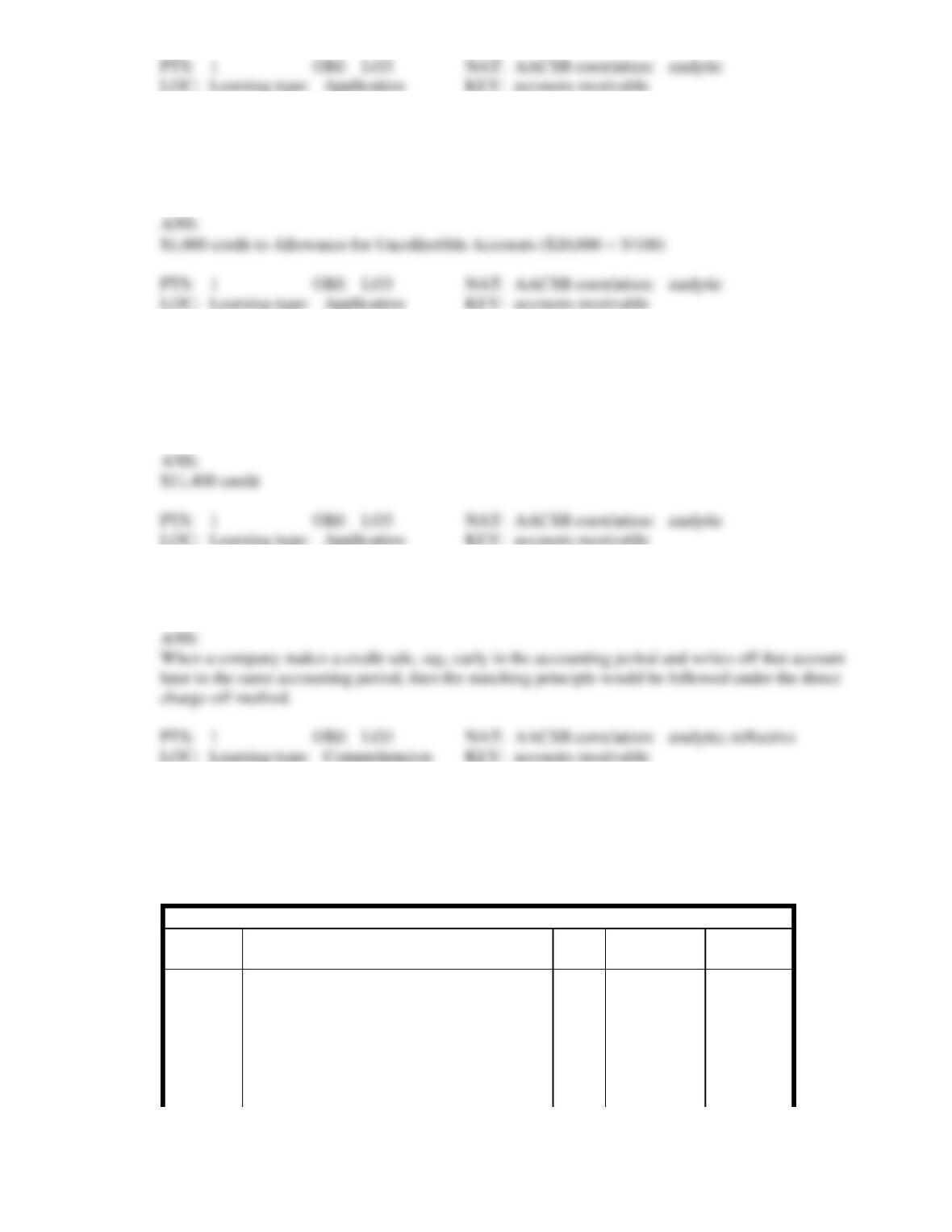

11. Using the following transactions for 2010, show how the T account below would appear after all

appropriate postings have been made. Assume an opening balance of $900.

Feb.

13

Wrote off an individual account for $1,000.

21

Reinstated the account written off on February 13.

July

8

Wrote off an individual account for $700.

Dec.

31

Made year-end adjustment of $800 for estimated uncollectible accounts.

12. Sally’s Dress Shop has $5,200 in Accounts Receivable at December 31. The company’s accountant

estimates that $300 of the $5,200 will never be collected. Complete the current asset section of the

balance sheet below.

Current assets

Cash

$14,000

Short-term investments

4,000

Accounts receivable

Inventory

50,000

Total current assets

$

13. How is the account Allowance for Uncollectible Accounts presented in the financial statements, and

what purpose does this presentation serve?

14. On December 31, Skinner Enterprises has a $400 debit balance in Allowance for Uncollectible

Accounts. If an accounts receivable aging method analysis indicated that an estimated $3,200 of

December 31 receivables are uncollectible, for what amount would the adjusting entry for

uncollectible accounts be recorded? (Show your work.)

15. On December 31, Alsop Products has a $300 credit balance in Allowance for Uncollectible Accounts.

It estimates that 4 percent of the $60,000 in sales are uncollectible. After the appropriate adjusting

entry for uncollectible accounts has been made using percentage of net sales method, what will be the

balance in Allowance for Uncollectible Accounts? Indicate if the balance is a debit or credit. (Show

your work.)

Current assets

Cash

Short-term investments

Accounts receivable

Less allowance for

uncollectible accounts

Inventory

Total current assets

16. At year end, Erwin Graphics has a $350 debit balance in Allowance for Uncollectible Accounts. It

estimates that 5 percent of the $20,000 in sales are uncollectible. Give the amount that should be used

in the adjusting entry using percentage of net sales method to record uncollectible accounts. (Show

your calculations.)

17. At year end, Gorgin Design Company has a $1,800 credit balance in Allowance for Uncollectible

Accounts. If an accounts receiving aging method analysis indicates that an estimated $11,400 of

year-end receivables are uncollectible, what will be the balance in Allowance for Uncollectible

Accounts after the appropriate adjusting entry for uncollectible accounts has been made? Indicate if the

balance is a debit or credit.

18. Under what specific circumstance will application of the direct charge-off method be in accordance

with the matching principle?

19. Assume that part of accounts and other receivables on Thompson Toys’ balance sheet is $16 million as

of February 2, 2010. Also assume that Allowance for Uncollectible Accounts has a credit balance of

$550,000 and that Thompson estimates its uncollectible accounts as 0.1 percent of net sales and the

sales for the year is $11,019,000,000. Record the adjusting entry to recognize uncollectible accounts

using the percentage of net sales method. Omit explanations.

General Journal

Page 1

Date

Description

Post.

Ref.

Debit

Credit